Global Coronary Intravascular Lithotripsy Ivl Market

Market Size in USD Million

USD

277.94 Million

USD

493.50 Million

2024

2032

USD

277.94 Million

USD

493.50 Million

2024

2032

| 2025 - 2032 | |

| USD 277.94 Million | |

| USD 493.50 Million | |

| % | |

|

Coronary Intravascular Lithotripsy (IVL) Market Size

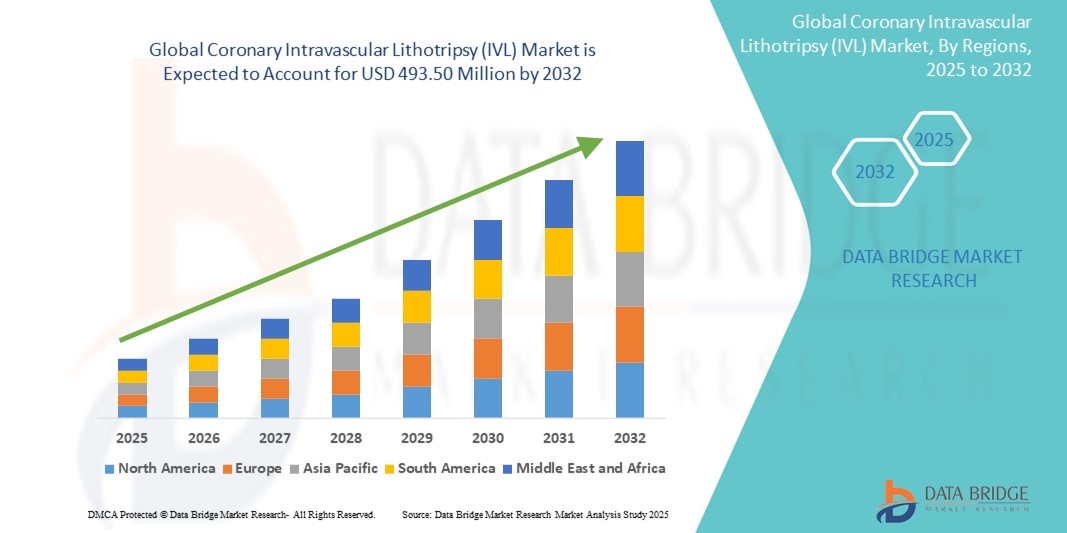

- The global coronary intravascular lithotripsy (IVL) market size was valued at USD 277.94 million in 2024 and is expected to reach USD 493.50 million by 2032, at a CAGR of 7.44% during the forecast period

- The market growth is largely driven by the increasing prevalence of calcified coronary artery disease, alongside a rising elderly population and growing awareness of minimally invasive cardiovascular procedures

- Furthermore, the enhanced safety profile and procedural simplicity of IVL compared to traditional atherectomy techniques is attracting cardiologists and healthcare systems asuch as. These converging factors are accelerating the adoption of IVL technologies, thereby significantly boosting the industry's growth

Coronary Intravascular Lithotripsy (IVL) Market Analysis

- Coronary intravascular lithotripsy (IVL), a novel technique for treating calcified coronary lesions using sonic pressure waves to fracture hardened plaque, is emerging as a critical tool in modern interventional cardiology due to its precision, safety profile, and ability to improve stent expansion outcomes in complex cases

- The growing demand for IVL is primarily fueled by the increasing prevalence of coronary artery disease (CAD), a rise in percutaneous coronary intervention (PCI) procedures, and the need for safer alternatives to traditional plaque modification techniques such as rotational atherectomy

- North America dominated the coronary intravascular lithotripsy (IVL) market with the largest revenue share of 43% in 2024, supported by advanced healthcare infrastructure, early technology adoption, and favorable reimbursement policies, with the U.S. witnessing high procedural uptake driven by clinical endorsements, increased training programs, and regulatory support for innovative cardiovascular devices

- Asia-Pacific is expected to be the fastest growing region in the coronary intravascular lithotripsy (IVL) market during the forecast period due to a rising geriatric population, increasing awareness of advanced treatment options, and expanding access to interventional cardiology in emerging economies

- Coronary Intravascular Lithotripsy (IVL) Balloon Catheters segment dominated the coronary intravascular lithotripsy (IVL) market with a market share of 67.9% in 2024, driven by its effectiveness in delivering localized shockwaves to modify calcified plaques and its widespread adoption in interventional cardiology procedures

Report Scope and Coronary Intravascular Lithotripsy (IVL) Market Segmentation

|

Attributes |

Coronary Intravascular Lithotripsy (IVL) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Coronary Intravascular Lithotripsy (IVL) Market Trends

“Rising Preference for IVL over Traditional Atherectomy Techniques”

- A significant and emerging trend in the global coronary intravascular lithotripsy (IVL) market is the growing clinical and procedural preference for IVL over conventional atherectomy in treating heavily calcified coronary lesions, primarily due to its enhanced safety profile and procedural simplicity

- For instance, Shockwave Medical’s IVL platform has seen rapid adoption globally, with interventional cardiologists increasingly favoring it for its reduced risk of vessel dissection or perforation compared to high-speed rotational atherectomy, particularly in complex PCI cases

- IVL technology utilizes localized sonic pressure waves to fracture calcium within the arterial wall while preserving soft tissue, leading to more predictable stent expansion and improved long-term outcomes. Clinical studies, such as DISRUPT CAD trials, continue to validate the efficacy and safety of IVL, supporting broader adoption in real-world practice

- Hospitals and specialty clinics are increasingly integrating IVL into their cath lab protocols, especially for high-risk patients with multiple comorbidities or those unsuitable for more aggressive mechanical plaque modification techniques

- This shift in practice is being reinforced by updated interventional cardiology guidelines and the growing body of evidence supporting IVL’s advantages. Medical device companies such as Shockwave Medical are responding to this trend by investing in expanded training programs and global product launches tailored to specific lesion subsets

- The expanding demand for IVL across key markets reflects a broader trend toward minimally invasive, operator-friendly technologies that deliver consistent outcomes while minimizing complications—reshaping procedural strategies in modern interventional cardiology

Coronary Intravascular Lithotripsy (IVL) Market Dynamics

Driver

“Growing Incidence of Calcified Coronary Artery Disease and Preference for Safer Alternatives”

- The rising global prevalence of calcified coronary artery disease, particularly among aging populations and patients with comorbidities such as diabetes and chronic kidney disease, is a primary driver of demand for IVL systems

- For instance, the increasing number of complex PCI procedures worldwide especially in high-volume centers is driving the need for safer, more predictable lesion preparation tools such as IVL. According to a 2024 study, IVL use has increased significantly in tertiary care hospitals due to its favorable safety profile

- Unsuch as rotational or orbital atherectomy, which require high operator skill and carry a higher risk of vessel trauma, IVL offers a simpler, intuitive technique that enables uniform calcium modification and improved stent deployment, even in tight or eccentric lesions

- In addition, strong support from clinical trial data, such as DISRUPT CAD III, and positive endorsements from interventional cardiology societies are boosting physician confidence in IVL adoption across varied clinical settings

- The procedural ease, shorter learning curve, and ability to treat high-risk lesions with fewer complications are further contributing to IVL's growing appeal as a preferred plaque-modification strategy

Restraint/Challenge

“High Device Cost and Limited Reimbursement in Emerging Markets”

- Despite its clinical advantages, the relatively high cost of IVL systems particularly the balloon catheters and associated console infrastructure poses a significant barrier to widespread adoption, especially in cost-sensitive or resource-limited settings

- For instance, in many emerging economies, budget constraints in public hospitals and limited insurance coverage for advanced interventional technologies restrict access to IVL, pushing clinicians toward lower-cost alternatives such as high-pressure balloons or atherectomy devices

- Reimbursement challenges in several countries remain a hurdle, as payers may not yet fully recognize the long-term cost-effectiveness of IVL in reducing procedural complications and repeat interventions

- Manufacturers are working to address these barriers through health-economic studies, targeted pricing strategies, and educational outreach to demonstrate the value of IVL in improving patient outcomes and lowering downstream healthcare costs

- Expanding reimbursement frameworks, increasing awareness among health authorities, and developing cost-effective device variants will be crucial to accelerating adoption across broader clinical geographies

Coronary Intravascular Lithotripsy (IVL) Market Scope

The market is segmented on the basis of device type, end user, application, technology, patient age group, and distribution channel.

- By Device Type

On the basis of device type, the coronary intravascular lithotripsy (IVL) market is segmented into Coronary Intravascular Lithotripsy (IVL) Balloon Catheters and Intravascular Lithotripsy (IVL) Control Consoles. The Coronary IVL Balloon Catheters segment dominated the market with the largest market revenue share of 67.9% in 2024, driven by their core role in delivering sonic pressure waves for effective plaque modification. These catheters are favored in interventional procedures for their minimally invasive application, ability to enhance stent expansion, and high compatibility with existing catheter systems, leading to widespread clinical adoption.

The Intravascular Lithotripsy (IVL) Control Consoles segment is expected to witness the fastest growth rate from 2025 to 2032, supported by rising procedure volumes and increasing installation of consoles in catheterization labs, especially in high-volume cardiovascular centers globally.

- By End User

On the basis of end user, the coronary intravascular lithotripsy (IVL) market is segmented into hospitals, ambulatory surgical centers, and specialty clinics. The Hospitals segment dominated the market with the largest market revenue share of 58.9% in 2024, owing to the concentration of advanced cardiovascular infrastructure, trained interventional cardiologists, and high patient flow. Hospitals serve as the primary centers for complex percutaneous coronary interventions (PCI), which has driven IVL adoption.

The Ambulatory Surgical Centers segment is expected to witness the fastest growth rate from 2025 to 2032, as outpatient care trends rise and these centers increasingly invest in minimally invasive cardiovascular technologies to reduce costs and procedure times while maintaining safety and efficacy.

- By Application

On the basis of application, the coronary intravascular lithotripsy (IVL) market is segmented into Coronary Artery Disease (CAD) and Peripheral Artery Disease (PAD). The Coronary Artery Disease (CAD) segment dominated the market with the largest market revenue share of 64.6% in 2024, driven by the high global burden of CAD and IVL’s ability to treat heavily calcified coronary lesions effectively. Clinical evidence supporting improved stent expansion and safety outcomes has made IVL a preferred treatment strategy in complex coronary procedures.

The Peripheral Artery Disease (PAD) segment is expected to witness the fastest growth rate from 2025 to 2032, with increasing awareness of peripheral vascular diseases and IVL’s expanding use in non-coronary territories such as the iliac and femoropopliteal arteries.

- By Technology

On the basis of technology, the coronary intravascular lithotripsy (IVL) market is segmented into single-use systems and multi-use systems. The Single-Use Systems segment held the largest market revenue share of 71.2% in 2024, attributed to their safety benefits, infection control advantages, and ease of use in clinical settings. These systems are widely adopted due to minimal sterilization requirements and their regulatory preference in interventional procedures.

The Multi-Use Systems segment is expected to witness the fastest growth rate from 2025 to 2032, driven by their cost-efficiency and long-term usability, particularly in large hospital networks and facilities equipped with advanced sterilization capabilities.

- By Patient Age Group

On the basis of patient age group, the coronary intravascular lithotripsy (IVL) market is segmented into Adult and Pediatric. The Adult segment dominated the market with the largest market revenue share of 89.7% in 2024, as coronary and peripheral artery diseases are predominantly found in the adult and elderly population. The rising prevalence of cardiovascular risk factors such as hypertension, diabetes, and obesity further drives demand in this group.

The Pediatric segment is expected to witness the fastest growth rate from 2025 to 2032, due to rare congenital cardiovascular conditions requiring minimally invasive interventions, as IVL technology continues to evolve for broader clinical use.

- By Distribution Channel

On the basis of distribution channel, the coronary intravascular lithotripsy (IVL) market is segmented into direct sales and retail sales. The Direct Sales segment dominated the market with the largest market revenue share of 66.1% in 2024, supported by strong manufacturer-hospital partnerships and the need for personalized sales, device training, and procedural support. Direct channels ensure reliable supply chains and greater customization of procurement contracts.

The Retail Sales segment is expected to witness the fastest growth rate from 2025 to 2032, with increased use of third-party distributors and online medical device platforms for replenishing consumables or components, particularly in outpatient and ambulatory settings.

Coronary Intravascular Lithotripsy (IVL) Market Regional Analysis

- North America dominated the coronary intravascular lithotripsy (IVL) market with the largest revenue share of 43% in 2024, supported by advanced healthcare infrastructure, early technology adoption, and favorable reimbursement policies

- Healthcare providers in the region are increasingly integrating IVL into routine practice due to its favorable safety profile, ease of use in complex calcified lesions, and growing support from clinical guidelines and reimbursement policies

- This widespread adoption is further supported by the presence of key industry players, increased training initiatives, and high procedural volumes in tertiary care centers, positioning IVL as a preferred plaque modification technique across the U.S. and Canada

U.S. Coronary Intravascular Lithotripsy (IVL) Market Insight

The U.S. coronary intravascular lithotripsy (IVL) market captured the largest revenue share of 79% in 2024 within North America, driven by the high burden of calcified coronary artery disease and widespread use of advanced interventional technologies. The presence of leading healthcare institutions, early FDA approvals, and strong physician adoption of IVL systems such as those by Shockwave Medical are accelerating procedural uptake. In addition, favorable reimbursement policies and increased investment in training and education are contributing to market expansion.

Europe Coronary Intravascular Lithotripsy (IVL) Market Insight

The Europe coronary intravascular lithotripsy (IVL) market is projected to grow at a substantial CAGR throughout the forecast period, supported by increasing adoption of minimally invasive cardiovascular procedures and growing awareness of IVL’s safety and efficacy. The region's strong emphasis on clinical guidelines, rising PCI volumes, and widespread availability of advanced cath labs are enhancing market penetration. Both public and private healthcare sectors are integrating IVL for improved outcomes in complex calcified lesion treatments.

U.K. Coronary Intravascular Lithotripsy (IVL) Market Insight

The U.K. coronary intravascular lithotripsy (IVL) market is anticipated to grow at a noteworthy CAGR during the forecast period, propelled by the country’s adoption of evidence-based cardiovascular practices and national focus on reducing complication rates in coronary interventions. Growing concerns over long-term stent outcomes in calcified arteries are encouraging hospitals to utilize IVL technologies. NHS support for innovative interventional therapies and structured training programs are further strengthening market growth.

Germany Coronary Intravascular Lithotripsy (IVL) Market Insight

The Germany coronary intravascular lithotripsy (IVL) market is expected to expand at a considerable CAGR during the forecast period, driven by high clinical demand for calcium modification tools and a robust medical device infrastructure. Germany’s emphasis on advanced medical technologies, along with an increasing number of high-risk patients requiring complex PCI, is bolstering the adoption of IVL. Furthermore, the integration of IVL into procedural guidelines and its acceptance in leading cardiovascular centers are supporting its growing use.

Asia-Pacific Coronary Intravascular Lithotripsy (IVL) Market Insight

The Asia-Pacific coronary intravascular lithotripsy (IVL) market is poised to grow at the fastest CAGR of 23.6% during the forecast period of 2025 to 2032, driven by rising cardiovascular disease prevalence, rapid urbanization, and expanding access to interventional cardiology services in countries such as China, Japan, and India. Increasing healthcare expenditure, a growing middle-class population, and government investments in cardiac care infrastructure are propelling the adoption of IVL systems. The region is also witnessing a growing interest in innovative minimally invasive procedures.

Japan Coronary Intravascular Lithotripsy (IVL) Market Insight

The Japan coronary intravascular lithotripsy (IVL) market is gaining momentum due to the country’s advanced healthcare system, aging population, and emphasis on high-precision cardiovascular care. Japanese interventional cardiologists are increasingly using IVL for safer calcium modification, especially in elderly patients with multiple comorbidities. The integration of IVL into complex PCI strategies and its compatibility with Japan’s precision-driven approach to medicine are fueling market growth.

India Coronary Intravascular Lithotripsy (IVL) Market Insight

The India coronary intravascular lithotripsy (IVL) market accounted for the largest market revenue share in Asia Pacific in 2024, supported by the country’s expanding interventional cardiology capacity, increasing rates of CAD, and the growing adoption of advanced technologies in private and tertiary hospitals. As awareness of complex lesion treatment grows and access to training and affordable IVL systems improves, the Indian market is rapidly transitioning toward the adoption of next-generation plaque modification tools, such as IVL, especially in urban cardiac centers.

Coronary Intravascular Lithotripsy (IVL) Market Share

The Coronary Intravascular Lithotripsy (IVL) industry is primarily led by well-established companies, including:

- Shockwave Medical, Inc. (U.S.)

- Medtronic (Ireland)

- Boston Scientific Corporation (U.S.)

- Abbott (U.S.)

- B. Braun SE (Germany)

- Koninklijke Philips N.V. (Netherlands)

- Terumo Corporation (Japan)

- Biotronik SE & Co. KG (Germany)

- Cardiovascular Systems, Inc. (U.S.)

- Cordis Corporation (U.S.)

- MicroPort Scientific Corporation (China)

- Alvimedica (Turkey)

- Lepu Medical Technology (Beijing) Co., Ltd. (China)

- Acist Medical Systems, Inc. (U.S.)

- Blue Sail Medical Co., Ltd. (China)

- Meril Life Sciences Pvt. Ltd. (India)

- Sino Medical Sciences Technology Inc. (China)

- CardioFlow Medtech (China)

- Relisys Medical Devices Ltd. (India)

- AngioScore, Inc. (U.S.)

What are the Recent Developments in Global Coronary Intravascular Lithotripsy (IVL) Market?

- In April 2024, Shockwave Medical, Inc., the leading innovator in intravascular lithotripsy technology, announced the expansion of its global clinical training program with the launch of the "IVL Education Alliance." This initiative is aimed at enhancing physician proficiency and procedural outcomes through hands-on workshops and virtual training sessions. The program underscores Shockwave’s commitment to advancing interventional cardiology education and supporting broader adoption of IVL technology in complex coronary interventions worldwide

- In March 2024, Philips partnered with leading cardiovascular centers in Europe to conduct a multi-center clinical study evaluating the efficacy of its next-generation IVL system in treating peripheral artery disease (PAD). The study is designed to gather real-world data to support expanded indications and regulatory approvals. This move reflects the growing interest in IVL beyond coronary applications and highlights Philips' strategic focus on broadening its cardiovascular product portfolio

- In February 2024, Abiomed, now a part of Johnson & Johnson MedTech, announced its strategic collaboration with hospitals in Japan to integrate coronary IVL into high-risk PCI procedures involving Impella-supported patients. The initiative seeks to optimize outcomes in patients with severe calcified coronary lesions, particularly those with poor left ventricular function. This development signals the increasing synergy between mechanical circulatory support and calcium modification technologies

- In January 2024, CardioFlow Medtech received CE certification for its proprietary IVL balloon catheter, marking its official entry into the European market. This regulatory milestone enables the China-based company to expand internationally and meet the growing demand for innovative, minimally invasive calcium modification tools. The CE approval reflects the rising global interest in alternative IVL systems and increased competition in the segment

- In December 2023, Medtronic plc announced an early-stage investment in a start-up focused on next-generation intravascular lithotripsy platforms with dual-energy delivery capabilities. The collaboration aims to explore novel mechanisms for enhanced plaque modification in highly calcified lesions. This move highlights Medtronic’s strategic intent to diversify its interventional cardiology solutions and capitalize on the growing IVL market segment through innovation and targeted partnerships.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.