Global Consumer Active Optical Cable Market

Market Size in USD Billion

USD

19.48 Billion

USD

84.32 Billion

2025

2033

USD

19.48 Billion

USD

84.32 Billion

2025

2033

| 2026 - 2033 | |

| USD 19.48 Billion | |

| USD 84.32 Billion | |

| % | |

|

Consumer Active Optical Cable Market Overview

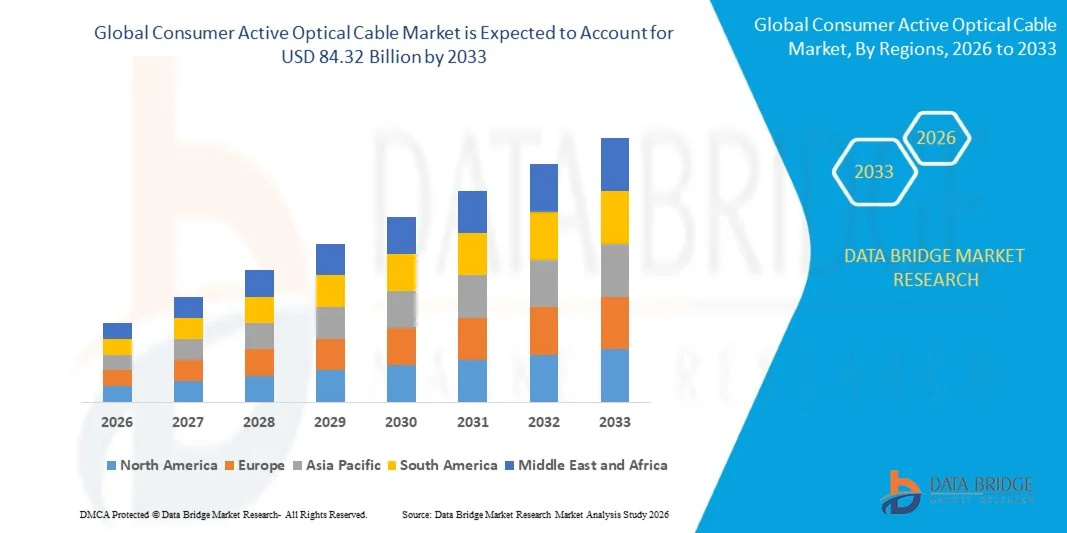

The Consumer Active Optical Cable Market was valued at USD 19.48 Billion in 2025 and is projected to reach USD 84.32 Billion by 2033, growing at a CAGR of 20.10% from 2026 to 2033. The market is experiencing consistent growth driven by rapid expansion of hyperscale data centers, increasing adoption of cloud computing infrastructure, and rising demand for high-speed, low-latency data transmission solutions. Continuous upgrades in network bandwidth requirements, including migration toward 400G and 800G architectures, are further accelerating the adoption of active optical cable technologies across enterprise and telecom environments.

The increasing global reliance on data-intensive applications such as artificial intelligence, machine learning, video streaming, and big data analytics is significantly boosting demand for advanced optical interconnect solutions. Enterprises are increasingly replacing traditional copper-based interconnects with active optical cables to improve energy efficiency, reduce latency, and enhance transmission distance. In addition, growing investments in digital transformation initiatives and next-generation data center expansion are further supporting sustained market growth across major regions.

Key Market Trends & Insights

- North America dominated the Consumer Active Optical Cable Market with the largest revenue share of 37.9% in 2025, supported by strong hyperscale data center expansion, high adoption of cloud computing infrastructure, and early deployment of high-speed networking technologies

- The ethernet segment led the market with a 48% share in 2025, driven by its widespread deployment in high-speed networking, enterprise connectivity, and data-intensive environments

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 12% from 2026 to 2033, fueled by rapid expansion of hyperscale data centers, increasing internet penetration, and strong growth in cloud computing and AI infrastructure

- Infiniband are the fastest-growing technology type, projected to register a CAGR of 16% from 2026 to 2033, supported by rising adoption in high-performance computing and advanced data center interconnects

- The SFP segment dominated the connector type category with a 44% revenue share in 2025, led by its compact design, cost efficiency, and strong compatibility with enterprise networking equipment

- Data center accounted for 32% of the market in 2025, preferred by exponential growth in cloud computing, AI workloads, and hyperscale infrastructure development.

- The CFP segment is the fastest-growing connector type category, with a CAGR of 14.5% from 2026 to 2033, driven by increasing demand for ultra-high bandwidth transmission in hyperscale data centers and backbone networks

Market Size & Forecast

- Global Market Value (2025): USD 19.48 Billion

- Expected Market Value (2033): USD 84.32 Billion

- Forecast CAGR (2026–2033): 20.10%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Consumer Active Optical Cable Market Segmentation

|

Attributes |

Consumer Active Optical Cable Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Molex, LLC (U.S.) · Finisar Corporation (U.S.) · Amphenol ICC (U.S.) · Shenzhen Gigalight Technology Co., Ltd. (China) · Shenzhen Sopto Technology Co., Ltd. (China) · FUJITSU (Japan) · Broadcom (U.S.) · 3M (U.S.) · IBM Corporation (U.S.) · Siemon (U.S.) · EMCORE Corporation (U.S.) · Sumitomo Electric Industries, Ltd. (Japan) · Samtec (U.S.) · Hitachi Metals, Ltd. (Japan) · Fujikura Ltd. (Japan) · Chromis (U.S.) · Cosemi Technologies, Inc. (U.S.) · Mellanox Technologies (Israel/U.S.) · Vishay Intertechnology, Inc. (U.S.) · STMicroelectronics (Switzerland/France) · Texas Instruments Incorporated (U.S.) · Analog Devices, Inc. (U.S.) · Semiconductor Components Industries, LLC (U.S.) · ams AG (Austria) · Hamamatsu Photonics K.K. (Japan) · ABB (Switzerland) · ROHM CO., LTD. (Japan) · Infineon Technologies AG (Germany) · Sony Corporation (Japan) · Fairchild Semiconductor International, Inc. (U.S.) |

|

Market Opportunities |

· Expansion of Hyperscale Data Center Infrastructure Globally · Growing Adoption in AI, Machine Learning, and High-Performance Computing Workloads · Rising Replacement of Copper Cables with Energy-Efficient Optical Interconnect Solutions |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Consumer Active Optical Cable Market Trends

Trend: Rising Adoption of 400G and 800G Data Center Interconnects

The Consumer Active Optical Cable market is witnessing a strong trend toward rapid deployment of 400G and 800G data center interconnects driven by exponential growth in AI workloads, cloud computing, and hyperscale infrastructure. Active optical cables are increasingly replacing copper-based interconnects to support higher bandwidth, longer transmission distance, and lower power consumption in dense server environments. Major hyperscale operators are upgrading network architectures to meet rising data traffic demands generated by machine learning and real-time analytics.

Companies such as Microsoft Azure and Google Cloud have been expanding 400G and early 800G-ready data center infrastructure, accelerating adoption of high-speed optical interconnect solutions across global cloud ecosystems.

Consumer Active Optical Cable Market Dynamics

Key Market Driver: Growing Demand for Low-Latency AI Driven Connectivity

The increasing adoption of artificial intelligence, high-performance computing, and real-time data processing is significantly driving demand for ultra-low latency connectivity solutions. Consumer Active Optical Cables are widely used in AI clusters, GPU-based computing systems, and hyperscale data centers where high-speed data transfer is critical. The shift toward distributed computing and edge AI infrastructure is further strengthening demand for high-bandwidth optical interconnects.

Companies such as NVIDIA and Meta Platforms are heavily deploying high-speed InfiniBand and Ethernet-based optical interconnect architectures to support AI training clusters and large-scale machine learning workloads.

Key Restraint/Challenge: High Deployment and Integration Cost of Active Optical Cables

Despite strong adoption, the market faces challenges due to high installation, deployment, and system integration costs associated with active optical cable infrastructure. Costs remain elevated due to advanced transceiver components, precision manufacturing requirements, and compatibility upgrades needed for 400G and 800G systems. Additional expenses arise from data center redesign, cooling requirements, and maintenance of high-density optical networks.

For instance, hyperscale data center operators such as Amazon Web Services (AWS) incur significant capital expenditure when transitioning from copper to high-speed optical interconnect architectures, particularly during large-scale network upgrades.

Key Market Opportunity: Expansion of Hyperscale Data Center Infrastructure Globally

The rapid expansion of hyperscale data centers across North America, Asia-Pacific, and Europe presents a major growth opportunity for the Consumer Active Optical Cable market. Increasing demand for cloud services, streaming platforms, and AI-driven applications is driving large-scale investments in new data center construction and expansion projects. Active optical cables are becoming essential for enabling scalable, high-density, and energy-efficient interconnect architectures in these facilities.

Companies such as Google, Microsoft, and Alibaba Cloud continue to expand hyperscale data center footprints globally, significantly boosting demand for next-generation optical connectivity solutions.

Consumer Active Optical Cable Market Scope

The consumer active optical cable market is segmented on the basis of technology, connector type, and end user.

- By Technology

On the basis of technology, the Consumer Active Optical Cable Market is segmented into High Definition Media Interface (HDMI), Infiniband, Ethernet, Serial-Attached SCSI (SAS), and others. The Ethernet segment dominated the market with the largest share of 48% in 2025, supported by its widespread deployment in high-speed networking, enterprise connectivity, and data-intensive environments. Strong compatibility with existing infrastructure and cost-efficient scalability strengthens its adoption across large-scale data transmission systems. Increasing demand for low-latency communication in cloud computing and enterprise networks further reinforces its leading position. Continuous upgrades in Ethernet bandwidth capabilities enhance its suitability for modern optical cable deployments.

The Infiniband segment is projected to register the fastest growth at a CAGR of 16% from 2026 to 2033, driven by rising adoption in high-performance computing and advanced data center interconnects. Expanding requirements for ultra-low latency and high-throughput communication in AI workloads and supercomputing clusters accelerate demand. Growing deployment in hyperscale data centers supports its integration with active optical cable solutions. Advancements in parallel processing architectures and high-speed interconnect technologies further boost segment expansion. Increasing investment in AI infrastructure globally continues to strengthen growth momentum.

- By Connector Type

On the basis of connector type, the Consumer Active Optical Cable Market is segmented into SFP, CFP, and others. The SFP segment dominated the market with a share of 44% in 2025, driven by its compact design, cost efficiency, and strong compatibility with enterprise networking equipment. High adoption in data centers and telecom infrastructure supports its widespread utilization for short to medium-range high-speed connectivity. Ease of installation and flexible deployment options further enhance its market penetration. Continuous upgrades to higher data rate SFP variants reinforce its dominant position in optical connectivity solutions.

The CFP segment is projected to register the fastest growth at a CAGR of 14.5% from 2026 to 2033, supported by increasing demand for ultra-high bandwidth transmission in hyperscale data centers and backbone networks. Rising deployment in 400G and 800G optical communication systems accelerates adoption. Growing need for long-distance, high-capacity data transfer strengthens its relevance in next-generation network architectures. Technological advancements in coherent optics and dense wavelength multiplexing further enhance performance capabilities. Expanding investments in global data center expansion continue to support segment growth.

- By End-user

On the basis of end-user application, the Consumer Active Optical Cable Market is segmented into data center, consumer electronics, and others. The data center segment dominated the market with the largest share of 32% in 2025, driven by exponential growth in cloud computing, AI workloads, and hyperscale infrastructure development. High demand for high-speed, low-latency interconnect solutions strengthens adoption of active optical cables in server-to-server and switch-to-switch connectivity. Rapid expansion of hyperscale facilities and colocation centers further supports market leadership. Continuous upgrades in data transmission capacity requirements reinforce sustained dominance.

The consumer electronics segment is projected to register the fastest growth at a CAGR of 13.5% from 2026 to 2033, driven by increasing demand for high-definition content streaming, gaming systems, and advanced home entertainment devices. Rising integration of high-speed optical connectivity in smart devices enhances user experience and performance. Growing penetration of ultra-high-definition displays and immersive media technologies supports adoption. Advancements in compact optical cable design and cost reduction further accelerate market expansion. Expanding digital consumption trends continue to drive strong growth momentum.

Consumer Active Optical Cable Market Regional Analysis

North America dominated the consumer active optical cable market and accounted for the largest revenue share of 37.9% in 2025, driven by strong hyperscale data center expansion, high adoption of cloud computing infrastructure, and early deployment of high-speed networking technologies. The region benefits from a highly mature digital ecosystem, widespread availability of advanced fiber optic infrastructure, and strong investment from leading technology companies in AI and high-performance computing clusters. Enterprises across IT, telecom, cloud services, and financial sectors are increasingly adopting active optical cables to support low-latency and high-bandwidth data transmission requirements. In addition, the presence of major data center operators and continuous upgrades in 400G and 800G network architectures further reinforce North America’s leadership position in the global market.

U.S. Consumer Active Optical Cable Market Insight

The U.S. Consumer Active Optical Cable market is witnessing strong growth driven by rapid expansion of hyperscale data centers, increasing AI workload processing, and large-scale deployment of cloud-based infrastructure. Enterprises are heavily investing in high-speed interconnect solutions to support data-intensive applications such as machine learning, big data analytics, and edge computing. The country’s strong presence of leading technology firms and advanced semiconductor ecosystem is enabling faster adoption of next-generation optical connectivity solutions. In addition, continuous upgrades in network bandwidth capacity and rising demand for ultra-low latency communication are further accelerating market expansion across the U.S.

Canada Consumer Active Optical Cable Market Insight

The Canada Consumer Active Optical Cable market is experiencing steady growth supported by increasing investments in data center infrastructure, expanding cloud adoption, and rising digital transformation across enterprises. Businesses in telecom, BFSI, and IT sectors are increasingly deploying high-speed optical connectivity solutions to enhance network performance and reliability. The country’s growing focus on secure and energy-efficient data transmission is encouraging adoption of active optical cables in modern networking environments. In addition, expansion of hyperscale and colocation data centers is further contributing to market growth across Canada.

Europe Consumer Active Optical Cable Market Insight

The Europe Consumer Active Optical Cable market is expanding steadily due to strong digital infrastructure development, increasing adoption of cloud services, and rising demand for high-speed enterprise networking solutions. The region benefits from robust regulatory frameworks supporting digital transformation and strong investments in next-generation data centers. Enterprises across IT, telecom, automotive, and financial services are increasingly adopting active optical cables to support high-bandwidth workloads and real-time data processing. In addition, growing deployment of AI-enabled infrastructure and sustainable data center initiatives continues to support regional market growth.

U.K. Consumer Active Optical Cable Market Insight

The U.K. Consumer Active Optical Cable market is growing steadily, driven by strong digital economy development, high cloud adoption rates, and increasing investments in data center expansion. Enterprises are focusing on upgrading legacy networking systems with high-speed optical connectivity to support modern workloads such as AI analytics and streaming services. The presence of a well-established fintech and IT services ecosystem further strengthens demand for advanced interconnect solutions. In addition, rising focus on energy-efficient and scalable data center infrastructure is supporting continued market expansion in the U.K.

Germany Consumer Active Optical Cable Market Insight

The Germany Consumer Active Optical Cable market is expanding due to strong industrial digitization, increasing deployment of smart manufacturing systems, and rising demand for high-performance data transmission. Enterprises in automotive, manufacturing, and enterprise IT sectors are adopting active optical cables to support advanced automation, IoT, and real-time analytics applications. The country’s emphasis on secure and reliable digital infrastructure is driving investments in high-speed optical networking technologies. In addition, growing integration of AI and cloud-based systems across industrial operations is further accelerating market development in Germany.

Asia-Pacific Consumer Active Optical Cable Market Insight

The Asia-Pacific Consumer Active Optical Cable market is expected to register the fastest growth with a CAGR of 12% from 2026 to 2033, driven by rapid expansion of hyperscale data centers, increasing internet penetration, and strong growth in cloud computing and AI infrastructure. Rising digital transformation across enterprises and SMEs is significantly boosting demand for high-speed optical connectivity solutions. Countries such as China, India, Japan, and South Korea are witnessing strong investments in data center expansion and advanced network architectures. In addition, growing adoption of 5G, edge computing, and e-commerce platforms is further accelerating regional market expansion.

Japan Consumer Active Optical Cable Market Insight

The Japan Consumer Active Optical Cable market is witnessing steady growth supported by advanced digital infrastructure, strong adoption of automation technologies, and increasing demand for high-speed data transmission in enterprise networks. Enterprises are leveraging active optical cables to enhance performance in data centers, telecom networks, and industrial IT systems. The country’s focus on robotics, AI integration, and smart city initiatives is further strengthening demand for high-bandwidth connectivity solutions. In addition, rising deployment of cloud-based services and edge computing applications is supporting continued market growth in Japan.

China Consumer Active Optical Cable Market Insight

The China Consumer Active Optical Cable market is growing rapidly due to massive expansion of hyperscale data centers, strong government support for digital infrastructure, and increasing adoption of AI-driven technologies. Enterprises are investing heavily in high-speed optical interconnect solutions to support large-scale cloud computing, e-commerce platforms, and big data analytics. The country’s strong manufacturing ecosystem for optical components further supports cost-efficient deployment of active optical cable solutions. In addition, rapid rollout of 5G networks and increasing demand for real-time data processing are further driving market growth in China.

Consumer Active Optical Cable Market Share

The consumer active optical cable industry is primarily led by well-established companies, including:

- Molex, LLC (U.S.)

- Finisar Corporation (U.S.)

- Amphenol ICC (U.S.)

- Shenzhen Gigalight Technology Co., Ltd. (China)

- Shenzhen Sopto Technology Co., Ltd. (China)

- FUJITSU (Japan)

- Broadcom (U.S.)

- 3M (U.S.)

- IBM Corporation (U.S.)

- Siemon (U.S.)

- EMCORE Corporation (U.S.)

- Sumitomo Electric Industries, Ltd. (Japan)

- Samtec (U.S.)

- Hitachi Metals, Ltd. (Japan)

- Fujikura Ltd. (Japan)

- Chromis (U.S.)

- Cosemi Technologies, Inc. (U.S.)

- Mellanox Technologies (Israel/U.S.)

- Vishay Intertechnology, Inc. (U.S.)

- STMicroelectronics (Switzerland/France)

- Texas Instruments Incorporated (U.S.)

- Analog Devices, Inc. (U.S.)

- Semiconductor Components Industries, LLC (U.S.)

- ams AG (Austria)

- Hamamatsu Photonics K.K. (Japan)

- ABB (Switzerland)

- ROHM CO., LTD. (Japan)

- Infineon Technologies AG (Germany)

- Sony Corporation (Japan)

- Fairchild Semiconductor International, Inc. (U.S.)

Latest Developments in Consumer Active Optical Cable Market

- In January 2025, Coherent Corp. expanded its high-speed optical interconnect portfolio to strengthen 400G and 800G active optical cable solutions for data center applications. This development significantly strengthens Coherent’s position in the rapidly expanding hyperscale and AI-driven data center market. The expansion enhances supply capacity for ultra-high bandwidth connectivity, directly supporting growing demand from AI training clusters and cloud infrastructure operators. It also improves the availability of advanced AOC solutions that reduce latency and power consumption in dense server environments. As a result, it reinforces competitive intensity in the global optical interconnect ecosystem

- In September 2024, NVIDIA advanced its integrated networking ecosystem through continued enhancement of its Mellanox-based InfiniBand and Ethernet platforms supporting optical interconnect technologies. This development strengthens NVIDIA’s dominance in AI infrastructure by enabling tighter integration between GPUs and high-speed optical networking systems. It accelerates adoption of active optical cable-based architectures in AI supercomputing environments where ultra-low latency is critical. The move enhances system-level performance efficiency across hyperscale data centers. It also reinforces demand for high-bandwidth optical connectivity in AI and machine learning workloads globally

- In June 2024, Cisco Systems expanded its 400G and early 800G optical networking portfolio to support next-generation data center scalability. This expansion improves Cisco’s ability to serve cloud service providers and enterprise data centers requiring ultra-high-speed interconnect solutions. It enhances the adoption of active optical cable technologies by enabling seamless integration with advanced switching and routing infrastructure. The development supports rising bandwidth demands driven by AI applications, video streaming, and edge computing. It further strengthens the transition toward high-capacity optical-based network architectures

- In March 2024, Amphenol Corporation strengthened its high-speed interconnect business by expanding its active optical cable assembly offerings for hyperscale data centers. This expansion enhances Amphenol’s market presence in high-density computing environments where compact, low-power interconnects are essential. It improves system reliability and thermal efficiency in large-scale server deployments. The development supports increasing adoption of optical cables in cloud and telecom infrastructure upgrades. It also reinforces supply chain scalability for high-speed connectivity solutions across global data center markets

- In January 2024, Molex expanded its portfolio of next-generation active optical cable solutions targeting cloud and enterprise networking applications. This development enhances Molex’s competitiveness in high-bandwidth interconnect markets by addressing growing demand for 100G and 400G connectivity. It supports improved energy efficiency and signal integrity in dense computing environments. The expansion aligns with rising hyperscale data center deployments and AI-driven infrastructure growth. It also strengthens the company’s position in the evolving high-speed optical connectivity ecosystem

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Consumer Active Optical Cable Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Consumer Active Optical Cable Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Consumer Active Optical Cable Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.