Global Computational Storage Market

Market Size in USD Million

USD

750.00 Million

USD

5,645.33 Million

2025

2033

USD

750.00 Million

USD

5,645.33 Million

2025

2033

| 2026 - 2033 | |

| USD 750.00 Million | |

| USD 5,645.33 Million | |

| % | |

|

What is the Global Computational Storage Market Size and Growth Rate?

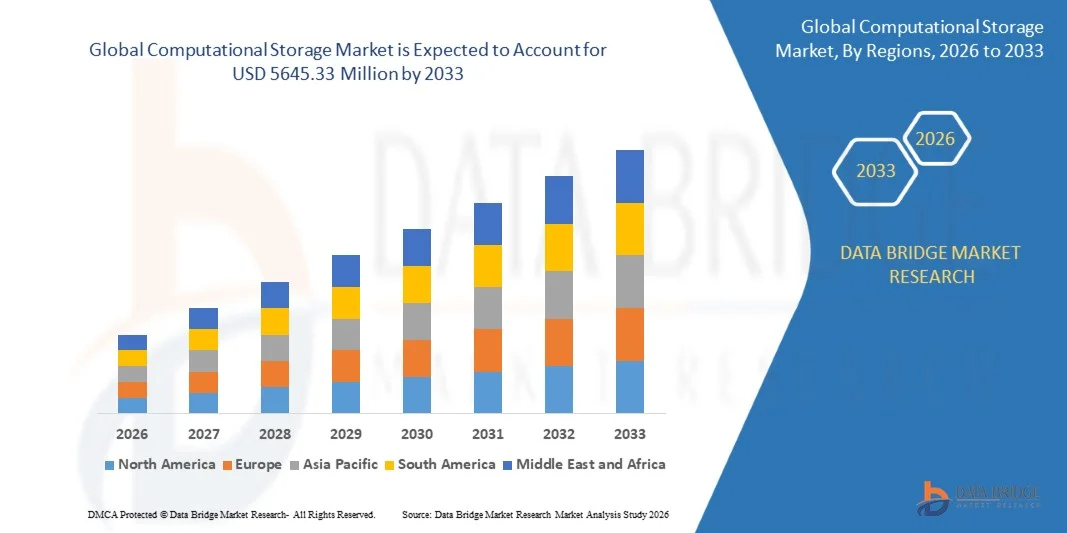

- The global computational storage market size was valued at USD 750 million in 2025 and is expected to reach USD 5645.33 million by 2033, at a CAGR of 28.70% during the forecast period

- Increasing demand for high-speed data processing, low-latency storage architectures, and energy-efficient data center infrastructure, along with rising deployment of AI workloads, edge computing, cloud storage platforms, and real-time analytics solutions, are some of the major as well as vital factors which will such asly augment the growth of the Computational Storage market

What are the Major Takeaways of Computational Storage Market?

- Growing demand for AI-driven applications, hyperscale data centers, enterprise storage modernization, and cloud service provider infrastructure across developing economies, along with rising number of research and development activities, will further contribute by generating massive opportunities that will lead to the growth of the computational storage market

- Lack of skilled system integration expertise, interoperability challenges, high initial deployment costs, design complexities, and system interaction issues will such asly act as major market restraint factors for the growth of the Computational Storage market

- North America dominated the computational storage market with a 41.0% revenue share in 2025, driven by strong growth in hyperscale data centers, enterprise cloud infrastructure, AI workloads, and high-performance computing environments across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 26.5% from 2026 to 2033, driven by rapid expansion in data center capacity, cloud services, AI adoption, and digital transformation initiatives across China, Japan, India, South Korea, and Southeast Asia

- The Hardware segment dominated the market with a 64.8% share in 2025, as it remains the core component of computational storage architecture, including computational storage drives (CSDs), storage processing units (SPUs), SSD controllers, and accelerator-enabled storage devices

Report Scope and Computational Storage Market Segmentation

|

Attributes |

Computational Storage Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Computational Storage Market?

“Increasing Shift Toward AI-Driven, Near-Data Processing and Programmable Storage Architectures”

- The computational storage market is witnessing strong adoption of near-data processing solutions, intelligent SSDs, and programmable storage devices designed to reduce latency and improve workload efficiency across data-intensive environments

- Manufacturers are introducing computational storage drives (CSDs), storage processing units (SPUs), and programmable storage controllers that offer advanced data compression, encryption, analytics acceleration, and real-time inference capabilities

- Growing demand for power-efficient, low-latency, and scalable storage infrastructure is driving usage across enterprise data centers, hyperscale cloud platforms, edge computing systems, and AI workloads

- For instance, companies such as Intel Corporation, Samsung Electronics, Marvell Technology, and ScaleFlux have upgraded their storage solutions with embedded compute capabilities, compression engines, and workload-specific acceleration

- Increasing need for rapid AI inference, real-time analytics, and reduced CPU bottlenecks is accelerating the shift toward programmable and intelligent storage systems

- As data volumes become more complex and compute-intensive, Computational Storage will remain vital for high-performance data processing, infrastructure efficiency, and scalable AI deployments

What are the Key Drivers of Computational Storage Market?

- Rising demand for real-time data processing, AI acceleration, and efficient storage utilization to support rapid analytics and large-scale data workloads is a major growth driver

- For instance, in 2025–2026, leading companies such as Intel Corporation, Samsung Electronics, and Advanced Micro Devices expanded their storage and compute portfolios to support higher throughput, intelligent offloading, and programmable architectures

- Growing adoption of AI workloads, machine learning, cloud data centers, edge computing, and IoT ecosystems is boosting demand across the U.S., Europe, and Asia-Pacific

- Advancements in storage controllers, FPGA-based acceleration, data compression, and near-data computing architectures have strengthened performance, scalability, and energy efficiency

- Rising use of large language models, hyperscale storage environments, and real-time business intelligence systems is creating demand for intelligent and programmable storage device

- Supported by steady investments in AI infrastructure, cloud modernization, and enterprise digital transformation, the Computational Storage market is expected to witness strong long-term growth

Which Factor is Challenging the Growth of the Computational Storage Market?

- High costs associated with advanced computational storage drives, programmable controllers, and AI-integrated storage systems restrict adoption among small enterprises and cost-sensitive organizations

- For instance, during 2025–2026, fluctuations in NAND flash, DRAM, and storage component prices, along with supply shortages, increased device manufacturing and deployment costs for several global vendors

- Complexity in integrating compute-enabled storage with legacy infrastructure, data pipelines, and enterprise software ecosystems increases the need for skilled engineers and training

- Limited awareness in emerging markets regarding near-data processing benefits, workload optimization, and storage programmability slows adoption

- Competition from traditional SSDs, cloud-native storage architectures, and GPU-centric acceleration frameworks creates pricing pressure and reduces product differentiation

- To address these issues, companies are focusing on cost-optimized architectures, software-defined integration, and AI-driven storage analytics to increase global adoption of Computational Storage

How is the Computational Storage Market Segmented?

The market is segmented on the basis of offering, type, and end-use industry.

• By Offering

On the basis of offering, the computational storage market is segmented into Hardware and Software. The Hardware segment dominated the market with a 64.8% share in 2025, as it remains the core component of computational storage architecture, including computational storage drives (CSDs), storage processing units (SPUs), SSD controllers, and accelerator-enabled storage devices. These hardware solutions are widely adopted across enterprise data centers, hyperscale cloud platforms, and edge computing infrastructure due to their ability to perform near-data processing, compression, encryption, and AI inference tasks directly within the storage layer. Rising demand for low-latency data movement and reduced CPU dependency continues to strengthen segment dominance.

The Software segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by increasing adoption of storage orchestration platforms, AI workload optimization tools, data pipeline software, and programmable firmware ecosystems. Growing need for software-defined storage intelligence and seamless infrastructure integration is accelerating growth.

• By Type

On the basis of type, the market is segmented into Fixed Computational Storage and Programmable Computational Storage. The Fixed Computational Storage segment dominated the market with a 57.2% share in 2025, supported by its strong adoption in pre-configured enterprise storage appliances, data compression systems, encryption-enabled drives, and workload-specific acceleration devices. These solutions offer optimized performance for repetitive, high-volume workloads such as database acceleration, video transcoding, and real-time analytics. Their standardized architecture and deployment simplicity make them highly suitable for enterprise and hyperscale environments.

The Programmable Computational Storage segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for custom AI inference, machine learning acceleration, workload-specific programmability, and flexible storage processing architectures. Rising use of programmable controllers, FPGA-enabled drives, and software-defined compute storage frameworks is expected to significantly accelerate segment expansion.

• By End-Use Industry

On the basis of end-use industry, the Computational Storage market is segmented into Enterprise Storage, Government, and CSP. The Enterprise Storage segment dominated the market with a 49.6% share in 2025, driven by extensive use across large-scale data centers, enterprise cloud environments, AI workloads, and business-critical storage infrastructure. Enterprises increasingly rely on computational storage solutions for real-time analytics, faster database processing, reduced network traffic, and improved power efficiency. Growing digital transformation initiatives and rising demand for intelligent storage architectures continue to strengthen this segment.

The CSP (Cloud Service Provider) segment is expected to grow at the fastest CAGR from 2026 to 2033, propelled by rapid expansion of hyperscale cloud infrastructure, edge cloud services, AI data lakes, and high-performance storage clusters. Increasing deployment of computational storage in multi-tenant cloud ecosystems is driving strong long-term growth.

Which Region Holds the Largest Share of the Computational Storage Market?

- North America dominated the computational storage market with a 41.0% revenue share in 2025, driven by strong growth in hyperscale data centers, enterprise cloud infrastructure, AI workloads, and high-performance computing environments across the U.S. and Canada. High adoption of computational storage drives (CSDs), storage processing units (SPUs), edge computing frameworks, and real-time analytics platforms continues to fuel demand across enterprise IT, telecom networks, BFSI, and government data infrastructure

- Leading companies in North America are introducing AI-enabled storage architectures, programmable controllers, and near-data processing solutions, strengthening the region’s technological advantage. Continuous investment in cloud modernization, data center expansion, and machine learning infrastructure drives long-term market expansion

- High concentration of leading technology companies, strong innovation ecosystems, and sustained investment in advanced digital infrastructure further reinforce regional market leadership

U.S. Computational Storage Market Insight

The U.S. is the largest contributor in North America, supported by strong AI infrastructure investments, hyperscale cloud platforms, and enterprise storage modernization initiatives. Increasing deployment of AI accelerators, large language model training clusters, edge data centers, and real-time data analytics systems intensifies demand for computational storage solutions capable of low-latency processing and reduced CPU bottlenecks. Presence of major technology companies, strong startup ecosystems, and high demand for advanced storage solutions further drives market growth.

Canada Computational Storage Market Insight

Canada contributes significantly to regional growth, driven by expanding cloud infrastructure, enterprise IT transformation, and public sector digitalization projects. Data centers and research institutions increasingly utilize computational storage for AI workloads, big data processing, and secure enterprise storage environments. Government-supported innovation programs, skilled workforce availability, and rising adoption of cloud-native technologies strengthen market adoption across the country.

Asia-Pacific Computational Storage Market

Asia-Pacific is projected to register the fastest CAGR of 26.5% from 2026 to 2033, driven by rapid expansion in data center capacity, cloud services, AI adoption, and digital transformation initiatives across China, Japan, India, South Korea, and Southeast Asia. High-volume deployment of enterprise IT systems, telecom infrastructure, IoT ecosystems, and AI-enabled applications increases demand for efficient near-data processing solutions. Growth in 5G, smart cities, and edge computing continues to accelerate the need for intelligent storage architectures across engineering and business applications.

China Computational Storage Market Insight

China is the largest contributor to Asia-Pacific due to massive data center investments, cloud expansion, and government-backed digital infrastructure initiatives. Rising development of AI clusters, hyperscale storage platforms, and enterprise cloud ecosystems drives demand for computational storage solutions with higher performance and scalability. Local manufacturing capabilities and competitive pricing further expand domestic and export market adoption.

Japan Computational Storage Market Insight

Japan shows steady growth supported by advanced enterprise IT infrastructure, cloud adoption, and industrial digitalization systems. Strong focus on data security, low-latency processing, and enterprise reliability drives adoption of premium computational storage solutions. Increasing need for AI-driven business analytics and high-performance data environments reinforces long-term market expansion.

India Computational Storage Market Insight

India is emerging as a major growth hub, driven by expanding data center construction, cloud adoption, startup activity, and government-backed digital transformation initiatives. Growing demand for enterprise storage, AI workloads, telecom data processing, and cloud-native infrastructure fuels adoption of computational storage solutions. Increasing R&D investments and digital infrastructure expansion further accelerate market penetration.

South Korea Computational Storage Market Insight

South Korea contributes significantly due to strong demand for advanced memory technologies, AI servers, 5G systems, and enterprise cloud platforms. Rapid development of AI infrastructure and semiconductor innovation drives adoption of computational storage with high-speed data processing and intelligent workload acceleration capabilities. Technological innovation, strong manufacturing capacity, and growing digital ecosystems support sustained market growth

Which are the Top Companies in Computational Storage Market?

The computational storage industry is primarily led by well-established companies, including:

- Intel Corporation (U.S.)

- NGD Systems (U.S.)

- ScaleFlux (U.S.)

- Eideticom (Canada)

- Marvell Technology (U.S.)

- NETINT Technologies (Canada)

- Advanced Micro Devices (AMD) (U.S.)

- Pliops (Israel)

- Samsung Electronics Co., Ltd. (South Korea)

- ARM (U.K.)

What are the Recent Developments in Global Computational Storage Market?

- In December 2025, AMD expanded its collaborations with storage vendors, OEMs, and cloud service providers to strengthen computational storage architectures through advanced reference designs and optimized platform solutions, accelerating deployment across enterprise and hyperscale data centers. This development is expected to enhance ecosystem compatibility and support long-term market growth

- In July 2024, a new high-performance NVMe CSD5000 series was introduced, powered by the FX5016 PCIe 5 SSD controller specifically designed for AI, cloud, and data center workloads, marking a major milestone in storage performance and capacity enhancement. This launch is anticipated to significantly boost demand for next-generation computational storage solutions

- In August 2023, AMD upgraded its ROCm software platform to support broader heterogeneous computing capabilities and stronger integration with data-centric workloads, enabling improved coordination between CPUs, accelerators, and storage-adjacent compute environments. This advancement is such asly to strengthen computational efficiency and expand enterprise adoption

- In July 2022, Samsung introduced its SmartSSD solution, integrating Xilinx FPGA-based processing with high-capacity NAND flash to enable in-storage data processing, including tasks such as data filtering, compression, and analytics offloading from the host CPU. This innovation is expected to improve data center performance and reduce data movement overhead significantly

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.