Global Continuous Bioprocessing Market

Market Size in USD Million

USD

174.40 Million

USD

670.83 Million

2024

2032

USD

174.40 Million

USD

670.83 Million

2024

2032

| 2025 - 2032 | |

| USD 174.40 Million | |

| USD 670.83 Million | |

| % | |

|

Continuous Bioprocessing Market Size

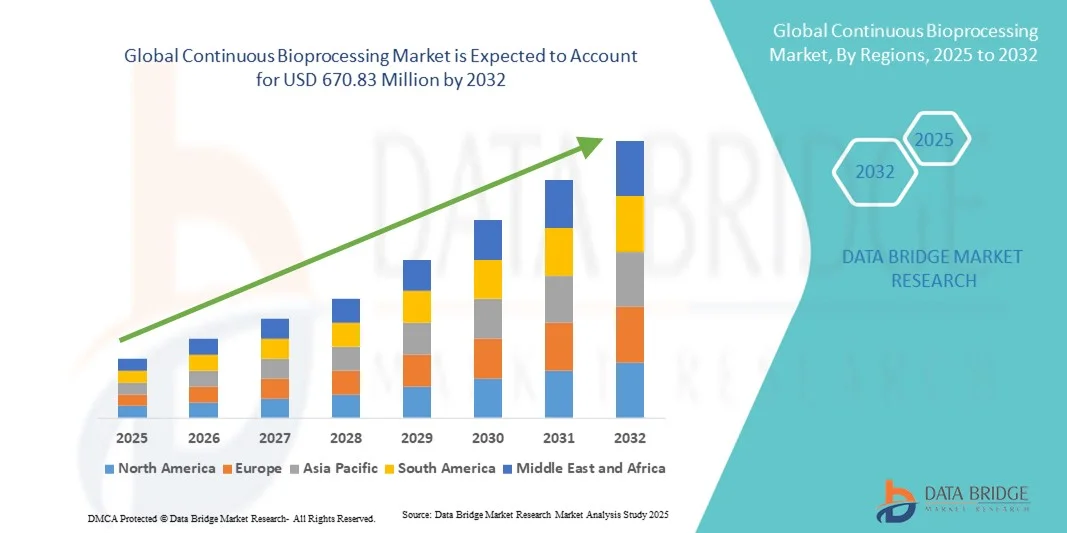

- The global continuous bioprocessing market size was valued at USD 174.40 million in 2024 and is expected to reach USD 670.83 million by 2032, at a CAGR of 18.34% during the forecast period

- The market growth is largely fueled by the increasing demand for biopharmaceuticals, including monoclonal antibodies, vaccines, and cell and gene therapies, driving adoption of more efficient manufacturing processes

- Furthermore, advancements in technologies such as single-use systems, real-time monitoring, and process analytical technology (PAT) are enhancing productivity, reducing operational costs, and improving process control, thereby accelerating the uptake of continuous bioprocessing solutions and significantly boosting the industry's growth

Continuous Bioprocessing Market Analysis

- Continuous bioprocessing, enabling uninterrupted production of biologics through technologies such as perfusion and continuous chromatography, is becoming a critical component of modern biopharmaceutical manufacturing due to its improved efficiency, reduced operational costs, and enhanced process control

- The rising demand for monoclonal antibodies, vaccines, and cell and gene therapies is the primary driver for continuous bioprocessing adoption, alongside the pharmaceutical industry's shift toward more flexible and scalable manufacturing approaches

- North America dominated the continuous bioprocessing market with the largest revenue share of 38.5% in 2024, supported by the presence of leading biopharmaceutical companies, advanced technological infrastructure, and early adoption of single-use and real-time monitoring systems, with the U.S. showing significant uptake in both contract manufacturing organizations (CMOs) and in-house production facilities

- Asia-Pacific is expected to be the fastest-growing region in the continuous bioprocessing market during the forecast period, driven by expanding biopharmaceutical production capacities, increasing healthcare investments, and growing adoption of advanced bioprocessing technologies in emerging markets

- Bioreactors segment dominated the market with a 31.6% share in 2024, owing to their central role in continuous production processes and ability to maintain high cell density cultures efficiently

Report Scope and Continuous Bioprocessing Market Segmentation

|

Attributes |

Continuous Bioprocessing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Continuous Bioprocessing Market Trends

Integration of Automation and Real-Time Monitoring

- A significant and accelerating trend in the global continuous bioprocessing market is the increasing incorporation of automated systems and real-time process monitoring tools, which enhance production efficiency, consistency, and regulatory compliance

- For Instance, advanced single-use bioreactors equipped with sensors can continuously monitor parameters such as pH, temperature, and dissolved oxygen, allowing seamless adjustment of process conditions without manual intervention

- Automation integration enables higher productivity, minimizes human error, and supports continuous quality verification, while real-time monitoring provides immediate insights into process deviations, ensuring consistent biologics quality

- The convergence of automation and data analytics with continuous bioprocessing platforms allows centralized control over multiple production stages, facilitating streamlined operations and scalability across multiple facilities

- This trend towards more intelligent, automated, and data-driven manufacturing is fundamentally transforming biopharmaceutical production, prompting companies such as Sartorius and Pall Corporation to develop integrated continuous bioprocessing systems with advanced process analytical technologies

- The demand for automated, real-time monitored continuous bioprocessing solutions is growing rapidly across both contract manufacturing organizations and in-house production facilities, as biopharma companies seek higher efficiency and regulatory compliance

Continuous Bioprocessing Market Dynamics

Driver

Rising Demand for Biologics and Efficient Manufacturing

- The increasing global demand for monoclonal antibodies, vaccines, and cell and gene therapies is a significant driver for continuous bioprocessing adoption, supporting the need for scalable and efficient manufacturing processes

- For Instance, leading pharmaceutical companies are investing in perfusion and continuous chromatography technologies to meet growing biologics demand while reducing production cycle times

- Continuous bioprocessing provides higher yields, improved product consistency, and lower operational costs compared to traditional batch manufacturing, making it an attractive solution for high-volume biologics production

- Furthermore, the focus on reducing time-to-market for critical therapies and increasing overall process efficiency is encouraging wider adoption of continuous bioprocessing platforms in both developed and emerging markets

- Companies are increasingly integrating continuous bioprocessing into their production pipelines to optimize resource utilization, enhance flexibility, and meet regulatory expectations, driving overall market growth

Restraint/Challenge

High Capital Investment and Regulatory Complexity

- The high initial investment required for continuous bioprocessing systems, along with the complexity of implementing and validating continuous production processes, poses a significant challenge for market expansion

- For Instance, installing fully automated single-use bioreactor systems and advanced PAT tools involves substantial capital expenditure, which can be a barrier for small and mid-sized biopharma companies

- Regulatory compliance and process validation in continuous bioprocessing are more complex than in traditional batch systems, as consistent monitoring and documentation of process parameters are required to meet stringent quality standards

- Furthermore, training personnel to operate continuous systems and integrating them with existing manufacturing infrastructure can be time-consuming and resource-intensive, adding to the adoption challenges

- Overcoming these challenges through modular system designs, scalable solutions, and streamlined regulatory strategies will be crucial for sustained growth in the continuous bioprocessing market

Continuous Bioprocessing Market Scope

The market is segmented on the basis of product, application, and end-user.

- By Product

On the basis of product, the continuous bioprocessing market is segmented into filtration systems and consumables, chromatography systems and consumables, bioreactors, cell culture media and reagents, and others. The bioreactors segment dominated the market with the largest revenue share of 31.5% in 2024, driven by their central role in continuous production processes. Bioreactors enable high cell density cultures and consistent product quality, making them indispensable for monoclonal antibody and vaccine manufacturing. The flexibility of bioreactors to support various production scales and integration with single-use systems further strengthens their adoption. In addition, their compatibility with real-time monitoring and process analytical technology enhances operational efficiency and reduces batch-to-batch variability. Pharmaceutical companies prioritize bioreactors for their reliability, scalability, and contribution to optimized production cycles.

The filtration systems and consumables segment is anticipated to witness the fastest growth rate of 20.8% from 2025 to 2032, fueled by the increasing need for downstream processing efficiency. Filtration systems are critical for separating cells, purifying proteins, and ensuring product sterility. The growing adoption of single-use filtration units reduces cross-contamination risks and enhances operational flexibility. Moreover, the increasing complexity of biologics production, including gene and cell therapies, drives demand for advanced filtration solutions. Companies are investing in innovative filtration consumables to improve recovery rates, reduce waste, and meet stringent regulatory requirements.

- By Application

On the basis of application, the continuous bioprocessing market is segmented into monoclonal antibodies, vaccines, cell and gene therapy, research & development, and other applications. The monoclonal antibodies segment dominated the market with the largest share of 40% in 2024, driven by the high global demand for therapeutic antibodies. Continuous bioprocessing provides enhanced yield, quality consistency, and reduced manufacturing costs for monoclonal antibodies, making it highly attractive for pharmaceutical companies. The scalability and efficiency of continuous platforms allow manufacturers to meet growing clinical and commercial demands. Integration with process analytical technology ensures compliance with regulatory standards and maintains product integrity. The increasing pipeline of monoclonal antibody therapies across various therapeutic areas further propels this segment’s growth.

The cell and gene therapy segment is expected to witness the fastest CAGR from 2025 to 2032 due to the emerging need for personalized medicines. Continuous bioprocessing enables precise control over complex cell cultures, essential for gene and cell therapy production. Rapid advancements in cell engineering, viral vector production, and high-value biologics are driving adoption of continuous manufacturing in this segment. Companies are leveraging automated and single-use continuous systems to reduce production time and cost while ensuring consistent quality. In addition, regulatory emphasis on scalable and reproducible manufacturing solutions supports the accelerated uptake of continuous bioprocessing in this field.

- By End-User

On the basis of end-user, the continuous bioprocessing market is segmented into pharmaceuticals and biotechnology companies, contract development and manufacturing organizations (CDMOs), and academics and research institutes. The pharmaceuticals and biotechnology companies segment dominated the market in 2024, driven by large-scale biologics production needs. These companies prioritize continuous bioprocessing for its efficiency, cost-effectiveness, and ability to meet high-volume demand for monoclonal antibodies and vaccines. Continuous platforms allow seamless integration with existing manufacturing facilities and support regulatory compliance. Advanced bioprocessing systems enable real-time monitoring and automation, enhancing productivity and reducing human intervention. Strategic investments in continuous manufacturing infrastructure by leading pharma companies further strengthen this segment’s dominance.

The contract development and manufacturing organizations (CDMOs) segment is expected to witness the fastest growth during the forecast period, owing to rising outsourcing of biologics production. CDMOs are adopting continuous bioprocessing to provide flexible, scalable, and cost-efficient manufacturing solutions for multiple clients. Increasing demand from small and mid-sized biotech firms that lack in-house production capabilities drives this adoption. The ability to offer faster turnaround times, higher productivity, and regulatory-compliant processes positions CDMOs to benefit significantly from this market trend.

Continuous Bioprocessing Market Regional Analysis

- North America dominated the continuous bioprocessing market with the largest revenue share of 38.5% in 2024, supported by the presence of leading biopharmaceutical companies, advanced technological infrastructure, and early adoption of single-use and real-time monitoring systems

- Pharmaceutical and biotechnology firms in the region prioritize efficiency, scalability, and regulatory compliance, making continuous bioprocessing an attractive solution for high-volume biologics production, including monoclonal antibodies and vaccines

- This widespread adoption is further supported by strong R&D capabilities, high healthcare investments, and increasing integration of single-use systems and process analytical technology (PAT), establishing continuous bioprocessing as a preferred manufacturing approach for both in-house production and contract development organizations

U.S. Continuous Bioprocessing Market Insight

The U.S. continuous bioprocessing market captured the largest revenue share of 42% in 2024 within North America, fueled by the rapid adoption of advanced biologics manufacturing technologies and the growing demand for monoclonal antibodies and vaccines. Companies are increasingly implementing single-use bioreactors, continuous chromatography, and real-time process monitoring to improve efficiency and reduce production costs. The focus on shortening time-to-market for critical therapies, coupled with strong R&D infrastructure and regulatory support, further propels the market. Moreover, contract development and manufacturing organizations (CDMOs) are expanding continuous processing capabilities, strengthening the overall industry growth.

Europe Continuous Bioprocessing Market Insight

The Europe continuous bioprocessing market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent regulatory requirements and the need for high-quality biologics production. Increasing urbanization, growing investments in pharmaceutical R&D, and the demand for efficient, scalable manufacturing solutions are fostering market adoption. European manufacturers are adopting continuous bioprocessing for monoclonal antibodies, vaccines, and cell and gene therapies, with a focus on reducing operational costs and maintaining consistent product quality.

U.K. Continuous Bioprocessing Market Insight

The U.K. continuous bioprocessing market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by investments in biologics R&D and the rising trend of outsourcing production to CDMOs. The country’s strong pharmaceutical and biotechnology sector, coupled with government support for innovation, is encouraging the adoption of continuous bioprocessing platforms. In addition, the need to meet stringent quality and regulatory standards is motivating companies to implement advanced continuous manufacturing technologies for improved efficiency and reliability.

Germany Continuous Bioprocessing Market Insight

The Germany continuous bioprocessing market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s focus on pharmaceutical innovation and high-quality manufacturing. Germany’s well-developed infrastructure, emphasis on research and development, and growing biopharmaceutical production capabilities promote the adoption of continuous bioprocessing systems. Integration with real-time monitoring and automation solutions is also becoming increasingly prevalent, with a strong preference for scalable, efficient, and regulatory-compliant manufacturing processes.

Asia-Pacific Continuous Bioprocessing Market Insight

The Asia-Pacific continuous bioprocessing market is poised to grow at the fastest CAGR of 23% during the forecast period of 2025 to 2032, driven by increasing investments in biopharmaceutical manufacturing, rising demand for monoclonal antibodies and vaccines, and technological advancements in countries such as China, Japan, and India. The region’s focus on capacity expansion, government initiatives supporting biotech innovation, and growing adoption of single-use and automated systems are driving market growth. Furthermore, Asia-Pacific is emerging as a hub for biologics manufacturing, improving accessibility and reducing costs for continuous bioprocessing solutions.

Japan Continuous Bioprocessing Market Insight

The Japan continuous bioprocessing market is gaining momentum due to the country’s advanced pharmaceutical sector, strong R&D capabilities, and demand for high-quality biologics. Adoption of continuous manufacturing platforms is driven by the need for efficiency, regulatory compliance, and consistent product quality. Integration with process analytical technology (PAT) and automation systems enhances productivity and reduces production cycle times. Moreover, Japan’s focus on innovative therapies, including cell and gene therapy, is further fueling the market’s growth.

India Continuous Bioprocessing Market Insight

The India continuous bioprocessing market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to the country’s expanding biopharmaceutical industry, growing healthcare investments, and rapid adoption of advanced manufacturing technologies. India is becoming a key market for biologics production, including monoclonal antibodies and vaccines, with increasing implementation of continuous bioprocessing in pharmaceutical and biotechnology companies. The push towards establishing biotech hubs, coupled with the availability of cost-effective solutions, is driving strong market growth.

Continuous Bioprocessing Market Share

The Continuous Bioprocessing industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- Sartorius AG (Germany)

- WuXi Biologics (China)

- GE Healthcare (U.S.)

- Repligen Corporation (U.S.)

- Lonza Group (Switzerland)

- Asahi Kasei Life Science Corporation (U.S.)

- Ginkgo Bioworks (U.S.)

- Danaher (U.S.)

- Eppendorf AG (Germany)

- Cytiva Life Sciences (U.S.)

- 3M U.S.)

- BIOVECTRA (Canada)

- BASF SE (Germany)

- Samsung Biologics (South Korea)

- Boehringer Ingelheim (Germany)

- Bayer AG (Germany)

- AbbVie Inc. (U.S.)

- FUJIFILM Biotechnologies. (Japan)

- CELLTRION INC. (South Korea)

What are the Recent Developments in Global Continuous Bioprocessing Market?

- In September 2025, Thermo Fisher Scientific announced the completion of its acquisition of Solventum's Purification & Filtration business for approximately USD 4.0 billion in cash. This strategic move is intended to strengthen Thermo Fisher's bioproduction portfolio, particularly its filtration offerings, to better serve the needs of its biopharma and biotech customers in the rapidly growing continuous bioprocessing market

- In May 2025, RoosterBio and Thermo Fisher Scientific announced a collaboration to advance cell and exosome therapy manufacturing. This partnership focuses on combining RoosterBio's expertise in human mesenchymal stem/stromal cells (hMSCs) and exosome technologies with Thermo Fisher's bioprocessing solutions. The collaboration aims to address challenges in manufacturing advanced biologics and cell and gene therapies, a key area of growth in the bioprocessing market

- In April 2025, Culture Biosciences unveiled Stratyx 250, a mobile, cloud-integrated bioreactor system for cell culture process development. The new system is designed to accelerate bioprocess development, reduce costs, and provide real-time remote control and monitoring. This development reflects a growing trend towards the integration of digital technologies and automation in bioprocessing to enable faster, more flexible, and more efficient development cycles

- In June 2023, Waters and Sartorius expanded their collaboration to deliver integrated analytical tools for downstream biomanufacturing. This partnership combines Sartorius' multi-column chromatography systems with Waters' process analytical technology, enabling bioprocess scientists to obtain vital analytical data more rapidly, thereby reducing production time and costs

- In May 2023, Tosoh Bioscience joined an enGenes-led consortium to advance continuous E. coli manufacturing. This collaboration focuses on developing a small-scale development platform to implement model predictive control and enhance continuous bioprocesses, aiming to improve efficiency and scalability in biomanufacturing

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.