Global Communication Surveillance Market

Market Size in USD Billion

USD

4.95 Billion

USD

11.65 Billion

2025

2033

USD

4.95 Billion

USD

11.65 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.95 Billion | |

| USD 11.65 Billion | |

| % | |

|

Communication Surveillance Market Overview

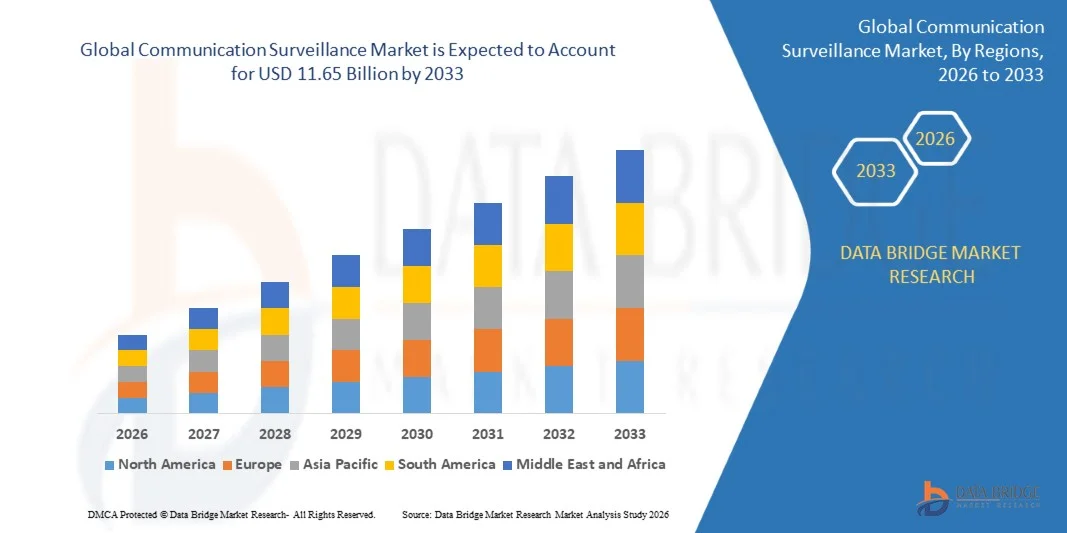

The Communication Surveillance Market was valued at USD 4.95 billion in 2025 and is projected to reach USD 11.65 billion by 2033, growing at a CAGR of 11.30% from 2026 to 2033. The market is witnessing strong growth driven by rising demand for advanced intelligence gathering solutions, increasing cybersecurity threats, and expanding adoption of digital communication monitoring technologies across government and enterprise sectors.

The growing need for national security, counterterrorism operations, and law enforcement intelligence is significantly boosting the deployment of communication surveillance systems. In addition, rapid expansion of internet-based communication platforms, cloud services, and encrypted messaging applications is pushing agencies and organizations to adopt AI-powered surveillance tools capable of real-time data interception, analysis, and threat detection while ensuring regulatory compliance and data security.

Key Market Trends & Insights

- North America dominated the communication surveillance market with the largest revenue share of 38.7% in 2025, supported by strong national security investments, advanced digital intelligence infrastructure, and widespread deployment of lawful interception and AI-based surveillance systems across defense and corporate sectors.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 12.2% from 2026 to 2033. Growth is driven by rapid digital transformation, increasing cybersecurity threats, rising internet penetration, and strong government initiatives for smart city development and national security enhancement across China, India, and Japan.

- The Software segment held the largest market revenue share of approximately 52.6% in 2025 driven by increasing adoption of AI-based monitoring platforms, real-time analytics engines, and encrypted communication interception solutions across government and enterprise surveillance systems. Software solutions are preferred due to their scalability, ease of integration, and ability to process large volumes of structured and unstructured communication data. Growing reliance on digital communication channels such as email, VoIP, and messaging applications is further strengthening demand for advanced surveillance software platforms. In addition, continuous upgrades in AI-driven threat detection models are improving accuracy in identifying suspicious communication patterns.

- The Services segment is projected to register the fastest growth at a CAGR of 12.4% from 2026 to 2033, driven by rising demand for managed surveillance services, system integration, and compliance support across regulatory-intensive industries. Expanding outsourcing of monitoring operations and cybersecurity intelligence services is further accelerating segment expansion. Organizations are increasingly relying on third-party expertise for deployment, maintenance, and optimization of surveillance infrastructure. In addition, growing complexity of multi-platform communication ecosystems is boosting demand for specialized consulting and support services.

- The Government Communications Surveillance segment held the largest market revenue share of approximately 46.8% in 2025 driven by strong national security initiatives, counterterrorism operations, and increasing investment in lawful interception systems by intelligence agencies across North America and Europe. Governments are increasingly modernizing intelligence frameworks to address rising cybercrime and digital threats. Expanding geopolitical tensions and cross-border data monitoring requirements are further supporting segment dominance.

- The Business Communications Surveillance segment is projected to register the fastest growth at a CAGR of 11.9% from 2026 to 2033, driven by rising corporate compliance requirements, insider threat detection needs, and increasing monitoring of enterprise communication channels such as email, VoIP, and collaboration platforms. Organizations are deploying surveillance tools to ensure regulatory adherence and prevent data leakage. Increasing hybrid and remote working models are also expanding the need for enterprise communication monitoring. Furthermore, rising financial fraud risks are accelerating adoption across corporate environments.

- The Real-Time Monitoring and Alerts segment held the largest market revenue share of approximately 34.2% in 2025 driven by increasing demand for immediate threat identification, rapid response capabilities, and continuous surveillance of high-risk communication channels. Security agencies prioritize real-time monitoring to prevent incidents before escalation. Growing data traffic across digital communication platforms is also boosting demand for continuous surveillance systems.

- The AI & NLP-based Analysis segment is projected to register the fastest growth at a CAGR of 13.1% from 2026 to 2033, driven by growing adoption of machine learning models for sentiment analysis, encrypted text interpretation, and automated threat detection across large-scale communication datasets. Increasing sophistication of cyber threats is pushing demand for intelligent analytics solutions. AI-driven tools are enhancing contextual understanding of communication patterns across multiple languages. In addition, advancements in deep learning are improving detection accuracy and reducing false positives.

- The On-premise segment held the largest market revenue share of approximately 57.3% in 2025 driven by strict data security regulations, government mandates, and preference for localized data control in intelligence and defense applications. Sensitive communication data is often required to remain within national boundaries for compliance reasons. High-security agencies continue to prioritize on-premise infrastructure for better control and isolation.

- The Cloud segment is projected to register the fastest growth at a CAGR of 14.2% from 2026 to 2033, driven by increasing adoption of scalable surveillance infrastructure, remote monitoring capabilities, and growing integration of AI-powered cloud analytics platforms in enterprise communication systems. Cloud deployment enables faster scalability and lower upfront infrastructure costs. Increasing digital transformation across enterprises is further accelerating cloud adoption. Moreover, advancements in secure cloud encryption are improving trust in cloud-based surveillance solutions.

- The Regulators and Government Agencies segment held the largest market revenue share of approximately 48.5% in 2025 driven by expanding national security programs, intelligence modernization initiatives, and increasing deployment of lawful interception and monitoring systems. Governments are investing heavily in digital intelligence infrastructure to counter evolving cyber threats. Rising need for public safety and crime prevention is also strengthening segment leadership.

- The Corporates and Enterprises segment is projected to register the fastest growth at a CAGR of 12.7% from 2026 to 2033, driven by rising concerns over data security, insider threats, regulatory compliance, and increasing adoption of enterprise communication monitoring solutions across banking, telecom, and IT sectors. Organizations are prioritizing risk mitigation strategies to protect sensitive data assets. Growing regulatory pressure regarding data governance is further boosting adoption. In addition, increasing use of cloud-based communication tools is expanding enterprise surveillance requirements.

Market Size & Forecast

- Global Market Value (2025): USD 4.95 Billion

- Expected Market Value (2033): USD 11.65 Billion

- Forecast CAGR (2026–2033): 11.30%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Communication Surveillance Market Segmentation

|

Attributes |

Communication Surveillance Key Market Insights |

|

Segments Covered |

· By Component: Hardware, Software, and Services · By Type: Electronic Communication Surveillance, Business Communications Surveillance, and Government Communications Surveillance · By Technology: AI & NLP-based Analysis, Archiving and Compliance Storage, Real-Time Monitoring and Alerts, and Behavioral Analytics and Pattern Detection · By Deployment: On-premise and Cloud · By End User: Financial Institution, Corporates and Enterprises, and Regulators and Government Agencies |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• BAE Systems (U.K.) |

|

Market Opportunities |

• Artificial Intelligence Driven Threat Intelligence Expansion |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Communication Surveillance Market Trends

Trend: Growth In AI Driven Communication Monitoring And Encrypted Traffic Surveillance Technologies

Increasing demand for advanced digital intelligence, real-time threat detection, and secure communication monitoring solutions across government, defense, and enterprise sectors. Rising cybersecurity threats, terrorism risks, and cross-border digital crimes are driving adoption of intelligent surveillance platforms capable of analyzing large volumes of voice, video, and data communications.

In modern surveillance systems, agencies are increasingly integrating AI-based analytics and natural language processing tools, For instance for monitoring encrypted messaging platforms, VoIP calls, and social media communications, to detect suspicious patterns and prevent security breaches in real time. Law enforcement agencies in countries such as the U.S. and U.K. are deploying advanced lawful interception systems capable of processing millions of daily communication records to support counterterrorism and cybercrime investigations.

The rapid expansion of cloud-based communication platforms and enterprise collaboration tools is also increasing demand for scalable surveillance architectures capable of monitoring distributed digital ecosystems. In addition, intelligence agencies and cybersecurity firms continue to rely on advanced surveillance frameworks, such as signal intelligence (SIGINT) systems used by organizations such as the NSA for large-scale data interception and analysis, due to their ability to process complex multi-channel communication networks. Growing industry validation through pilot cybersecurity deployments in 2025 integrating AI-driven surveillance platforms into national security infrastructures is showing threat detection accuracy improvements of nearly 15–20% in identifying anomalous communication behavior under high-volume data environments.

Communication Surveillance Market Dynamics

Key Market Driver: Rising Demand For National Security And Cyber Threat Intelligence Systems

Governments and enterprises worldwide are facing increasing pressure to strengthen cybersecurity frameworks, prevent data breaches, and monitor digital communication channels for potential threats. The exponential growth of internet usage, encrypted messaging applications, and cloud-based communication platforms has significantly expanded the attack surface for cybercriminal activities, driving demand for advanced surveillance technologies.

Security agencies are increasingly deploying communication surveillance systems to support counterterrorism operations, financial fraud detection, and criminal intelligence gathering across digital networks. Law enforcement bodies are actively integrating AI-powered monitoring tools to analyze voice, text, and metadata communications in real time to improve situational awareness and response efficiency.

Similarly, enterprises in sectors such as banking, telecom, and critical infrastructure are adopting surveillance solutions to detect insider threats and ensure regulatory compliance. Real-world deployments in 2024 across North America and Europe integrating AI-based interception systems into national cybersecurity frameworks demonstrated improvements of approximately 12–18% in early threat detection and incident response times across monitored communication channels.

Key Restraint/Challenge: Privacy Regulations And High Implementation Complexity

The communication surveillance market faces significant challenges due to strict data privacy regulations and legal restrictions governing the monitoring of personal communications. Frameworks such as GDPR in Europe and various national data protection laws impose limitations on data collection, storage, and processing, creating compliance complexities for solution providers and end users.

In addition, the deployment of advanced surveillance infrastructure requires high investment in hardware, software, and secure data centers, increasing overall operational costs for governments and organizations. Integration challenges with legacy communication systems and the need for highly skilled cybersecurity professionals further limit large-scale adoption in developing regions.

Industry assessments indicate that compliance-related delays and regulatory approval processes can extend deployment timelines by 20–30% in large-scale surveillance projects, particularly in jurisdictions with strict privacy enforcement and cross-border data transfer restrictions.

Key Market Opportunity: Expansion Of AI Powered Cloud Surveillance And Cross Platform Intelligence Systems

The growing shift toward cloud-based communication platforms and hybrid work environments is creating significant opportunities for scalable, AI-powered surveillance solutions capable of monitoring distributed communication networks. Organizations are increasingly seeking unified platforms that can analyze voice, video, email, and messaging data across multiple digital channels in real time.

Government agencies are adopting cloud-native surveillance architectures to improve intelligence sharing and operational efficiency across national and international security networks. For instance, several European cybersecurity initiatives launched in 2025 have begun integrating cross-platform analytics systems to enhance coordinated threat detection across telecom and internet service providers.

In addition, advancements in machine learning, speech recognition, and behavioral analytics are improving the accuracy and speed of threat identification. Growing adoption of secure cloud infrastructure by defense and intelligence agencies in North America and Asia-Pacific is further enabling expansion of next-generation surveillance ecosystems capable of processing over 5 billion communication events daily in high-security monitoring environments.

Communication Surveillance Market Scope

The market is segmented on the basis of component, type, technology, deployment, and end-use application.

- By Component

On the basis of component, the communication surveillance market is segmented into Hardware, Software, and Services. The Software segment held the largest market revenue share of approximately 52.6% in 2025 driven by increasing adoption of AI-based monitoring platforms, real-time analytics engines, and encrypted communication interception solutions across government and enterprise surveillance systems. Software solutions are preferred due to their scalability, ease of integration, and ability to process large volumes of structured and unstructured communication data. Growing reliance on digital communication channels such as email, VoIP, and messaging applications is further strengthening demand for advanced surveillance software platforms. In addition, continuous upgrades in AI-driven threat detection models are improving accuracy in identifying suspicious communication patterns.

The Services segment is projected to register the fastest growth at a CAGR of 12.4% from 2026 to 2033, driven by rising demand for managed surveillance services, system integration, and compliance support across regulatory-intensive industries. Expanding outsourcing of monitoring operations and cybersecurity intelligence services is further accelerating segment expansion. Organizations are increasingly relying on third-party expertise for deployment, maintenance, and optimization of surveillance infrastructure. In addition, growing complexity of multi-platform communication ecosystems is boosting demand for specialized consulting and support services.

- By Type

On the basis of type, the communication surveillance market is segmented into Electronic Communication Surveillance, Business Communications Surveillance, and Government Communications Surveillance. The Government Communications Surveillance segment held the largest market revenue share of approximately 46.8% in 2025 driven by strong national security initiatives, counterterrorism operations, and increasing investment in lawful interception systems by intelligence agencies across North America and Europe. Governments are increasingly modernizing intelligence frameworks to address rising cybercrime and digital threats. Expanding geopolitical tensions and cross-border data monitoring requirements are further supporting segment dominance.

The Business Communications Surveillance segment is projected to register the fastest growth at a CAGR of 11.9% from 2026 to 2033, driven by rising corporate compliance requirements, insider threat detection needs, and increasing monitoring of enterprise communication channels such as email, VoIP, and collaboration platforms. Organizations are deploying surveillance tools to ensure regulatory adherence and prevent data leakage. Increasing hybrid and remote working models are also expanding the need for enterprise communication monitoring. Furthermore, rising financial fraud risks are accelerating adoption across corporate environments.

- By Technology

On the basis of technology, the communication surveillance market is segmented into AI & NLP-based Analysis, Archiving and Compliance Storage, Real-Time Monitoring and Alerts, and Behavioral Analytics and Pattern Detection. The Real-Time Monitoring and Alerts segment held the largest market revenue share of approximately 34.2% in 2025 driven by increasing demand for immediate threat identification, rapid response capabilities, and continuous surveillance of high-risk communication channels. Security agencies prioritize real-time monitoring to prevent incidents before escalation. Growing data traffic across digital communication platforms is also boosting demand for continuous surveillance systems.

The AI & NLP-based Analysis segment is projected to register the fastest growth at a CAGR of 13.1% from 2026 to 2033, driven by growing adoption of machine learning models for sentiment analysis, encrypted text interpretation, and automated threat detection across large-scale communication datasets. Increasing sophistication of cyber threats is pushing demand for intelligent analytics solutions. AI-driven tools are enhancing contextual understanding of communication patterns across multiple languages. In addition, advancements in deep learning are improving detection accuracy and reducing false positives.

- By Deployment

On the basis of deployment, the communication surveillance market is segmented into On-premise and Cloud. The On-premise segment held the largest market revenue share of approximately 57.3% in 2025 driven by strict data security regulations, government mandates, and preference for localized data control in intelligence and defense applications. Sensitive communication data is often required to remain within national boundaries for compliance reasons. High-security agencies continue to prioritize on-premise infrastructure for better control and isolation.

The Cloud segment is projected to register the fastest growth at a CAGR of 14.2% from 2026 to 2033, driven by increasing adoption of scalable surveillance infrastructure, remote monitoring capabilities, and growing integration of AI-powered cloud analytics platforms in enterprise communication systems. Cloud deployment enables faster scalability and lower upfront infrastructure costs. Increasing digital transformation across enterprises is further accelerating cloud adoption. Moreover, advancements in secure cloud encryption are improving trust in cloud-based surveillance solutions.

- By End User

On the basis of end user, the communication surveillance market is segmented into Financial Institutions, Corporates and Enterprises, and Regulators and Government Agencies. The Regulators and Government Agencies segment held the largest market revenue share of approximately 48.5% in 2025 driven by expanding national security programs, intelligence modernization initiatives, and increasing deployment of lawful interception and monitoring systems. Governments are investing heavily in digital intelligence infrastructure to counter evolving cyber threats. Rising need for public safety and crime prevention is also strengthening segment leadership.

The Corporates and Enterprises segment is projected to register the fastest growth at a CAGR of 12.7% from 2026 to 2033, driven by rising concerns over data security, insider threats, regulatory compliance, and increasing adoption of enterprise communication monitoring solutions across banking, telecom, and IT sectors. Organizations are prioritizing risk mitigation strategies to protect sensitive data assets. Growing regulatory pressure regarding data governance is further boosting adoption. In addition, increasing use of cloud-based communication tools is expanding enterprise surveillance requirements.

Communication Surveillance Market Regional Analysis

North America Communication Surveillance Market Insight

North America dominated the communication surveillance market with the largest revenue share of 38.7% in 2025, supported by rising national security investments, increasing cybersecurity threats, and strong adoption of advanced digital intelligence and lawful interception systems. The region benefits from a highly developed digital infrastructure, widespread enterprise communication networks, and strong regulatory frameworks that mandate monitoring and compliance across critical sectors. Growing concerns over terrorism, cybercrime, and data breaches are further driving demand for AI-powered surveillance solutions across government and corporate environments.

U.S. Communication Surveillance Market Insight

The U.S. communication surveillance market captured the largest revenue share in 2025 within North America, driven by extensive deployment of intelligence surveillance systems by federal agencies and increasing adoption of AI-based monitoring tools across defense, homeland security, and law enforcement sectors. Rising use of encrypted communication platforms has strengthened demand for advanced interception and analytics solutions. In addition, strong presence of leading technology providers and continuous modernization of cybersecurity infrastructure are further accelerating market growth across government and enterprise applications.

Europe Communication Surveillance Market Insight

The Europe communication surveillance market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by strict data protection regulations, rising cybersecurity threats, and increasing demand for lawful interception systems across government and enterprise sectors. The region is experiencing strong adoption of AI-based monitoring tools to enhance digital security and compliance with regulatory frameworks such as GDPR. Expanding digital communication networks and growing cross-border cybercrime incidents are further encouraging investment in advanced surveillance infrastructure across public and private organizations.

U.K. Communication Surveillance Market Insight

The U.K. communication surveillance market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing investments in national security systems, rising cybercrime cases, and growing demand for advanced intelligence monitoring solutions. Government agencies and enterprises are increasingly adopting AI-powered surveillance platforms to enhance real-time threat detection and communication monitoring. The country’s strong digital economy, expanding fintech sector, and high dependence on cloud-based communication systems are further supporting market expansion.

Germany Communication Surveillance Market Insight

The Germany communication surveillance market is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising focus on digital sovereignty, increasing cybersecurity awareness, and strong demand for secure communication monitoring systems across industrial and government sectors. Germany’s advanced technological infrastructure and emphasis on data privacy and compliance are encouraging adoption of AI-driven surveillance solutions. In addition, growing industrial digitization and increasing cyber threats targeting critical infrastructure are accelerating market growth.

Asia-Pacific Communication Surveillance Market Insight

The Asia-Pacific communication surveillance market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid digital transformation, increasing internet penetration, and rising cybersecurity threats across countries such as China, India, and Japan. The region is experiencing strong government initiatives for smart city development and digital security enhancement, driving demand for advanced surveillance systems. Expanding telecom networks and growing adoption of cloud-based communication platforms are further boosting market growth across both public and private sectors.

Japan Communication Surveillance Market Insight

The Japan communication surveillance market is expected to witness strong growth from 2026 to 2033 due to increasing demand for advanced cybersecurity systems, rising digital communication adoption, and strong emphasis on national security and data protection. The country’s high-tech infrastructure and integration of AI and IoT-based communication systems are supporting adoption of advanced surveillance technologies. In addition, Japan’s aging population and increasing reliance on digital communication platforms are driving demand for secure and intelligent monitoring solutions across government and enterprise applications.

China Communication Surveillance Market Insight

The China communication surveillance market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid digitalization, large-scale internet usage, and strong government investments in cybersecurity and surveillance infrastructure. The country’s extensive telecom network and widespread adoption of mobile and cloud-based communication platforms are driving demand for advanced monitoring systems. Growing focus on smart city development, national security initiatives, and AI integration in public safety systems are further propelling market expansion across China.

Communication Surveillance Market Share

The Communication Surveillance industry is primarily led by well-established companies, including:

• BAE Systems (U.K.)

• Verint Systems (U.S.)

• NICE (Israel)

• Utimaco (Germany)

• Ericsson (Sweden)

• Cisco Systems (U.S.)

• Nokia (Finland)

• Thales (France)

• Elbit Systems (Israel)

• SS8 Technologies (U.S.)

Latest Developments in Communication Surveillance Market

- In June 2025, SS8 Networks was acquired by Mill Point Capital LLC, a strategic development aimed at accelerating the company’s expansion and strengthening its AI-driven communication surveillance and intelligence capabilities. The acquisition is expected to enhance SS8’s portfolio of investigative and lawful interception solutions for intelligence agencies and law-enforcement organizations. This move is likely to improve product innovation and operational scale, thereby strengthening competitive positioning in the Communication Surveillance Market. It also supports faster deployment of advanced analytics-based monitoring systems across critical security infrastructures.

- In September 2020, BAE Systems signed a five-year agreement with a major North American telecommunications service provider, marking a significant development in 5G lawful interception capabilities. The deal focuses on deploying a 5G Stand-Alone lawful interception solution integrated into next-generation telecom networks. This advancement enables secure, standardized interception of communications within high-speed 5G environments for national security and law enforcement agencies. It strengthens BAE Systems’ leadership in secure telecom surveillance technologies while enhancing real-time monitoring efficiency and regulatory compliance across evolving communication infrastructures.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.