Global Congenital Hematological Disease Drug Market

Market Size in USD Million

USD

132.22 Million

USD

311.36 Million

2025

2033

USD

132.22 Million

USD

311.36 Million

2025

2033

| 2026 - 2033 | |

| USD 132.22 Million | |

| USD 311.36 Million | |

| % | |

|

Congenital Hematological Disease Drug Market Size

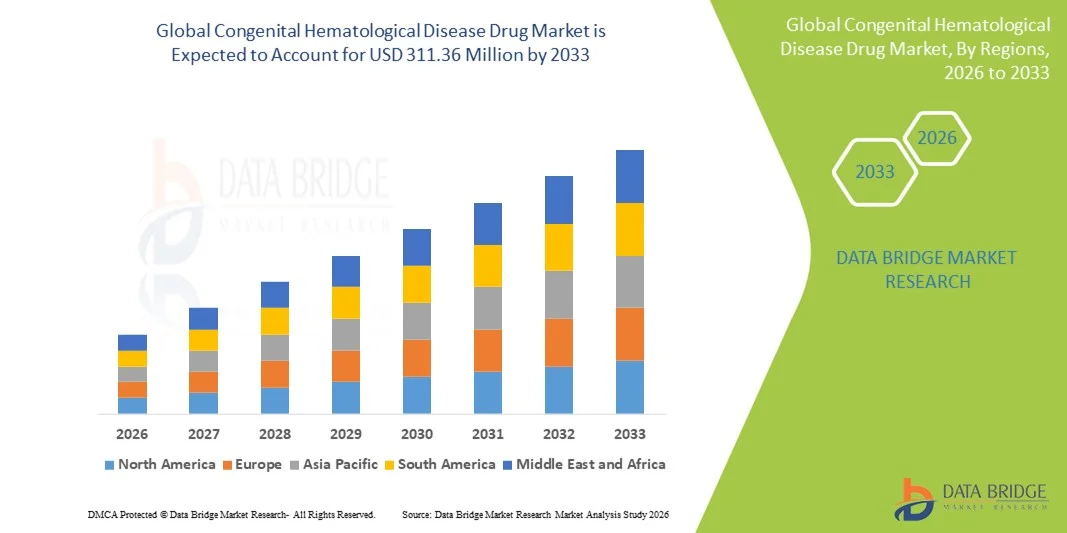

- The global congenital hematological disease drug market size was valued at USD 132.22 million in 2025 and is expected to reach USD 311.36 million by 2033, at a CAGR of 11.30% during the forecast period

- The market growth is largely fueled by the increasing prevalence of congenital blood disorders such as sickle cell disease and thalassemia, rising awareness of treatment options, and ongoing advancements in innovative therapies including gene therapy and novel biologics

- Furthermore, growing demand for effective, targeted therapeutics and improved diagnostic capabilities is driving adoption of advanced drug treatments across both developed and emerging markets, positioning congenital hematological disease drugs as vital components of personalized medicine strategies. These converging factors are accelerating market uptake and significantly boosting the industry’s growth trajectory

Congenital Hematological Disease Drug Market Analysis

- Drugs used for congenital hematological diseases such as sickle cell disease, thalassemia, and hemophilia are becoming increasingly critical within modern therapeutic portfolios due to their role in managing genetic blood disorders, improving survival rates, and supporting long-term disease control through advanced biologics, gene therapies, and supportive care treatments

- The growing demand for these therapies is primarily driven by the rising global prevalence of inherited blood disorders, expanding access to diagnostic services, and the accelerating development of curative gene-based treatments, alongside a heightened clinical emphasis on early intervention and personalized medicine

- North America dominated the congenital hematological disease drug market with a 38.8% revenue share in 2025, supported by strong healthcare infrastructure, high treatment accessibility, and the early availability of innovative therapies such as gene therapy for sickle cell disease and hemophilia, with the U.S. leading adoption due to substantial investment in rare-disease drug development and well-established reimbursement systems

- Asia-Pacific is expected to be the fastest-growing region during the forecast period, driven by a large patient pool, improving healthcare expenditure, and increasing government initiatives aimed at expanding diagnosis and treatment for hemoglobinopathies, particularly in countries such as India, China, and Southeast Asia

- The biologics segment dominated the congenital hematological disease drug market with a share of 46.7% in 2025, supported by its established efficacy in chronic management of hemophilia and related disorders, along with continuous improvements such as extended half-life factor therapies that enhance compliance and reduce dosing frequency

Report Scope and Congenital Hematological Disease Drug Market Segmentation

|

Attributes |

Congenital Hematological Disease Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Congenital Hematological Disease Drug Market Trends

Accelerated Shift Toward Gene Therapy and Personalized Treatment Approaches

- A significant and accelerating trend in the global congenital hematological disease drug market is the expanding integration of advanced gene therapy platforms and personalized medicine approaches aimed at providing long-term or curative solutions for disorders such as sickle cell disease, thalassemia, and hemophilia

- For instance, therapies such as Vertex/CRISPR’s Casgevy and Bluebird Bio’s Zynteglo demonstrate how gene correction and gene addition technologies are reshaping treatment expectations, offering durable outcomes that reduce reliance on lifelong supportive care

- Gene-based therapies enable targeted disease modification, improved hemoglobin production, and sustained factor expression, with several new candidates utilizing CRISPR editing, lentiviral vectors, and in-vivo delivery platforms to achieve deeper clinical benefits. Furthermore, advanced biologics continue to evolve with extended half-life factors and non-factor therapies providing more consistent disease control and reduced treatment burden

- The growing incorporation of genomic profiling and molecular diagnostics supports treatment selection, enabling clinicians to tailor therapies more precisely based on mutation type, response predictors, and disease severity, thereby strengthening the shift toward individualized care pathways

- This trend toward more precise, durable, and technologically advanced treatments is fundamentally reshaping clinical expectations and long-term management strategies for congenital hematological diseases. Consequently, companies such as Pfizer, BioMarin, Vertex, and CRISPR Therapeutics are expanding pipelines that include next-generation gene therapies with improved safety, delivery, and patient accessibility

- The demand for therapies offering curative potential and personalized disease management is rising rapidly across both developed and emerging markets, as healthcare systems increasingly prioritize transformative treatments and long-term reduction of disease burden

Congenital Hematological Disease Drug Market Dynamics

Driver

Growing Treatment Demand Due to Rising Prevalence and Advancements in Curative Therapies

- The increasing prevalence of inherited blood disorders such as sickle cell disease, β-thalassemia, and hemophilia, combined with rapid advancements in gene therapy and novel biologics, is a significant driver of rising demand for congenital hematological disease treatments

- For instance, in December 2023, the approval of Casgevy, the world’s first CRISPR-based therapy, marked a major breakthrough that is expected to accelerate investment and innovation in gene-editing approaches for congenital blood disorders

- As more patients seek improved outcomes and relief from the lifelong burden of chronic therapy, advanced treatments offer enhanced benefits such as reduced hospitalization, fewer complications, and the potential for sustainable cure, making them a compelling shift away from traditional care approaches

- Furthermore, expanding newborn screening programs, improved diagnostic capabilities, and earlier disease detection are increasing patient identification rates, enabling timely access to advanced therapies and driving overall treatment adoption

- The convenience of once-off or infrequent dosing associated with gene therapies, alongside reduced transfusion dependence and improved quality of life, are key factors propelling the uptake of next-generation treatments across global healthcare settings

- The trend toward precision medicine, combined with strong clinical pipelines and rising investment from biotech companies, continues to strengthen the market outlook and is expected to drive significant growth throughout the forecast period

Restraint/Challenge

High Treatment Costs and Complex Regulatory Pathways

- The extremely high cost of gene therapies and advanced biologics, along with complex long-term safety requirements, poses a significant challenge to broad patient access and widespread adoption of congenital hematological disease treatments

- For instance, therapies such as Zynteglo and Hemgenix have list prices exceeding USD 2 million, creating substantial reimbursement hurdles and making affordability a major concern for both healthcare systems and patients

- Addressing these cost barriers through innovative payment models, outcome-based reimbursement strategies, and expanded insurance coverage is crucial for improving accessibility; however, many regions continue to face difficulties due to limited healthcare budgets and reimbursement constraints

- In addition, stringent regulatory frameworks for gene-editing and gene-addition therapies require extensive long-term follow-up, manufacturing validation, and safety monitoring, extending approval timelines and adding significant development costs for manufacturers

- The limited availability of highly specialized treatment centers, coupled with the need for complex procedures such as stem cell mobilization and conditioning regimens, further restricts patient access and slows broader market penetration, particularly in low- and middle-income regions

- Overcoming these challenges through reduced therapy costs, improved reimbursement systems, and expansion of treatment infrastructure will be essential for enabling sustained market growth and increasing global accessibility to transformative therapies

Congenital Hematological Disease Drug Market Scope

The market is segmented on the basis of therapy, indication, end user, and distribution channel.

- By Therapy

On the basis of therapy, the global congenital hematological disease drug market is segmented into gene therapy, gene editing therapy, biologics, small molecules, and adjunctive therapies. The biologics segment dominated the market with the largest revenue share of 46.7% in 2025, driven by strong adoption of recombinant clotting factors, monoclonal antibodies, and enzyme-replacement therapies across major disorders such as hemophilia and sickle cell disease. Biologics continue to be the mainstay of treatment due to well-established clinical efficacy, predictable safety, and broad reimbursement coverage in developed markets. Their availability in long-acting formulations and extensive clinical pipelines further strengthen their position. Widespread hospital and specialty center reliance on biologics for both acute and chronic management contributes significantly to sustained market leadership. Growing R&D spending by pharmaceutical companies and stable regulatory pathways enhance their dominance in this segment.

The gene therapy segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing approvals of curative treatments for sickle cell disease and beta-thalassemia. One-time gene therapy procedures are reshaping clinical pathways by reducing long-term treatment burden and offering durable benefits. Rising investments in viral vector manufacturing capacity and global regulatory support for advanced therapies continue to accelerate market expansion. As clinical evidence becomes stronger and payer frameworks evolve, uptake is expected to surge, particularly in high-income countries. Increasing focus on personalized and functional cure approaches further drives rapid growth in this segment.

- By Indication

On the basis of indication, the market is segmented into sickle cell disease, thalassemia, hemophilia A, hemophilia B, and other congenital hematological disorders. The sickle cell disease segment dominated the market in 2025 owing to its high global prevalence and strong adoption of disease-modifying therapies, biologics, and recently launched gene therapies. Expanded newborn screening programs in North America, Europe, and parts of Africa support higher diagnosis rates and early initiation of treatment. Multiple new therapeutic modalities targeting vaso-occlusive crises and hemoglobin modulation have broadened the treatment landscape. Government-backed awareness programs and increased access to curative options strengthen segment growth. Pharmaceutical companies remain highly active with robust pipelines, further reinforcing its leadership.

The hemophilia A segment is projected to witness the fastest growth rate from 2026 to 2033, driven by significant advancements in long-acting factor VIII products, subcutaneous non-factor therapies, and emerging gene therapy platforms. Increasing transitions from plasma-derived products to recombinant solutions contribute to steady growth. Widening patient access through government reimbursement initiatives and patient-support programs further stimulates adoption. Innovations such as bispecific antibodies are improving treatment convenience, adherence, and bleeding-prevention outcomes. The expanding clinical pipeline continues to strengthen the future growth outlook of this segment.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, ambulatory care centers, and homecare. The hospital segment dominated the market with the largest revenue share in 2025, supported by the concentration of specialized hematology units, infusion centers, and advanced diagnostic capabilities within hospital settings. High-value gene therapies, biologics, and emergency interventions are predominantly administered in hospitals due to clinical supervision requirements. Hospitals also serve as key hubs for clinical trials, enabling early access to novel therapies. Strong reimbursement pathways and the availability of multidisciplinary care teams further enhance their leading position. Increased prevalence of severe congenital hematological conditions continues to drive patient flow to hospitals.

The homecare segment is expected to witness the fastest growth rate during the forecast period, fueled by the rising adoption of self-administration treatment models and long-acting biologics that reduce dependency on hospitals. Portable drug-delivery devices and telehealth platforms are enabling safer and more convenient home-based management of chronic hematological disorders. Growing emphasis on lowering healthcare costs through decentralized care supports rapid expansion. Enhanced patient-support services from manufacturers and specialty pharmacies are improving adherence and outcomes outside of traditional clinical settings. Greater patient preference for comfort and flexibility accelerates the shift toward homecare.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, specialty pharmacies, and online pharmacies. The hospital pharmacies segment held the largest market revenue share in 2025, driven by the requirement for controlled dispensing of high-value biologics, gene therapies, and critical-care medications. Hospital pharmacies ensure proper storage, cold-chain compliance, and clinical oversight during therapy administration. Their integration with hospital treatment workflows streamlines patient monitoring and reimbursement coordination. In addition, hospital pharmacies often manage complex approvals for advanced therapies, ensuring timely access for patients. Strong institutional trust and established procurement systems further solidify their market dominance.

The specialty pharmacies segment is anticipated to grow at the fastest CAGR from 2026 to 2033, supported by their expertise in managing complex, high-touch therapies commonly used in congenital hematological diseases. Specialty pharmacies provide personalized patient support, adherence monitoring, and coordinated care services that enhance treatment outcomes. Their advanced logistics capabilities, including cold-chain management and real-time tracking, make them preferred partners for high-cost therapies. Increasing collaboration between manufacturers, payers, and specialty pharmacies is improving therapy accessibility. Growing demand for long-acting biologics and gene therapies is expected to significantly accelerate segment growth.

Congenital Hematological Disease Drug Market Regional Analysis

- North America dominated the congenital hematological disease drug market with a 38.8% revenue share in 2025, supported by strong healthcare infrastructure, high treatment accessibility, and the early availability of innovative therapies such as gene therapy for sickle cell disease and hemophilia

- The region benefits from well-established newborn screening programs, enabling early diagnosis and timely treatment initiation for conditions such as sickle cell disease, hemophilia, and thalassemia

- In addition, high healthcare expenditure, supportive reimbursement structures, and continuous investment in R&D contribute to rapid uptake of novel therapies and higher treatment penetration across patient populations

U.S. Congenital Hematological Disease Drug Market Insight

The U.S. congenital hematological disease drug market captured the largest revenue share within North America in 2025, driven by early adoption of advanced biologics, gene therapies, and gene-editing platforms. The country’s strong clinical trial ecosystem and widespread newborn screening programs enable timely diagnosis, facilitating rapid initiation of disease-modifying treatments for conditions such as sickle cell disease, hemophilia, and thalassemia. Growing investment from major biopharmaceutical companies, along with robust reimbursement frameworks, further accelerates access to high-cost innovative therapies. In addition, increasing patient awareness, expanding specialty pharmacy networks, and rising uptake of FDA-approved curative gene therapies continue to propel market expansion across the U.S.

Europe Congenital Hematological Disease Drug Market Insight

The Europe congenital hematological disease drug market is projected to expand at a substantial CAGR throughout the forecast period, driven by stringent clinical standards, strong genetic screening programs, and expanding demand for advanced treatment modalities. The region’s focus on early detection and structured care pathways supports adoption of emerging biologics and long-acting therapies. Increasing investments in rare-disease research, combined with favorable regulatory incentives for orphan drugs, are boosting innovation across several European countries. Growing awareness among patients and healthcare providers, along with the modernization of hematology care infrastructure, is supporting widespread integration of next-generation treatment options.

U.K. Congenital Hematological Disease Drug Market Insight

The U.K. congenital hematological disease drug market is anticipated to grow at a noteworthy CAGR, driven by the expanding implementation of national genetic screening programs and rising adoption of advanced therapeutics. The country’s emphasis on improving rare-disease care pathways is encouraging faster diagnosis and better long-term management of hemophilia, sickle cell disease, and thalassemia. In addition, the National Health Service’s (NHS) structured support programs and increased availability of high-cost biologics are strengthening access to treatment. Growing focus on curative gene therapies and clinical research collaboration across leading U.K. hospitals further contributes to market growth.

Germany Congenital Hematological Disease Drug Market Insight

The Germany congenital hematological disease drug market is expected to expand at a considerable CAGR, driven by the country’s advanced healthcare infrastructure, strong biotechnology sector, and emphasis on precision medicine. Germany’s robust regulatory support for orphan drug development encourages continuous introduction of innovative therapies. Growing adoption of extended half-life factor products and rising use of prophylactic treatments are improving patient outcomes and expanding market penetration. Enhanced investment in gene therapy research, combined with a strong network of specialized hematology centers, further accelerates treatment adoption across the country.

Asia-Pacific Congenital Hematological Disease Drug Market Insight

The Asia-Pacific congenital hematological disease drug market is poised to grow at the fastest CAGR during the forecast period, fueled by a large patient population, improving diagnostic capabilities, and rising healthcare expenditure in countries such as China, India, and Japan. Rapid expansion of newborn screening programs and increasing government initiatives for managing hemoglobinopathies are accelerating treatment adoption. Growing availability of affordable biosimilars, combined with improving access to specialty care, is widening treatment reach across the region. In addition, APAC’s emergence as a key clinical trial and biomanufacturing hub is contributing to improved affordability and availability of innovative therapies.

Japan Congenital Hematological Disease Drug Market Insight

The Japan congenital hematological disease drug market is gaining strong momentum due to the country’s advanced medical infrastructure, high-tech healthcare ecosystem, and strong emphasis on patient safety and precision therapies. Rising adoption of long-acting biologics and emerging gene therapy solutions is transforming disease management for hemophilia and other hereditary blood disorders. Japan’s rapidly aging population, coupled with comprehensive insurance coverage and early diagnostic initiatives, is further boosting market expansion. Increasing integration of novel therapies within specialty hematology centers continues to enhance treatment accessibility.

India Congenital Hematological Disease Drug Market Insight

The India congenital hematological disease drug market accounted for one of the largest shares within the Asia-Pacific region in 2025, supported by a high prevalence of hemoglobinopathies, expanding awareness programs, and rapid improvements in healthcare infrastructure. The country’s growing middle class, rising uptake of diagnostic testing, and expansion of specialty hematology clinics are propelling demand for biologics and supportive therapies. Government initiatives targeting thalassemia and sickle cell disease management, along with expanding availability of cost-effective biosimilars, are significantly improving treatment accessibility. The push toward national screening programs and strengthening domestic biopharmaceutical production further amplifies market growth.

Congenital Hematological Disease Drug Market Share

The Congenital Hematological Disease Drug industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Vertex Pharmaceuticals Incorporated (U.S.)

- CRISPR Therapeutics AG (Switzerland)

- bluebird bio, Inc. (U.S.)

- Intellia Therapeutics, Inc. (U.S.)

- Sangamo Therapeutics, Inc. (U.S.)

- Swedish Orphan Biovitrum AB (Sweden)

- CSL Behring (Australia)

- Amicus Therapeutics, Inc. (U.S.)

- Emmaus Life Sciences, Inc. (U.S.)

- Prolong Pharmaceuticals, LLC (U.S.)

- Gamida Cell Ltd. (Israel)

- Global Blood Therapeutics, Inc. (U.S.)

- Alnylam Pharmaceuticals, Inc. (U.S.)

- Acceleron Pharma Inc. (U.S.)

- Bayer AG (Germany)

- Boehringer Ingelheim International GmbH (Germany)

- F. Hoffmann La Roche Ltd (Switzerland)

- Takeda Pharmaceutical Company Limited (Japan)

- Regeneron Pharmaceuticals, Inc. (U.S.)

What are the Recent Developments in Global Congenital Hematological Disease Drug Market?

- In December 2025, Vertex Pharmaceuticals reported promising clinical results for Casgevy in younger children (ages 5–11) with sickle cell disease and transfusion-dependent beta-thalassemia, showing sustained symptom-free outcomes and support for potential regulatory expansion into pediatric populations

- In January 2025, the UK’s National Health Service (NHS) began offering the groundbreaking CRISPR-based gene therapy exagamglogene autotemcel (Casgevy) to eligible sickle cell disease patients, describing it as a transformative “game-changing” treatment that can drastically reduce painful crises

- In April 2024, the U.S. FDA approved BEQVEZ™ (fidanacogene elaparvovec-dzkt), a one-time gene therapy for adults with moderate to severe hemophilia B, designed to enable lasting FIX production and reduce or eliminate the need for routine factor infusions

- In January 2024, the FDA expanded the approval of Casgevy (exagamglogene autotemcel) to include treatment of transfusion-dependent beta-thalassemia (TDT) for patients aged 12 and older, broadening the clinical scope of this CRISPR/Cas9 gene-edited therapy

- In December 2023, the U.S. Food and Drug Administration approved Casgevy (exagamglogene autotemcel) and Lyfgenia (lovotibeglogene autotemcel), marking the first FDA-approved gene therapies for sickle cell disease (SCD), offering potentially curative one-time treatments for patients aged 12 and older

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.