Global Copper Indium Gallium Selenide Solar Cells Market

Market Size in USD Billion

USD

3.08 Billion

USD

5.60 Billion

2025

2033

USD

3.08 Billion

USD

5.60 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.08 Billion | |

| USD 5.60 Billion | |

| % | |

|

Copper Indium Gallium Selenide Solar Cells (Ci(G)S) Market Overview

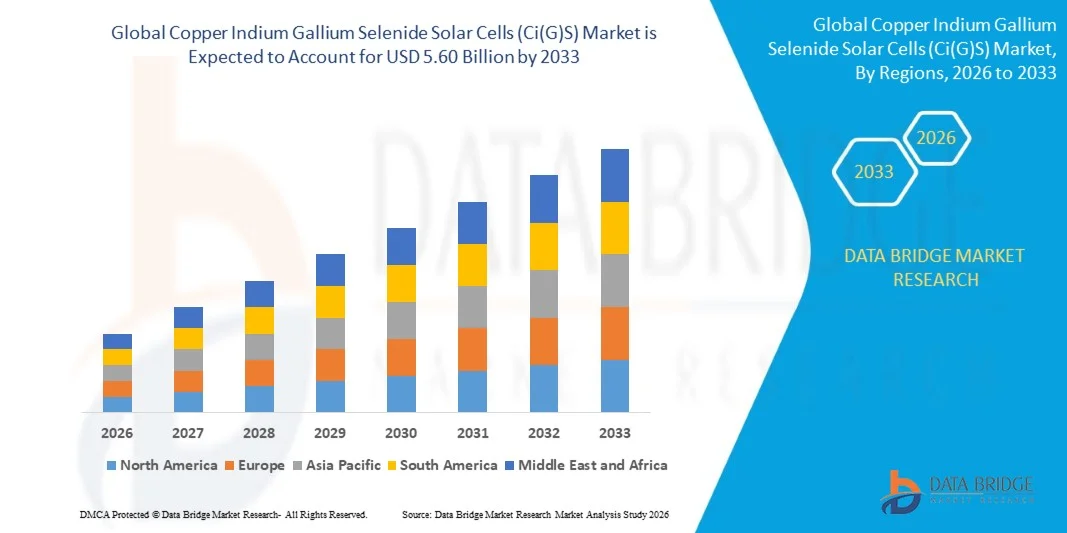

As per Data Bridge Market Research analysis The copper indium gallium selenide solar cells (Ci(G)S) market was valued at USD 3.08 billion in 2025 and is projected to reach USD 5.60 billion by 2033, growing at a CAGR of 7.78% from 2026 to 2033. The market is experiencing consistent growth driven by increasing adoption of renewable energy, rising demand for lightweight and flexible photovoltaic technologies, and continuous improvements in thin-film solar cell efficiency.

The growing focus on decarbonization, government incentives supporting solar power deployment, and increasing adoption of building-integrated photovoltaics (BIPV) are accelerating demand for CIGS solar cells across residential, commercial, and utility-scale applications. In addition, advancements in flexible module manufacturing, improvements in deposition technologies, and the superior high-temperature performance of CIGS compared with conventional crystalline silicon technologies are expanding its application in portable electronics, automotive, and next-generation solar installations.

Market Size & Forecast

- Global Market Value (2025): USD 3.08 Billion

- Expected Market Value (2033): USD 5.60 Billion

- Forecast CAGR (2026–2033): 7.78%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Key Market Trends & Insights

- North America dominated the copper indium gallium selenide solar cells (Ci(G)S) market with the largest revenue share of 38.2% in 2025, supported by strong government incentives, established manufacturing capabilities, advanced research infrastructure, and increasing investments in renewable energy deployment.

- The co-evaporation segment led the market with a 45.5% share in 2025, driven by its capability to achieve the highest commercial conversion efficiencies and superior absorber layer quality.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 11.8% from 2026 to 2033, fueled by massive renewable energy deployment targets, manufacturing scale advantages, and growing energy demand across emerging economies.

- Chemical vapour deposition are the fastest-growing type, projected to register a CAGR of 11.1%, reflecting the surge in demand for scalable and cost-efficient manufacturing technologies.

- The 2–3 micro meters segment dominated the film thickness category with a 50.5% revenue share in 2025, led by its optimal balance between light absorption, carrier collection efficiency, and material utilization.

- Utility-scale accounted for 38.5% of the market, preferred by the increasing deployment of large-scale solar farms and grid-connected renewable energy projects

- The building-integrated photovoltaics (BIPV) segment is the fastest-growing application category, with a CAGR of 14.1%, driven by increasing adoption of energy-efficient building designs and net-zero construction initiatives.

Report Scope and Copper Indium Gallium Selenide Solar Cells (Ci(G)S) Market Segmentation

|

Attributes |

Copper Indium Gallium Selenide Solar Cells (Ci(G)S) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Ascent Solar Technologies (U.S.) · AVANCIS GmbH (Germany) · MiaSolé (U.S.) · Midsummer AB (Sweden) · Heliatek GmbH (Germany) · ULVAC, Inc. (Japan) · Manz AG (Germany) · Sunplugged GmbH (Austria) · Solar Cloth System Ltd (U.K.) · Exeger Operations AB (Sweden) · Fujikura Europe Limited. (U.K.) · G24 Power Ltd. (U.K.) · Konica Minolta Sensing Europe B.V. (Netherlands) · Merck KGaA (Germany) · Oxford Photovoltaics Ltd (U.K.) · Peccell Technologies, Inc. (Japan) · Solaronix SA (Switzerland) · First Solar. (U.S.) · ALPS Technology Inc. (U.S.) · SunPower Inc. (U.S.) · Suniva Inc (U.S.) |

|

Market Opportunities |

· Growing adoption of Building-Integrated Photovoltaics (BIPV) · Expanding use in transportation, aerospace, and portable electronics · Rural electrification and off-grid solar deployment in emerging economies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Copper Indium Gallium Selenide Solar Cells (Ci(G)S) Market Trends

Trend: Digitalized Manufacturing and Supply Chain Transformation

The copper indium gallium selenide (CIGS) solar cells market is witnessing increasing adoption of digitalized manufacturing processes, automated production systems, and advanced process monitoring technologies to improve production efficiency and module quality. Manufacturers are increasingly shifting toward continuous roll-to-roll deposition architectures that enable scalable production compared with conventional batch manufacturing approaches. Advanced process control systems are improving the monitoring of absorber layer deposition, temperature management, and material composition optimization across large-area substrates. Digital manufacturing technologies are helping CIGS producers reduce yield variations, improve process stability, and implement predictive maintenance strategies. Real-time monitoring solutions, automated inspection systems, and data-driven production optimization are becoming increasingly important as manufacturers focus on improving conversion efficiency and reducing production costs.

For instance, in May 2025, Roltec announced plans to establish a new CIGS solar module manufacturing facility in Poland, with Singulus Technologies supplying advanced physical vapor deposition (PVD) vacuum sputtering systems for the production line. The facility will manufacture CIGS solar cells on glass substrates using advanced thin-film deposition equipment designed for research, development, and large-scale production, highlighting the industry's ongoing shift toward automated and scalable CIGS manufacturing processes.

Copper Indium Gallium Selenide Solar cells (Ci(G)S) Market Dynamics

Key Market Driver: Growing Demand for Building-Integrated Photovoltaics and Flexible Solar Solutions

The expanding building-integrated photovoltaics (BIPV) market represents a major growth driver for copper indium gallium selenide (CIGS) solar cells, as architects and developers increasingly seek renewable energy solutions that can be integrated into building structures. CIGS technology offers significant advantages due to its ability to be deposited on different substrates, including glass, metal foils, and flexible materials, enabling applications across facades, curved surfaces, rooftops, and customized architectural designs. Unlike conventional rigid photovoltaic modules, flexible CIGS panels provide lightweight and adaptable solutions for space-constrained urban environments. Their ability to perform effectively under diffuse light conditions makes them suitable for vertical building applications where direct solar exposure may be limited. Growing adoption of sustainable construction practices, net-zero buildings, and renewable energy integration is creating new opportunities for CIGS technology. Flexible CIGS modules are also enabling applications beyond traditional solar installations, including portable electronics, automotive-integrated photovoltaics, and aerospace systems.

For instance, in December 2024, research published on global building-integrated photovoltaic potential highlighted the increasing importance of facade photovoltaic applications, showing significant potential for integrating solar technologies into building surfaces beyond conventional rooftop installations.

Key Restraint/Challenge: Material Supply Chain Constraints and Price Volatility Impact Market Stability

The availability and price fluctuations of critical raw materials remain significant challenges for the copper indium gallium selenide (CIGS) solar cells market. CIGS manufacturing depends on key materials such as indium and gallium, which have complex supply chains and are primarily obtained as by-products from other mining and refining activities. Indium supply is closely linked to zinc refining operations, while gallium availability depends largely on aluminum and zinc processing capacity. Supply concentration in specific regions creates potential risks related to geopolitical changes, export restrictions, and raw material price fluctuations. These uncertainties can affect manufacturing costs, investment decisions, and long-term production planning for CIGS manufacturers. Improving material recycling, developing alternative sourcing strategies, and reducing dependency on critical minerals remain important focus areas for ensuring sustainable growth of the CIGS solar industry.

For instance, according to the U.S. Geological Survey (USGS), indium is primarily recovered as a by-product of zinc processing, while gallium supply is dependent on refining activities, creating supply-chain sensitivity for industries using these materials, including photovoltaic applications.

Key Market Opportunity: Expansion in Off-Grid and Remote Area Electrification

The expansion of off-grid and remote electrification programs represents a significant opportunity for the copper indium gallium selenide (CIGS) solar cells market. The lightweight, flexible, and durable characteristics of CIGS modules make them suitable for deployment in locations where conventional solar panels face transportation, installation, or infrastructure challenges. Remote communities, disaster relief operations, military applications, and portable energy systems are increasingly adopting lightweight photovoltaic technologies due to their ease of installation and mobility advantages. Flexible CIGS modules can be transported easily and deployed in areas with limited grid connectivity, creating opportunities across emerging economies and humanitarian energy programs. Government initiatives and international organizations focusing on universal energy access are supporting demand for decentralized renewable energy solutions. The increasing requirement for reliable power sources in remote locations is expected to create additional growth opportunities for CIGS manufacturers.

For instance, in May 2025, Roltec announced plans to establish a new CIGS solar module manufacturing facility in Poland, with Singulus Technologies supplying advanced physical vapor deposition (PVD) vacuum sputtering systems for the production line. The facility will manufacture CIGS solar cells on glass substrates using advanced thin-film deposition equipment designed for research, development, and large-scale production, highlighting the industry's ongoing shift toward automated and scalable CIGS manufacturing processes

Copper Indium Gallium Selenide Solar Cells (Ci(G)S) Market Scope

The copper indium gallium selenide solar cells (Ci(G)S) market is segmented on the basis of type, film thickness, form, application, and end user.

- By Type

On the basis of type, the market is segmented into electrospray deposition, chemical vapour deposition, co-evaporation, and film production. The co-evaporation segment dominated the market with the largest revenue share of 45.5% in 2025, owing to its capability to achieve the highest commercial conversion efficiencies and superior absorber layer quality. The process enables precise control of copper, indium, gallium, and selenium deposition, resulting in improved module performance and long-term reliability. It is the preferred manufacturing method for high-efficiency CIGS solar cells and is extensively adopted by leading manufacturers. Continuous investments in utility-scale photovoltaic production and advancements in deposition equipment continue to strengthen demand. The technology also supports large-area manufacturing with consistent film quality, making it the most commercially established deposition process. Its proven scalability and manufacturing maturity continue to reinforce its market leadership.

The chemical vapour deposition (CVD) segment is projected to witness the fastest growth at a CAGR of 11.1% during the forecast period, driven by increasing demand for scalable and cost-efficient manufacturing technologies. CVD provides excellent process control, high deposition uniformity, and compatibility with large-area substrates. Manufacturers are investing in advanced CVD systems to improve throughput while reducing production costs and material wastage. The technology also enables fabrication on flexible substrates, supporting emerging applications in portable electronics and building-integrated photovoltaics. Continuous innovations in deposition equipment are improving manufacturing efficiency. These factors are expected to accelerate adoption of CVD-based CIGS production.

- By Film Thickness

On the basis of film thickness, the market is segmented into 1–2 micro meters, 2–3 micro meters, and 3–4 micro meters. The 2–3 micro meters segment dominated the market with the largest revenue share of 50.5% in 2025, owing to its optimal balance between light absorption, carrier collection efficiency, and material utilization. Research demonstrates that absorber layers within this thickness range deliver excellent photovoltaic performance while minimizing raw material consumption. Manufacturers widely prefer this thickness because it supports commercial-scale production with stable conversion efficiencies. The segment is extensively utilized across commercial and utility-scale installations. Continuous improvements in thin-film engineering have further enhanced module efficiency within this thickness range. Its established role in commercial CIGS manufacturing continues to support its leading market position.

The 1–2 micro meters segment is expected to register the fastest growth at a CAGR of 10.1% during the forecast period due to increasing focus on reducing manufacturing costs and improving material efficiency. Advanced light-trapping structures and improved absorber engineering are enabling thinner films to maintain competitive efficiencies. Manufacturers are actively developing ultra-thin CIGS modules to reduce indium and gallium consumption while lowering production costs. Growing demand for lightweight and flexible photovoltaic products is further supporting adoption. Research and development efforts continue to improve electrical performance in thinner absorber layers. These technological advancements are expected to drive rapid market growth.

- By Form

On the basis of form, the market is segmented into thin film, flexible, and glass-based. The thin film segment dominated the market with the largest revenue share of 61.9% in 2025, owing to the superior material efficiency, high light absorption capability, and cost advantages associated with CIGS thin-film photovoltaic technology. Thin-film CIGS cells require lower semiconductor material usage compared with conventional solar technologies while maintaining high conversion efficiency under varying environmental conditions. The segment is extensively adopted in utility-scale solar installations, commercial photovoltaic systems, and building-integrated photovoltaic (BIPV) applications. Continuous improvements in deposition techniques, absorber-layer engineering, and manufacturing scalability are enhancing production efficiency. Increasing investments in advanced photovoltaic technologies and demand for lightweight solar modules are further supporting segment growth. The established commercial presence of thin-film CIGS technology continues to maintain its leading position in the global market.

The flexible segment is projected to register the fastest growth at a CAGR of 12.1% from 2026 to 2033, driven by increasing demand for lightweight, portable, and adaptable photovoltaic solutions. The segment benefits from roll-to-roll manufacturing capabilities that enable scalable production and reduced material consumption. Increasing adoption of vehicle-integrated photovoltaics and off-grid solar solutions is creating new growth opportunities. Continuous advancements in flexible substrate technologies are improving durability and efficiency. Rising demand for versatile solar solutions where traditional rigid panels are unsuitable is expected to accelerate segment expansion.

- By Application

On the basis of application, the market is segmented into building integrated photovoltaic (BIPV), transportation, consumer electronics, utility-scale and industrial. The utility-scale segment dominated the market with a 38.5% revenue share in 2025, driven by increasing deployment of large-scale solar farms and grid-connected renewable energy projects. Utility developers prefer CIGS technology because of its superior performance under high temperatures and low-light conditions. Continuous reductions in manufacturing costs and improving module efficiencies have enhanced project economics. Government renewable energy policies and utility procurement programs continue to stimulate installations globally. Increasing investments in sustainable electricity generation further support segment growth. Expanding utility-scale solar capacity across Asia-Pacific, North America, and Europe continues to reinforce its dominant market position.

The building-integrated photovoltaics (BIPV) segment is expected to witness the fastest growth at a CAGR of 14.1% during the forecast period, driven by increasing adoption of energy-efficient building designs and net-zero construction initiatives. Lightweight and flexible CIGS modules can be seamlessly integrated into building facades, rooftops, skylights, and windows without compromising architectural aesthetics. Growing investments in green buildings and supportive energy-efficiency regulations are accelerating adoption worldwide. Architects and developers increasingly prefer flexible photovoltaic materials for modern infrastructure projects. Continuous product innovations are improving module appearance and installation flexibility. These factors are expected to drive strong growth throughout the forecast period.

- By End User

On the basis of end user, the market is segmented into automobiles, electronics and electrical, energy and power, and others. The energy and power segment dominated the market with a 60.1% revenue share in 2025, owing to increasing deployment of CIGS technology in utility companies, independent power producers, and renewable energy generation projects. Rising investments in clean energy infrastructure and global decarbonization initiatives continue to support demand. CIGS modules offer advantages such as excellent high-temperature performance, flexibility, and reliable electricity generation under varying environmental conditions. Utility operators continue to diversify their renewable energy portfolios through thin-film photovoltaic technologies. Public and private investments in solar infrastructure are further strengthening the segment. Its widespread use in large-scale electricity generation maintains its dominant market position.

The automobiles segment is projected to register the fastest growth, expanding at a CAGR of 18.7% during 2026–2033, driven by increasing integration of lightweight and flexible CIGS modules into electric vehicles. Automotive manufacturers are utilizing CIGS technology in solar roofs and auxiliary charging systems to improve vehicle energy efficiency. Flexible thin-film modules can be integrated onto curved vehicle surfaces without adding significant weight. Rising production of electric vehicles and increasing investments in vehicle-integrated photovoltaics are accelerating adoption. Continuous research into solar-assisted mobility solutions is creating new commercial opportunities. Growing focus on sustainable transportation is expected to further strengthen this segment.

Copper Indium Gallium Selenide Solar Cells (Ci(G)S) Market Regional Analysis

North America dominated the copper indium gallium selenide solar cells (Ci(G)S) market with the largest revenue share of 38.2% in 2025, supported by strong government incentives, established manufacturing capabilities, advanced research infrastructure, and increasing investments in renewable energy deployment. The region also benefits from the early adoption of advanced photovoltaic manufacturing technologies, smart energy management systems, and digital monitoring platforms that enhance solar asset performance. Growing investments in utility-scale solar projects, building-integrated photovoltaics (BIPV), and next-generation thin-film solar technologies are accelerating market expansion. The presence of leading research institutions and ongoing efforts to improve module efficiency and production scalability continue to support innovation across the value chain.

U.S. Copper Indium Gallium Selenide Solar Cells (Ci(G)S) Market Insight

The U.S. copper indium gallium selenide (CIGS) solar cells market is witnessing strong growth due to increasing investments in domestic solar manufacturing, renewable energy deployment, and advanced photovoltaic research. The country's federal Investment Tax Credit (ITC), Production Tax Credit (PTC), and Department of Energy funding for thin-film technologies are accelerating CIGS commercialization. Growing adoption of building-integrated photovoltaics (BIPV), utility-scale solar projects, and corporate renewable energy procurement is driving market demand. In addition, the Inflation Reduction Act is encouraging domestic manufacturing and technology innovation, while continuous improvements in module efficiency and flexible solar applications are strengthening the U.S. position in the global CIGS industry.

Europe Copper Indium Gallium Selenide (CIGS) Solar Cells Market Insight

The Europe copper indium gallium selenide (CIGS) solar cells market remains a major contributor to global revenue, driven by ambitious climate targets, the European Green Deal, and increasing investments in renewable energy technologies. The widespread deployment of CIGS modules in building-integrated photovoltaics (BIPV), commercial rooftops, and sustainable infrastructure projects is supporting market expansion. Increasing government support, stringent building energy regulations, and the REPowerEU initiative are encouraging adoption of advanced thin-film photovoltaic technologies. Furthermore, continuous investments in clean technology manufacturing and growing demand for energy-efficient buildings continue to strengthen the CIGS market across Europe.

U.K. Copper Indium Gallium Selenide (CIGS) Solar Cells Market Insight

The U.K. copper indium gallium selenide (CIGS) solar cells market is experiencing steady growth, supported by rising investments in renewable energy infrastructure and the country's commitment to achieving net-zero emissions. Increasing adoption of building-integrated photovoltaics, commercial rooftop solar systems, and low-carbon construction practices is contributing to market growth. Government policies promoting energy efficiency and clean electricity generation continue to encourage deployment of advanced thin-film solar technologies. Moreover, ongoing research into flexible photovoltaic materials and sustainable building solutions is positioning the U.K. as an emerging market for CIGS innovation.

Germany Copper Indium Gallium Selenide (CIGS) Solar Cells Market Insight

The Germany copper indium gallium selenide (CIGS) solar cells market is expanding steadily due to the country's strong renewable energy policies, advanced photovoltaic manufacturing capabilities, and continuous investments in solar innovation. Germany remains a leading adopter of building-integrated photovoltaics and thin-film solar technologies supported by the Renewable Energy Sources Act (EEG). Increasing installations of commercial and industrial solar systems, together with strong research capabilities and government incentives, are driving market expansion. Continuous focus on carbon neutrality and next-generation photovoltaic manufacturing further strengthens Germany's leadership in the European CIGS market.

Asia-Pacific Copper Indium Gallium Selenide (CIGS) Solar Cells Market Insight

The Asia-Pacific copper indium gallium selenide (CIGS) solar cells market is expected to witness rapid growth, driven by expanding photovoltaic manufacturing capacity, increasing renewable energy investments, and supportive government policies across China, India, Japan, and South Korea. The region benefits from cost-efficient manufacturing, integrated supply chains, and rising deployment of utility-scale and distributed solar projects. Increasing demand for flexible photovoltaic products, building-integrated solar systems, and portable energy solutions is further supporting market expansion. In addition, growing investments in advanced thin-film production facilities and continuous technology innovation are accelerating adoption of CIGS solar cells throughout the region.

Japan Copper Indium Gallium Selenide (CIGS) Solar Cells Market Insight

The Japan copper indium gallium selenide (CIGS) solar cells market is witnessing consistent growth due to increasing investments in advanced photovoltaic technologies, energy security initiatives, and commercialization of high-efficiency thin-film modules. Government support through the Green Innovation Fund and increasing adoption of lightweight building-integrated photovoltaic solutions are strengthening market development. Japanese manufacturers continue to invest in improving CIGS efficiency and flexible module technologies for residential, commercial, and specialty applications. Furthermore, the country's emphasis on sustainable infrastructure and renewable energy diversification is supporting continued market growth.

China Copper Indium Gallium Selenide (CIGS) Solar Cells Market Insight

The China copper indium gallium selenide (CIGS) solar cells market is growing rapidly, driven by large-scale photovoltaic manufacturing, supportive government policies, and ambitious renewable energy capacity expansion targets. Increasing investments under the 14th Five-Year Plan, expansion of domestic CIGS manufacturing capacity, and rising deployment of utility-scale solar projects are significantly boosting market demand. Growing adoption of flexible photovoltaic technologies, continuous improvements in production efficiency, and strong government support for advanced thin-film solar technologies are positioning China as one of the fastest-growing CIGS markets globally. The country's integrated manufacturing ecosystem and expanding clean energy investments continue to reinforce its global leadership in photovoltaic production.

Copper Indium Gallium Selenide Solar Cells (Ci(G)S) Market Share

The copper indium gallium selenide solar cells (Ci(G)S) industry is primarily led by well-established companies, including:

- Ascent Solar Technologies (U.S.)

- AVANCIS GmbH (Germany)

- MiaSolé (U.S.)

- Midsummer AB (Sweden)

- Heliatek GmbH (Germany)

- ULVAC, Inc. (Japan)

- Manz AG (Germany)

- Sunplugged GmbH (Austria)

- Solar Cloth System Ltd (U.K.)

- Exeger Operations AB (Sweden)

- Fujikura Europe Limited. (U.K.)

- G24 Power Ltd. (U.K.)

- Konica Minolta Sensing Europe B.V. (Netherlands)

- Merck KGaA (Germany)

- Oxford Photovoltaics Ltd (U.K.)

- Peccell Technologies, Inc. (Japan)

- Solaronix SA (Switzerland)

- First Solar. (U.S.)

- ALPS Technology Inc. (U.S.)

- SunPower Inc. (U.S.)

- Suniva Inc (U.S.)

Latest Developments in Copper Indium Gallium Selenide Solar Cells (Ci(G)S) Market

- In June 2025, Ascent Solar Technologies announced that it achieved a 15.7% AM0 production-scale efficiency for its flexible CIGS photovoltaic technology, improving from 14% in early 2024. The milestone was achieved through material quality enhancements, process optimization, and manufacturing improvements, strengthening the company's position in space-grade flexible solar technology for satellite and aerospace applications.

- In June 2025, Saatvik Solar commenced construction of an integrated 4.8 GW solar cell and 4 GW module manufacturing facility in Odisha, India. The project aims to expand domestic photovoltaic manufacturing capacity and support future production of advanced thin-film and next-generation solar technologies alongside conventional solar products

- In November 2023, a 14-member European consortium launched a €5.9 million Horizon Europe project to advance commercial CIGS solar cell manufacturing. The initiative targets 25% power conversion efficiency by improving manufacturing processes and scaling bifacial, semi-transparent, and tandem CIGS technologies for commercial production and outdoor module testing

- In September 2023, Ascent Solar Technologies announced that it had achieved 15.2% production-trial efficiency for its CIGS solar cells after replacing the conventional cadmium sulfide buffer layer with a new material. The development significantly improved commercially manufactured CIGS cell performance and highlighted continued progress toward higher-efficiency flexible thin-film solar modules

- In September 2021, researchers at the National Renewable Energy Laboratory and collaborators reported a world-record efficiency of 23.35% for a CIGS solar cell, demonstrating further improvements in thin-film photovoltaic performance through optimized absorber and interface engineering. The achievement reinforced the long-term commercial potential of high-efficiency CIGS technology for next-generation solar applications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Copper Indium Gallium Selenide Solar Cells Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Copper Indium Gallium Selenide Solar Cells Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Copper Indium Gallium Selenide Solar Cells Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.