Global Constipation Therapeutics Market

Market Size in USD Billion

USD

8.62 Billion

USD

13.84 Billion

2025

2033

USD

8.62 Billion

USD

13.84 Billion

2025

2033

| 2026 - 2033 | |

| USD 8.62 Billion | |

| USD 13.84 Billion | |

| % | |

|

Constipation Therapeutics Market Overview

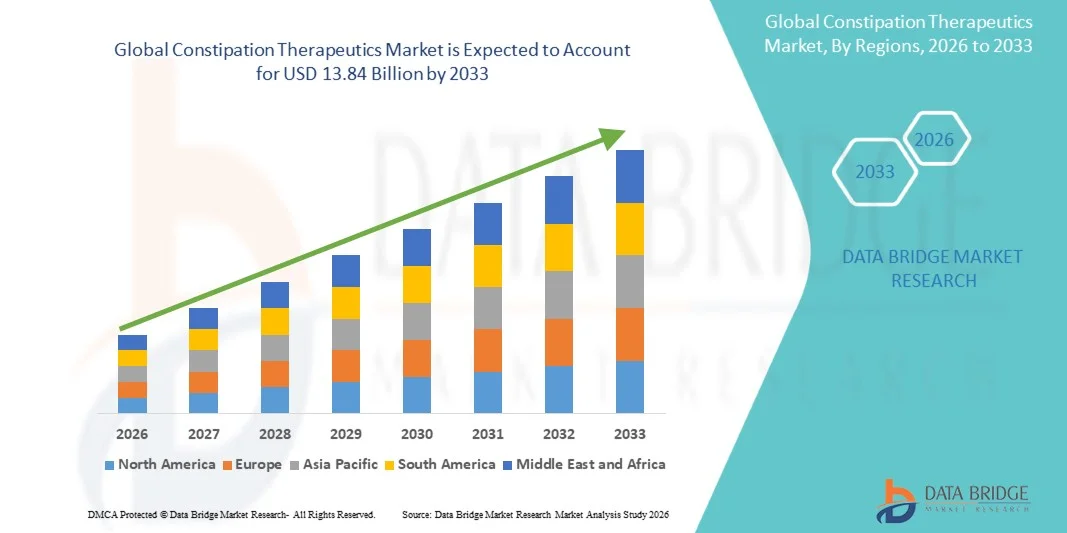

As per Data Bridge Market Research analysis The constipation therapeutics market was valued at USD 8.62 billion in 2025 and is projected to reach USD 13.84 billion by 2033, growing at a CAGR of 6.10% from 2026 to 2033. The market is experiencing consistent growth driven by the increasing prevalence of gastrointestinal disorders, a rapidly aging population, rising awareness of digestive health, and continued pharmaceutical innovation in targeted constipation therapies.

The growing burden of chronic idiopathic constipation (CIC), irritable bowel syndrome with constipation (IBS-C), and opioid-induced constipation (OIC), coupled with increasing adoption of advanced therapeutics such as guanylate cyclase-C agonists, chloride channel activators, and 5-HT4 receptor agonists, is accelerating market expansion. In addition, improved diagnosis rates, expanding access to prescription and over-the-counter therapies, and the development of novel gastrointestinal motility agents are supporting sustained demand for constipation therapeutics worldwide

Market Size & Forecast

- Global Market Value (2025): USD 8.62 Billion

- Expected Market Value (2033): USD 13.84 Billion

- Forecast CAGR (2026–2033): 6.10%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Key Market Trends & Insights

- North America dominated the constipation therapeutics market with a revenue share of 37.0% in 2025, supported by advanced healthcare infrastructure, high diagnosis rates, favorable reimbursement systems, and strong adoption of prescription gastrointestinal therapies.

- The laxatives segment led the market with a 44.3% share in 2025, driven by the widespread first-line use, broad over-the-counter availability, and strong physician familiarity across healthcare settings.

- Asia-Pacific is expected to be the fastest-growing region, projected to expand at a CAGR of 8.7% during the forecast period, fueled by rising healthcare expenditure, increasing awareness of gastrointestinal disorders, improving access to treatment, and a growing elderly population

- Guanylate cyclase-C (GC-C) agonists are the fastest-growing therapeutic type, projected to register a CAGR of 9.5%, reflecting the surge in adoption of targeted prescription therapies for chronic constipation disorders.

- The chronic idiopathic constipation (CIC) segment dominated the disease type category with a 51.7% revenue share in 2025, led by its high prevalence and increasing diagnosis among adult and elderly populations worldwide

- Over-the-counter drugs accounted for 58.4% of the market, preferred by the easy accessibility, lower treatment costs, and strong consumer preference for self-management approaches.

- The prescription drugs segment is the fastest-growing prescription type category, with a CAGR of 9.2%, driven by increasing diagnosis of chronic constipation disorders and expanding use of targeted therapies.

Report Scope and Constipation Therapeutics Market Segmentation

|

Attributes |

Constipation Therapeutics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Constipation Therapeutics Market Trends

Trend: Increasing Adoption of Targeted and Novel Therapies for Chronic Constipation

Healthcare providers are increasingly adopting targeted prescription therapies for chronic constipation management, moving beyond conventional laxatives toward treatments that address specific gastrointestinal motility and secretion pathways. Guanylate cyclase-C (GC-C) agonists, chloride channel activators, and selective 5-hydroxytryptamine receptor 4 (5-HT4) agonists are gaining wider clinical acceptance due to their ability to improve bowel movement frequency and symptom control in patients with chronic idiopathic constipation and irritable bowel syndrome with constipation. At the same time, innovation in non-pharmacological treatment modalities and microbiome-focused approaches is expanding the therapeutic landscape, providing new options for patients who experience inadequate relief from traditional therapies. For instance, In May 2023, the American Gastroenterological Association (AGA) and American College of Gastroenterology (ACG) jointly recommended linaclotide, plecanatide, prucalopride, and lubiprostone for adults with chronic idiopathic constipation who do not respond adequately to over-the-counter therapies, highlighting the growing shift toward targeted prescription therapeutics.

This trend is expected to accelerate the transition from symptom-based management to mechanism-driven treatment approaches, supporting improved clinical outcomes, greater physician confidence in advanced therapies, and continued innovation across the constipation therapeutics market.

Constipation Therapeutics Market Dynamics

Key Market Driver: Rising Prevalence of Chronic Idiopathic Constipation and Aging Population

The increasing prevalence of chronic idiopathic constipation, irritable bowel syndrome with constipation, and opioid-induced constipation has created substantial demand for advanced constipation therapeutics. Older adults are particularly affected due to age-related declines in gastrointestinal motility, multiple chronic conditions, and extensive medication use. Growing awareness of digestive health, improved diagnosis rates, and greater availability of prescription treatment options are supporting the expansion of the constipation therapeutics market. Healthcare organizations are increasingly emphasizing evidence-based management strategies to address the significant clinical and economic burden associated with chronic constipation. For instance, In June 2024, the American Gastroenterological Association published updated epidemiological findings indicating that chronic constipation remains one of the most common gastrointestinal disorders worldwide, particularly among elderly populations, reinforcing demand for effective long-term therapeutic solutions.

The continued growth of the aging population, combined with increasing recognition of chronic constipation as a significant healthcare concern, is expected to sustain demand for innovative and effective treatment options, thereby driving long-term expansion of the constipation therapeutics market.

Key Restraint/Challenge: Persistent Unmet Need and Inadequate Symptom Control

A significant challenge in the constipation therapeutics market is the persistence of unmet clinical needs despite the availability of multiple treatment options. Many patients continue to experience inadequate symptom relief, recurrent constipation episodes, abdominal discomfort, bloating, and treatment-related adverse effects. Long-term disease management often requires treatment escalation, switching between therapies, or combination approaches, creating challenges for patient adherence and overall treatment satisfaction. These limitations underscore the need for more effective and durable therapeutic solutions. For instance, In September 2023, the AGA-ACG Clinical Practice Guideline on Chronic Idiopathic Constipation concluded that several prescription therapies received only conditional recommendations based on low- or moderate-certainty evidence, highlighting ongoing limitations in treatment effectiveness and the need for better long-term therapeutic options for patients with chronic constipation.

This challenge is expected to encourage continued investment in gastrointestinal research, next-generation therapeutics, and personalized treatment approaches aimed at improving efficacy, tolerability, and long-term patient outcomes. Addressing these unmet needs will remain critical for enhancing treatment satisfaction and supporting sustainable growth in the constipation therapeutics market.

Key Market Opportunity: Integration of AI and Autonomous Vehicle Validation Platforms

The development of drug-free therapeutic technologies and precision gastrointestinal treatments presents a significant market opportunity. Emerging approaches such as vibrating capsule systems, microbiome-targeted therapies, and next-generation gastrointestinal motility agents are designed to address patients who do not respond adequately to conventional laxatives or existing prescription medications. Continued investment in gut microbiome research, personalized medicine, and innovative device-based treatments is creating new avenues for market growth while expanding therapeutic choices for chronic constipation management. For instance, In August 2022, the U.S. Food and Drug Administration (FDA) granted clearance to the Vibrant System, the first prescription vibrating capsule for adults with chronic idiopathic constipation, establishing a new non-drug treatment category and demonstrating the commercial potential of innovative gastrointestinal therapeutic technologies.

This opportunity is expected to accelerate the diversification of treatment options beyond traditional pharmacological therapies, fostering innovation in gastrointestinal care and improving outcomes for patients with difficult-to-treat constipation.

Constipation Therapeutics Market Scope

The constipation therapeutics market is segmented on the basis of therapeutic type, disease type, prescription type, and distribution channel.

- By Therapeutic Type

On the basis of therapeutic type, the constipation therapeutics market is segmented into laxatives, chloride channel activators, peripherally acting mu-opioid receptor antagonists (PAMORAs), guanylate cyclase-C (GC-C) agonists, and other therapeutics. The laxatives segment dominated the market with an estimated 44.3% share in 2025, owing to widespread first-line use, broad over-the-counter availability, and strong physician familiarity across healthcare settings. These therapies remain the standard initial treatment for occasional and chronic constipation due to their established efficacy and affordability. The segment benefits from a diverse product portfolio including bulk-forming, osmotic, stimulant, and stool-softening agents. Extensive retail pharmacy penetration and strong consumer awareness continue to support demand. Generic availability further enhances accessibility across developed and emerging markets. Consistent recommendations in clinical practice and self-medication trends continue to reinforce the segment’s leading position globally. The AGA and ACG guideline continued to recommend polyethylene glycol and stimulant laxatives as evidence-based first-line treatments for chronic idiopathic constipation.

The guanylate cyclase-C (GC-C) agonists segment is projected to register the fastest growth at a CAGR of 9.5% during the forecast period, driven by increasing adoption of targeted prescription therapies for chronic constipation disorders. These therapies improve intestinal fluid secretion and accelerate bowel transit through a well-defined mechanism of action. Growing physician preference for evidence-based prescription treatments is supporting increased utilization. Expanding clinical guideline endorsements for linaclotide and plecanatide are strengthening market adoption. Rising diagnosis rates of chronic idiopathic constipation and irritable bowel syndrome with constipation are creating sustained demand. Continued investment in gastrointestinal drug innovation is expected to further accelerate segment growth over the coming years.

- By Disease Type

On the basis of disease type, the constipation therapeutics market is segmented into chronic idiopathic constipation (CIC), irritable bowel syndrome with constipation (IBS-C), and opioid-induced constipation (OIC). The chronic idiopathic constipation (CIC) segment dominated the market with an estimated 51.7% share in 2025, driven by its high prevalence and increasing diagnosis among adult and elderly populations worldwide. CIC remains one of the most frequently encountered functional gastrointestinal disorders requiring long-term therapeutic intervention. The segment benefits from the availability of both over-the-counter and advanced prescription treatment options. Growing awareness among healthcare professionals is improving disease recognition and management. Updated treatment guidelines have expanded therapeutic choices for patients with persistent symptoms. The chronic and recurrent nature of the condition continues to generate sustained demand for constipation therapeutics globally. The AGA and ACG published comprehensive treatment recommendations specifically addressing the management of chronic idiopathic constipation in adults.

The opioid-induced constipation (OIC) segment is expected to witness the fastest growth at a CAGR of 8.9 % during the forecast period, driven by increasing opioid utilization in chronic pain and cancer pain management. OIC remains one of the most common and persistent adverse effects associated with long-term opioid therapy. Rising awareness among clinicians regarding quality-of-life impacts is supporting earlier diagnosis and intervention. The availability of targeted therapies such as PAMORAs is improving treatment outcomes for affected patients. Growing palliative care utilization and increasing cancer prevalence are further supporting segment expansion. Enhanced recognition of OIC as a distinct clinical condition is expected to drive continued market growth. Relistor (methylnaltrexone), a PAMORA specifically indicated for opioid-induced constipation, continues to support the growing focus on targeted OIC management.

- By Prescription Type

On the basis of prescription type, the constipation therapeutics market is segmented into prescription drugs and over-the-counter drugs. The over-the-counter drugs segment dominated the market in 2025 with a market share of 58.4%, driven by easy accessibility, lower treatment costs, and strong consumer preference for self-management approaches. Products including polyethylene glycol, stimulant laxatives, and stool softeners remain widely used as initial treatment options. The segment benefits from broad retail distribution and strong brand recognition among consumers. Many patients seek non-prescription therapies before consulting healthcare professionals for chronic symptoms. Established safety profiles and affordability continue to support widespread utilization. Increasing awareness of digestive health is further contributing to demand across global markets. Polyethylene glycol products remain among the most widely recommended and purchased over-the-counter therapies for constipation management worldwide.

The prescription drugs segment is projected to experience the fastest growth at a CAGR of 9.2% during the forecast period, supported by increasing diagnosis of chronic constipation disorders and expanding use of targeted therapies. Prescription treatments offer improved efficacy for patients who do not respond adequately to conventional laxatives. Growing adoption of GC-C agonists, PAMORAs, and chloride channel activators is driving segment expansion. Updated clinical guidelines increasingly support escalation to prescription medications when necessary. Pharmaceutical innovation continues to expand available treatment options. Rising healthcare expenditure and specialist consultations are expected to further strengthen segment growth. The AGA-ACG guideline strongly recommended prescription therapies including linaclotide, plecanatide, and prucalopride for selected patients with chronic idiopathic constipation

- By Distribution Channel

On the basis of distribution channel, the constipation therapeutics market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. The retail pharmacies segment accounted for the largest market share of 46.1% in 2025, driven by extensive geographic coverage, convenience, and broad product availability. Retail pharmacies serve as the primary channel for both prescription and over-the-counter constipation therapeutics. Pharmacists frequently provide treatment recommendations and patient counseling for constipation management. The segment benefits from strong consumer trust and established healthcare infrastructure. Availability of branded and generic products supports accessibility across diverse patient populations. Continued preference for community-based pharmacy services reinforces the segment’s dominant market position. Major pharmacy chains continue to stock extensive portfolios of constipation treatments, including laxatives and prescription gastrointestinal therapies, supporting retail channel leadership.

The online pharmacies segment is expected to register the fastest growth at a CAGR of 10.1% during the forecast period, driven by increasing digital healthcare adoption and consumer preference for convenient medication purchasing. Online platforms provide home delivery services and access to a broad range of constipation therapeutics. Rising internet penetration and smartphone usage are accelerating online pharmacy utilization globally. Telemedicine expansion and electronic prescribing are further supporting market growth. Competitive pricing and subscription-based refill programs enhance patient convenience. Continued digital transformation of healthcare delivery is expected to drive significant growth within this segment. The expansion of telehealth-enabled prescription fulfillment platforms has increased online access to chronic gastrointestinal medications, including constipation therapeutic

Constipation Therapeutics Market Regional Analysis

North America dominated the constipation therapeutics market with a revenue share of 37.0% in 2025, supported by advanced healthcare infrastructure, high diagnosis rates, favorable reimbursement systems, and strong adoption of prescription gastrointestinal therapies. The region also benefits from early uptake of guanylate cyclase-C (GC-C) agonists, 5-HT4 receptor agonists, and other targeted therapeutics for chronic idiopathic constipation and opioid-induced constipation. Strong presence of leading pharmaceutical manufacturers, expanding clinical guideline adoption, and increasing availability of innovative therapies such as vibrating capsule systems are further accelerating market growth. Rising prevalence of chronic constipation among the aging population, together with high healthcare expenditure and extensive retail pharmacy networks, continues to strengthen North America's leadership position in the global constipation therapeutics market.

U.S. Constipation Therapeutics Market Insight

The U.S. constipation therapeutics market is witnessing strong growth due to the high prevalence of chronic idiopathic constipation, irritable bowel syndrome with constipation, and opioid-induced constipation across diverse patient populations. The country benefits from advanced healthcare infrastructure, favorable reimbursement frameworks, and widespread access to innovative prescription therapies, including guanylate cyclase-C agonists, 5-HT4 receptor agonists, and peripherally acting mu-opioid receptor antagonists. Strong adoption of evidence-based clinical guidelines is improving treatment outcomes and encouraging earlier intervention for chronic constipation. In addition, increasing awareness of gastrointestinal health, rising healthcare expenditure, and continued investment in gastrointestinal drug development are supporting market expansion. The presence of leading pharmaceutical manufacturers and ongoing regulatory approvals for novel therapies further strengthen the U.S. market. In June 2023, the U.S. FDA approved an expanded indication for LINZESS (linaclotide) for the treatment of functional constipation in pediatric patients aged 6–17 years, making it the first FDA-approved prescription therapy for this patient population.

Europe Constipation Therapeutics Market Insight

The Europe constipation therapeutics market remains a major contributor to global revenue, supported by well-established healthcare systems, favorable reimbursement policies, and increasing adoption of advanced gastrointestinal therapies. Rising diagnosis rates of chronic idiopathic constipation and irritable bowel syndrome with constipation are contributing to greater utilization of both prescription and over-the-counter treatment options. The region benefits from strong implementation of clinical practice guidelines and extensive physician awareness regarding long-term constipation management. Growing research activities focused on gastrointestinal diseases and continuous pharmaceutical innovation are supporting the introduction of novel treatment approaches. CONSTELLA (linaclotide) became the first medicine approved in the European Union for adults with IBS-C and continues to be commercialized across several European countries by AbbVie.

U.K. Constipation Therapeutics Market Insight

The U.K. constipation therapeutics market is experiencing steady growth, driven by increasing awareness of chronic gastrointestinal disorders and growing demand for effective long-term treatment solutions. The country's healthcare system supports broad patient access to both established and innovative constipation therapies through evidence-based treatment pathways. Rising prevalence of constipation among elderly individuals and patients with multiple chronic conditions is contributing to increasing therapeutic demand. Healthcare professionals are increasingly adopting guideline-recommended therapies for patients who do not respond adequately to traditional laxatives. Ongoing clinical research and advances in gastroenterology care are improving disease management and patient outcomes. The National Institute for Health and Care Excellence (NICE) recommends linaclotide for treating chronic constipation in adults whose symptoms persist despite optimal laxative treatment.

Germany Constipation Therapeutics Market Insight

The Germany constipation therapeutics market is expanding steadily due to strong healthcare infrastructure, increasing diagnosis of functional gastrointestinal disorders, and growing utilization of innovative treatment options. The country has a well-developed healthcare system that facilitates patient access to both prescription and over-the-counter constipation therapies. Healthcare providers are increasingly emphasizing early diagnosis and evidence-based management of chronic idiopathic constipation and related disorders. Growing awareness among patients regarding digestive health and treatment availability is further supporting therapeutic adoption. Germany also benefits from active participation in gastrointestinal research and clinical development programs, contributing to continued pharmaceutical innovation

Asia-Pacific Constipation Therapeutics Market Insight

The Asia-Pacific constipation therapeutics market is expected to witness rapid growth, driven by expanding healthcare infrastructure, increasing healthcare expenditure, and rising awareness of gastrointestinal diseases across major economies such as China, India, Japan, and South Korea. Growing urbanization, changing dietary patterns, and increasingly sedentary lifestyles are contributing to a higher prevalence of chronic constipation disorders throughout the region. Improvements in healthcare accessibility and diagnostic capabilities are leading to earlier disease detection and treatment initiation. The growing availability of advanced prescription therapies is expanding treatment options for patients with chronic gastrointestinal conditions. Pharmaceutical companies are increasingly focusing on the region due to its large patient population and significant growth potential.

Japan Constipation Therapeutics Market Insight

The Japan constipation therapeutics market is witnessing consistent growth due to the country's rapidly aging population and increasing prevalence of chronic constipation among elderly individuals. Strong healthcare infrastructure and high levels of healthcare utilization support broad access to both conventional and advanced treatment options. Physicians are increasingly adopting targeted prescription therapies to improve symptom management and long-term patient outcomes. Growing awareness regarding gastrointestinal health and increasing focus on preventive healthcare are contributing to earlier diagnosis and treatment. Japan's active pharmaceutical sector continues to support innovation in gastrointestinal therapeutics through research and development activities. LINZESS was launched in Japan in 2018 for chronic constipation, where it is commercialized by Astellas Pharma, expanding access to advanced GC-C agonist therapy.

China Constipation Therapeutics Market Insight

The China constipation therapeutics market is growing rapidly, driven by increasing urbanization, changing dietary habits, expanding healthcare coverage, and rising awareness of gastrointestinal disorders. A growing middle-class population and improving healthcare accessibility are supporting increased diagnosis and treatment of chronic constipation conditions. Healthcare providers are increasingly adopting modern therapeutic approaches as awareness of evidence-based gastrointestinal care continues to improve. The expansion of pharmaceutical distribution networks and retail pharmacy infrastructure is improving patient access to constipation therapies throughout the country. Rising healthcare expenditure and government initiatives aimed at strengthening healthcare services are further supporting market growth. LINZESS was launched in China in November 2019 for adults with irritable bowel syndrome with constipation and is commercialized by AstraZeneca, expanding access to innovative constipation therapies.

Constipation Therapeutics Market Share

The constipation therapeutics industry is primarily led by well-established companies, including:

- Ironwood (U.S.)

- AbbVie Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Astellas Pharma Inc. (Japan)

- Bausch Health Companies Inc. (Canada)

- Sanofi (France)

- Bayer AG (Germany)

- Pfizer Inc. (U.S.)

- Johnson & Johnson Services Inc. (U.S.)

- AstraZeneca (U.K.)

- GSK plc (U.K.)

- Sebela Pharmaceuticals. (U.S.)

- Ardelyx, Inc. (U.S.)

- Vibrant, LTD. (Israel)

- Cosmo Pharmaceuticals N.V. (Ireland)

- Ferring Pharmaceuticals (Switzerland)

- Roivant Sciences Ltd. (U.K.)

- Janssen Pharmaceuticals, Inc. (U.S.)

- EA Pharma Co., Ltd. (Japan)

- Sucampo Pharmaceuticals, Inc. (U.S.)

Latest Developments in Constipation Therapeutics Market

- In May 2025, the U.S. Food and Drug Administration (FDA) approved the first generic methylnaltrexone bromide injection, referencing Relistor Injection, for the treatment of opioid-induced constipation (OIC) in adults with chronic non-cancer pain. The approval is expected to improve patient access by increasing the availability of lower-cost treatment options for OIC while expanding competition in the constipation therapeutics market

- In December 2024, the U.S. Food and Drug Administration (FDA) approved the first generic version of Motegrity® (prucalopride) tablets for the treatment of chronic idiopathic constipation (CIC) in adults. The approval is expected to improve patient access to selective 5-HT4 receptor agonist therapy by increasing market competition and providing a more affordable treatment option for adults with chronic idiopathic constipation

- In June 2023, Ironwood Pharmaceuticals announced that the U.S. FDA approved LINZESS® (linaclotide) as the first and only prescription therapy for functional constipation in children aged 6–17 years. The approval expanded the therapeutic use of LINZESS beyond adults, providing an evidence-based treatment option for pediatric patients with functional constipation

- In May 2023, the American Gastroenterological Association (AGA) and the American College of Gastroenterology (ACG) jointly released their first evidence-based clinical practice guideline for the pharmacological management of chronic idiopathic constipation (CIC) in adults. The guideline introduced recommendations covering both over-the-counter and prescription therapies, including magnesium oxide, senna, linaclotide, plecanatide, lubiprostone, and prucalopride, supporting more standardized treatment approaches worldwide

- In August 2022, Vibrant Gastro Inc. announced that the U.S. FDA granted marketing authorization for the Vibrant System, the first drug-free vibrating capsule indicated for adults with chronic idiopathic constipation who had not achieved adequate relief with laxative therapy. The technology introduced a novel, non-pharmacological treatment approach by mechanically stimulating the colon to improve bowel motility

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.