Global Congenital Lymphedema Treatment Market

Market Size in USD Billion

USD

32.41 Billion

USD

64.76 Billion

2025

2033

USD

32.41 Billion

USD

64.76 Billion

2025

2033

| 2026 - 2033 | |

| USD 32.41 Billion | |

| USD 64.76 Billion | |

| % | |

|

Congenital Lymphedema Treatment Market Size

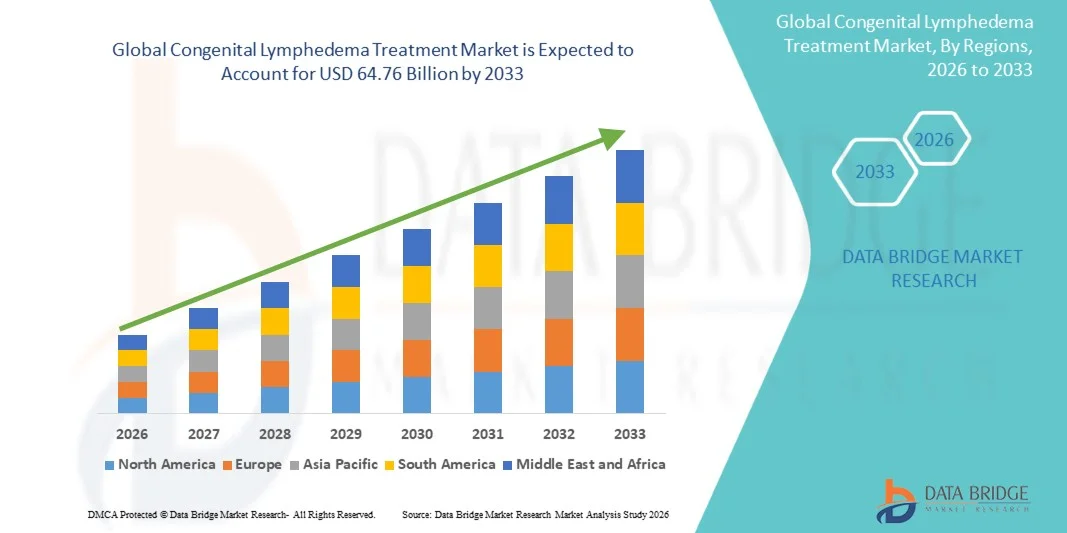

- The global congenital lymphedema treatment market size was valued at USD 32.41 billion in 2025 and is expected to reach USD 64.76 billion by 2033, at a CAGR of 9.04% during the forecast period

- The market growth is largely driven by increasing awareness of congenital lymphedema, rising prevalence of hereditary lymphatic disorders, and advancements in diagnostic and therapeutic technologies, enabling earlier detection and improved management in both pediatric and adult patients

- The escalating demand for effective treatment options is primarily fueled by the adoption of compression therapy, manual lymphatic drainage, surgical interventions, and pharmacological solutions, as well as the growing emphasis on long-term patient care and quality of life improvements

Congenital Lymphedema Treatment Market Analysis

- Congenital Lymphedema treatments, including compression therapy, manual lymphatic drainage, pharmacological interventions, and surgical procedures, are increasingly vital components of modern patient care due to their effectiveness in managing lymphatic disorders, improving quality of life, and preventing disease progression

- The escalating demand for congenital lymphedema treatments is primarily fueled by growing awareness of hereditary lymphatic disorders, increasing prevalence of the condition, and the rising preference for comprehensive, long-term management solutions that combine therapy, monitoring, and supportive care.

- North America dominated the congenital lymphedema treatment market with the largest revenue share of approximately 40% in 2025, characterized by well-established healthcare infrastructure, high disposable incomes, and a strong presence of key industry players, with the U.S. experiencing substantial adoption of advanced lymphedema therapies

- Asia-Pacific is expected to be the fastest growing region in the congenital lymphedema treatment market during the forecast period due to increasing healthcare awareness, rising urbanization, growing investments in healthcare infrastructure, and improving access to specialized treatment centers

- The Physical Examination segment dominated with 46.3% revenue share in 2025, as it remains the primary initial diagnostic method for congenital lymphedema

Report Scope and Congenital Lymphedema Treatment Market Segmentation

|

Attributes |

Congenital Lymphedema Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Congenital Lymphedema Treatment Market Trends

“Rising Adoption of Early Diagnosis and Innovative Therapeutics”

- A significant and accelerating trend in the global Congenital Lymphedema Treatment market is the increasing adoption of early diagnostic technologies and innovative therapeutic interventions. These advances are improving patient outcomes and enabling personalized treatment approaches

- For instance, in 2023, several clinical centers in Europe and North America reported successful integration of novel lymphatic imaging techniques to better assess lymphatic abnormalities, thereby tailoring treatment plans more effectively

- Advanced pharmacological treatments, compression therapies, and surgical interventions are being increasingly combined with regular patient monitoring to optimize efficacy

- The development of minimally invasive surgical techniques, coupled with improved lymphatic drainage therapies, is transforming the standard of care and expanding treatment accessibility

- This trend toward early intervention, personalized therapy, and integrated treatment regimens is fundamentally reshaping patient management and expectations in congenital lymphedema care

Congenital Lymphedema Treatment Market Dynamics

Driver

“Increasing Awareness and Need for Specialized Treatment”

- The rising prevalence of congenital lymphedema and growing awareness among healthcare professionals and patients are major drivers for market growth

- For instance, in 2024, multiple healthcare organizations launched awareness campaigns highlighting early detection and effective management of lymphatic disorders, increasing patient referrals and treatment adoption

- The availability of specialized treatment centers offering comprehensive care—including pharmacological therapy, physical therapy, and surgical options—encourages patients and clinicians to seek appropriate interventions

- Expanded research into novel therapies, alongside government and NGO support for rare disease management, is further driving demand

- Enhanced patient education on long-term management, improved access to diagnostic testing, and increased insurance coverage for treatment are also contributing factors boosting market growth

Restraint/Challenge

“Limited Awareness, High Treatment Costs, and Clinical Complexity”

- Despite growing awareness, congenital lymphedema remains underdiagnosed in several regions due to lack of specialized knowledge among healthcare providers, posing a challenge for timely intervention

- The high cost of advanced treatment modalities, including compression devices, surgery, and ongoing therapeutic management, can limit accessibility, especially in developing countries or for uninsured patients

- For instance, in India, limited insurance coverage and high out-of-pocket expenses often prevent patients from accessing surgical interventions and continuous therapeutic care for congenital lymphedema

- Clinical complexity and the need for individualized, multidisciplinary care may discourage some healthcare facilities from offering specialized treatment, thereby restricting market penetration

- Limited reimbursement policies for rare disease treatments in certain regions further impede patient access to optimal care

- Inadequate healthcare infrastructure and scarcity of trained lymphology specialists in emerging markets create additional barriers to treatment availability and quality of care

- Overcoming these challenges through awareness programs, cost-reduction strategies, expanded insurance coverage, training of specialized personnel, and broader availability of treatment centers will be critical for sustained market growth

Congenital Lymphedema Treatment Market Scope

The market is segmented on the basis of type, treatment, and diagnosis.

• By Type

On the basis of type, the Congenital Lymphedema Treatment market is segmented into Milroy Disease, Meige Disease, and Others. The Milroy Disease segment dominated the market with a revenue share of 45.6% in 2025, owing to its higher prevalence among newborns and infants and well-established treatment protocols. Increasing awareness among parents and caregivers regarding early diagnosis and management of Milroy Disease is driving demand. Healthcare providers are focusing on preventive care and routine monitoring, further boosting adoption. Genetic counseling and testing for Milroy Disease are becoming more accessible, leading to higher case identification and early intervention. In addition, advancements in conservative therapy, compression therapy, and surgical treatment options tailored to Milroy Disease contribute to its market dominance. The segment also benefits from initiatives in developed countries aimed at improving pediatric care for rare lymphatic disorders. Public and private hospitals increasingly offer dedicated lymphedema treatment units, increasing patient inflow. Awareness campaigns and patient education programs enhance recognition of Milroy Disease, supporting market growth. The segment is further aided by collaborations between hospitals, research institutes, and patient advocacy groups to promote early intervention and effective management strategies.

The Meige Disease segment is projected to witness the fastest CAGR of 9.2% from 2026 to 2033, driven by increasing diagnosis in adolescence and early adulthood. Rising investment in genetic testing and imaging technologies has improved identification rates. Meige Disease patients often require personalized management plans, including compression therapy, manual lymphatic drainage, and surgical options. The growing availability of minimally invasive surgical procedures and home-based care solutions is fueling adoption. Improved healthcare access in emerging economies also contributes to rising awareness and treatment uptake. Patient-centric approaches, including physiotherapy and continuous monitoring, are increasing treatment adherence. The segment’s growth is further supported by research initiatives focusing on rare lymphatic disorders and the development of advanced therapeutic interventions. Increased training of clinicians in lymphatic disorder management has enhanced treatment quality and outcomes. Additionally, advocacy programs targeting rare disease awareness are raising the visibility of Meige Disease, further propelling the segment’s CAGR.

• By Treatment

On the basis of treatment, the market is segmented into Conservative Therapy, Compression Therapy, Manual Lymphatic Drainage, Surgical Treatment, and Others. The Compression Therapy segment dominated with a revenue share of 42.8% in 2025, due to its proven efficacy in reducing limb swelling and preventing disease progression. Compression garments and devices are increasingly preferred by healthcare providers for long-term management. Rising patient awareness, technological advancements in garment materials, and improved comfort and durability are driving adoption. Insurance coverage for compression therapy in certain regions also supports market penetration. Standardized treatment protocols recommend compression therapy as a first-line approach, leading to widespread usage. The segment benefits from the increasing number of specialized lymphedema clinics offering customized compression solutions. Integration with physiotherapy and rehabilitation programs further enhances outcomes. Patient education on consistent use of compression devices contributes to higher adherence. The segment also gains momentum from partnerships between manufacturers and healthcare institutions to improve accessibility.

The Surgical Treatment segment is expected to register the fastest CAGR of 8.9% from 2026 to 2033, fueled by advancements in minimally invasive techniques and microsurgery. Increased awareness among patients and physicians about reconstructive lymphatic surgeries is contributing to growth. Hospitals in developed regions are expanding surgical treatment capabilities. Government funding and NGO support for rare disease management also drive adoption. Improved post-operative care and follow-up programs enhance patient outcomes. Rising investment in surgical research and clinical trials contributes to better safety and effectiveness. Emerging economies are gradually adopting surgical interventions as part of comprehensive lymphedema management. The growth is further accelerated by technological integration, such as lymphatic imaging and robotic-assisted surgery. Patient preference for long-term, definitive solutions supports the segment’s CAGR.

• By Diagnosis

On the basis of diagnosis, the market is segmented into Physical Examination, Lymphoscintigraphy, Magnetic Resonance Imaging (MRI), Genetic Testing, and Others. The Physical Examination segment dominated with 46.3% revenue share in 2025, as it remains the primary initial diagnostic method for congenital lymphedema. Routine clinical assessments, coupled with early detection protocols in pediatric care, drive adoption. This segment is supported by the widespread availability of experienced clinicians and primary healthcare facilities. Early diagnosis via physical examination enables timely intervention with compression and conservative therapy. Standardization of assessment guidelines enhances accuracy and reproducibility. Integration with telemedicine services is improving accessibility for patients in remote regions. Physical examination remains cost-effective and non-invasive, making it the preferred choice for initial screening. Clinicians increasingly combine physical assessment with imaging or genetic testing for comprehensive evaluation.

The Genetic Testing segment is projected to register the fastest CAGR of 10.1% from 2026 to 2033, driven by the rising importance of precise diagnosis and personalized treatment planning. Advances in molecular genetics and decreasing costs of sequencing technologies are making genetic testing more accessible. Early identification of pathogenic mutations in Milroy and Meige disease enables targeted intervention and counseling. Government and private funding initiatives support genetic testing programs for rare diseases. Genetic insights inform prognosis and treatment selection, further encouraging adoption. Clinicians are increasingly integrating genetic testing with imaging and physical assessments to provide comprehensive patient care. Patient awareness campaigns and genetic counseling programs are contributing to the growing acceptance of this diagnostic method.

Congenital Lymphedema Treatment Market Regional Analysis

- North America dominated the congenital lymphedema treatment market with the largest revenue share of approximately 40% in 2025

- Characterized by well-established healthcare infrastructure, high disposable incomes, and a strong presence of key industry players

- Increasing awareness of congenital lymphedema and better access to specialized healthcare facilities further support market growth in the region

U.S. Congenital Lymphedema Treatment Market Insight

The U.S. congenital lymphedema treatment market captured the largest share within the region, driven by substantial adoption of advanced lymphedema therapies such as compression therapy, manual lymphatic drainage, surgical interventions, and pharmacological treatments. Increasing awareness of congenital lymphedema and better access to specialized healthcare facilities further support market growth in the region.

Europe Congenital Lymphedema Treatment Market Insight

The Europe congenital lymphedema treatment market is projected to expand at a steady CAGR throughout the forecast period, driven by rising healthcare awareness, well-established medical infrastructure, and increasing investment in specialized treatment centers. Growth is also supported by initiatives to improve patient outcomes for rare hereditary lymphatic disorders, fostering adoption of both conservative and advanced treatment solutions across residential, clinical, and hospital settings.

U.K. Congenital Lymphedema Treatment Market Insight

The U.K. congenital lymphedema treatment market is anticipated to grow at a notable CAGR during the forecast period, propelled by increased awareness of congenital lymphedema, improved access to specialized clinics, and the adoption of comprehensive treatment programs. Government health initiatives and the robust healthcare system also facilitate the delivery of advanced lymphedema therapies to both pediatric and adult patients.

Germany Congenital Lymphedema Treatment Market Insight

Germany’s congenital lymphedema treatment market is expected to expand at a considerable CAGR during the forecast period due to a strong focus on healthcare innovation, well-developed medical infrastructure, and growing emphasis on patient-centric care. Adoption of advanced diagnostic tools such as lymphoscintigraphy, MRI, and genetic testing, alongside conservative and surgical interventions, is supporting market growth in residential, hospital, and clinical settings.

Asia-Pacific Congenital Lymphedema Treatment Market Insight

The Asia-Pacific congenital lymphedema treatment market is expected to be the fastest growing region during the forecast period, driven by increasing healthcare awareness, rising urbanization, growing investments in healthcare infrastructure, and improving access to specialized treatment centers. Countries such as China, Japan, and India are witnessing greater adoption of advanced lymphedema therapies, supported by initiatives to improve patient outcomes and expansion of healthcare services in both urban and semi-urban areas.

Japan Congenital Lymphedema Treatment Market Insight

The Japan congenital lymphedema treatment market is gaining momentum due to high healthcare standards, increased awareness of congenital lymphatic disorders, and demand for effective treatment solutions. The focus on early diagnosis, preventive care, and patient-centric therapy programs is driving adoption in hospitals and clinics.

China Congenital Lymphedema Treatment Market Insight

The China congenital lymphedema treatment market accounted for the largest revenue share in the Asia-Pacific region in 2025, owing to the rising prevalence of congenital lymphedema, expanding healthcare access, and growing awareness of advanced treatment options. Increasing government support, development of specialized treatment centers, and investment in healthcare infrastructure are expected to further drive market growth across hospitals, clinics, and rehabilitation centers.

Congenital Lymphedema Treatment Market Share

The Congenital Lymphedema Treatment industry is primarily led by well-established companies, including:

- BD (U.S.)

- Thermo Fisher Scientific (U.S.)

- Stryker (U.S.)

- Medi (Germany)

- Juzo (Germany)

- Hy-Tape International (U.S.)

- Smith & Nephew (U.K.)

- Coban 3M (U.S.)

- Henry Schein (U.S.)

- BSN Medical (Germany)

- LymphaTech (France)

- Cardinal Health (U.S.)

- ConvaTec (U.K.)

- Paul Hartmann AG (Germany)

- Integra LifeSciences (U.S.)

- Cure Lymphedema Solutions (U.S.)

- Lympha Press (U.S.)

- Arjo (Sweden)

- Medical Compression Systems (U.K.)

- Lymphatic Technology (U.S.)

Latest Developments in Global Congenital Lymphedema Treatment Market

- In March 2024, a review article titled “Advances in Surgical Lymphedema Management: The Emergence and Refinement of Lymph Node‑to‑Vein Anastomosis (LNVA)” was published, highlighting how LNVA — a microsurgical technique — has evolved and improved. The article notes newer imaging and radiofrequency‑based localization plus refined supermicrosurgical methods that significantly improve the procedure’s effectiveness in lower-extremity lymphedema

- In September 2024, a study was published demonstrating the first clinical use of robotic-assisted microsurgery for central lymphatic reconstruction (using a system called Symani Surgical System) in patients — including children (“8 months”) to adults — with rare anomalies of the central lymphatic system. The study reported patent anastomoses and reduced chyle leakage post-operatively

- In August 2024, a new treatment algorithm — the P‑LYMA (Primary LYmphedema Multidisciplinary Approach) — was proposed to manage primary lower extremity lymphedema. The protocol involved combinations of pre‑ and post‑operative decongestive therapy and physiologic or excisional surgical procedures, tailored per patient. This represents a move toward standardization of care in congenital/primary lymphedema

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.