Global Continuous Bioprocessing Consumables Market

Market Size in USD Million

USD

656.88 Million

USD

1,927.06 Million

2025

2033

USD

656.88 Million

USD

1,927.06 Million

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 656.88 Million |

Market Size (Forecast Year) |

USD 1,927.06 Million |

CAGR |

% |

Major Markets Players |

|

Continuous Bioprocessing Consumables Market Size

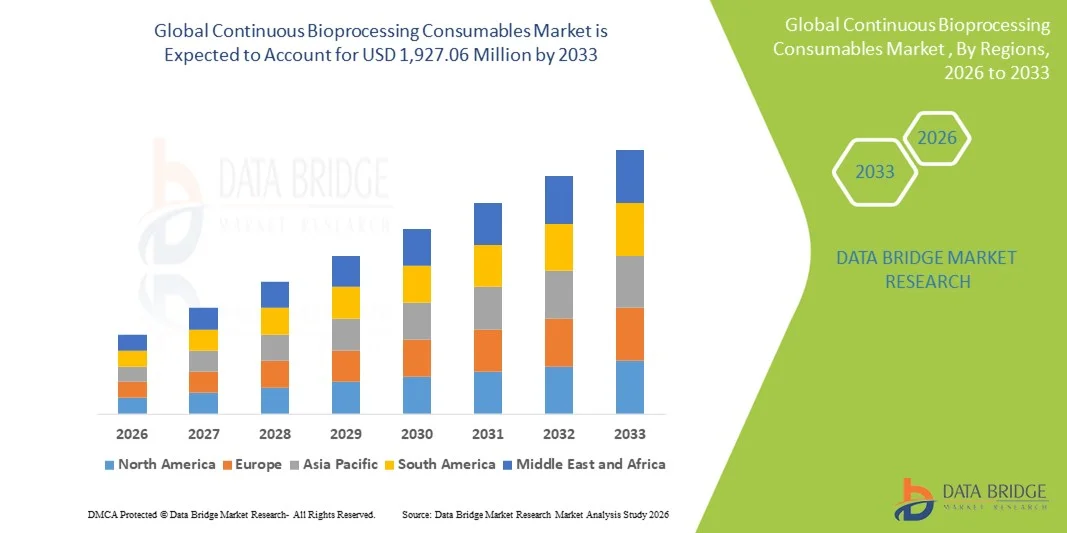

- The global continuous bioprocessing consumables market size was valued at USD 656.88 million in 2025 and is expected to reach USD 1,927.06 million by 2033, at a CAGR of 14.40% during the forecast period

- The market growth is largely fueled by the increasing shift toward continuous manufacturing, driven by rising biologics production, demand for higher process efficiency, and strong adoption of single-use systems across upstream and downstream bioprocessing

- Furthermore, the need for cost-efficient, scalable, and contamination-free production workflows is positioning continuous bioprocessing consumables such as filters, tubing, bags, and chromatography membranes as essential components of modern biomanufacturing. These converging factors are accelerating the deployment of continuous platforms, thereby significantly boosting the industry's growth

Continuous Bioprocessing Consumables Market Analysis

- Continuous bioprocessing consumables, including single-use assemblies & bags, tubing, fittings, filtration consumables, membranes, chromatography resins, and disposable sensors, are becoming increasingly vital components of modern biologics manufacturing due to their ability to support sterile, flexible, and fully integrated continuous upstream and downstream operations

- The escalating demand for these consumables is primarily fueled by the rapid shift toward continuous manufacturing in biopharma, growing biologics production volumes, and rising preference for single-use solutions that reduce contamination risks, lower operational costs, and eliminate cleaning and validation requirements

- North America dominated the continuous bioprocessing consumables market with the largest revenue share of 40.6% in 2025, characterized by strong adoption of advanced biomanufacturing technologies, significant investment from major biopharmaceutical companies, and a mature ecosystem of suppliers and CDMOs, with the U.S. leading continuous platform installations supported by regulatory encouragement and high biologics output

- Asia-Pacific is expected to be the fastest growing region in the continuous bioprocessing consumables market during the forecast period due to expanding biopharmaceutical manufacturing capacity, increasing government investments, and rapid adoption of single-use systems in emerging biologics hubs such as China, India, South Korea, and Singapore

- Single-use assemblies & bags dominated the continuous bioprocessing consumables market with a market share of 30.9% in 2025, driven by their essential role in sterile fluid handling, perfusion culture, buffer management, and downstream processing, along with their ease of integration into continuous systems and compatibility with flexible, multi-product manufacturing setups

Report Scope and Continuous Bioprocessing Consumables Market Segmentation

|

Attributes |

Continuous Bioprocessing Consumables Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Continuous Bioprocessing Consumables Market Trends

Accelerated Shift Toward Integrated Single-Use Continuous Platforms

- A significant and accelerating trend in the global continuous bioprocessing consumables market is the deepening shift toward fully integrated single-use continuous platforms across upstream and downstream operations, as biomanufacturers increasingly prioritize sterility, operational flexibility, and real-time process efficiency

- For instance, Sartorius’ single-use continuous bioreactor and filtration assemblies enable seamless connection of perfusion culture with downstream purification, supporting uninterrupted biologics production with reduced manual intervention

- AI-enabled automation within continuous systems enhances process analytics by learning performance patterns, predicting deviations, and optimizing consumable usage; for instance, advanced single-use sensors from companies such as Fluence Analytics are being adopted for real-time monitoring of critical quality attributes in continuous workflows

- The seamless integration of continuous consumables with process analytical technologies (PAT) and manufacturing control software enables centralized oversight of culture, filtration, and chromatography operations, supporting end-to-end continuous manufacturing environments

- This trend toward more intelligent, interconnected, and efficiency-driven continuous bioprocessing systems is reshaping expectations for scalable biologics manufacturing; consequently, companies such as Repligen are expanding single-use flow path offerings to improve connectivity and automated control across continuous operations

- The demand for consumables that support automated, integrated, and contamination-free continuous workflows is rising rapidly across biopharma and CDMO facilities, as manufacturers increasingly prioritize productivity, consistency, and cost-efficient biologics production

Continuous Bioprocessing Consumables Market Dynamics

Driver

Growing Need Due to Rising Biologics Production and Shift Toward Continuous Manufacturing

- The increasing global demand for biologics, coupled with the accelerating industry shift from batch to continuous manufacturing, is a significant driver for the growing requirement for continuous bioprocessing consumables

- For instance, in April 2025, Thermo Fisher Scientific expanded its single-use continuous filtration and chromatography consumables portfolio to support higher-yield biologics manufacturing at commercial scale, reinforcing the industry’s transition toward continuous platforms

- As manufacturers seek greater process efficiency, reduced contamination risk, and faster turnaround times, continuous consumables offer advantages such as closed-loop fluid management, real-time monitoring, and reduced cleaning demands, making them a compelling upgrade over traditional reusable systems

- Furthermore, the rising adoption of single-use assemblies, sensors, and filtration consumables in biopharma facilities is driven by the need for flexible, modular production lines that integrate easily with perfusion, continuous capture, and continuous polishing systems

- The convenience of simplified changeovers, scalability from pilot to commercial operations, and improved sterility control are key factors propelling the adoption of continuous consumables across pharmaceutical companies, CDMOs, and research facilities. The trend toward automation-ready, standardized single-use components further contributes to market growth

Restraint/Challenge

Sterility Assurance Issues and Regulatory Compliance Hurdle

- Concerns surrounding the sterility assurance of single-use consumables and the strict validation requirements associated with continuous bioprocessing pose a significant challenge to broader adoption across global biomanufacturing

- For instance, reports highlighting extractables and leachables concerns or failure of single-use components under continuous high-pressure operations have made some manufacturers cautious about rapid implementation of such systems

- Addressing these sterility and compliance challenges through stronger material characterization, robust quality control, and validated continuous-use testing is crucial for building customer confidence; companies such as Merck emphasize advanced material science and rigorous testing to reassure potential users. In addition, the relatively high cost of specialized continuous consumables compared to conventional batch consumables can be a barrier for smaller manufacturers or cost-sensitive facilities

- While prices are gradually decreasing, the perceived premium for advanced single-use continuous components can still hinder widespread adoption, especially for organizations transitioning from deeply established batch processes

- Overcoming these challenges through improved regulatory guidance, increased transparency around material testing, and development of more cost-efficient continuous consumable alternatives will be vital for sustained market growth

Continuous Bioprocessing Consumables Market Scope

The market is segmented on the basis of product, process stage, application, and end user.

- By Product

On the basis of product, the continuous bioprocessing consumables market is segmented into single-use assemblies & bags, tubing, fittings & connectors, filtration consumables, membranes & cartridges, chromatography resins & single-use columns, single-use sensors & probes, sampling & aseptic transfer consumables, media & buffer consumables, and ancillary disposables. The single-use assemblies & bags segment dominated the market with the largest market revenue share of 30.9% in 2025, driven by their essential role as core fluid-handling components in perfusion bioreactors, buffer preparation, and continuous downstream operations. Manufacturers rely heavily on assemblies & bags due to their high sterility assurance, scalability, and seamless compatibility with integrated continuous platforms. Their ability to be customized for diverse unit operations such as media storage, harvest, and aseptic transfer reinforces their widespread adoption. The growing shift toward end-to-end single-use bioprocessing further strengthens demand, as these consumables offer operational flexibility and significantly reduce cleaning validation efforts. Their extensive use by CDMOs and large biopharma manufacturers ensures sustained market leadership.

The single-use sensors & probes segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for real-time process monitoring and automation within continuous biomanufacturing environments. These sensors support critical parameters such as pH, DO, pressure, and biomass measurement, enabling high-precision control of continuous upstream and downstream workflows. For instance, the increasing adoption of PAT (Process Analytical Technology) frameworks is encouraging manufacturers to deploy disposable sensors that enhance process robustness while reducing contamination risk. As biologics production becomes more data-driven, real-time analytics through single-use sensors are becoming indispensable. Their compatibility with closed, sterile, single-use systems makes them ideal for integrated continuous processing setups. Advancements in optical and biosensor technologies are further accelerating segment growth.

- By Process Stage

On the basis of process stage, the market is segmented into upstream, downstream, and integrated continuous processing. The upstream segment dominated the market with the largest market revenue share of 46.7% in 2025, primarily due to the rapid adoption of perfusion-based bioreactors and intensified cell culture systems. In continuous upstream processes, consumables such as single-use bioreactor bags, perfusion filters, and tubing sets are essential for maintaining long-duration, high-density cultures. The rising demand for monoclonal antibodies and recombinant proteins requiring sustained upstream operations supports segment dominance. Continuous perfusion technologies also significantly reduce footprint while enhancing productivity, leading to higher consumption of upstream consumables. As biopharma manufacturers shift from fed-batch to continuous upstream operations, the need for scalable, sterile, and durable consumables continues to rise. Strong investment in next-generation bioreactors further reinforces this leadership.

The integrated continuous processing segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing industry shift toward fully connected end-to-end continuous biomanufacturing. Integrated systems require a complete suite of consumables—ranging from assemblies and filtration devices to sensors and chromatography columns—that can operate seamlessly across upstream and downstream functions. For instance, biopharma manufacturers implementing connected perfusion-to-continuous chromatography workflows are generating strong demand for unified, automation-ready consumables. Integrated processing enhances productivity, reduces batch variability, and supports rapid scale-out manufacturing models, making it highly attractive for biologics and advanced therapies. As regulatory agencies increasingly endorse continuous manufacturing frameworks, adoption of integrated systems and associated consumables is accelerating. This trend is further reinforced by rising CDMO investments in end-to-end continuous platforms.

- By Application

On the basis of application, the market is segmented into monoclonal antibodies, recombinant proteins, vaccines, gene therapy, and biosimilars. The monoclonal antibodies (mAbs) segment dominated the market with the largest market revenue share of 41.2% in 2025, supported by high global demand for therapeutic antibodies and the strong suitability of continuous bioprocessing for mAb production. Continuous perfusion culture and chromatography enable higher product yield, improved quality consistency, and reduced operational costs for mAbs, driving consumable use across upstream and downstream functions. For instance, leading biopharma manufacturers producing blockbuster mAbs are increasingly adopting continuous operations to enhance output. The expansion of oncology and autoimmune disease therapeutics further increases mAb production needs. Given that mAbs remain the largest revenue-generating biologics class, their reliance on continuous manufacturing consumables ensures sustained dominance. CDMOs dedicated to mAb production also contribute significantly to segment share.

The gene therapy segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rapid expansion of viral vector manufacturing and advanced therapy pipelines. Continuous bioprocessing offers major benefits for gene therapy production, including improved scalability, reduced shear stress, and enhanced process consistency for viral vectors such as AAV and lentivirus. For instance, several biotech firms are adopting perfusion-based systems for vector production, increasing reliance on high-performance single-use consumables. Gene therapies often require high-purity processing, which boosts demand for specialized filtration, chromatography, and aseptic transfer consumables. As the number of commercial approvals and clinical trials grows globally, manufacturers are turning to continuous processes to meet production efficiency requirements. This strong momentum is driving rapid segment expansion.

- By End User

On the basis of end user, the market is segmented into pharmaceutical & biopharmaceutical companies, CMOs, academic & research institutes, and equipment OEMs. The pharmaceutical & biopharmaceutical companies segment dominated the market with the largest market revenue share of 52.8% in 2025, owing to the widespread adoption of continuous bioprocessing technologies by major biologics producers. Large biopharma companies increasingly rely on continuous production to enhance efficiency, reduce manufacturing costs, and support growing global demand for biologics. For instance, leading manufacturers implementing intensified upstream and continuous downstream workflows are driving demand for high-volume single-use consumables. These companies also operate multiple commercial biologics facilities, resulting in continuous and large-scale consumable consumption. Their strong investment capability and focus on innovation keep this segment at the forefront of market adoption. The expansion of biologics pipelines further reinforces segment dominance.

The CMOs segment is anticipated to witness the fastest growth rate from 2026 to 2033, propelled by the rising trend of outsourcing biologics manufacturing and the need for flexible, multi-product production environments. CMOs adopt continuous bioprocessing consumables to offer cost-efficient, scalable, and rapid manufacturing solutions to multiple clients. For instance, several global CDMOs are expanding their continuous manufacturing suites to attract biopharma partners seeking faster development timelines. Continuous systems also support high-throughput processing, making them ideal for clinical trial material production. As more biotech startups and mid-sized firms choose outsourcing over in-house manufacturing, CMOs’ utilization of continuous consumables increases significantly. Their ability to serve diverse biologics modalities further accelerates segment growth.

Continuous Bioprocessing Consumables Market Regional Analysis

- North America dominated the continuous bioprocessing consumables market with the largest revenue share of 40.6% in 2025, characterized by strong adoption of advanced biomanufacturing technologies, significant investment from major biopharmaceutical companies, and a mature ecosystem of suppliers and CDMOs

- Manufacturers in the region highly value the improved productivity, reduced footprint, and enhanced sterility assurance offered by continuous consumables integrated into upstream and downstream systems

- This adoption is further supported by a well-established regulatory environment that encourages innovation in biologics manufacturing, along with substantial R&D expenditure by major pharma and biotech firms

U.S. Continuous Bioprocessing Consumables Market Insight

The U.S. continuous bioprocessing consumables market captured the largest revenue share of 82% in 2025 within North America, fueled by rapid adoption of single-use technologies and the strong transition toward intensified biologics manufacturing processes. Biopharmaceutical companies are increasingly prioritizing continuous upstream and downstream workflows to enhance throughput, reduce costs, and ensure sterility. The growing preference for fully connected, automated biomanufacturing suites, combined with rising investments in continuous platforms by major biologics producers, further propels market expansion. Moreover, the widespread integration of PAT tools, single-use sensors, and perfusion-enabled consumables is significantly contributing to the market’s growth.

Europe Continuous Bioprocessing Consumables Market Insight

The Europe continuous bioprocessing consumables market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent regulatory encouragement for advanced manufacturing and the growing need for reliable, contamination-free biologics production. The increase in biopharmaceutical R&D activities, coupled with the rising demand for flexible, single-use–enabled facilities, is fostering adoption across the region. European manufacturers are also drawn to the efficiency, sustainability, and reduced footprint associated with continuous bioprocessing. The region is experiencing significant growth across monoclonal antibody, vaccine, and biosimilar manufacturing, with continuous consumables being incorporated into both new biomanufacturing facilities and modernization projects.

U.K. Continuous Bioprocessing Consumables Market Insight

The U.K. continuous bioprocessing consumables market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the escalating emphasis on biopharmaceutical innovation and the rising demand for advanced, flexible production systems. In addition, expanding biologics research and increasing investments in next-generation manufacturing facilities are encouraging both established companies and emerging biotechs to adopt continuous processing. The U.K.’s strong life sciences ecosystem, paired with government support for digital and automated biomanufacturing, is expected to continue stimulating market growth.

Germany Continuous Bioprocessing Consumables Market Insight

The Germany continuous bioprocessing consumables market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of manufacturing efficiency and the demand for technologically advanced, eco-conscious production solutions. Germany’s well-developed biopharmaceutical infrastructure, combined with its emphasis on precision engineering and sustainability, promotes the rapid adoption of continuous consumables in both upstream and downstream systems. The integration of automated, sensor-equipped single-use technologies is becoming increasingly prevalent, with a strong preference for high-quality, compliant solutions aligning with local industry expectations.

Asia-Pacific Continuous Bioprocessing Consumables Market Insight

The Asia-Pacific continuous bioprocessing consumables market is poised to grow at the fastest CAGR of 24% during the forecast period of 2026 to 2033, driven by expanding biologics manufacturing capacity, rising investment in biopharma infrastructure, and accelerated adoption of single-use systems in countries such as China, Japan, South Korea, and India. The region’s growing inclination toward high-efficiency bioprocessing, supported by government initiatives promoting biomanufacturing modernization, is driving demand for continuous consumables. Furthermore, as APAC strengthens its position as a global hub for biologics and biosimilar production, the affordability and accessibility of high-quality consumables are expanding rapidly.

Japan Continuous Bioprocessing Consumables Market Insight

The Japan continuous bioprocessing consumables market is gaining momentum due to the country’s advanced technological environment, aging population demanding biologics, and strong focus on manufacturing precision. The Japanese market places significant emphasis on consistency, sterility, and process control, driving adoption of continuous systems in monoclonal antibody and vaccine production. The integration of continuous consumables with other high-tech automation systems, including real-time monitoring tools and advanced single-use sensors, is fueling market growth. Moreover, Japan’s commitment to pharmaceutical innovation is such asly to spur increasing demand for efficient, high-performance consumable solutions.

India Continuous Bioprocessing Consumables Market Insight

The India continuous bioprocessing consumables market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s expanding biopharmaceutical manufacturing landscape, rapid growth in biosimilar production, and increasing adoption of single-use technologies. India stands as one of the fastest-growing biologics manufacturing hubs, and continuous consumables are becoming increasingly essential in both upstream and downstream systems across research, clinical, and commercial facilities. The push toward biomanufacturing modernization, paired with strong local suppliers and cost-efficient production capabilities, is a key factor propelling market growth in India.

Continuous Bioprocessing Consumables Market Share

The Continuous Bioprocessing Consumables industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc. (U.S.)

- Sartorius AG (Germany)

- Merck KGaA (Germany)

- Danaher (U.S.)

- Pall Corporation (U.S.)

- Repligen Corporation (U.S.)

- Eppendorf AG (Germany)

- Corning Incorporated (U.S.)

- Meissner Filtration Products, Inc (U.S.)

- Avantor, Inc. (U.S.)

- Saint Gobain Life Sciences (France)

- Entegris, Inc. (U.S.)

- PBS Biotech, Inc. (U.S.)

- Lonza Group AG (Switzerland)

- FUJIFILM Diosynth Biotechnologies (Japan)

- Asahi Kasei Corporation (Japan)

- 3M (U.S.)

- Getinge AB (Sweden)

- GE Healthcare (U.S.)

- Samsung Biologics (South Korea)

What are the Recent Developments in Global Continuous Bioprocessing Consumables Market?

- In June 2025, Ecolab Life Sciences introduced a new affinity chromatography resin Purolite AP+50 at the BIO International Convention. The resin uses a 50‑micron bead size to combine high dynamic binding capacity with durability, promising more efficient monoclonal antibody capture and improved process economics

- In September 2023, Getinge launched the AppliFlex ST GMP, a single‑use bioreactor designed for mRNA manufacturing and cell/gene therapies, offering cGMP-compliant, scalable, and disposable upstream processing aligning with continuous bioprocessing and flexible manufacturing trends

- In May 2023, 3M announced a major investment to expand its capabilities to support biotech manufacturing a move aimed at boosting supply of single‑use bioprocessing consumables (bags, assemblies, etc.) across Europe. This expansion is expected to support increasing demand from continuous bioprocessing adoption

- In April 2023, Merck KGaA launched a new single‑use process container film Ultimus single-use process container film designed to deliver enhanced strength and leak resistance for single-use assemblies used in bioprocessing. This improves reliability and integrity of disposable consumables in continuous workflows

- In April 2022, Thermo Fisher Scientific inaugurated a new production facility for single‑use technologies in Ogden, Utah (USA), under its multi-year investment plan. The facility aims to support expanded manufacturing of single-use consumables to meet rising demand for continuous bioprocessing and novel biologics

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.