Global Compostable Foodservice Packaging Market

Market Size in USD Billion

USD

22.67 Billion

USD

43.23 Billion

2025

2033

USD

22.67 Billion

USD

43.23 Billion

2025

2033

| 2026 - 2033 | |

| USD 22.67 Billion | |

| USD 43.23 Billion | |

| % | |

|

Compostable Food Service Packaging Market Overview

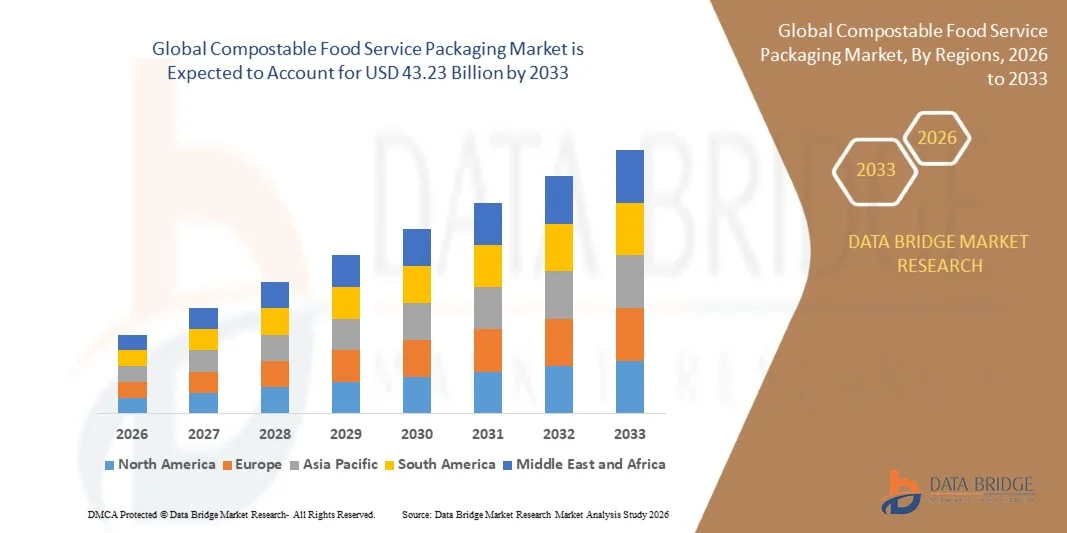

The Compostable Food Service Packaging Market was valued at USD 22.67 billion in 2025 and is projected to reach USD 43.23 billion by 2033, growing at a CAGR of 8.40% from 2026 to 2033. The market is experiencing strong growth driven by increasing consumer preference for sustainable packaging solutions, rising regulatory restrictions on single-use plastics, and expanding adoption of eco-friendly packaging across restaurants, cafés, quick-service restaurants (QSRs), catering services, and food delivery platforms.

Growing environmental concerns related to plastic waste generation, combined with stringent government regulations promoting biodegradable and compostable materials, are encouraging food service operators and packaging manufacturers to transition toward compostable alternatives. Products made from bagasse, polylactic acid (PLA), paper, bamboo, and other plant-based materials are increasingly replacing conventional plastic containers, cups, trays, cutlery, and takeaway packaging in many markets. In addition, the rapid growth of online food delivery services and the increasing focus of food brands on sustainability commitments are accelerating demand for compostable food service packaging, offering environmentally responsible, commercially viable, and consumer-friendly solutions for modern food service operations.

Key Market Trends & Insights

- North America dominated the compostable foodservice packaging market with the largest revenue share of 38.6% in 2025, supported by strong regulatory pressure on single-use plastics, rising adoption of sustainable packaging in foodservice chains, and growing consumer preference for eco-friendly dining and takeaway solutions.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 9.2% from 2026 to 2033, driven by rapid urbanization, expansion of food delivery platforms, increasing environmental awareness, and government initiatives promoting plastic alternatives.

- The Cups segment held the largest market revenue share of approximately 28.6% in 2025 driven by extensive usage across coffee shops, quick-service restaurants, beverage chains, and takeaway food outlets. Growing replacement of conventional plastic and foam cups with compostable paper-based and biopolymer alternatives, coupled with increasing regulations on disposable beverage packaging, continues to support segment dominance.

- The Clamshell segment is projected to register the fastest growth at a CAGR of 9.8% from 2026 to 2033, driven by the rapid expansion of food delivery services, takeaway meals, and sustainable packaging initiatives among restaurant operators. Increasing demand for durable compostable containers capable of maintaining food quality during transportation is accelerating segment growth.

- The Paper and Paperboard segment accounted for the largest market revenue share of approximately 46.9% in 2025 driven by strong availability, cost-effectiveness, high consumer acceptance, and widespread adoption across cups, trays, containers, and food wraps. Regulatory support for fiber-based packaging and increasing investment in sustainable paper packaging technologies are further strengthening market leadership.

- The Bagasse and Seaweed segment is expected to witness the fastest growth at a CAGR of 10.5% from 2026 to 2033 due to increasing demand for renewable and fully compostable packaging materials with lower environmental impact. Rising adoption among foodservice providers seeking plastic-free packaging solutions and ongoing innovations in agricultural waste-derived materials are supporting segment expansion.

- The Chain Restaurants segment held the largest market revenue share of approximately 31.7% in 2025 driven by large-scale sustainability commitments, regulatory compliance requirements, and high-volume procurement of compostable packaging products. Major restaurant chains continue to transition toward compostable containers, cups, lids, and cutlery as part of broader environmental responsibility programs.

- The Delivery Catering segment is projected to register the fastest growth at a CAGR of 10.9% from 2026 to 2033 driven by the continuing expansion of online food delivery platforms, cloud kitchens, and takeaway food services globally. Growing consumer preference for environmentally responsible packaging and increasing demand for compostable meal delivery solutions are accelerating adoption across the segment.

Market Size & Forecast

- Global Market Value (2025): USD 22.67 Billion

- Expected Market Value (2033): USD 43.23 Billion

- Forecast CAGR (2026–2033): 8.40%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Compostable Food Service Packaging Market Segmentation

|

Attributes |

Compostable Food Service Packaging Key Market Insights |

|

Segments Covered |

· By Packaging Type: Plates, Trays, Bowls, Cups, Clamshell, Cutlery, Pouches and Sachets, and Others · By Material: Plastic, Paper and Paperboard, Bagasse and Seaweed, and Others · By End- User: Chain Restaurants, Non- Chain Restaurants, Chain Cafe, Non- Chain Cafe, Delivery Catering, Independent Sellers and Kiosks, and Other |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Novolex (U.S.) |

|

Market Opportunities |

• Expansion Of Compostable Packaging Adoption Across Emerging Economies • Growing Investments In Industrial Composting Infrastructure And Circular Economy Initiatives |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Compostable Food Service Packaging Market Trends

Key Market Trend: Rising Adoption Of Fiber-Based And Certified Compostable Packaging Solutions

Growing environmental concerns, tightening regulations on single-use plastics, and increasing consumer preference for sustainable packaging are accelerating demand for compostable food service packaging across restaurants, cafés, catering services, and food delivery platforms. Conventional plastic packaging contributes significantly to landfill accumulation and marine pollution, encouraging food service operators to transition toward compostable alternatives made from bagasse, molded fiber, bamboo, paperboard, and bioplastics.

Major food service chains are increasingly integrating compostable packaging, For instance for takeaway containers, cups, bowls, lids, and cutlery, to support corporate sustainability commitments and comply with emerging packaging regulations. The rapid expansion of online food delivery services is further increasing demand for environmentally responsible packaging capable of maintaining food quality while reducing waste generation. Educational institutions, airports, and large event venues are also adopting compostable packaging as part of broader waste reduction programs.

Growing industry validation is evident through large-scale sustainability initiatives. In 2025, several foodservice operators participating in compostable packaging transition programs reported diversion of more than 60–70% of packaging waste from landfill streams where commercial composting infrastructure was available. Certified compostable products carrying industrial compostability certifications are also experiencing increasing adoption across North America and Europe as sustainability reporting requirements become more stringent.

Compostable Food Service Packaging Market Dynamics

Key Market Driver: Stringent Regulations On Single-Use Plastics And Packaging Waste Reduction

Governments worldwide are implementing stricter regulations aimed at reducing plastic pollution, improving waste management, and promoting circular economy practices. Restrictions on disposable plastic food containers, cutlery, straws, and cups are creating strong demand for compostable alternatives that meet both regulatory compliance requirements and consumer sustainability expectations.

Food service operators, quick-service restaurant chains, and institutional catering providers are increasingly replacing traditional plastic packaging with certified compostable solutions to align with environmental policies and avoid regulatory penalties. Large multinational restaurant brands are expanding sustainable packaging initiatives, while municipalities are encouraging adoption through procurement guidelines and waste reduction targets.

Real-world policy implementation continues to support market growth. The European Union’s Single-Use Plastics Directive and similar regulatory frameworks across North America and Asia-Pacific have accelerated investment in compostable foodservice packaging solutions. Industry assessments conducted during 2024–2025 indicated that regions implementing stricter plastic reduction measures recorded substantially higher adoption rates of compostable food containers and serviceware compared to markets with limited regulatory intervention.

Key Market Restraint/Challenge: Higher Product Costs And Limited Composting Infrastructure

Despite strong sustainability benefits, compostable food service packaging remains more expensive than conventional plastic alternatives due to higher raw material costs, specialized manufacturing processes, and certification requirements. Materials such as PLA, molded fiber, and bagasse-based products often carry premium pricing, creating affordability concerns for small food service businesses operating under cost-sensitive conditions.

In addition, the environmental effectiveness of compostable packaging depends on access to industrial composting facilities capable of processing certified compostable materials. Many regions continue to face insufficient compost collection networks and limited composting infrastructure, resulting in compostable products being disposed of through conventional landfill systems. Consumer confusion regarding proper disposal practices further reduces potential environmental benefits.

Industry benchmarking studies indicate that compostable foodservice packaging products can cost approximately 20–50% more than conventional plastic alternatives depending on product category and material composition. Furthermore, industrial composting infrastructure remains unavailable to a significant portion of global municipalities, creating operational challenges for large-scale adoption and waste diversion efforts.

Key Market Opportunity: Expansion Of Food Delivery Platforms And Circular Economy Initiatives

The rapid growth of food delivery services, takeaway consumption, and sustainability-focused procurement programs is creating substantial opportunities for compostable food service packaging manufacturers. Food service operators increasingly require packaging solutions that combine durability, food safety, and environmental responsibility while supporting corporate sustainability objectives.

Restaurant chains and delivery platforms are expanding the use of compostable packaging, For instance for meal containers, beverage cups, trays, and disposable utensils, to strengthen environmental credentials and address growing consumer demand for eco-friendly products. Rising investment in municipal composting infrastructure and zero-waste initiatives is further supporting market development by improving end-of-life processing capabilities for compostable materials.

Advancements in barrier coatings, molded fiber technology, and compostable biopolymer formulations are improving heat resistance, moisture protection, and product durability, enabling broader use across hot and cold food applications. Food service sustainability programs implemented across North America, Europe, and Asia-Pacific during 2025 reported reductions in single-use plastic consumption exceeding 30–40% after transitioning portions of their packaging portfolios to certified compostable alternatives, creating significant long-term growth opportunities for market participants.

Compostable Food Service Packaging Market Scope

The market is segmented on the basis of packaging type, material, and end-user.

- By Packaging Type

On the basis of packaging type, the compostable foodservice packaging market is segmented into Plates, Trays, Bowls, Cups, Clamshell, Cutlery, Pouches and Sachets, and Others. The Cups segment held the largest market revenue share of approximately 28.6% in 2025 driven by extensive usage across coffee shops, quick-service restaurants, beverage chains, and takeaway food outlets. Growing replacement of conventional plastic and foam cups with compostable paper-based and biopolymer alternatives, coupled with increasing regulations on disposable beverage packaging, continues to support segment dominance.

The Clamshell segment is projected to register the fastest growth at a CAGR of 9.8% from 2026 to 2033, driven by the rapid expansion of food delivery services, takeaway meals, and sustainable packaging initiatives among restaurant operators. Increasing demand for durable compostable containers capable of maintaining food quality during transportation is accelerating segment growth.

- By Material

On the basis of material, the compostable foodservice packaging market is segmented into Plastic, Paper and Paperboard, Bagasse and Seaweed, and Others. The Paper and Paperboard segment accounted for the largest market revenue share of approximately 46.9% in 2025 driven by strong availability, cost-effectiveness, high consumer acceptance, and widespread adoption across cups, trays, containers, and food wraps. Regulatory support for fiber-based packaging and increasing investment in sustainable paper packaging technologies are further strengthening market leadership.

The Bagasse and Seaweed segment is expected to witness the fastest growth at a CAGR of 10.5% from 2026 to 2033 due to increasing demand for renewable and fully compostable packaging materials with lower environmental impact. Rising adoption among foodservice providers seeking plastic-free packaging solutions and ongoing innovations in agricultural waste-derived materials are supporting segment expansion.

- By End-User

On the basis of end-user, the compostable foodservice packaging market is segmented into Chain Restaurants, Non-Chain Restaurants, Chain Cafe, Non-Chain Cafe, Delivery Catering, Independent Sellers and Kiosks, and Other. The Chain Restaurants segment held the largest market revenue share of approximately 31.7% in 2025 driven by large-scale sustainability commitments, regulatory compliance requirements, and high-volume procurement of compostable packaging products. Major restaurant chains continue to transition toward compostable containers, cups, lids, and cutlery as part of broader environmental responsibility programs.

The Delivery Catering segment is projected to register the fastest growth at a CAGR of 10.9% from 2026 to 2033 driven by the continuing expansion of online food delivery platforms, cloud kitchens, and takeaway food services globally. Growing consumer preference for environmentally responsible packaging and increasing demand for compostable meal delivery solutions are accelerating adoption across the segment.

Compostable Food Service Packaging Market Regional Analysis

North America Compostable Foodservice Packaging Market Insight

North America dominated the compostable foodservice packaging market with the largest revenue share of 38.6% in 2025, supported by strong regulatory pressure on single-use plastics, rising adoption of sustainable packaging in foodservice chains, and growing consumer preference for eco-friendly dining and takeaway solutions. The region benefits from advanced waste management systems and increasing availability of certified composting infrastructure, particularly in urban centers across the U.S. and Canada. Major quick-service restaurant chains and institutional foodservice providers are increasingly shifting toward compostable cups, containers, and cutlery to align with corporate sustainability targets and environmental compliance requirements.

U.S. Compostable Foodservice Packaging Market Insight

The U.S. compostable foodservice packaging market captured the largest revenue share of 82.3% within North America in 2025, driven by rapid expansion of food delivery platforms, strong regulatory frameworks restricting plastic use in states such as California and New York, and increasing corporate sustainability commitments from major restaurant chains. The growing penetration of certified compostable products in quick-service restaurants, cafés, and institutional catering is further accelerating market growth. In 2025, several large foodservice operators reported replacing more than 50% of single-use plastic packaging in urban outlets with compostable alternatives, supported by expanding industrial composting programs across major metropolitan areas.

Europe Compostable Foodservice Packaging Market Insight

The Europe compostable foodservice packaging market is expected to witness the fastest growth rate from 2026 to 2033, driven by stringent EU directives on single-use plastics, strong circular economy policies, and increasing consumer awareness regarding environmental sustainability. The region is experiencing rapid adoption across restaurants, food delivery services, and institutional catering due to strict waste reduction targets and mandatory recyclable or compostable packaging standards in several countries. Rising investments in composting infrastructure and extended producer responsibility schemes are further strengthening market expansion across residential and commercial foodservice applications.

U.K. Compostable Foodservice Packaging Market Insight

The U.K. compostable foodservice packaging market is expected to witness strong growth from 2026 to 2033, driven by increasing government initiatives to reduce plastic waste, growing adoption of sustainable packaging among food delivery platforms, and rising consumer demand for environmentally responsible dining solutions. Major restaurant chains and café operators are transitioning to compostable packaging for takeaway meals and beverages. In 2025, several UK-based foodservice brands reported significant reductions in plastic packaging usage following the adoption of fiber-based and compostable alternatives across urban store networks.

Germany Compostable Foodservice Packaging Market Insight

The Germany compostable foodservice packaging market is expected to witness steady growth from 2026 to 2033, supported by strong environmental regulations, high consumer awareness of sustainability, and advanced waste separation and recycling systems. The country’s emphasis on circular economy practices and packaging waste reduction is driving adoption of compostable solutions across restaurants, institutional catering, and retail foodservice outlets. Increasing integration of certified compostable materials in urban food delivery systems is further contributing to market expansion.

Asia-Pacific Compostable Foodservice Packaging Market Insight

The Asia-Pacific compostable foodservice packaging market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid urbanization, expanding food delivery ecosystems, and increasing government initiatives to reduce plastic waste in countries such as China, India, and Japan. Rising disposable incomes and growing awareness of environmental sustainability are accelerating adoption across quick-service restaurants and cloud kitchens. In 2025, several major APAC food delivery platforms reported pilot programs integrating compostable packaging in urban centers, reducing single-use plastic consumption by more than 25–35% in participating regions.

Japan Compostable Foodservice Packaging Market Insight

The Japan compostable foodservice packaging market is expected to witness strong growth from 2026 to 2033 due to increasing environmental consciousness, advanced waste management systems, and rising adoption of sustainable packaging in convenience stores and restaurant chains. The country’s emphasis on reducing plastic waste and improving recycling efficiency is encouraging foodservice operators to shift toward compostable containers, cups, and cutlery. In 2025, several Japanese municipalities expanded composting initiatives, supporting wider adoption of certified compostable packaging in urban foodservice networks.

China Compostable Foodservice Packaging Market Insight

The China compostable foodservice packaging market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, expansion of online food delivery platforms, and strong government initiatives aimed at reducing plastic pollution. China’s large-scale foodservice industry and growing middle-class population are driving demand for sustainable packaging solutions across restaurants, cafés, and delivery services. In 2025, multiple leading food delivery platforms in China reported significant adoption of biodegradable and compostable packaging options in tier-1 and tier-2 cities, supported by increasing domestic production capacity for fiber-based and biopolymer materials.

Compostable Food Service Packaging Market Share

The Compostable Food Service Packaging industry is primarily led by well-established companies, including:

• Novolex (U.S.)

• Dart Container Corporation (U.S.)

• Good Start Packaging (U.S.)

• Be Green Packaging (U.S.)

• ecoenclose (U.S.)

• Huhtamäki Oyj (Finland)

• Georgia-Pacific (U.S.)

• WestRock Company (U.S.)

• Virosac Srl. (Italy)

• BioGreen (U.K.)

• Elevate Packaging (U.S.)

• Genpak, LLC. (U.S.)

• BioBag Americas, Inc. (U.S.)

• International Paper (U.S.)

• Biosphere Plastic, LLC (U.S.)

• Anchor Packaging (U.S.)

• Eco-Products, Inc. (U.S.)

Latest Developments in Compostable Food Service Packaging Market

- In September, Eco-Products (U.S.), launched a new line of compostable food containers made from renewable resources targeting the fast-casual dining segment, aiming to strengthen product innovation and differentiation, which is expected to enhance its market position and increase adoption across sustainability-focused foodservice operators.

- In August, World Centric (U.S.), entered a partnership with a leading food delivery service to supply fully compostable packaging for meal kits, aiming to expand its sustainable packaging portfolio, which is expected to improve brand visibility, strengthen consumer trust, and boost adoption in the rapidly growing food delivery ecosystem

- In July, Vegware (U.K.), expanded its operations into the Asia-Pacific region by establishing a manufacturing facility in Singapore, aiming to enhance regional supply chain efficiency and meet rising demand, which is expected to reduce logistics costs, improve responsiveness, and strengthen its competitive position in emerging sustainable packaging markets.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Compostable Foodservice Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Compostable Foodservice Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Compostable Foodservice Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.