Global Concentrated Pv Cell Cvp And Hcvp Market

Market Size in USD Billion

USD

2.70 Billion

USD

6.68 Billion

2025

2033

USD

2.70 Billion

USD

6.68 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.70 Billion | |

| USD 6.68 Billion | |

| % | |

|

Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Market Overview

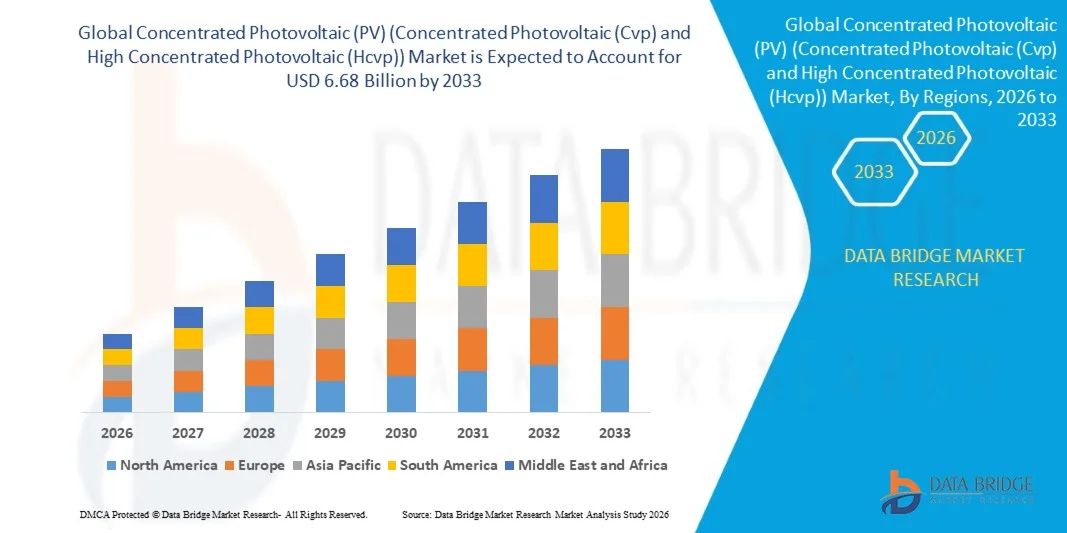

The Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Market was valued at USD 2.70 billion in 2025 and is projected to reach USD 6.68 billion by 2033, growing at a CAGR of 12.00% from 2026 to 2033. The global Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (CPV) and High Concentrated Photovoltaic (HCPV)) market is experiencing steady growth driven by increasing demand for high-efficiency solar power generation, rising investments in renewable energy infrastructure, and advancements in photovoltaic cell technology. The market is gaining momentum due to the growing need for clean energy solutions, declining costs of solar technologies, and government initiatives supporting large-scale renewable energy deployment.

The increasing focus on reducing carbon emissions, expanding utility-scale solar projects, and improving energy conversion efficiency is encouraging the adoption of CPV and HCPV systems in regions with high solar irradiation. These technologies offer higher efficiency compared with conventional photovoltaic systems by using optical concentrators and advanced solar cells to maximize electricity generation. Rising investments in solar research and development, integration of advanced tracking systems, and growing demand for reliable renewable energy sources across commercial, industrial, and utility applications are further supporting market expansion.

Key Market Trends & Insights

- North America dominated the global concentrated photovoltaic (PV) (concentrated photovoltaic (CPV) and high concentrated photovoltaic (HCPV)) market with the largest revenue share of 36.2% in 2025, supported by strong renewable energy investments, increasing deployment of utility-scale solar projects, favorable government policies promoting clean energy adoption, and the presence of advanced solar technology developers across the region.

- The Utility segment dominated the market with a 72.3% share in 2025, driven by increasing deployment of large-scale solar power plants and growing demand for high-efficiency renewable energy generation.

- Asia-Pacific is expected to be the fastest-growing region with a CAGR of 8.1% from 2026 to 2033, fueled by rapid solar infrastructure expansion, increasing renewable energy targets, rising electricity demand, and growing investments in concentrated solar technologies across China, India, Japan, and Southeast Asian countries.

- The reflectors segment dominated the product category with a 62.4% revenue share in 2025, owing to their ability to enhance solar concentration efficiency, improve energy capture, and provide cost-effective optical solutions for CPV and HCPV systems.

Market Size & Forecast

- Global Market Value (2025): USD 2.70 Billion

- Expected Market Value (2033): USD 6.68 Billion

- Forecast CAGR (2026–2033): 12.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Market Segmentation

|

Attributes |

Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Soitec (France) |

|

Market Opportunities |

· Growing Adoption of High-Efficiency Solar Technologies in High Solar Irradiation Regions · Rising Investments in Utility-Scale Solar Projects and Renewable Energy Infrastructure · Advancements in Multi-Junction Solar Cells, Tracking Systems, and Hybrid Energy Solutions |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Market Trends

Trend: Increasing Adoption of High-Efficiency Concentrated Photovoltaic (PV) Systems in Utility-Scale Solar Projects

The global Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (CPV) and High Concentrated Photovoltaic (HCPV)) market is witnessing increasing adoption of high-efficiency solar technologies as governments and energy developers focus on maximizing electricity generation from limited land resources. CPV and HCPV systems use optical components such as lenses and reflectors to concentrate sunlight onto high-efficiency photovoltaic cells, enabling higher conversion efficiency compared with conventional PV technologies, particularly in regions with high direct normal irradiance (DNI). Utility-scale solar developers are increasingly exploring HCPV systems for high-solar-radiation regions such as the southwestern United States, Middle East, and parts of Asia-Pacific. For instance, Amonix Inc., a U.S.-based CPV technology developer, has deployed concentrated photovoltaic systems designed for utility-scale applications, demonstrating the suitability of CPV technology for high-efficiency solar generation. In addition, research institutions and solar technology companies continue to improve optical designs, tracking systems, and multi-junction solar cell efficiency to enhance CPV performance. The integration of advanced tracking systems, improved semiconductor materials, and lightweight reflective structures is further supporting market growth by increasing energy yield and reducing operational costs. The rising focus on renewable energy targets and decarbonization initiatives is expected to accelerate the adoption of CPV and HCPV technologies across utility and commercial solar applications.

Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Market Dynamics

Key Market Driver: Rising Demand for High-Efficiency Solar Technologies in Renewable Energy Expansion

The growing global transition toward renewable energy is a major driver for the CPV and HCPV market. As countries aim to increase solar power generation capacity, concentrated photovoltaic technologies are gaining attention due to their ability to deliver higher efficiency under suitable solar conditions. Unlike traditional photovoltaic systems, CPV technologies concentrate sunlight onto smaller, highly efficient solar cells, improving power output per unit area. Governments worldwide are supporting large-scale solar deployment through renewable energy programs and investments. For example, the United States Department of Energy (DOE) has continued funding research initiatives focused on improving photovoltaic efficiency and reducing solar technology costs under programs supporting next-generation solar technologies. Similarly, countries including China and India are expanding solar infrastructure under national renewable energy targets, creating opportunities for advanced photovoltaic technologies. The increasing installation of utility-scale solar farms, demand for improved land utilization, and need for higher energy output are encouraging developers to evaluate CPV and HCPV solutions, especially in areas with strong sunlight availability.

Key Restraint/Challenge: High Installation Cost and Dependence on High Solar Irradiance Conditions

A significant challenge for the global Concentrated Photovoltaic market is the high initial investment required for system installation, including advanced optical components, precision tracking mechanisms, high-performance photovoltaic cells, and specialized infrastructure. Compared with conventional solar PV systems, CPV and HCPV technologies involve higher upfront costs, limiting adoption in price-sensitive markets. In addition, CPV systems require high direct normal irradiance (DNI) levels to achieve optimal performance, making them less suitable for regions with frequent cloud cover or diffuse sunlight conditions. This geographic limitation reduces deployment flexibility compared with traditional photovoltaic modules. For instance, several early CPV projects in regions with insufficient solar concentration conditions experienced lower-than-expected performance, highlighting the importance of site selection and solar resource availability. These challenges have encouraged manufacturers to focus on cost reduction, improved tracking accuracy, and hybrid solar solutions to enhance commercial viability.

Key Market Opportunity: Integration of Advanced Materials, Multi-Junction Cells, and Hybrid Solar Systems

The integration of advanced photovoltaic materials, multi-junction solar cells, and improved optical technologies presents significant growth opportunities for the CPV and HCPV market. Multi-junction cells, which utilize multiple semiconductor layers to capture a broader range of the solar spectrum, enable higher conversion efficiencies compared with conventional silicon-based cells. Research organizations such as the National Renewable Energy Laboratory (NREL) in the United States have achieved record-breaking solar cell efficiency levels through advanced multi-junction photovoltaic technologies, supporting future innovation in concentrated photovoltaic applications. In addition, combining CPV systems with energy storage solutions, smart grid technologies, and hybrid renewable energy systems is creating new opportunities for commercial and utility applications. The expansion of solar projects across Asia-Pacific, particularly in China and India, is expected to provide strong growth potential as these countries continue investing in large-scale renewable energy infrastructure. The increasing focus on reducing carbon emissions, improving solar efficiency, and optimizing land use is expected to strengthen demand for CPV and HCPV technologies during the forecast period.

Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Market Scope

The concentrated photovoltaic (PV) (concentrated photovoltaic (CPV) and high concentrated photovoltaic (HCPV)) market is segmented on the basis of product, level of concentration, and application.

- By Product

On the basis of product, the global concentrated photovoltaic (PV) (CPV and HCPV) market is segmented into Reflectors and Refractors. The Reflectors segment dominated the market with a 61.8% share in 2025, owing to its widespread adoption in concentrated solar systems due to superior sunlight redirection capabilities, cost advantages, and higher optical efficiency. Reflectors play a crucial role in concentrating solar radiation onto photovoltaic cells, improving energy generation efficiency while reducing the required photovoltaic cell area. The segment is gaining strong traction in utility-scale solar projects, particularly in regions with high direct normal irradiance (DNI), such as North America, the Middle East, and parts of Asia-Pacific. Increasing investments in large-scale renewable energy infrastructure and advancements in reflective materials, including lightweight mirrors and improved coatings, are further supporting segment growth. In addition, the relatively lower manufacturing complexity and scalability of reflector-based CPV systems compared with other optical technologies are reinforcing their market dominance.

The refractors segment is expected to witness the fastest growth at a CAGR of 7.6% from 2026 to 2033, driven by increasing adoption of advanced optical concentration technologies and improvements in lens design. Refractive components, including Fresnel lenses, enable efficient sunlight concentration and support higher energy conversion performance in HCPV systems. Growing research into lightweight, durable, and high-transmittance optical materials is improving the efficiency and commercial viability of refractor-based systems. The segment is also benefiting from increasing demand for compact CPV solutions in commercial solar applications and regions with limited installation space. Furthermore, technological advancements in optical engineering and precision manufacturing are expected to accelerate the adoption of refractors during the forecast period.

- By Level of Concentration

On the basis of level of concentration, the global concentrated photovoltaic (PV) (CPV and HCPV) market is segmented into High Concentration Photovoltaic (HCPV) and Low Concentration Photovoltaic (LCPV).The High Concentration Photovoltaic (HCPV) segment dominated the market with a 57.4% share in 2025, supported by its ability to deliver higher conversion efficiency by concentrating sunlight onto advanced multi-junction solar cells. HCPV systems are increasingly preferred for utility-scale applications due to their higher power output, improved land utilization, and suitability for high solar irradiance regions. The segment benefits from rising investments in renewable energy projects, increasing focus on maximizing solar efficiency, and growing demand for high-performance photovoltaic technologies. Utility developers are adopting HCPV systems in regions such as the United States, China, Australia, and the Middle East where strong sunlight availability enables optimal system performance. Additionally, continuous improvements in tracking systems, solar cell technology, and optical concentration designs are enhancing the efficiency and reliability of HCPV installations.

The Low concentration photovoltaic (LCPV) segment is projected to register the fastest CAGR of 7.9% from 2026 to 2033, driven by increasing demand for cost-effective and flexible concentrated solar solutions. LCPV systems require less complex optical and tracking infrastructure compared with HCPV, making them suitable for commercial and medium-scale applications. Growing adoption among commercial facilities seeking renewable energy solutions with reduced installation complexity is supporting segment expansion. The segment is also benefiting from increasing integration with rooftop solar applications, distributed energy systems, and hybrid renewable energy projects. Improvements in system affordability and easier maintenance requirements are expected to further accelerate LCPV adoption across emerging markets.

- By Application

On the basis of application, the global concentrated photovoltaic (PV) (CPV and HCPV) market is segmented into Utility and Commercial. The Utility segment dominated the market with a 72.3% share in 2025, driven by increasing deployment of large-scale solar power plants and growing demand for high-efficiency renewable energy generation. Utility-scale projects benefit from CPV and HCPV technologies due to their ability to generate higher electricity output from limited land areas, especially in regions with high solar radiation. Government initiatives supporting renewable energy expansion, carbon reduction targets, and investments in large solar infrastructure are strengthening the adoption of concentrated photovoltaic systems. Countries including the United States, China, India, and Spain are increasing renewable energy capacity, creating opportunities for CPV technology deployment. Furthermore, advancements in tracking systems, energy optimization, and high-efficiency photovoltaic cells are improving the economic feasibility of utility-scale CPV installations.

The commercial segment is expected to witness the fastest growth at a CAGR of 7.4% from 2026 to 2033, fueled by rising demand for decentralized renewable energy solutions and increasing efforts by businesses to reduce electricity costs and carbon emissions. Commercial users are adopting concentrated photovoltaic technologies for improving energy efficiency and achieving sustainability targets. The segment is supported by growing awareness of clean energy solutions among commercial buildings, industrial facilities, and institutional users. Technological improvements that reduce system costs and simplify installation are encouraging wider adoption beyond traditional utility-scale projects. In addition, the integration of CPV systems with smart energy management platforms and hybrid renewable solutions is expected to create new growth opportunities in commercial applications.

Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Market Regional Analysis

North America dominated the global concentrated photovoltaic (PV) (concentrated photovoltaic (CPV) and high concentrated photovoltaic (HCPV)) market with the largest revenue share of 36.2% in 2025, supported by strong renewable energy investments, increasing deployment of utility-scale solar projects, favorable government policies promoting clean energy adoption, and the presence of advanced solar technology developers across the region. The region benefits from high solar irradiation areas, growing demand for efficient solar power generation systems, and continuous advancements in high-efficiency photovoltaic technologies. Increasing investments in large-scale solar farms, energy transition initiatives, and clean energy targets are further strengthening the adoption of CPV and HCPV systems across utility and commercial applications.

U.S. Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Market Insight

The U.S. concentrated photovoltaic (PV) (CPV and HCPV) market is witnessing steady growth due to rising investments in renewable energy infrastructure, expansion of utility-scale solar projects, and increasing demand for high-efficiency solar technologies. The country’s strong ecosystem of solar technology developers, research institutions, and clean energy companies is supporting innovation in multi-junction solar cells, optical concentrators, and advanced tracking systems. In addition, favorable government initiatives promoting solar energy adoption and decarbonization goals are accelerating the deployment of CPV and HCPV solutions across utility and commercial sectors.

Europe Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Market Insight

The Europe concentrated photovoltaic (PV) (CPV and HCPV) market is expanding due to increasing renewable energy targets, government support for clean power generation, and growing investments in advanced solar technologies. The region’s focus on reducing carbon emissions and improving energy security is encouraging the adoption of efficient solar solutions. Countries across Europe are investing in next-generation photovoltaic technologies, including high concentration photovoltaic systems, to improve solar energy output and optimize land utilization. Rising research and development activities and supportive regulatory frameworks continue to contribute to regional market growth.

U.K. Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Market Insight

The U.K. concentrated photovoltaic (PV) (CPV and HCPV) market is experiencing gradual growth, supported by increasing renewable energy investments, clean energy transition initiatives, and rising adoption of advanced solar technologies. The country’s focus on expanding renewable electricity generation and reducing dependency on conventional energy sources is creating opportunities for concentrated photovoltaic solutions. Increasing investments in solar infrastructure, energy efficiency programs, and sustainable power generation technologies are contributing to market development.

Germany Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Market Insight

The Germany concentrated photovoltaic (PV) (CPV and HCPV) market is growing steadily due to the country’s strong renewable energy ecosystem, advanced engineering capabilities, and commitment toward clean energy expansion. Germany’s focus on solar power integration, technological innovation, and energy transition policies is supporting the development of high-performance photovoltaic systems. Increasing investments in efficient solar generation technologies and the presence of leading research organizations are strengthening the adoption of CPV and HCPV solutions.

Asia-Pacific Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Market Insight

The Asia-Pacific concentrated photovoltaic (PV) (CPV and HCPV) market is expected to be the fastest-growing region with a CAGR of 8.1% from 2026 to 2033, driven by rapid solar infrastructure expansion, increasing renewable energy targets, rising electricity demand, and growing investments in concentrated solar technologies across China, India, Japan, and Southeast Asian countries. The region is witnessing strong growth due to government initiatives supporting renewable energy deployment, increasing utility-scale solar projects, and rising demand for efficient power generation solutions. Expanding solar manufacturing capabilities and technological advancements in photovoltaic systems are further accelerating CPV and HCPV adoption across the region.

Japan Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Market Insight

The Japan concentrated photovoltaic (PV) (CPV and HCPV) market is witnessing consistent growth due to increasing investments in renewable energy, advanced solar technologies, and energy security initiatives. The country’s focus on improving solar efficiency, reducing carbon emissions, and expanding clean energy capacity is supporting market development. Rising adoption of innovative photovoltaic technologies, along with government support for renewable power generation, is creating growth opportunities for CPV and HCPV systems in Japan.

China Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Market Insight

The China concentrated photovoltaic (PV) (CPV and HCPV) market is growing rapidly, driven by large-scale renewable energy expansion, increasing solar power installations, and strong government support for clean energy development. China’s significant investments in solar infrastructure, advanced photovoltaic manufacturing capabilities, and renewable energy targets are supporting the adoption of concentrated photovoltaic technologies. The increasing demand for high-efficiency solar generation systems, particularly in regions with high solar irradiation, is positioning China as a key growth market for CPV and HCPV technologies globally.

Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Market Share

The concentrated photovoltaic (PV) (concentrated photovoltaic (Cvp) and high concentrated photovoltaic (Hcvp)) industry is primarily led by well-established companies, including:

- Soitec (France)

- Arzon Solar (France)

- Amonix (U.S.)

- Magpower (China)

- SolFocus (U.S.)

- GreenVolts (U.S.)

- Semprius (U.S.)

- SunPower Corporation (U.S.)

- Spectrolab (U.S.)

- Suncore Photovoltaic Technology Co., Ltd. (China)

- Solar Junction (U.S.)

- Morgan Solar (Canada)

- Isofoton (Spain)

- BSQ Solar (Spain)

- Emcore Corporation (U.S.)

- Fraunhofer Institute for Solar Energy Systems ISE (Germany)

- NREL (U.S.)

- TNO (Netherlands)

- BrightSource Energy (U.S.)

- Abengoa Solar (Spain)

- Aalborg CSP (Denmark)

- Cogenra Solar (U.S.)

- Azelio (Sweden)

- RayGen Resources (Australia)

Latest Developments in Concentrated Photovoltaic (PV) (Concentrated Photovoltaic (Cvp) and High Concentrated Photovoltaic (Hcvp)) Market

- In April 2021, Fraunhofer Institute for Solar Energy Systems ISE hosted the 17th International Conference on Concentrator Photovoltaic Systems (CPV-17), highlighting the latest advancements in high- and low-concentration photovoltaic technologies, advanced solar cells, optical systems, and tracker-based CPV solutions. The conference showcased innovations including multi-junction solar cells, novel optical concepts, micro-CPV systems, hybrid photovoltaic modules, and integrated tracking technologies aimed at improving efficiency and expanding CPV applications across utility, building-integrated, and emerging solar markets

- In May 2021, researchers from King Abdullah University of Science and Technology (KAUST) and Donghua University developed a concentrated photovoltaic-thermal (CPV-T) hybrid system designed to generate both electricity and freshwater through integrated solar concentration and desalination technology. The system combined CPV collectors, solar thermal components, and vacuum multi-effect membrane distillation, demonstrating the potential of concentrated photovoltaic technologies beyond conventional electricity generation and supporting future applications in water-stressed regions

- In February 2021, researchers published advancements in the CPV technology framework, focusing on application-oriented concentrator photovoltaic solutions to improve solar energy conversion performance. The development emphasized improvements in optical designs, high-efficiency solar cells, hybrid CPV concepts, and approaches to overcome cost and scalability challenges, supporting the continued evolution of CPV systems for specialized renewable energy applications

- In November 2021, researchers reported advancements in concentrated photovoltaic system design focusing on optical performance improvement, thermal management, and efficiency optimization. The developments highlighted the ability of CPV technology to achieve higher conversion efficiency compared with conventional photovoltaic systems under high solar irradiance conditions while emphasizing improvements in concentration ratio, cooling systems, and overall system reliability

- In October 2021, researchers developed an improved concentrated photovoltaic-thermal (CPV-T) system using hybrid absorber technology integrated with advanced solar cells to enhance electricity and thermal energy generation. The innovation focused on reducing system costs and improving energy utilization efficiency, creating opportunities for broader deployment of concentrated photovoltaic technology in hybrid renewable energy applications

- In March 2022, the European Union continued supporting advanced photovoltaic research initiatives focused on improving next-generation solar technologies, including concentrated photovoltaic concepts, high-efficiency solar cells, and innovative photovoltaic materials. These research activities aimed to improve conversion efficiency, reduce manufacturing costs, and accelerate the adoption of advanced solar technologies in future renewable energy projects

- In September 2022, research developments in high concentration photovoltaic (HCPV) systems focused on improving multi-junction solar cell performance, optical concentration methods, and solar tracking technologies. These advancements supported the deployment of HCPV solutions in high direct normal irradiance (DNI) regions by improving energy output and enhancing the economic feasibility of concentrated solar power generation

- In June 2023, advancements in concentrated photovoltaic technology focused on integrating CPV systems with hybrid renewable energy solutions, including energy storage and solar thermal applications. These developments aimed to improve the reliability and commercial viability of CPV systems by addressing intermittency challenges and enabling more consistent renewable electricity generation

- In November 2023, researchers continued developing advanced optical materials and high-efficiency photovoltaic cells for concentrated solar applications, focusing on improving durability, reducing optical losses, and increasing overall system efficiency. These innovations supported the growth of CPV and HCPV technologies in utility-scale solar projects where maximizing power output and land-use efficiency are critical

- In April 2024, Fraunhofer Institute for Solar Energy Systems ISE continued research activities in advanced photovoltaic technologies, including concentrator photovoltaic solutions, focusing on improving solar cell efficiency, system reliability, and cost reduction. The developments highlighted the importance of innovative photovoltaic architectures and advanced materials in supporting future renewable energy deployment

- In August 2024, developments in concentrated photovoltaic systems emphasized improvements in high-efficiency solar modules, advanced tracking mechanisms, and optical concentration technologies to enhance energy yield. Industry participants continued focusing on reducing the cost gap between CPV/HCPV and conventional photovoltaic systems while targeting specialized applications in high-solar-resource regions

- In February 2025, concentrated photovoltaic technology development continued to advance through improvements in multi-junction solar cells, lightweight optical components, and high-precision tracking systems. These innovations supported the growing demand for high-efficiency solar technologies, particularly for utility-scale renewable energy projects seeking improved land utilization and higher electricity generation capacity

- In May 2025, the global CPV and HCPV market witnessed increasing interest in high-efficiency photovoltaic solutions as renewable energy developers focused on maximizing solar power generation in regions with strong solar irradiation. The market continued moving toward advanced concentrated solar technologies, supported by ongoing research, improved component efficiency, and increasing investments in clean energy infrastructure

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Concentrated Pv Cell Cvp And Hcvp Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Concentrated Pv Cell Cvp And Hcvp Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Concentrated Pv Cell Cvp And Hcvp Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.