Global Continuous Integration Ci Tools Market

Market Size in USD Billion

USD

2.33 Billion

USD

8.09 Billion

2025

2033

USD

2.33 Billion

USD

8.09 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.33 Billion | |

| USD 8.09 Billion | |

| % | |

|

What is the Global Continuous Integration (CI) Tools Market Size and Growth Rate?

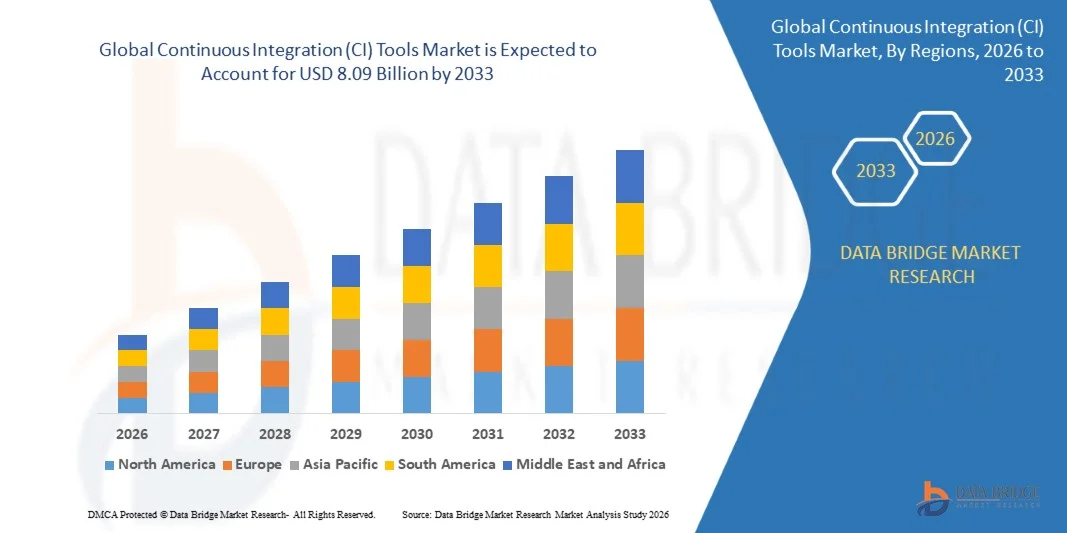

- The global continuous integration (CI) tools market size was valued at USD 2.33 billion in 2025 and is expected to reach USD 8.09 billion by 2033, at a CAGR of 16.80% during the forecast period

- The continuous integration (CI) tools market is being driven by the rising demand of automation in the advancement process of software. The upsurge in the demand for continuous integration (CI) tools among all industry verticals is a major factor driving the market's growth. The increase in the productivity along with the help of continuous integration (CI) tools is driving up demand for continuous integration (CI) tools market

What are the Major Takeaways of Continuous Integration (CI) Tools Market?

- High demand for advanced data integration as well as management tools and the significant shift towards the technologies such as machine learning and artificial intelligence will influence the continuous integration (CI) tools market for the forecast period mentioned above

- Moreover, increase in the adoption rate of cloud computing solutions and growing demand of automated tools amongst enterprises will boost the beneficial opportunities for the continuous integration (CI) tools market growth

- North America dominated the continuous integration (CI) tools market with a 41.95% revenue share in 2025, driven by strong adoption of DevOps practices, rapid cloud migration, enterprise software modernization, and increasing demand for automated software delivery pipelines across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 10.72% from 2026 to 2033, driven by rapid expansion of software development hubs, rising cloud adoption, and growing digital transformation across China, India, Japan, South Korea, and Southeast Asia

- The Cloud segment dominated the market with a 61.4% share in 2025, as it remains the preferred deployment model for enterprises seeking scalability, remote accessibility, faster implementation, and lower infrastructure costs

Report Scope and Continuous Integration (CI) Tools Market Segmentation

|

Attributes |

Continuous Integration (CI) Tools Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Continuous Integration (CI) Tools Market?

“Increasing Shift Toward Cloud-Native, AI-Enabled, and DevOps-Integrated CI Platforms”

- The continuous integration (CI) tools market is witnessing strong adoption of cloud-based, scalable, and automation-driven platforms designed to support faster software builds, testing, and deployment across agile development environments

- Vendors are introducing AI-enabled pipeline optimization, automated testing frameworks, and DevSecOps integrations that enhance deployment speed, code quality, and release efficiency

- Growing demand for continuous software delivery, microservices architecture, and containerized applications is driving usage across enterprises, SaaS providers, and digital-native organizations

- For instance, companies such as Microsoft, Atlassian, CloudBees, AWS, and GitHub are expanding CI capabilities with advanced orchestration, real-time monitoring, and cloud-native integrations

- Increasing need for rapid release cycles, collaboration across distributed teams, and automated quality assurance is accelerating the shift toward integrated CI platforms

- As software ecosystems become more agile and complex, CI tools will remain vital for faster releases, automated testing, and continuous product innovation

What are the Key Drivers of Continuous Integration (CI) Tools Market?

- Rising demand for faster software development cycles and automated code validation is a major growth driver across enterprises and startups

- For instance, in 2025–2026, leading vendors expanded their platforms with AI-assisted debugging, test automation, and pipeline analytics capabilities

- Growing adoption of DevOps, Agile, Kubernetes, cloud computing, and remote engineering teams is boosting demand across the U.S., Europe, and Asia-Pacific

- Advancements in CI/CD orchestration, API integrations, container support, and cloud-native deployment workflows have strengthened platform performance and scalability

- Rising use of AI applications, enterprise SaaS products, fintech platforms, and mobile applications is creating strong demand for robust CI tools

- Supported by steady investments in digital transformation, enterprise software, and cloud infrastructure, the CI tools market is expected to witness strong long-term growth

Which Factor is Challenging the Growth of the Continuous Integration (CI) Tools Market?

- High costs associated with enterprise-grade CI platforms, premium integrations, and large-scale cloud deployments restrict adoption among SMEs and early-stage startups

- For instance, during 2024–2025, rising cloud infrastructure expenses and software licensing costs increased deployment budgets for several organizations

- Complexity in managing multi-cloud pipelines, legacy system integration, and security compliance workflows increases the need for skilled DevOps professionals and training

- Limited awareness in emerging markets regarding CI/CD best practices and automation maturity slows adoption

- Competition from open-source alternatives, integrated DevOps suites, and in-house deployment frameworks creates pricing pressure and reduces product differentiation

- To address these issues, companies are focusing on cost-optimized subscriptions, AI-driven automation, and simplified integrations to increase global adoption of Continuous Integration (CI) Tools

How is the Continuous Integration (CI) Tools Market Segmented?

The market is segmented on the basis of deployment mode, organization size, and vertical.

• By Deployment Mode

On the basis of deployment mode, the Continuous Integration (CI) Tools market is segmented into On-Premises and Cloud. The Cloud segment dominated the market with a 61.4% share in 2025, as it remains the preferred deployment model for enterprises seeking scalability, remote accessibility, faster implementation, and lower infrastructure costs. Cloud-based CI tools are widely adopted for automated build pipelines, code testing, version control integration, and DevOps collaboration across distributed teams. Their ability to support real-time updates, seamless third-party integrations, and faster software release cycles continues to drive strong adoption across startups and large enterprises. Increasing use of SaaS-based development environments and growing demand for agile software delivery further strengthen segment dominance.

The On-Premises segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by rising demand from highly regulated industries such as BFSI, healthcare, and government, where data control, security compliance, and customized infrastructure remain critical.

• By Organization Size

On the basis of organization size, the market is segmented into Small and Medium Enterprises and Large Enterprises. The Large Enterprises segment dominated the market with a 57.8% share in 2025, supported by extensive software development operations, higher DevOps budgets, and strong demand for enterprise-grade automation pipelines. Large organizations increasingly deploy CI tools to streamline code integration, automate testing, improve release quality, and reduce deployment downtime across multiple teams and business units. Integration with enterprise tools such as container orchestration, security testing, and performance monitoring platforms further supports adoption.

The Small and Medium Enterprises segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing digital transformation, rising SaaS adoption, and growing awareness of DevOps practices among startups and mid-sized companies.

• By Vertical

On the basis of vertical, the continuous integration (CI) Tools market is segmented into Banking, Financial Services and Insurance, Retail and E-Commerce, Telecommunication, Education, Media and Entertainment, Healthcare, Manufacturing, and Others. The IT & Telecommunication segment dominated the market with a 34.6% share in 2025, driven by continuous software releases, cloud-native application development, and high demand for agile DevOps workflows. Telecom providers and software companies extensively utilize CI tools for faster application updates, network software testing, and service reliability enhancement.

The Banking, Financial Services and Insurance segment is expected to grow at the fastest CAGR from 2026 to 2033, propelled by increasing digitization of financial services, rapid app deployment needs, and strong focus on secure, automated software delivery pipelines.

Which Region Holds the Largest Share of the Continuous Integration (CI) Tools Market?

- North America dominated the continuous integration (CI) tools market with a 41.95% revenue share in 2025, driven by strong adoption of DevOps practices, rapid cloud migration, enterprise software modernization, and increasing demand for automated software delivery pipelines across the U.S. and Canada. High penetration of cloud-native application development, microservices architecture, containerization, and agile workflows continues to fuel demand for CI tools across software enterprises, BFSI institutions, telecom providers, healthcare IT systems, and large digital platforms.

- Leading companies in North America are introducing advanced CI/CD platforms with AI-powered code testing, automated deployment workflows, container orchestration integration, and real-time monitoring capabilities, strengthening the region’s technological leadership. Continuous investment in software engineering innovation, cybersecurity, and digital transformation drives long-term market expansion.

- High concentration of technology talent, mature startup ecosystems, and sustained enterprise IT investments further reinforce regional market leadership

U.S. Continuous Integration (CI) Tools Market Insight

The U.S. is the largest contributor in North America, supported by the presence of major cloud service providers, software development firms, and enterprise technology companies. Increasing adoption of DevOps pipelines, Git-based workflows, automated testing frameworks, and release automation platforms intensifies demand for advanced CI tools across BFSI, SaaS, healthcare, retail, and telecom sectors. Strong demand for faster product releases, reduced deployment errors, and enhanced collaboration between development and operations teams continues to accelerate market growth.

Canada Continuous Integration (CI) Tools Market Insight

Canada contributes significantly to regional growth, driven by rising investments in digital infrastructure, growing SaaS startups, and increasing enterprise cloud adoption. Organizations are increasingly utilizing CI tools for automated builds, code validation, and deployment efficiency. Government-backed innovation initiatives and strong software talent availability continue to strengthen adoption across the country.

Asia-Pacific Continuous Integration (CI) Tools Market

Asia-Pacific is projected to register the fastest CAGR of 10.72% from 2026 to 2033, driven by rapid expansion of software development hubs, rising cloud adoption, and growing digital transformation across China, India, Japan, South Korea, and Southeast Asia. Increasing demand for faster application deployment, mobile app development, and enterprise automation continues to accelerate CI tool adoption across startups and large enterprises.

China Continuous Integration (CI) Tools Market Insight

China is the largest contributor to Asia-Pacific due to strong growth in enterprise IT, cloud infrastructure, and large-scale software development ecosystems. Rapid digitalization across finance, retail, telecom, and manufacturing drives strong demand for CI platforms.

Japan Continuous Integration (CI) Tools Market Insight

Japan shows steady growth supported by enterprise software modernization, strong telecom infrastructure, and increasing automation across corporate IT systems.

India Continuous Integration (CI) Tools Market Insight

India is emerging as a major growth hub, driven by expanding IT services, startup ecosystems, SaaS companies, and rising DevOps adoption.

South Korea Continuous Integration (CI) Tools Market Insight

South Korea contributes significantly due to rapid digital transformation, advanced telecom infrastructure, and strong enterprise software innovation.

Which are the Top Companies in Continuous Integration (CI) Tools Market?

The continuous integration (CI) tools industry is primarily led by well-established companies, including:

- Broadcom Inc. (U.S.)

- Amazon Web Services, Inc. (U.S.)

- Microsoft Corporation (U.S.)

- IBM (U.S.)

- Oracle Corporation (U.S.)

- CloudBees, Inc. (U.S.)

- Red Hat, Inc. (U.S.)

- Circle Internet Services, Inc. (CircleCI) (U.S.)

- JetBrains s.r.o. (Czech Republic)

- Buildkite Pty Ltd. (Australia)

- TRAVIS CI GmbH (Germany)

- Bitrise Limited (Hungary)

- Nevercode Ltd. (U.K.)

- SmartBear Software (U.S.)

- Atlassian (Australia)

- Micro Focus (U.K.)

- Puppet (U.S.)

- VSoft Technologies Pvt. Ltd. (India)

- JFrog Ltd. (Israel)

- AutoRABIT (U.S.)

- AppVeyor Systems Inc. (Canada)

- Harness Inc. (U.S.)

- Rendered Text (Serbia)

What are the Recent Developments in Global Continuous Integration (CI) Tools Market?

- In January 2026, CloudBees introduced a unified multi-platform DevOps management solution designed to streamline enterprise toolchains by enabling centralized governance across platforms such as GitHub, GitLab, and Jenkins through a single SaaS-based control plane, thereby strengthening workflow visibility, governance efficiency, and enterprise-scale CI/CD orchestration capabilities

- In December 2025, JetBrains upgraded TeamCity with native Docker integration and advanced pipeline visualization features, making CI/CD setup easier for SMEs through drag-and-drop editors and built-in container support, thereby improving deployment efficiency, usability, and adoption among mid-sized development teams

- In November 2025, GitHub Actions rolled out significant architectural enhancements, including YAML anchors, private workflow templates, deeper reusable workflow capabilities, and expanded cache capacities, thereby increasing flexibility, performance, and scalability for large-scale CI/CD environments

- In March 2024, JetBrains launched TeamCity Pipelines, which was later integrated into its enterprise edition to simplify CI/CD pipeline management with a more intuitive interface and improved scalability for larger teams, thereby supporting better collaboration, faster releases, and stronger enterprise DevOps workflows

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.