Global Computer Vision Technologies Market

Market Size in USD Billion

USD

17.60 Billion

USD

33.30 Billion

2025

2033

USD

17.60 Billion

USD

33.30 Billion

2025

2033

| 2026 - 2033 | |

| USD 17.60 Billion | |

| USD 33.30 Billion | |

| % | |

|

Computer Vision Technologies Market Size

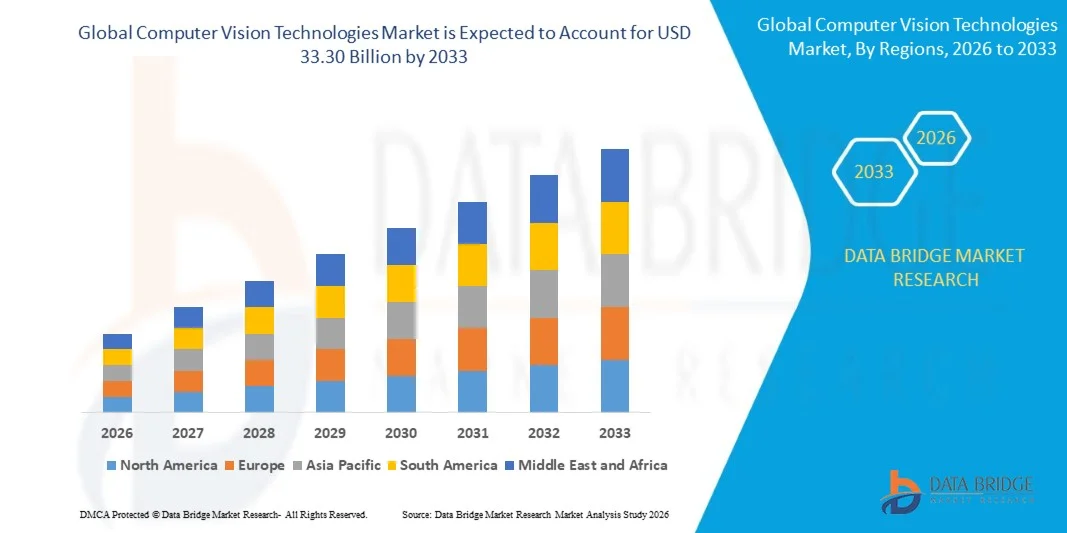

- The global computer vision technologies market size was valued at USD 17.60 billion in 2025 and is expected to reach USD 33.30 billion by 2033, at a CAGR of 8.3% during the forecast period

- The market growth is largely fueled by the increasing adoption of AI, machine learning, and deep learning technologies across industries, driving the implementation of computer vision solutions for automation, quality inspection, surveillance, and analytics

- Furthermore, rising demand for real-time visual intelligence, enhanced operational efficiency, and error reduction in manufacturing, logistics, retail, and healthcare sectors is establishing computer vision as a critical technology for industrial and non-industrial applications. These factors are accelerating the deployment of vision-based systems, thereby significantly boosting the market's growth

Computer Vision Technologies Market Analysis

- Computer vision technologies involve the use of cameras, sensors, AI algorithms, and software to capture, process, and interpret visual data, enabling machines to perform tasks that typically require human vision. These systems are widely applied in robotics, autonomous vehicles, industrial automation, healthcare diagnostics, and smart surveillance

- The escalating demand for computer vision is primarily driven by increasing automation in industrial processes, the need for accurate and fast quality inspection, growing adoption of AI-enabled devices, and the push for smart infrastructure in both commercial and residential sectors

- North America dominated the computer vision technologies market with a share of 38.19% in 2025, due to growing adoption of AI and automation across industries, as well as increased investment in advanced surveillance, robotics, and smart manufacturing solutions

- Asia-Pacific is expected to be the fastest growing region in the computer vision technologies market during the forecast period due to rapid industrialization, technological advancement, and rising adoption of AI-powered automation in countries such as China, Japan, and India

- Software segment dominated the market with a market share of 61.5% in 2025, due to the increasing reliance on advanced algorithms, AI-powered analytics, and deep learning models for image and video processing. Software solutions are crucial for applications such as object detection, defect inspection, and autonomous decision-making in both industrial and non-industrial environments

Report Scope and Computer Vision Technologies Market Segmentation

|

Attributes |

Computer Vision Technologies Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Computer Vision Technologies Market Trends

“Increasing Adoption of AI-Powered Image and Video Analysis”

- A significant trend in the computer vision technologies market is the rising adoption of AI-powered image and video analysis across multiple sectors, driven by the need for automated, accurate, and real-time visual data processing. This trend is expanding the application of computer vision from industrial automation to retail analytics, enhancing operational efficiency and decision-making

- For instance, NVIDIA provides AI-enabled computer vision platforms that are widely implemented in autonomous driving, smart retail, and manufacturing inspection systems. These solutions improve object recognition, anomaly detection, and predictive analytics, supporting faster and more reliable operational workflows

- The integration of computer vision into autonomous vehicles is accelerating, where image recognition, depth sensing, and environmental analysis are critical for navigation and safety systems. This is positioning computer vision as a core enabler for advanced driver-assistance systems (ADAS) and fully autonomous mobility solutions

- Healthcare providers are increasingly adopting computer vision for diagnostic imaging, patient monitoring, and surgical assistance, where AI algorithms enhance image clarity and interpretation. Such applications are driving innovation in non-invasive procedures and enabling real-time medical decision-making

- Retail and e-commerce sectors are leveraging computer vision to optimize customer experience, track shopper behavior, and automate checkout systems. This trend is enhancing personalized marketing, inventory management, and store efficiency across global retail operations

- The industrial and manufacturing sectors are implementing computer vision for quality inspection, predictive maintenance, and process automation, where cameras and sensors detect defects and operational inefficiencies. This rising incorporation of AI-driven visual analytics is reinforcing digital transformation initiatives across industries

Computer Vision Technologies Market Dynamics

Driver

“Rising Integration of Computer Vision in Autonomous Vehicles”

- The growing focus on autonomous driving and advanced driver-assistance systems is driving the integration of computer vision technologies that support real-time object detection, lane tracking, and traffic analysis. These technologies enhance vehicle safety, navigation, and operational reliability

- For instance, Mobileye, an Intel company, provides computer vision-based ADAS and autonomous driving solutions widely adopted by automotive manufacturers such as BMW and Nissan. Their AI-powered vision systems enable precise detection of pedestrians, vehicles, and road signs, supporting safer and more efficient driving

- The adoption of robotics and automation in industrial settings is also boosting demand for computer vision solutions that facilitate precise object recognition, sorting, and operational monitoring. This is enabling manufacturers to optimize processes and reduce human error in high-volume production

- Smart city initiatives are increasingly relying on computer vision for traffic management, public safety, and infrastructure monitoring, where AI-based cameras enhance surveillance and analytics. Such deployments improve urban mobility, security, and resource efficiency

- The rapid evolution of AI algorithms, machine learning models, and sensor technologies is strengthening the driver, as advanced software and hardware enable more accurate, faster, and scalable visual analysis. This continuous innovation is expanding the use of computer vision across emerging applications

Restraint/Challenge

“High Computational and Implementation Costs”

- The computer vision technologies market faces challenges due to the high computational requirements and implementation costs associated with AI-driven image and video analysis. Advanced GPUs, specialized sensors, and large-scale data storage contribute to significant capital expenditure and operational expenses

- For instance, companies such as NVIDIA and Intel offer high-performance vision processing units, but the investment in hardware and software integration remains substantial for small and medium enterprises. These cost considerations can slow adoption and limit accessibility across sectors

- Developing and deploying computer vision systems require extensive training datasets, annotation processes, and continuous model optimization, which adds to the operational complexity. These requirements increase time-to-market and resource consumption for companies

- Integration with existing IT and operational systems can be challenging, especially when deploying computer vision at scale across multiple locations or platforms. Compatibility, network bandwidth, and cybersecurity considerations further elevate costs and complexity

- Maintaining system accuracy, reliability, and scalability over time necessitates ongoing software updates, hardware upgrades, and technical support. These sustained requirements place additional financial and operational pressure on organizations seeking to implement computer vision solutions

Computer Vision Technologies Market Scope

The market is segmented on the basis of component, application, end-user, product, and deployment.

• By Component

On the basis of component, the computer vision technologies market is segmented into software and hardware. The software segment dominated the largest market revenue share of 61.5% in 2025, driven by the increasing reliance on advanced algorithms, AI-powered analytics, and deep learning models for image and video processing. Software solutions are crucial for applications such as object detection, defect inspection, and autonomous decision-making in both industrial and non-industrial environments. Their flexibility allows easy integration with different hardware platforms, cameras, and sensors, enhancing operational efficiency. Enterprises also prefer software-centric solutions for scalability and frequent updates that improve accuracy and performance over time.

The hardware segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising deployment of high-resolution cameras, edge computing devices, and GPU-enabled processors. For instance, NVIDIA provides hardware solutions optimized for real-time AI inference in industrial automation and robotics. Growing adoption of embedded vision systems, smart sensors, and robotics accelerates hardware demand across sectors, as these components are critical for real-time processing and edge-level analytics.

• By Application

On the basis of application, the computer vision technologies market is segmented into face recognition, gesture recognition, character recognition, and others. The face recognition segment dominated the largest market revenue share in 2025, driven by its widespread use in security, surveillance, and identity verification systems. Face recognition technology is increasingly integrated into smartphones, airports, banking services, and access control systems for quick and accurate authentication. Its ability to provide real-time identification with AI-powered accuracy makes it indispensable for both enterprise and government applications, enhancing safety and operational efficiency.

The gesture recognition segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising adoption in AR/VR devices, gaming, human-computer interfaces, and industrial automation. For instance, Leap Motion has developed gesture-based control solutions for immersive virtual experiences and touchless operations. Growing demand for contactless interaction and intuitive controls in consumer electronics, healthcare, and smart factories drives the rapid expansion of gesture recognition technologies.

• By End-User

On the basis of end-user, the computer vision technologies market is segmented into industrial and non-industrial sectors. The industrial segment dominated the largest market revenue share in 2025, driven by the increasing deployment of computer vision in manufacturing for quality inspection, process automation, and predictive maintenance. Industries such as automotive, electronics, and pharmaceuticals leverage computer vision to reduce errors, enhance throughput, and improve safety standards. Integration with robotics, IoT platforms, and AI-driven analytics further strengthens computer vision adoption in smart factories and large-scale industrial applications.

The non-industrial segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by adoption in healthcare, retail, smart cities, and public safety applications. For instance, Amazon uses computer vision in its cashier-less stores to track customer behavior and optimize operations. The rising need for automation, contactless monitoring, and AI-powered analytics in non-industrial domains accelerates growth in healthcare diagnostics, security, and personalized consumer experiences.

• By Product

On the basis of product, the computer vision technologies market is segmented into PC-based computer vision systems and smart camera-based computer vision systems. The smart camera-based systems segment dominated the largest market revenue share in 2025, driven by the ease of installation, embedded processing capabilities, and ability to perform real-time analytics at the edge. Smart cameras reduce latency and bandwidth requirements while enabling deployment across surveillance, industrial inspection, and robotic applications. Their compatibility with AI frameworks and IoT devices makes them suitable for diverse industrial and non-industrial environments.

The PC-based computer vision systems segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for high-performance computing capable of handling complex AI workloads. For instance, Intel provides PC-based platforms optimized for machine learning and computer vision in robotics and industrial automation. Adoption in robotic cells, autonomous systems, and large-scale industrial environments drives the expansion of PC-based systems due to their flexibility and superior processing power.

• By Deployment

On the basis of deployment, the computer vision technologies market is segmented into general and robotic cell deployments. The general deployment segment dominated the largest market revenue share in 2025, fueled by its application in conventional manufacturing, surveillance, retail analytics, and non-specialized automation. General deployment offers easy integration with existing systems, providing cost-effective and scalable solutions for a broad range of tasks such as quality inspection, monitoring, and anomaly detection. Its flexibility allows industries to implement computer vision without major infrastructure changes, supporting gradual adoption.

The robotic cell deployment segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing use of computer vision in collaborative robots (cobots) and autonomous production lines. For instance, Fanuc integrates vision systems in robotic cells for precise material handling and inspection. Rising demand for automation, accuracy, and real-time decision-making in smart manufacturing and high-precision industrial tasks accelerates adoption of robotic cell computer vision deployments.

Computer Vision Technologies Market Regional Analysis

- North America dominated the computer vision technologies market with the largest revenue share of 38.19% in 2025, driven by growing adoption of AI and automation across industries, as well as increased investment in advanced surveillance, robotics, and smart manufacturing solutions

- Organizations in the region increasingly rely on computer vision for applications such as quality inspection, predictive maintenance, and automated monitoring in manufacturing and logistics

- High technology adoption rates, robust R&D infrastructure, and a strong focus on Industry 4.0 initiatives further support widespread implementation of computer vision solutions across industrial and non-industrial sectors

U.S. Computer Vision Technologies Market Insight

The U.S. computer vision technologies market captured the largest revenue share in North America in 2025, fueled by the rapid deployment of AI-powered industrial automation and intelligent surveillance systems. Enterprises are prioritizing the integration of computer vision into robotics, quality inspection, and process monitoring to improve operational efficiency. The growing adoption of smart cameras, cloud-based vision analytics, and AI-driven software platforms further propels market growth. In addition, collaborations between tech companies and industrial firms to develop customized computer vision solutions are accelerating market expansion in the U.S.

Europe Computer Vision Technologies Market Insight

The Europe computer vision technologies market is projected to grow at a substantial CAGR during the forecast period, primarily driven by increasing industrial automation, stringent safety regulations, and the need for advanced monitoring in manufacturing and logistics. European enterprises are integrating computer vision with robotics, AI, and IoT platforms to improve productivity and reduce operational errors. The region is witnessing significant growth in applications across industrial, retail, healthcare, and smart city projects, supporting the adoption of computer vision systems in both new setups and upgrades.

U.K. Computer Vision Technologies Market Insight

The U.K. computer vision technologies market is expected to grow at a notable CAGR, driven by digital transformation initiatives and increasing automation across manufacturing, retail, and public safety sectors. Concerns regarding workplace safety, process optimization, and operational efficiency are encouraging enterprises to adopt AI-enabled vision solutions. The U.K.’s well-established IT and e-commerce infrastructure further supports deployment, enabling integration with cloud services, smart cameras, and analytics platforms.

Germany Computer Vision Technologies Market Insight

The Germany computer vision technologies market is expected to expand at a significant CAGR, fueled by strong industrial automation trends, technological innovation, and high awareness of AI and digital manufacturing. Germany’s advanced industrial base, emphasis on precision engineering, and focus on energy-efficient solutions promote the adoption of computer vision in factories and commercial operations. Integration with robotic cells and IoT-enabled smart systems is gaining traction, aligning with local industry requirements for secure, precise, and efficient automation solutions.

Asia-Pacific Computer Vision Technologies Market Insight

The Asia-Pacific computer vision technologies market is poised to grow at the fastest CAGR from 2026 to 2033, driven by rapid industrialization, technological advancement, and rising adoption of AI-powered automation in countries such as China, Japan, and India. Government initiatives promoting smart factories, AI, and digital transformation are accelerating computer vision deployment. In addition, the region is emerging as a hub for manufacturing vision hardware and software solutions, making technology more affordable and accessible to a wide range of industrial and non-industrial users.

Japan Computer Vision Technologies Market Insight

The Japan computer vision technologies market is gaining momentum due to the country’s technology-oriented industrial ecosystem, advanced robotics adoption, and increasing demand for automation and precision in manufacturing. Japanese industries are leveraging computer vision for robotics, quality inspection, and human-machine collaboration. Furthermore, integration with IoT devices and AI platforms in smart factories and urban infrastructure is accelerating market growth, with a focus on efficiency, reliability, and safety.

China Computer Vision Technologies Market Insight

The China computer vision technologies market accounted for the largest revenue share in Asia-Pacific in 2025, supported by rapid industrialization, technological adoption, and government-backed AI initiatives. China is a leading market for manufacturing automation, smart cities, and intelligent surveillance solutions. Rising demand for robotics, quality inspection systems, and AI-based monitoring in industrial and non-industrial applications is driving growth, alongside strong domestic players providing cost-effective computer vision hardware and software solutions.

Computer Vision Technologies Market Share

The computer vision technologies industry is primarily led by well-established companies, including:

- Intel Corporation (U.S.)

- KEYENCE Corporation (Japan)

- Microsoft (U.S.)

- Nvidia Corporation (U.S.)

- Sony Corporation (Japan)

- Autoliv Inc. (Sweden)

- Cognex Corporation (U.S.)

- NATIONAL INSTRUMENTS CORP. (U.S.)

- Basler AG (Germany)

- ISRA VISION AG (Germany)

- Cadence Design System, Inc. (U.S.)

- Baumer (Switzerland)

- MediaTek Inc. (Taiwan)

- Zebra Technologies Corp (U.S.)

- MVTec Software GmbH (Germany)

- Synopsys, Inc. (U.S.)

- OMRON Corporation (Japan)

- Teledyne Technologies Incorporated (U.S.)

- Dataiku (France)

- Cortexica Vision (U.K.)

- DENSO CORPORATION (Japan)

Latest Developments in Global Computer Vision Technologies Market

- In March 2026, NVIDIA introduced its Dynamo 1.0 inference operating system for AI factories. This new platform enables manufacturers and robotics developers to deploy AI inference workflows at industrial scale with enhanced efficiency and scalability. By providing an open-source, high-performance inference OS, Dynamo 1.0 allows integration of multiple computer vision models across distributed production lines and autonomous systems. The platform reduces deployment costs while improving processing speed and real-time analytics, enabling faster decision-making and predictive maintenance. This development strengthens the adoption of AI-driven computer vision solutions in smart factories, industrial automation, and autonomous operations, positioning NVIDIA as a key enabler in the industrial computer vision ecosystem

- In December 2025, e-con Systems launched the Darsi Pro AI Compute Box powered by NVIDIA Jetson, targeting autonomous systems and intelligent traffic applications. The Darsi Pro platform delivers up to 100 TOPS of AI processing power with multi-sensor connectivity, supporting rugged and high-performance edge computing for real-time computer vision tasks. Its design is optimized for applications such as autonomous vehicles, smart traffic management, and industrial robotics, allowing immediate AI processing at the edge without reliance on cloud resources. By enhancing the speed, accuracy, and reliability of edge computer vision systems, this product drives broader adoption of vision-based automation in both industrial and non-industrial sectors, including transportation and mobility solutions

- In August 2024, Zebra Technologies Corp. enhanced its Aurora machine vision software with advanced AI and deep learning capabilities. The updated Aurora suite provides sophisticated visual inspection solutions for industries such as automotive, electronics, semiconductors, packaging, and food and beverage. Its deep learning tools improve defect detection, anomaly identification, and complex visual analysis that traditional systems cannot achieve. By enabling engineers, programmers, and data scientists to optimize production quality and operational efficiency, Aurora strengthens enterprise adoption of AI-powered computer vision systems. This development demonstrates the market trend toward software-centric solutions that enhance industrial automation and precision inspection

- In May 2024, Aetina Corporation launched the AIP-KQ67 Edge AI platform for computing and AI inference. Equipped with Intel’s 12th/13th generation Core processors, NVIDIA-certified GPUs, and high-speed I/O connectivity, the platform is engineered for high-performance AI and computer vision workloads. It supports industrial applications such as automated inspection, robotics, and predictive maintenance by enabling real-time processing of complex visual data at the edge. The AIP-KQ67 facilitates faster deployment of AI-driven vision solutions in industrial and commercial environments, addressing the growing demand for reliable, low-latency, and high-throughput computer vision technologies

- In April 2024, Cognex Corporation introduced the In-Sight L38 3D Vision System, combining AI with advanced 3D and 2D vision technologies. This system generates projection images that merge 3D data into easily labeled 2D formats, simplifying AI model training and detecting features that traditional 2D imaging cannot identify. Its AI tools automatically recognize variable or undefined features, while rule-based algorithms ensure precise 3D measurements and consistent inspection results. By improving the accuracy, reliability, and efficiency of industrial visual inspection, this development expands computer vision adoption in manufacturing, quality control, and automation, reflecting the market shift toward intelligent and hybrid vision systems

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Computer Vision Technologies Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Computer Vision Technologies Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Computer Vision Technologies Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.