Global Commercial Air Brake Market

Market Size in USD Billion

USD

13.72 Billion

USD

17.33 Billion

2025

2033

USD

13.72 Billion

USD

17.33 Billion

2025

2033

| 2026 - 2033 | |

| USD 13.72 Billion | |

| USD 17.33 Billion | |

| % | |

|

Commercial Air Brake Market Overview

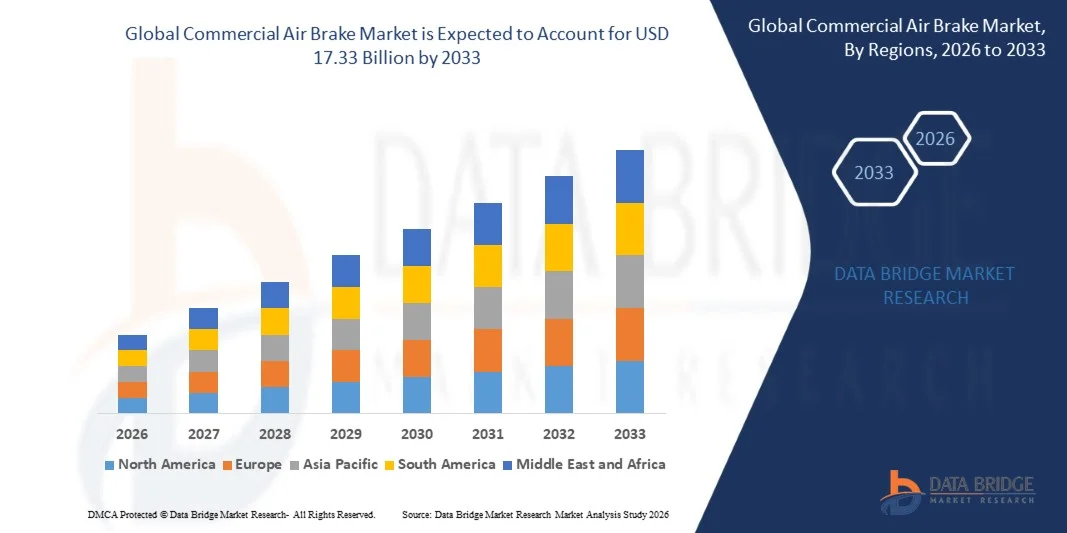

As per Data Bridge Market Research analysis the Commercial Air Brake Market was valued at USD 13.72 billion in 2025 and is projected to reach USD 17.33 billion by 2033, growing at a CAGR of 2.97% from 2026 to 2033. The market is witnessing steady growth driven by increasing production of heavy commercial vehicles, stringent government regulations regarding vehicle safety and braking performance, and rising investments in freight transportation and logistics infrastructure.

The growing demand for reliable braking systems in trucks, buses, trailers, and other heavy-duty commercial vehicles, combined with the expansion of long-haul transportation and construction activities, is accelerating the adoption of advanced air brake technologies. Manufacturers are increasingly integrating electronic braking systems (EBS), anti-lock braking systems (ABS), and lightweight, corrosion-resistant components to improve braking efficiency, vehicle stability, and operational safety while meeting evolving regulatory standards and reducing maintenance costs.

Market Size & Forecast

- Global Market Value (2025): USD 13.72 Billion

- Expected Market Value (2033): USD 17.33 Billion

- Forecast CAGR (2026–2033): 2.97%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America dominated the commercial air brake market with the largest revenue share of approximately 45% in 2025, supported by stringent commercial vehicle safety regulations, a well-established freight transportation network, and the presence of leading air brake manufacturers.

- Asia-Pacific commercial air brake market holding approximately 20% of the global market share and is expected to witness the fastest growth from 2026 to 2033, supported by rapid industrialization, expanding logistics infrastructure, rising commercial vehicle production, and increasing government investments in road transportation networks.

- The compressor segment held the largest market revenue share in 2025. Compressors serve as the core of air brake systems by generating compressed air required for braking operations, making them indispensable across trucks, buses, and trailers. Rising production of heavy commercial vehicles, coupled with increasing adoption of electronically controlled braking systems requiring high-performance compressed air supply, continues to support segment dominance. Public market studies also identify compressors as the leading component within the air brake system market.

- The brake chamber segment is projected to register the fastest growth from 2026 to 2033, driven by increasing integration of lightweight diaphragm brake chambers, higher replacement demand in aging commercial fleets, and expanding deployment of advanced braking systems in heavy-duty trucks. Growing emphasis on improved braking response and reduced maintenance requirements is expected to accelerate adoption across OEM and aftermarket channels.

- The disc brakes held the largest market revenue share in 2025, driven by increasing adoption in heavy-duty trucks and buses due to superior heat dissipation, shorter stopping distances, reduced brake fade, and lower maintenance requirements compared to conventional drum brakes. Growing integration with electronically controlled braking systems (EBS), anti-lock braking systems (ABS), and advanced driver assistance systems (ADAS) further supported segment dominance.

- The drum brakes segment is projected to register the fastest growth from 2026 to 2033 owing to its extensive deployment in heavy-duty trucks, buses, and trailers because of its durability, lower acquisition cost, and ability to withstand high-load commercial transportation applications. Industry analyses continue to indicate drum brakes as the leading brake configuration across commercial air brake systems.

Report Scope and Commercial Air Brake Market Segmentation

|

Attributes |

Commercial Air Brake Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Commercial Air Brake Market Trends

Trend: Increasing Adoption Of Electronically Controlled And Intelligent Air Braking Systems

Growing emphasis on commercial vehicle safety, regulatory compliance, and fleet operational efficiency is accelerating the transition from conventional pneumatic braking systems to electronically controlled air brake technologies across heavy-duty trucks, buses, and trailers. Traditional air brake systems rely heavily on mechanical actuation and longer response times, while electronically controlled air brake systems provide faster brake response, improved vehicle stability, shorter stopping distances, and enhanced integration with advanced driver assistance systems (ADAS).

In modern commercial vehicles, manufacturers are integrating electronically controlled braking systems, for instance ZF's modular Brake System Platform (mBSP XBS), which entered series production with major European OEMs in 2024, combines centralized electronic brake control with ADAS to improve braking response and vehicle stability. Trailer manufacturers are also deploying intelligent Electronic Braking Systems (EBS) equipped with tire pressure monitoring and cloud-enabled diagnostics that continuously monitor brake performance and system health, improving fleet uptime and reducing maintenance requirements.

The rapid deployment of connected commercial vehicles and autonomous driving technologies is further increasing demand for intelligent air brake systems capable of communicating with collision mitigation, adaptive cruise control, and electronic stability control technologies. In addition, implementation of the European Union's General Safety Regulation (GSR II) from July 2024 has accelerated adoption of advanced braking and safety technologies across newly registered heavy commercial vehicles. Knorr-Bremse also announced in 2024 that it would become the first manufacturer to mass produce an Electronic Braking System (EBS) in the U.S., highlighting growing industry adoption of electronically controlled commercial braking platforms.

Commercial Air Brake Market Dynamics

Key Market Driver: Rising Implementation Of Advanced Commercial Vehicle Safety Regulations

Governments worldwide are strengthening commercial vehicle safety regulations to reduce road accidents, improve freight transportation safety, and enhance fleet operational efficiency. Increasing logistics activity, expanding heavy-duty vehicle production, and mandatory safety requirements are encouraging fleet operators and OEMs to replace conventional pneumatic brake systems with electronically controlled air brake technologies offering improved braking performance, reliability, and regulatory compliance.

Commercial vehicle manufacturers are increasingly deploying advanced air braking systems, for instance Bendix Commercial Vehicle Systems is accelerating the adoption of Electropneumatic Braking Systems (EBS) across North America, highlighting EBS as the foundation for future ADAS, automated driving functions, and electric commercial vehicles. Similarly, ZF's mBSP XBS platform enables scalable brake control from ABS to full EBS while supporting automation up to SAE Level 5, helping manufacturers comply with evolving global safety standards.

Similarly, increasing regulatory focus on collision avoidance and advanced driver assistance technologies is driving investment in intelligent braking platforms across Europe and North America. The European General Safety Regulation (GSR II), effective from July 2024, requires multiple advanced safety technologies for newly approved heavy commercial vehicles, significantly accelerating deployment of electronically controlled braking systems throughout the commercial vehicle industry.

Key Restraint/Challenge: High Maintenance Requirements And Rising System Complexity

Modern commercial air brake systems incorporate electronic control units, sensors, pneumatic valves, compressors, and software-controlled braking modules that require regular inspection, calibration, and specialized maintenance to maintain optimal braking performance. Failure to properly maintain these systems can reduce braking efficiency, increase vehicle downtime, and raise operating costs for fleet operators.

In addition, electronically controlled braking systems require specialized diagnostic equipment and trained technicians, increasing maintenance expenditure compared with conventional pneumatic braking systems. Small fleet operators and transportation companies in cost-sensitive markets often face affordability challenges due to higher initial installation costs and ongoing maintenance requirements. The increasing integration of ADAS and electronic brake controls also adds software validation and cybersecurity requirements, further increasing system complexity.

Commercial vehicle manufacturers acknowledge that the migration from conventional air brakes to fully electronic braking architectures requires significant investments in service infrastructure, technician training, and digital diagnostics before fleets can fully benefit from intelligent braking technologies.

Key Market Opportunity: Expansion Of Connected Commercial Vehicles And Autonomous Driving Technologies

Growing deployment of connected commercial vehicles, autonomous driving technologies, and intelligent transportation systems is creating significant opportunities for advanced commercial air brake manufacturers. Modern heavy-duty vehicles increasingly require integrated braking systems capable of communicating with advanced driver assistance systems, telematics platforms, and autonomous vehicle control architectures to improve operational safety and fleet efficiency.

Commercial vehicle manufacturers are increasingly integrating intelligent air braking technologies, for instance ZF's mBSP XBS braking platform supports centralized electronic control, over-the-air software capability, and automation-ready architecture, enabling seamless integration with autonomous driving systems. Similarly, Bendix identifies Electropneumatic Braking Systems (EBS) as the enabling platform for future ADAS functions and highly automated commercial vehicles in North America.

In addition, increasing investments in connected freight transportation, digital fleet management, and autonomous logistics are accelerating demand for intelligent braking technologies capable of supporting predictive maintenance and real-time vehicle diagnostics. Knorr-Bremse continues expanding its digital commercial vehicle portfolio by integrating braking systems with connected vehicle technologies designed to improve fleet safety, operational efficiency, and automated vehicle functionality across global commercial vehicle markets.

Commercial Air Brake Market Scope

The market is segmented on the basis of component, brake type, on-highway vehicle type, end use, and distribution channel.

- By Component

On the basis of component, the commercial air brake market is segmented into compressor, reservoir, foot valve, brake chamber, and others. The compressor segment held the largest market revenue share in 2025. Compressors serve as the core of air brake systems by generating compressed air required for braking operations, making them indispensable across trucks, buses, and trailers. Rising production of heavy commercial vehicles, coupled with increasing adoption of electronically controlled braking systems requiring high-performance compressed air supply, continues to support segment dominance. Public market studies also identify compressors as the leading component within the air brake system market.

The brake chamber segment is projected to register the fastest growth from 2026 to 2033, driven by increasing integration of lightweight diaphragm brake chambers, higher replacement demand in aging commercial fleets, and expanding deployment of advanced braking systems in heavy-duty trucks. Growing emphasis on improved braking response and reduced maintenance requirements is expected to accelerate adoption across OEM and aftermarket channels.

- By Brake Type

On the basis of brake type, the commercial air brake market is segmented into disc brakes, controlled brake, and drum brakes. The disc brakes held the largest market revenue share in 2025, driven by increasing adoption in heavy-duty trucks and buses due to superior heat dissipation, shorter stopping distances, reduced brake fade, and lower maintenance requirements compared to conventional drum brakes. Growing integration with electronically controlled braking systems (EBS), anti-lock braking systems (ABS), and advanced driver assistance systems (ADAS) further supported segment dominance.

The drum brakes segment is projected to register the fastest growth from 2026 to 2033 owing to its extensive deployment in heavy-duty trucks, buses, and trailers because of its durability, lower acquisition cost, and ability to withstand high-load commercial transportation applications. Industry analyses continue to indicate drum brakes as the leading brake configuration across commercial air brake systems.

- By On-Highway Vehicle Type

On the basis of on-highway vehicle type, the commercial air brake market is segmented into rigid body, heavy-duty truck, semi-trailer, and bus. The heavy-duty truck segment held the largest market revenue share in 2025 driven by growing freight transportation activities, expanding logistics networks, and mandatory installation of air braking systems in high-load commercial vehicles. Increasing cross-border freight movement and fleet expansion continue to strengthen demand for advanced air brake technologies in this segment.

The bus segment is projected to register the fastest growth from 2026 to 2033, supported by increasing investments in public transportation infrastructure, rising procurement of electric and low-emission buses, and stringent passenger safety regulations requiring advanced air braking technologies. Expanding urbanization and government initiatives to modernize mass transit fleets are further accelerating segment growth.

- By End Use

On the basis of end use, the commercial air brake market is segmented into logistics, public transportation, construction, and mining. The logistics segment held the largest market revenue share in 2025 due to increasing commercial freight movement, rapid expansion of e-commerce supply chains, and continuous fleet modernization by logistics operators. Growing demand for safe, efficient, and reliable heavy-duty transportation continues to support widespread adoption of advanced air brake systems.

The public transportation segment is projected to register the fastest growth from 2026 to 2033, driven by rising investments in sustainable urban mobility, expanding bus rapid transit (BRT) networks, increasing adoption of electric and hybrid buses, and stringent safety regulations promoting advanced electronically controlled air braking systems across municipal transit fleets.

- By Distribution Channel

On the basis of distribution channel, the commercial air brake market is segmented into OEM and aftermarket. The OEM segment held the largest market revenue share of approximately 67.5% in 2025, driven by strong production of commercial vehicles and factory installation of advanced air braking technologies, including electronically controlled braking systems. Increasing regulatory requirements and integration of safety technologies at the manufacturing stage continue to reinforce OEM dominance.

The aftermarket segment is projected to register the fastest growth at a CAGR of approximately 9.9% through the forecast period, driven by the growing global commercial vehicle parc, increasing replacement demand for brake components, and rising maintenance requirements associated with electronically controlled air brake systems. Aging vehicle fleets and predictive maintenance practices are further supporting segment expansion.

Commercial Air Brake Market Regional Analysis

North America Commercial Air Brake Market Insight

North America dominated the commercial air brake market with the largest revenue share of approximately 45% in 2025, supported by stringent commercial vehicle safety regulations, a well-established freight transportation network, and the presence of leading air brake manufacturers. The region benefits from high production and sales of heavy-duty trucks and trailers, increasing adoption of electronically controlled braking systems (EBS), and continuous fleet modernization initiatives. Growing investments in connected commercial vehicles, advanced driver assistance systems (ADAS), and predictive fleet maintenance further strengthen demand for advanced commercial air brake systems across logistics, construction, and public transportation sectors.

U.S. Commercial Air Brake Market Insight

The U.S. commercial air brake market captured the largest revenue share in 2025 within North America, fueled by expanding freight transportation, increasing production of Class 8 trucks, and stringent safety standards established by federal transportation authorities. Fleet operators are increasingly adopting electronically controlled air brake systems, anti-lock braking systems (ABS), and connected braking technologies to improve vehicle safety, operational efficiency, and regulatory compliance. The growing deployment of autonomous trucking technologies and smart fleet management platforms is further supporting market expansion.

Canada Commercial Air Brake Market Insight

The Canada commercial air brake market is expected to witness significant growth from 2026 to 2033, driven by expanding freight transportation, increasing investments in commercial fleet modernization, and stringent vehicle safety regulations governing heavy-duty trucks and trailers. Rising cross-border trade with the U.S., coupled with growing adoption of electronically controlled braking systems (EBS), anti-lock braking systems (ABS), and connected fleet management technologies, is accelerating demand for advanced commercial air brake systems. Moreover, increasing infrastructure development, mining activities, and replacement demand for aging commercial vehicle fleets are further supporting market growth across the country.

Europe Commercial Air Brake Market Insight

The Europe is the second-largest market for commercial air brakes, accounting for approximately 30% in 2025, primarily driven by stringent vehicle safety regulations, rapid adoption of intelligent braking technologies, and increasing investments in sustainable commercial transportation. The implementation of the European Union's General Safety Regulation (GSR II) is encouraging manufacturers to integrate advanced braking systems with electronic stability control and ADAS. Increasing replacement of aging commercial fleets and growing demand for connected heavy-duty vehicles continue to support regional market growth.

U.K. Commercial Air Brake Market Insight

The U.K. commercial air brake market is expected to witness notable growth from 2026 to 2033, driven by expanding logistics activities, increasing investments in public transportation, and growing adoption of advanced commercial vehicle safety technologies. Fleet operators are focusing on reducing maintenance costs and improving operational efficiency through predictive maintenance solutions and electronically controlled braking systems. The ongoing transition toward connected and low-emission commercial vehicles is expected to further accelerate market demand.

Germany Commercial Air Brake Market Insight

The Germany commercial air brake market accounted for the largest revenue share in Europe in 2025, supported by the country's strong commercial vehicle manufacturing base and the presence of major braking system manufacturers such as Knorr-Bremse and ZF. Increasing production of heavy-duty trucks, continuous technological advancements in electronic braking systems, and growing investments in autonomous and connected commercial vehicles continue to drive market expansion. Strong regulatory compliance requirements further encourage widespread adoption of intelligent air brake technologies.

Asia-Pacific Commercial Air Brake Market Insight

The Asia-Pacific commercial air brake market holding approximately 20% of the global market share and is expected to witness the fastest growth from 2026 to 2033, supported by rapid industrialization, expanding logistics infrastructure, rising commercial vehicle production, and increasing government investments in road transportation networks. Growing demand for heavy-duty trucks and buses across developing economies, coupled with stricter commercial vehicle safety regulations, is accelerating the adoption of advanced air braking systems. The expanding manufacturing presence of global and regional OEMs further contributes to market growth across the region.

Japan Commercial Air Brake Market Insight

The Japan commercial air brake market is expected to witness significant growth from 2026 to 2033 due to increasing adoption of intelligent transportation systems, advanced commercial vehicle technologies, and connected fleet management solutions. Commercial vehicle manufacturers are integrating electronically controlled braking systems to improve operational safety, vehicle stability, and fuel efficiency. Rising investments in autonomous driving technologies and next-generation logistics infrastructure are further supporting market development.

China Commercial Air Brake Market Insight

The China commercial air brake market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country's position as the world's largest commercial vehicle producer, rapid expansion of logistics and e-commerce industries, and substantial investments in transportation infrastructure. Increasing production of heavy-duty trucks, implementation of stricter vehicle safety regulations, and growing adoption of electronically controlled braking systems by domestic manufacturers are accelerating market growth. Rising exports of commercial vehicles and continuous fleet modernization initiatives further strengthen China's leadership in the regional market.

Commercial Air Brake Market Share

The Commercial Air Brake industry is primarily led by well-established companies, including:

- Knorr-Bremse AG (Germany)

- ZF Friedrichshafen AG (Germany)

- Wabtec Corporation (U.S.)

- Meritor, Inc. (U.S.)

- Haldex AB (Sweden)

- Nabtesco Automotive Corporation (Japan)

- Tenneco Inc. (U.S.)

- Brakes India Private Limited (India)

- UNO Minda Limited (India)

- ANAND Group (India)

- SORL Auto Parts, Inc. (China)

- TSE Brakes Inc. (Canada)

- Fricción y Tecnología, S.A. de C.V. (Mexico)

- Airmaster Brake Systems (Turkey)

- Yumak Air Brake Systems (Turkey)

Latest Developments in Commercial Air Brake Market

- In August 2026, Knorr-Bremse AG, Strategic Partnership, Knorr-Bremse announced a strategic partnership with a leading electric commercial vehicle manufacturer to develop next-generation braking systems specifically designed for electric trucks and buses. The collaboration aims to enhance braking efficiency, energy recovery, and vehicle safety while supporting the growing adoption of zero-emission commercial vehicles. This partnership strengthens Knorr-Bremse's position in sustainable mobility and is expected to accelerate innovation in the Commercial Air Brake Market.

- In September 2025, WABCO, Product Launch, WABCO unveiled a new generation of AI-enabled smart air brake systems capable of optimizing braking performance in real time through advanced electronic controls and predictive diagnostics. The solution is designed to improve vehicle safety, reduce maintenance requirements, and enhance fleet operational efficiency. This development reinforces the industry's transition toward intelligent, connected braking technologies and strengthens WABCO's competitive position in the market.

- In July 2024, Bendix Commercial Vehicle Systems, Capacity Expansion, Bendix Commercial Vehicle Systems expanded its manufacturing operations in North America to increase production of advanced commercial air brake components. The expansion is intended to strengthen supply chain resilience, improve production efficiency, and meet rising demand from OEMs and aftermarket customers. This investment enhances Bendix's manufacturing capabilities while supporting the growing adoption of advanced commercial air brake systems across North America.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.