Global Compound Semiconductor Market

Market Size in USD Billion

USD

40.86 Billion

USD

66.12 Billion

2024

2032

USD

40.86 Billion

USD

66.12 Billion

2024

2032

| 2025 - 2032 | |

| USD 40.86 Billion | |

| USD 66.12 Billion | |

| % | |

|

Compound Semiconductor Market Size

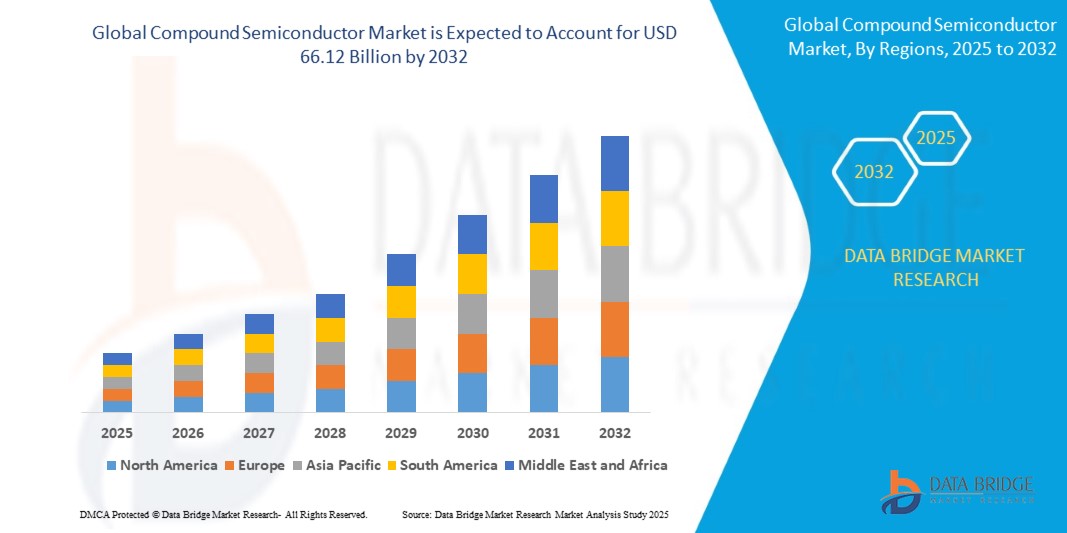

- The global compound semiconductor market size was valued at USD 40.86 billion in 2024 and is expected to reach USD 66.12 billion by 2032, at a CAGR of 6.20% during the forecast period

- The market growth is largely fuelled by the increasing demand for high-performance electronic components across applications such as consumer electronics, automotive, and telecommunications, particularly in 5G and electric vehicle (EV) technologies

- In addition, advancements in power electronics, growing use in renewable energy systems, and the rise in demand for optoelectronic devices further contribute to the market expansion

Compound Semiconductor Market Analysis

- Compound semiconductors, which include materials such as gallium nitride (GaN), gallium arsenide (GaAs), silicon carbide (SiC), and indium phosphide (InP), are gaining prominence due to their superior properties including high electron mobility, thermal conductivity, and frequency performance

- The market is experiencing rapid growth in segments such as radio frequency (RF) communication, power electronics, and photonics, where traditional silicon-based semiconductors fall short

- North America dominated the compound semiconductor market with the largest revenue share of 38.2% in 2024, driven by strong demand from automotive, defense, and telecommunication sectors

- Asia-Pacific region is expected to witness the highest growth rate in the global compound semiconductor market, driven by large-scale adoption of smartphones, electric vehicles, and renewable energy systems in countries such as China, Japan, South Korea, and India

- The III-V compound semiconductors segment accounted for the largest market revenue share in 2024, driven by their high electron mobility and direct bandgap properties, which make them ideal for high-speed and optoelectronic applications. These materials, such as gallium arsenide and indium phosphide, are widely used in radio frequency devices, LEDs, and photovoltaic cells. Their efficiency in high-frequency and high-power conditions contributes significantly to their demand across telecom and aerospace industries

Report Scope and Compound Semiconductor Market Segmentation

|

Attributes |

Compound Semiconductor Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Compound Semiconductor Market Trends

“Surging Demand for Gallium Nitride (GaN) and Silicon Carbide (SiC) in Power Electronics”

- Compound semiconductors such as gallium nitride (GaN) and silicon carbide (SiC) are increasingly being used in power electronics due to their superior efficiency and performance over traditional silicon, especially in high-voltage and high-frequency environments

- The rising adoption of electric vehicles has significantly accelerated the demand for SiC and GaN components, as automakers seek solutions that reduce energy loss and improve overall system reliability

- These materials are also facilitating the miniaturization of electronic devices by enabling compact, lightweight, and thermally stable designs, which are especially useful in consumer electronics and telecom hardware

- Renewable energy sectors, including solar and wind, are incorporating compound semiconductors into power conversion systems to enhance grid efficiency and lower maintenance costs

- For instance, Tesla integrated SiC-based inverters in its Model 3 to improve energy efficiency, reduce heat, and extend vehicle range

Compound Semiconductor Market Dynamics

Driver

“Expansion of 5G Infrastructure and High-Frequency Applications”

- Compound semiconductors are a key enabler in 5G networks as they provide the high-frequency performance needed for power amplifiers and antenna modules used in base stations and mobile devices

- The growth of IoT and connected devices is increasing demand for low-latency, high-bandwidth communication systems, which depend on compound semiconductors for fast and reliable signal transmission

- Governments in countries such as the U.S., China, and South Korea are investing heavily in 5G infrastructure, creating a positive ripple effect for semiconductor materials that meet RF and millimeter-wave requirements

- Compound semiconductors are also supporting satellite communication and radar systems by offering higher breakdown voltage and temperature tolerance than conventional silicon components

- For instance, GaN-based RF components are being deployed in 5G base stations to deliver better performance with lower energy consumption

Restraint/Challenge

“High Cost of Material Production and Complex Manufacturing Processes”

- The cost of producing compound semiconductors remains significantly higher than that of traditional silicon due to expensive raw materials and specialized fabrication processes

- Wafer fragility and the need for precise cutting, polishing, and packaging contribute to low manufacturing yields and higher overall defect rates in compound semiconductor production

- There is a limited number of fabrication facilities globally that can handle GaN, SiC, or InP wafers, leading to supply constraints and long lead times for manufacturers

- Small and medium enterprises often struggle to enter the compound semiconductor market because of the high capital investment and technical expertise required for production

- For instance, the brittle nature of SiC wafers increases the risk of damage during handling and processing, adding to production cost and complexity

Compound Semiconductor Market Scope

The market is segmented on the basis of type, product, deposition technologies, and application.

• By Type

On the basis of type, the compound semiconductor market is segmented into III-V compound semiconductors, II-VI compound semiconductors, sapphire, IV-IV compound semiconductors, and others. The III-V compound semiconductors segment accounted for the largest market revenue share in 2024, driven by their high electron mobility and direct bandgap properties, which make them ideal for high-speed and optoelectronic applications. These materials, such as gallium arsenide and indium phosphide, are widely used in radio frequency devices, LEDs, and photovoltaic cells. Their efficiency in high-frequency and high-power conditions contributes significantly to their demand across telecom and aerospace industries.

The sapphire segment is expected to witness the fastest growth rate from 2025 to 2032, fuelled by its increasing application as a substrate in LED production and its exceptional thermal stability. Sapphire’s durability, high optical transparency, and compatibility with gallium nitride (GaN) deposition make it highly suitable for displays and optical components in both consumer electronics and defense systems.

• By Product

On the basis of product, the market is segmented into LED, optoelectronics, RF devices, and power electronics. The LED segment held the largest market revenue share in 2024, supported by growing demand for energy-efficient lighting, backlighting in displays, and automotive lighting applications. LEDs based on compound semiconductors offer longer lifespan, higher brightness, and lower energy consumption, contributing to widespread adoption in both commercial and residential settings.

The RF devices segment is expected to witness the fastest growth rate from 2025 to 2032, driven by increasing usage in 5G base stations, satellite communication, and defense applications. The ability of compound semiconductors to operate at high frequencies with minimal signal loss positions RF devices as a vital component in modern communication infrastructure.

• By Deposition Technologies

On the basis of deposition technologies, the market is segmented into chemical vapor deposition (CVD), molecular beam epitaxy, hydride vapor phase epitaxy (HVPE), ammonothermal, liquid phase epitaxy, atomic layer deposition (ALD), and others. The CVD segment dominated the market in 2024, owing to its widespread use in large-scale, high-purity semiconductor production. CVD processes allow precise control of material thickness and uniformity, making it suitable for fabricating high-performance optoelectronic and power devices.

The molecular beam epitaxy segment is expected to witness the fastest growth rate from 2025 to 2032, attributed to its ability to produce ultra-pure and highly controlled crystal structures used in advanced research and high-speed electronic devices. Its precision and adaptability support growing demand in aerospace, research institutions, and niche microelectronic manufacturing.

• By Application

On the basis of application, the compound semiconductor market is segmented into general lighting, telecommunication, military, defense, and aerospace, automotive, power supply, datacom, commercial, consumer display, consumer devices, and others. The telecommunication segment accounted for the largest revenue share in 2024, driven by rapid deployment of 5G infrastructure and increasing data consumption globally. Compound semiconductors such as GaN and GaAs are critical to producing high-frequency, high-efficiency components used in network systems.

The automotive segment is expected to witness the fastest growth rate from 2025 to 2032, fuelled by rising adoption of electric vehicles and autonomous systems. Compound semiconductors offer superior thermal conductivity, power efficiency, and miniaturization, which are vital for next-generation automotive powertrains, radar systems, and infotainment modules.

Compound Semiconductor Market Regional Analysis

- North America dominated the compound semiconductor market with the largest revenue share of 38.2% in 2024, driven by strong demand from automotive, defense, and telecommunication sectors

- The region benefits from the presence of major industry players, high adoption of electric vehicles, and significant investment in 5G infrastructure and smart devices

- In addition, rising emphasis on energy efficiency and high-frequency electronics continues to support the growing use of compound semiconductors in North America

U.S. Compound Semiconductor Market Insight

The U.S. compound semiconductor market accounted for the highest revenue share of over 79% in 2024 within North America, propelled by robust demand across aerospace, 5G telecommunications, and power electronics sectors. The market is benefiting from the government’s increasing support for domestic chip manufacturing and the strategic importance of semiconductors in defense applications. Further, rapid developments in silicon carbide (SiC) and gallium nitride (GaN) technologies are spurring innovation, especially in electric vehicle powertrains and renewable energy systems. The presence of leading chip manufacturers and growing research and development investments are enhancing the market’s technological advancement and commercial adoption.

Europe Compound Semiconductor Market Insight

The Europe compound semiconductor market is expected to witness the fastest growth rate from 2025 to 2032, supported by growth in renewable energy systems, high-speed rail, and industrial automation. The region is experiencing increasing adoption of wide bandgap materials in power devices and optoelectronics for use in smart grids, automotive safety, and clean energy technologies. European Union initiatives focused on green technology adoption and digital transformation are further accelerating the shift toward compound semiconductor-based solutions in power conversion and high-speed communication systems.

Germany Compound Semiconductor Market Insight

The Germany compound semiconductor market is expected to witness the fastest growth rate from 2025 to 2032, driven by the country’s leadership in the automotive and industrial manufacturing sectors. Germany is actively integrating compound semiconductor components such as GaN and SiC into electric vehicle infrastructure, power supplies, and industrial equipment. The country's strong research ecosystem and strategic investment in semiconductor fabrication facilities are also contributing to greater innovation and self-reliance in the technology supply chain. Furthermore, Germany's push toward carbon neutrality is aligning with the increased use of energy-efficient semiconductor materials in power electronics.

U.K. Compound Semiconductor Market Insight

The U.K. compound semiconductor market is expected to witness the fastest growth rate from 2025 to 2032, driven by rising investments in advanced electronics and increasing demand for high-performance power devices. The country’s focus on developing next-generation communication systems, particularly 5G and future 6G networks, is enhancing the adoption of compound semiconductors such as gallium arsenide (GaAs) and gallium nitride (GaN). Government-backed initiatives such as the Compound Semiconductor Applications (CSA) Catapult in Wales are playing a pivotal role in fostering innovation and commercialization. In addition, the U.K.’s growing electric vehicle sector and renewable energy infrastructure are further contributing to the integration of energy-efficient semiconductor materials in power management, radar systems, and optoelectronic applications.

Asia-Pacific Compound Semiconductor Market Insight

The Asia-Pacific compound semiconductor market is expected to witness the fastest growth rate from 2025 to 2032, driven by rapid technological advancements, expanding 5G networks, and surging demand for electric vehicles in China, South Korea, Japan, and India. APAC benefits from a strong manufacturing base, favorable government policies, and increasing foreign investments in semiconductor production. Growing usage of LED lighting, advanced consumer electronics, and smartphone applications across emerging economies is also significantly contributing to market expansion.

China Compound Semiconductor Market Insight

The China compound semiconductor market captured the highest revenue share in Asia-Pacific in 2024, attributed to the country’s extensive industrial base, robust 5G rollout, and dominance in consumer electronics manufacturing. The Chinese government’s continued investment in chip fabrication and localization efforts are further stimulating market demand. Compound semiconductors are increasingly being deployed in China’s smart city projects, EV charging infrastructure, and power distribution systems, establishing China as a global leader in the application of these technologies.

Japan Compound Semiconductor Market Insight

The Japan compound semiconductor market is expected to witness the fastest growth rate from 2025 to 2032, supported by advancements in optoelectronics, automotive, and medical electronics applications. Japan’s expertise in precision manufacturing and materials engineering is helping drive adoption of advanced semiconductors in high-reliability environments. The growing need for compact, energy-efficient components in electronics and the nation’s increasing investments in 6G research are expected to enhance future demand. In addition, Japan’s automotive sector is leveraging SiC and GaN solutions to improve vehicle performance and energy efficiency in hybrid and electric vehicle systems.

Compound Semiconductor Market Share

The compound semiconductor industry is primarily led by well-established companies, including:

- NICHIA CORPORATION (Japan)

- Qorvo, Inc. (U.S.)

- SAMSUNG (South Korea)

- ams-OSRAM AG.(Austria)

- Skyworks Solutions, Inc. (U.S.)

- Cree LED, an SGH company. (U.S.)

- Infineon Technologies AG (Germany)

- STMicroelectronics (Switzerland)

- TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION (Japan)

- Broadcom (U.S.)

- Lumentum Operations LLC (U.S.)

- NXP Semiconductors (Netherlands)

- Sumitomo Electric Industries, Ltd. (Japan)

- Renesas Electronics Corporation (Japan)

- Microchip Technology Inc. (U.S.)

- Efficient Power Conversion Corporation (U.S.)

- Mitsubishi Electric Corporation (Japan)

Latest Developments in Global Compound Semiconductor Market

- In 2022, Infineon Technologies AG and II-VI Incorporated solidified a strategic multiyear supply agreement for wafers, bolstering Infineon's access to critical semiconductor material. This collaboration was crucial in meeting heightened customer demand within the sector, reinforcing Infineon's multi-sourcing strategy and fortifying the resilience of its supply chain

- In 2022, Qorvo launched its latest innovation, the UF4C/SC series, representing the fourth generation of 1200V SiCFETs. Derived from recently acquired UnitedSiC technology, these SiCFETs were tailored for 800V bus architectures. Targeting applications such as electric vehicle onboard chargers, industrial battery chargers, and solar inverters, this release signified Qorvo's commitment to advancing power electronics for various industrial and renewable energy sectors

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Compound Semiconductor Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Compound Semiconductor Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Compound Semiconductor Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.