Global Control Unit In Vehicle Infotainment Market

Market Size in USD Billion

USD

24.25 Billion

USD

50.48 Billion

2025

2033

USD

24.25 Billion

USD

50.48 Billion

2025

2033

| 2026 - 2033 | |

| USD 24.25 Billion | |

| USD 50.48 Billion | |

| % | |

|

Control Unit in Vehicle Infotainment Market Overview

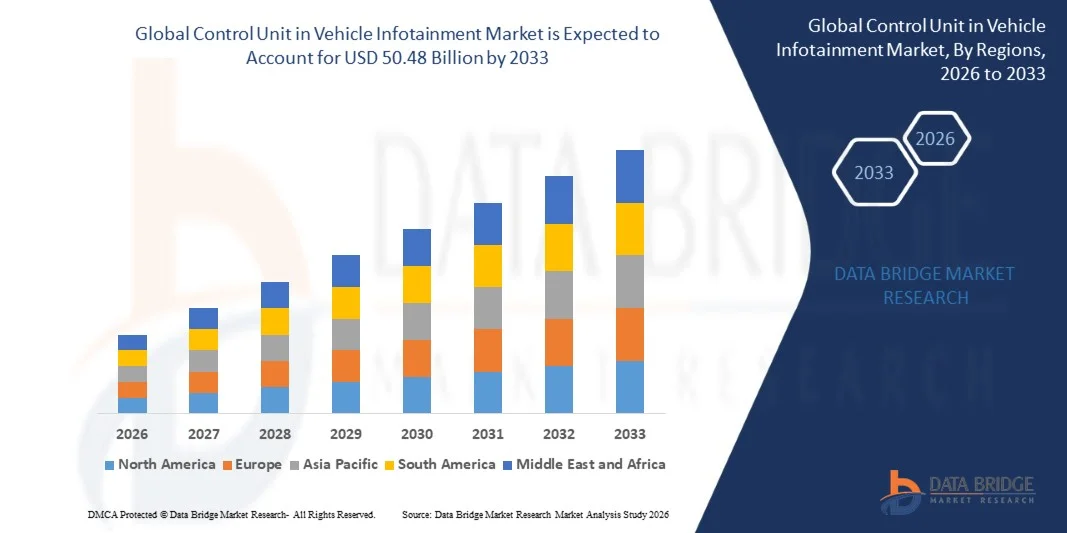

As per Data Bridge Market Research analysis The control unit in vehicle infotainment market was valued at USD 24.25 billion in 2025 and is projected to reach USD 50.48 billion by 2033, growing at a CAGR of 9.60% from 2026 to 2033. The market is witnessing steady expansion driven by the rapid integration of advanced infotainment systems, increasing consumer demand for connected in-vehicle experiences, and the growing adoption of smart cockpit architectures across passenger and commercial vehicles.

The increasing penetration of electric and autonomous vehicles, along with rising demand for seamless connectivity, voice-enabled controls, and real-time navigation systems, is significantly accelerating the adoption of advanced infotainment control units. Automakers are increasingly embedding high-performance domain controllers to unify audio, video, navigation, and connectivity functions, replacing traditional distributed electronic control systems with centralized computing platforms that enhance user experience, system efficiency, and software upgradability.

Key Market Trends & Insights

- North America dominated the control unit in vehicle infotainment market with the largest revenue share of 32.35% in 2025, supported by high penetration of connected vehicles, strong presence of leading automotive OEMs, and rapid adoption of advanced digital cockpit and infotainment systems.

- The Embedded segment led the market with a 46% share in 2025, driven by the strong OEM integration, high system reliability, and its ability to manage multiple infotainment and connectivity functions within a unified hardware-software architecture

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 10.1% from 2026 to 2033, fueled by rising vehicle production, accelerating EV adoption, and increasing demand for smart, connected infotainment systems across China, India, Japan, and South Korea.

- Integrated are the fastest-growing form type, projected to register a CAGR of 10.1%, reflecting the surge in shift toward centralized domain controllers in software-defined vehicles.

- The OE Fitted segment dominated the fit type category with a 72% revenue share in 2025, led by strong OEM preference for factory-installed infotainment control units that ensure seamless integration and compliance with automotive safety standards.

- Front Row accounted for 78% of the market, preferred by drivers and OEMs as the primary human–machine interface for infotainment, navigation, and vehicle control functions.

- The 5G segment is the fastest-growing connectivity category, with a CAGR of 12.4%, driven by ultra-low latency, high bandwidth, and enhanced V2X communication capabilities.

Market Size & Forecast

- Global Market Value (2025): USD 24.25 Billion

- Expected Market Value (2033): USD 50.48 Billion

- Forecast CAGR (2026–2033): 9.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Control Unit in Vehicle Infotainment Market Segmentation

|

Attributes |

Control Unit in Vehicle Infotainment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Robert Bosch GmbH (Germany) · Continental AG (Germany) · DENSO CORPORATION (Japan) · Visteon Corporation (U.S.) · HARMAN International (U.S.) · Panasonic Automotive Systems Co., Ltd. (Japan) · Aptiv PLC (Ireland) · Marelli Holdings Co., Ltd. (Japan) · Hyundai Mobis Co., Ltd. (South Korea) · Alpine Electronics, Inc. (Japan) · Pioneer Corporation (Japan) · JVCKENWOOD Corporation (Japan) · Mitsubishi Electric Corporation (Japan) · Garmin Ltd. (Switzerland) · Qualcomm Technologies, Inc. (U.S.) · NVIDIA Corporation (U.S.) · LG Electronics Inc. (South Korea) · Sony Group Corporation (Japan) · FORVIA (France) · TomTom International BV (Netherlands) |

|

Market Opportunities |

· Rapid shift toward centralized vehicle E/E architecture · Growing adoption of software-defined vehicles · Increasing penetration of EVs and connected cars |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Control Unit in Vehicle Infotainment Market Trends

Trend: Expansion of Software-Defined Digital Cockpit Platforms

Automotive manufacturers are rapidly transitioning from hardware-centric infotainment systems to software-defined digital cockpits, where multiple in-vehicle functions are managed through centralized control units. This shift enables seamless integration of infotainment, navigation, ADAS alerts, voice assistants, and vehicle settings into a unified interface controlled by domain controllers. The use of high-performance SoCs (System-on-Chip), GPU acceleration, and cloud connectivity allows real-time processing of data from multiple vehicle sensors and displays. It also supports over-the-air (OTA) updates, enabling continuous feature upgrades without hardware replacement, significantly improving lifecycle value and user personalization.

For instance, systems such as BMW iDrive 8/9 and Mercedes-Benz MBUX Hyperscreen demonstrate how modern infotainment control units unify multiple displays, AI-based voice interaction, and cloud services into a single intelligent cockpit ecosystem, setting new standards for premium and mid-range vehicles.

Control Unit in Vehicle Infotainment Market Dynamics

Key Market Driver: Rising Demand for Connected and Smart Vehicles

The accelerating demand for connected cars and intelligent mobility solutions is a primary driver of the control unit in vehicle infotainment market. Consumers increasingly expect real-time navigation, streaming services, smartphone mirroring, predictive maintenance alerts, and voice-controlled systems as standard features. This is pushing OEMs to deploy advanced infotainment control units capable of handling high data bandwidth, multi-device connectivity, and cloud-based services within vehicles. In addition, the rise of electric vehicles (EVs) and autonomous driving technologies is reinforcing the need for centralized control architectures. These systems allow integration of infotainment with ADAS, battery management interfaces, and telematics, improving efficiency and driving experience.

For instance, Tesla’s infotainment and vehicle control ecosystem integrates navigation, entertainment, diagnostics, and vehicle performance controls into a single continuously updated platform, demonstrating how connected vehicle demand is shaping next-generation control unit development.

Key Restraint/Challenge: High System Complexity and Development Costs

One of the major challenges in this market is the increasing complexity of designing and integrating centralized infotainment control units that must manage multiple high-performance functions simultaneously. These systems require advanced semiconductor chips, powerful processors, and sophisticated software architectures capable of ensuring real-time responsiveness, safety, and reliability across diverse vehicle environments. Development costs are further increased by cybersecurity requirements, functional safety compliance (ISO 26262), and long validation cycles, especially for global vehicle platforms that must operate across different regulatory environments. In addition, ensuring compatibility between infotainment systems, ADAS modules, and vehicle operating systems adds further engineering burden for OEMs and Tier-1 suppliers.

For instance, premium EV platforms such as Lucid Air’s advanced digital cockpit architecture highlight the significant investment required to build high-resolution multi-display systems integrated with centralized domain controllers, reflecting both technological sophistication and high development cost barriers.

Key Market Opportunity: Growth of Software-Defined Vehicles and AI-Driven Infotainment Ecosystems

The transition toward software-defined vehicles (SDVs) presents a major growth opportunity for the control unit in vehicle infotainment market, as automakers increasingly decouple hardware from software to enable continuous innovation. This shift allows infotainment control units to evolve into centralized computing hubs capable of managing entertainment, navigation, vehicle diagnostics, connectivity, and driver assistance functions through upgradable software platforms. It also enables new revenue models such as subscription-based features, in-car app ecosystems, and pay-per-use services, significantly increasing long-term monetization potential for OEMs and suppliers. At the same time, the integration of artificial intelligence (AI) and edge computing is enhancing infotainment systems with predictive personalization, natural voice interaction, and context-aware services that adapt to driver behavior and road conditions.

For instance, platforms such as Android Automotive OS-based infotainment systems in Volvo and Polestar vehicles illustrate how AI-enabled, software-driven ecosystems can transform traditional control units into continuously evolving digital platforms, opening scalable opportunities across both premium and mass-market vehicle segments.

Control Unit in Vehicle Infotainment Market Scope

The control unit in vehicle infotainment market is segmented on the basis of form, fit type, location, connectivity, operating system, service, alternate fuel vehicle, vehicle type, and installation.

- By Form

On the basis of form, the market is segmented into embedded, tethered, and integrated systems. The Embedded segment dominated the market with a 46% share in 2025, owing to strong OEM integration, high system reliability, and its ability to manage multiple infotainment and connectivity functions within a unified hardware-software architecture. Embedded control units are widely deployed in modern digital cockpits due to their stable performance and low latency response. They support advanced features such as real-time navigation, voice assistance, and multimedia processing. Their compatibility with vehicle ECUs makes them highly scalable across vehicle segments. Increasing adoption of OTA updates further enhances their lifecycle value. However, their architecture is gradually evolving toward more centralized computing platforms.

The Integrated segment is expected to be the fastest growing at 10.1% CAGR from 2026 to 2033, driven by the shift toward centralized domain controllers in software-defined vehicles. Integrated systems combine infotainment, connectivity, ADAS, and vehicle control functions into a single high-performance computing unit. This reduces wiring complexity, improves efficiency, and lowers overall system cost. Rising penetration of EVs and autonomous vehicles is accelerating adoption. These systems also enable seamless multi-display synchronization and cloud-based services. Continuous advancements in automotive processors and chipsets are strengthening their growth trajectory. Advancements in high-performance automotive processors are accelerating adoption across OEMs.

- By Fit Type

On the basis of fit type, the market is segmented into OE fitted and aftermarket systems. The OE Fitted segment dominated the market with 72% share in 2025, driven by strong OEM preference for factory-installed infotainment control units that ensure seamless integration and compliance with automotive safety standards. OE fitted systems offer better cybersecurity, reliability, and performance optimization compared to aftermarket solutions. They are increasingly embedded in EVs and premium vehicles with advanced digital cockpit features. Growing demand for connected vehicle ecosystems further supports dominance. OEM integration also enables OTA updates and long-term software upgrades. Standardization across global platforms reinforces this segment’s leadership.

The Aftermarket segment is expected to be the fastest growing at 9.0% CAGR from 2026 to 2033, driven by rising consumer demand for infotainment upgrades in existing vehicle fleets. Users are increasingly adopting retrofit solutions offering navigation, multimedia, and smartphone connectivity features. Declining hardware costs and plug-and-play installation systems are supporting expansion. Growth in used vehicle markets, especially in emerging economies, is significantly boosting demand. Consumers are prioritizing connected mobility even in older vehicles. Technological miniaturization and wireless integration are further accelerating adoption. Rising consumer demand for digital features in legacy vehicles is boosting growth.

- By Location

On the basis of location, the market is segmented into front row and rear row systems. The Front Row segment dominated the market with 78% share in 2025, as it serves as the primary interface for driver-centric infotainment and vehicle control functions. Front row systems are deeply integrated with digital dashboards, central displays, and instrument clusters. They support navigation, entertainment, and vehicle settings in real time. Increasing adoption of large touchscreen cockpits is reinforcing dominance. OEMs prioritize front row systems for enhanced user experience and safety integration. Continuous evolution of human-machine interface technologies further strengthens this segment.

The Rear Row segment is expected to be the fastest growing at 8.9% CAGR from 2026 to 2033, driven by rising demand for in-cabin entertainment in premium, autonomous, and ride-sharing vehicles. Rear infotainment systems offer personalized multimedia, streaming, and connectivity services for passengers. Growth in luxury vehicle sales and shared mobility platforms is boosting adoption. OEMs are increasingly offering independent rear control units for enhanced passenger experience. Rising focus on comfort and digital experiences in vehicles is accelerating demand. Expansion of autonomous mobility will further support long-term growth. Focus on in-cabin comfort and digital experience is strengthening growth.

- By Connectivity

On the basis of connectivity, the market is segmented into 3G, 4G, 5G, Bluetooth, and Wi-Fi. The 4G segment dominated the market with 52% share in 2025, due to its widespread global infrastructure, cost efficiency, and stable connectivity performance. It supports essential infotainment functions such as navigation, streaming, and telematics services. OEMs continue to deploy 4G in mid-range and mass-market vehicles. Its reliability and affordability make it the current standard for connected infotainment systems. It also supports OTA updates and cloud connectivity. However, its dominance is gradually shifting toward next-generation networks.

The 5G segment is expected to be the fastest growing at 12.4% CAGR from 2026 to 2033, driven by ultra-low latency, high bandwidth, and enhanced V2X communication capabilities. 5G enables advanced infotainment applications such as cloud gaming, real-time HD streaming, and AI-powered navigation. It is also critical for autonomous driving and connected vehicle ecosystems. OEMs are increasingly integrating 5G-ready control units into next-generation vehicles. Government investments in smart mobility infrastructure are further accelerating adoption. It is becoming a foundational technology for software-defined vehicles. Smart mobility infrastructure development is accelerating adoption globally.

- By Operating System

On the basis of operating system, the market is segmented into Linux, QNX, Microsoft, and OS-others. The Linux segment dominated the market with 48% share in 2025, driven by its open-source flexibility, scalability, and strong developer ecosystem. Linux supports high customization across infotainment platforms and integrates seamlessly with Android Automotive OS. OEMs prefer it for both premium and mass-market vehicles. Its cost efficiency and adaptability make it highly attractive. Continuous innovation from the open-source community strengthens its dominance. It remains the backbone of modern infotainment architectures.

The QNX segment is expected to be the fastest growing at 11.2% CAGR from 2026 to 2033, due to its real-time processing capabilities and strong functional safety compliance. QNX is widely used in premium and safety-critical infotainment systems. It ensures high reliability in complex automotive environments. Increasing demand for multi-display digital cockpits is driving adoption. OEMs prefer it for EV and luxury vehicle platforms. Its robustness and certification standards support strong long-term growth. Its reliability makes it suitable for advanced vehicle computing systems.

- By Service

On the basis of service, the market is segmented into entertainment services, navigation services, e-call, vehicle diagnostics, and others. The Entertainment Services segment dominated the market with 38% share in 2025, driven by strong consumer demand for in-car media streaming, gaming, and personalized content experiences. Integration with smartphones and cloud platforms enhances usability. OEMs are embedding rich infotainment ecosystems into vehicles. Rising connected mobility trends are reinforcing adoption. It remains the primary revenue-generating service segment. Continuous innovation in digital content is strengthening growth.

The Vehicle Diagnostics segment is expected to be the fastest growing at 10.1% CAGR from 2026 to 2033, driven by predictive maintenance and real-time vehicle health monitoring. Integration with telematics systems enables early fault detection. Fleet operators increasingly rely on diagnostics for operational efficiency. AI-based analytics enhance predictive accuracy and system intelligence. Growth in connected vehicles is accelerating adoption. It is becoming a key enabler of smart mobility services. It remains the most revenue-generating service category.

- By Alternate Fuel Vehicle

On the basis of alternate fuel vehicle, the market is segmented into BEV, HEV, and PHEV. The BEV segment dominated the market with 44% share in 2025, driven by rapid EV adoption and strong integration of advanced infotainment systems in electric vehicle platforms. BEVs rely heavily on centralized control units for energy management and digital cockpit functionality. OEMs position infotainment as a key differentiator in EVs. Government incentives and emission regulations further support dominance. Increasing EV production globally strengthens this segment. It is closely aligned with next-generation vehicle architecture.

The PHEV segment is expected to be the fastest growing at 10.2% CAGR from 2026 to 2033, driven by transitional adoption between ICE and fully electric vehicles. PHEVs require advanced infotainment systems for managing dual powertrain operations. Consumers prefer flexibility and extended driving range. Expanding charging infrastructure supports adoption. OEMs are enhancing hybrid system interfaces for better user experience. Regulatory pressure toward electrification is further boosting growth.

- By Vehicle Type

On the basis of vehicle type, the market is segmented into passenger cars, light commercial vehicles, and heavy commercial vehicles. The Passenger Cars segment dominated the market with 67% share in 2025, driven by strong consumer demand for connected infotainment features such as navigation, voice control, and multimedia systems. OEMs are heavily investing in digital cockpit innovations for passenger vehicles. Rising EV penetration further strengthens dominance. AI-driven personalization enhances user engagement. High global production volumes also support leadership. Continuous innovation in automotive electronics reinforces this segment.

The Light Commercial Vehicle (LCV) segment is expected to be the fastest growing at 9.0% CAGR from 2026 to 2033, driven by fleet digitalization and logistics optimization. LCVs increasingly rely on infotainment-integrated telematics for route planning and tracking. Growth of e-commerce and delivery services is boosting adoption. Fleet operators are investing in connected mobility solutions. Electrification of LCVs further supports demand. It is emerging as a key growth segment. Regulatory pressure toward electrification is boosting demand. Connected mobility solutions are expanding rapidly in this segment.

- By Installation

On the basis of installation, the market is segmented into OEM and aftermarket systems. The OEM segment dominated the market with 74% share in 2025, driven by factory-installed infotainment control units ensuring seamless integration, high reliability, and compliance with automotive standards. OEM systems support OTA updates and advanced connected services. Automakers prefer standardized architectures for cost efficiency and scalability. Rising EV production strengthens OEM dominance. Enhanced cybersecurity and system performance further support adoption. It remains the primary deployment channel globally.

The Aftermarket segment is expected to be the fastest growing at 9.0% CAGR from 2026 to 2033, driven by rising demand for infotainment upgrades in existing vehicles. Consumers are increasingly adopting retrofit solutions with connectivity and multimedia capabilities. Declining hardware costs and plug-and-play systems are accelerating adoption. Growth in used vehicle markets, especially in emerging economies, is expanding the base. Increasing consumer demand for smart mobility features is boosting growth. Technological advancements in compact control units are further supporting expansion. Technological miniaturization is further enabling widespread adoption.

Control Unit in Vehicle Infotainment Market Regional Analysis

North America dominated the control unit in vehicle infotainment market with the largest revenue share of 32.35% in 2025, supported by high penetration of connected vehicles, strong presence of leading automotive OEMs, and rapid adoption of advanced digital cockpit and infotainment systems. The region benefits from early integration of software-defined vehicle architectures, strong consumer demand for in-vehicle connectivity, and widespread deployment of infotainment systems with cloud-based and AI-enabled features. Increasing investments in EV platforms, autonomous driving technologies, and 5G-enabled connectivity are further strengthening market growth. Growing focus on enhanced in-car user experience and continuous software upgrades continues to reinforce North America’s leadership position in the global market.

U.S. Control Unit in Vehicle Infotainment Market Insight

The U.S. control unit in vehicle infotainment market is witnessing strong growth due to rapid adoption of connected vehicles, advanced digital cockpit systems, and increasing integration of AI-enabled infotainment platforms. Strong presence of leading automotive OEMs and technology companies is driving innovation in domain control units and software-defined vehicle architectures. Rising demand for in-car connectivity, real-time navigation, and cloud-based entertainment services is further supporting market expansion. In addition, increasing penetration of electric vehicles and autonomous driving technologies is accelerating deployment of centralized infotainment control units. Continuous investments in 5G connectivity and over-the-air software ecosystems are strengthening the country’s leadership in this market.

Europe Control Unit in Vehicle Infotainment Market Insight

The Europe control unit in vehicle infotainment market remains a major contributor to global revenue, driven by strong automotive engineering capabilities, strict regulatory standards, and high adoption of advanced infotainment technologies. The region benefits from widespread deployment of digital cockpit systems across premium and mass-market vehicles. Increasing focus on vehicle connectivity, safety compliance, and sustainability is supporting market expansion. European OEMs are heavily investing in centralized vehicle architectures and software-defined infotainment platforms. Growing demand for EVs and luxury vehicles is further accelerating adoption of advanced control units across the region.

U.K. Control Unit in Vehicle Infotainment Market Insight

The U.K. control unit in vehicle infotainment market is experiencing steady growth, supported by rising adoption of connected mobility solutions and increasing integration of advanced infotainment systems in passenger vehicles. Strong automotive R&D capabilities and a growing focus on software-driven vehicle technologies are driving innovation in infotainment control units. Demand for premium in-car entertainment and navigation systems is also increasing across urban mobility markets. In addition, investments in autonomous vehicle testing and smart transportation infrastructure are supporting market expansion. Integration of AI and cloud-based infotainment services is further strengthening the U.K.’s position in this sector.

Germany Control Unit in Vehicle Infotainment Market Insight

The Germany control unit in vehicle infotainment market is expanding steadily due to its strong automotive manufacturing base and leadership in vehicle electronics innovation. Major OEMs are actively adopting centralized domain control architectures for infotainment and cockpit systems. Increasing focus on premium vehicle segments and advanced driver assistance integration is driving demand for high-performance infotainment control units. Germany’s emphasis on engineering precision and automotive software development is further strengthening market growth. Continuous advancements in electric mobility and connected vehicle technologies are also accelerating adoption across the country.

Asia-Pacific Control Unit in Vehicle Infotainment Market Insight

The Asia-Pacific control unit in vehicle infotainment market is expected to witness rapid growth, driven by rising vehicle production, expanding EV adoption, and increasing demand for connected mobility solutions. Countries such as China, India, Japan, and South Korea are leading regional expansion through large-scale automotive manufacturing and technology integration. Growing investments in smart transportation infrastructure and digital cockpit technologies are further supporting market development. Rising consumer preference for advanced infotainment features such as voice control and real-time connectivity is boosting demand. In addition, strong growth in automotive R&D and software development is accelerating regional adoption.

Japan Control Unit in Vehicle Infotainment Market Insight

The Japan control unit in vehicle infotainment market is witnessing steady growth due to strong automotive innovation and early adoption of advanced electronics in vehicles. Leading Japanese OEMs are integrating high-performance infotainment control units to enhance user experience and vehicle connectivity. Increasing focus on hybrid and electric vehicles is further driving demand for centralized infotainment systems. The country’s emphasis on robotics, AI, and smart mobility solutions is supporting technological advancement in this sector. Continuous development of next-generation cockpit systems is strengthening Japan’s role in the global market.

China Control Unit in Vehicle Infotainment Market Insight

The China control unit in vehicle infotainment market is growing rapidly, driven by large-scale vehicle production, strong EV adoption, and increasing demand for smart connected vehicles. Domestic OEMs are aggressively integrating advanced infotainment control units to enhance competitiveness in both domestic and global markets. Rising adoption of AI-powered and cloud-connected cockpit systems is significantly boosting market expansion. Government support for smart mobility and digital infrastructure is further accelerating growth. In addition, increasing consumer preference for high-tech in-vehicle experiences is positioning China as one of the fastest-growing markets globally.

Control Unit in Vehicle Infotainment Market Share

The control unit in vehicle infotainment industry is primarily led by well-established companies, including:

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- DENSO CORPORATION (Japan)

- Visteon Corporation (U.S.)

- HARMAN International (U.S.)

- Panasonic Automotive Systems Co., Ltd. (Japan)

- Aptiv PLC (Ireland)

- Marelli Holdings Co., Ltd. (Japan)

- Hyundai Mobis Co., Ltd. (South Korea)

- Alpine Electronics, Inc. (Japan)

- Pioneer Corporation (Japan)

- JVCKENWOOD Corporation (Japan)

- Mitsubishi Electric Corporation (Japan)

- Garmin Ltd. (Switzerland)

- Qualcomm Technologies, Inc. (U.S.)

- NVIDIA Corporation (U.S.)

- LG Electronics Inc. (South Korea)

- Sony Group Corporation (Japan)

- FORVIA (France)

- TomTom International BV (Netherlands)

Latest Developments in Control Unit in Vehicle Infotainment Market

- In September 2022, NVIDIA unveiled its DRIVE Thor centralized computing platform designed to unify infotainment, autonomous driving, and cockpit functions into a single high-performance vehicle control unit. The system replaces multiple electronic control units with a centralized AI-powered architecture. It enables advanced infotainment capabilities such as real-time graphics rendering, deep learning applications, and multi-domain integration. The platform is designed to support next-generation software-defined vehicles and autonomous systems

- In January 2022, Qualcomm launched its Snapdragon Digital Chassis platform, a unified automotive solution integrating infotainment, connectivity, and cloud services through advanced control unit architecture. The platform supports AI-powered digital cockpit experiences, 5G connectivity, and real-time data processing for vehicles. It enables automakers to build scalable and software-defined infotainment systems across multiple vehicle segments. The solution enhances integration of navigation, entertainment, and safety features within a centralized computing framework

- In October 2021, General Motors announced its Ultifi software platform designed to enable a software-defined vehicle ecosystem powered by centralized infotainment and control unit architecture. The platform allows continuous over-the-air updates, app-based vehicle features, and cloud-connected infotainment services across GM vehicles. It decouples hardware and software, enabling long-term scalability and feature expansion. Ultifi integrates infotainment, diagnostics, and vehicle control into a unified digital system

- In June 2021, BMW launched its next-generation iDrive 8 infotainment system with the BMW iX, featuring a fully digital curved display and centralized infotainment control unit architecture. The system integrates navigation, entertainment, vehicle settings, and cloud-based services into a unified software platform. It supports over-the-air updates and AI-driven personalization for enhanced user experience. The architecture reflects BMW’s shift toward software-defined vehicle systems and connected mobility ecosystems

- In January 2021, Mercedes-Benz introduced the MBUX Hyperscreen system for its EQS flagship electric vehicle, featuring a 56-inch curved digital cockpit powered by a centralized infotainment control unit. The system integrates instrument cluster, infotainment, and passenger display into a unified AI-driven architecture, enabling personalized user experiences, real-time navigation, and advanced multimedia functions. It represents a major step toward centralized vehicle computing and software-defined infotainment systems. The platform uses high-performance processors and machine learning to adapt to driver behavior and preferences

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.