Global Craniopharyngioma Treatment Market

Market Size in USD Million

USD

600.50 Million

USD

957.10 Million

2024

2032

USD

600.50 Million

USD

957.10 Million

2024

2032

| 2025 - 2032 | |

| USD 600.50 Million | |

| USD 957.10 Million | |

| % | |

|

Craniopharyngioma Treatment Market Size

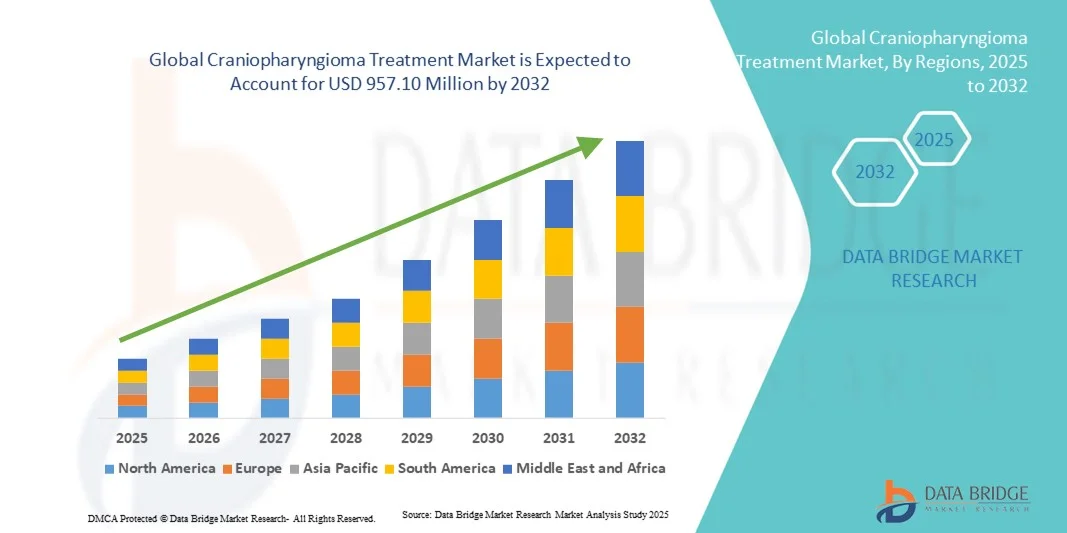

- The global craniopharyngioma treatment market size was valued at USD 600.50 Million in 2024 and is expected to reach USD 957.10 Million by 2032, at a CAGR of 6.00% during the forecast period

- The market growth is largely fueled by the growing advancements in diagnostic imaging technologies and the development of targeted therapies, leading to improved detection and treatment outcomes for patients with craniopharyngioma

- Furthermore, rising awareness of rare brain tumors, increasing investment in neuro-oncology research, and the availability of advanced surgical and radiotherapy techniques are driving the adoption of Craniopharyngioma Treatment solutions, thereby significantly boosting the industry's growth

Craniopharyngioma Treatment Market Analysis

- Craniopharyngioma Treatment, involving a multidisciplinary approach that includes surgery, radiation therapy, and pharmacological management, is becoming increasingly vital in improving survival rates and quality of life for patients affected by this rare benign brain tumor. Advancements in minimally invasive neurosurgery, targeted radiotherapy, and hormone replacement therapies are driving the market forward

- The rising prevalence of pituitary and hypothalamic disorders, coupled with growing awareness and improved diagnostic capabilities, is fueling demand for early and effective treatment options for craniopharyngioma across major healthcare markets

- North America dominated the craniopharyngioma treatment market with the largest revenue share of 41.7% in 2024, supported by advanced healthcare infrastructure, high diagnosis rates, and significant research funding in neuro-oncology. The U.S. continues to lead the region due to strong collaborations between hospitals, research institutions, and biotech companies focused on rare brain tumor therapies

- Asia-Pacific is expected to be the fastest-growing region in the craniopharyngioma treatment market during the forecast period, registering a CAGR of 10.2% from 2025 to 2032, driven by expanding access to specialized neurosurgical care, growing healthcare investments, and increasing awareness of pediatric brain tumor management

- The adamantinomatous craniopharyngioma segment dominated the market with a 67.4% share in 2024, owing to its higher prevalence among pediatric patients and the complex management associated with cystic formations

Report Scope and Craniopharyngioma Treatment Market Segmentation

|

Attributes |

Craniopharyngioma Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Craniopharyngioma Treatment Market Trends

Advancements in Targeted Therapies and Personalized Treatment Approaches

- A significant and accelerating trend in the global craniopharyngioma treatment market is the growing focus on precision medicine and targeted therapeutic strategies aimed at improving clinical outcomes and minimizing adverse effects. Pharmaceutical companies and research institutes are investing heavily in developing novel therapies that address the complex molecular pathways involved in tumor growth and recurrence

- For instance, several institutions are exploring the role of targeted agents such as BRAF and MEK inhibitors for papillary craniopharyngioma, offering promising outcomes in patients with BRAF V600E mutations. Similarly, immunotherapy-based approaches and advancements in proton beam radiotherapy are gaining traction as viable alternatives to conventional surgical methods

- Recent clinical studies have shown that the integration of genomic profiling in treatment planning enables clinicians to design more personalized therapy regimens that optimize efficacy while reducing treatment-related complications

- The use of AI-driven diagnostic tools and imaging analytics is also enhancing precision in tumor localization and surgical navigation, thereby reducing risks and improving postoperative outcomes. In addition, radiogenomic techniques are being adopted to better predict tumor behavior and patient response to treatment

- Furthermore, research collaborations among major oncology centers are accelerating the development of targeted drugs and advanced radiation technologies, fostering a more patient-specific treatment environment

- This trend toward personalized and targeted medicine is reshaping how clinicians approach craniopharyngioma management, shifting from traditional, one-size-fits-all treatments to a more sophisticated, data-driven therapeutic model that emphasizes safety, accuracy, and long-term disease control

Craniopharyngioma Treatment Market Dynamics

Driver

Rising Prevalence and Advancements in Diagnostic Imaging Technologies

- The increasing incidence of craniopharyngioma, particularly among pediatric and young adult populations, coupled with enhanced diagnostic imaging modalities, is a major driver of market growth

- For instance, in May 2023, Elekta introduced advancements in its MR-guided radiotherapy platform, enabling superior visualization of intracranial tumors like craniopharyngioma during treatment. Such innovations are expanding clinical precision and supporting treatment efficacy

- As awareness of early diagnosis and access to multidisciplinary care improves, healthcare systems are prioritizing advanced neurosurgical and radiation-based therapies, propelling market demand

- Furthermore, the growing adoption of hybrid treatment approaches—combining surgery, radiotherapy, and pharmacological intervention—is enhancing overall survival rates and improving patient quality of life

- The rise in global healthcare expenditure and the presence of dedicated neuro-oncology centers are also contributing significantly to market expansion, as they provide patients with access to cutting-edge therapeutic options and expert clinical management

- Advancements in minimally invasive neurosurgical tools and real-time imaging-guided techniques further enable safer tumor resection, reducing postoperative complications and accelerating recovery

Restraint/Challenge

Complex Disease Management and High Treatment Costs

- Managing craniopharyngioma presents unique challenges due to its proximity to critical brain structures and the high risk of postoperative complications such as hormonal imbalances, vision impairment, and cognitive decline. These complexities often lead to prolonged treatment cycles and increased healthcare costs

- For instance, high-profile clinical studies have reported that despite surgical success, patients frequently require lifelong endocrinological monitoring and hormone replacement therapy, adding to the financial burden of long-term care

- Addressing these management challenges requires a multidisciplinary approach involving neurosurgeons, endocrinologists, oncologists, and radiologists. However, such specialized care may not be readily available in resource-limited regions, restricting access to advanced treatment options

- Moreover, the high cost associated with proton beam therapy and targeted biological agents limits their adoption among low- and middle-income populations. Insurance coverage gaps for emerging therapies further exacerbate affordability issues

- While ongoing research aims to simplify treatment regimens and reduce costs, the intricate nature of craniopharyngioma care continues to pose significant challenges to healthcare providers

- Overcoming these barriers through improved global access to advanced treatment technologies, increased clinical funding, and broader insurance inclusion will be essential for sustaining market growth

Craniopharyngioma Treatment Market Scope

The market is segmented on the basis of symptom, cause, diagnosis, route of administration, and distribution channel.

- By Symptom

On the basis of symptom, the Craniopharyngioma Treatment market is segmented into pituitary gland dysfunction, hypothalamic dysfunction, optic nerves and optic chiasm compression, and foramen of Monro occlusion. The pituitary gland dysfunction segment dominated the largest market revenue share of 38.5% in 2024, driven by the increasing number of patients developing hormonal imbalance due to tumor compression on the pituitary gland. This leads to lifelong dependency on hormone replacement therapies including growth hormone, thyroid, and cortisol supplementation. The availability of advanced hormonal therapies and improved endocrinological monitoring tools contributes to the segment’s dominance. Furthermore, the rising awareness regarding early hormonal assessments, the introduction of novel hormone analogs, and an increase in pituitary-targeted treatment protocols in leading hospitals have strengthened segment growth. The adoption of multidisciplinary treatment approaches combining surgery, radiotherapy, and endocrinology care continues to make this the most critical and revenue-generating segment in the Craniopharyngioma Treatment market.

The hypothalamic dysfunction segment is projected to witness the fastest growth with a CAGR of 9.8% from 2025 to 2032, primarily driven by the increasing recognition of hypothalamic syndromes such as obesity, thermoregulation issues, and sleep disturbances in post-treatment patients. The focus on preserving hypothalamic integrity during surgical resection and the introduction of neuroprotective drugs are promoting faster growth. Moreover, advancements in neuroimaging, ongoing clinical trials targeting hypothalamic injury repair, and specialized rehabilitation programs for behavioral and metabolic disorders are expanding this segment. Increasing patient awareness about neurological recovery therapies and supportive care innovations will further boost its rapid growth in the coming years.

- By Cause

On the basis of cause, the Craniopharyngioma Treatment market is segmented into adamantinomatous craniopharyngioma and papillary craniopharyngioma. The adamantinomatous craniopharyngioma segment dominated the market with a 67.4% share in 2024, owing to its higher prevalence among pediatric patients and the complex management associated with cystic formations. The segment benefits from increased funding in pediatric neuro-oncology research and the availability of targeted therapies for CTNNB1 mutations. In addition, the growing number of pediatric surgical interventions, advancements in cyst decompression techniques, and improved long-term survival rates after surgery contribute to this segment’s leading position. Enhanced post-operative care, hormone replacement therapy advancements, and focus on quality-of-life improvement for children have also sustained the dominance of adamantinomatous cases across leading medical centers globally.

The papillary craniopharyngioma segment is estimated to grow at the fastest CAGR of 10.2% from 2025 to 2032, driven by increased diagnosis among adult patients and the emergence of targeted precision therapies. Innovations in molecular oncology have identified BRAF V600E and MEK mutation targets, leading to effective personalized treatments such as BRAF inhibitors that significantly reduce tumor recurrence. The growing number of clinical trials and FDA approvals for targeted agents in adult craniopharyngioma, combined with less invasive treatment methods, are fueling this growth. Moreover, increasing awareness of molecular diagnostics and favorable therapeutic outcomes in papillary variants continue to attract investment and development in this rapidly expanding segment.

- By Diagnosis

On the basis of diagnosis, the Craniopharyngioma Treatment market is segmented into clinical history and physical exam, laboratory tests, and imaging. The imaging segment dominated the largest revenue share of 54.1% in 2024, attributed to the indispensable role of imaging in early tumor detection, localization, and surgical guidance. MRI and CT remain gold-standard modalities for defining tumor boundaries, cystic structures, and involvement of adjacent brain regions. Technological advancements such as functional MRI, intraoperative navigation, and 3D reconstruction imaging are revolutionizing precision surgery and postoperative evaluation. Moreover, the integration of AI in imaging analysis enhances diagnostic accuracy, supporting this segment’s leadership. The continuous demand for sophisticated neuroimaging systems in major hospitals and cancer centers ensures the segment’s consistent dominance.

The laboratory tests segment is expected to record the fastest growth at a CAGR of 8.9% from 2025 to 2032, driven by the increasing use of endocrine testing and genetic screening to detect hormone deficiencies and mutations linked to tumor behavior. The rising adoption of advanced molecular assays and biomarker profiling supports early and precise diagnosis. Ongoing research in genetic mapping, coupled with the rise of personalized medicine approaches, has accelerated growth. The use of laboratory diagnostics in pre- and post-surgical monitoring and long-term hormone therapy management is also fueling segment expansion during the forecast period.

- By Route of Administration

On the basis of route of administration, the Craniopharyngioma Treatment market is segmented into oral, injection, and transdermal. The oral segment held the largest share of 45.6% in 2024, primarily due to the extensive use of oral hormone replacement therapies and corticosteroids in long-term disease management. Patients with pituitary or hypothalamic dysfunction often require continuous oral medication for hormonal stabilization. The convenience of self-administration, availability of various formulations, and improved patient adherence drive this segment’s dominance. Pharmaceutical innovation in sustained-release oral hormone products and combination therapies also boosts growth. In addition, affordability and easy accessibility through hospital and retail pharmacies sustain the widespread use of oral treatments in global markets.

The injection segment is projected to grow at the fastest CAGR of 9.4% from 2025 to 2032, fueled by the rising adoption of injectable biologics, targeted immunotherapies, and long-acting hormonal agents. The demand for precision dosing, immediate bioavailability, and higher therapeutic efficiency supports the use of injectable forms in clinical settings. Increasing introduction of depot formulations, peptide-based therapies, and growth hormone injectables is further driving this segment. Moreover, hospital-based administration for critical cases and improved patient outcomes in complex hormonal treatments are accelerating its growth trajectory.

- By Distribution Channel

On the basis of distribution channel, the Craniopharyngioma Treatment market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with a share of 52.8% in 2024, attributed to the strong reliance on hospital-based care for diagnosis, surgical intervention, and hormone therapy management. Hospitals serve as primary points of distribution for complex drug regimens, biologics, and post-surgical maintenance medications. The increasing presence of specialized neuroendocrinology units and integrated treatment centers ensures timely drug availability, driving segment dominance. In addition, the role of hospital pharmacies in supporting clinical trials and oncology drug management strengthens their market position globally.

The online pharmacy segment is forecasted to register the fastest CAGR of 10.7% from 2025 to 2032, supported by the digital transformation of healthcare and rising preference for convenient home-based treatment options. Online pharmacies are witnessing increased demand for maintenance drugs, hormone therapies, and post-operative medications. The availability of verified online platforms offering home delivery, automatic prescription refills, and patient support tools enhances accessibility. Furthermore, increasing collaborations between pharmaceutical manufacturers and e-pharmacy providers and the expansion of telemedicine platforms are key drivers for this segment’s rapid growth across emerging and developed markets.

Craniopharyngioma Treatment Market Regional Analysis

- North America dominated the craniopharyngioma treatment market with the largest revenue share of 41.7% in 2024, supported by advanced healthcare infrastructure, high diagnosis rates, and significant research funding in neuro-oncology

- The region’s well-established hospital systems, cutting-edge diagnostic imaging facilities, and presence of specialized neurosurgical centers have contributed to superior patient outcomes. Furthermore, the growing number of pediatric brain tumor registries, the availability of multidisciplinary treatment programs, and continuous innovation in hormone replacement and radiotherapy techniques have strengthened North America’s market leadership

- Collaboration between academic institutions, biotechnology firms, and clinical research organizations is accelerating the development of targeted therapies and precision medicine approaches for craniopharyngioma

U.S. Craniopharyngioma Treatment Market Insight

The U.S. craniopharyngioma treatment market captured the largest revenue share in 2024 within North America, driven by the presence of leading neurosurgery and endocrinology centers such as Mayo Clinic, Johns Hopkins, and Massachusetts General Hospital. The nation benefits from advanced diagnostic platforms, a robust clinical trial ecosystem, and strong government support for rare disease research. Continuous investment in imaging innovations, such as intraoperative MRI, and the growing use of stereotactic radiosurgery techniques have enhanced treatment precision. Additionally, the introduction of patient-centered hormonal management programs and long-term rehabilitation services has elevated the U.S. as the epicenter for craniopharyngioma treatment advancements.

Europe Craniopharyngioma Treatment Market Insight

The Europe craniopharyngioma treatment market is expected to grow steadily at a healthy CAGR throughout the forecast period, fueled by government-backed healthcare reforms, expanded neurosurgical capacities, and improved rare tumor diagnosis rates. The adoption of minimally invasive surgical methods and advanced imaging for early detection is gaining traction across major European countries. National health systems increasingly focus on post-treatment endocrinological rehabilitation and long-term quality-of-life management. Additionally, ongoing collaborations under European Reference Networks (ERNs) for rare neurological disorders are fostering data sharing and treatment innovation across borders, sustaining Europe’s strong growth momentum.

U.K. Craniopharyngioma Treatment Market Insight

The U.K. craniopharyngioma treatment market is projected to grow at a noteworthy CAGR during the forecast period, supported by the National Health Service’s (NHS) focus on early tumor detection and integrated patient management. The country has made significant progress in establishing specialized pediatric neuro-oncology units and investing in digital health platforms for post-surgical follow-up. The increasing prevalence of clinical trials and government initiatives for rare disease therapies have strengthened the treatment landscape. Moreover, public–private partnerships are advancing the availability of targeted and hormone-based therapies, positioning the U.K. as a key hub for innovation in craniopharyngioma care.

Germany Craniopharyngioma Treatment Market Insight

The Germany craniopharyngioma treatment market is anticipated to expand at a strong CAGR over the forecast period, driven by the nation’s advanced neurosurgical infrastructure and consistent focus on precision diagnostics. German hospitals are early adopters of hybrid operating rooms, integrating intraoperative MRI and neuronavigation systems for safer tumor resections. The presence of well-funded research institutions and favorable reimbursement policies for rare disease treatment supports steady growth. Furthermore, Germany’s emphasis on integrating post-treatment endocrine and psychological rehabilitation enhances patient recovery outcomes, reinforcing its position as one of Europe’s leading treatment markets.

Asia-Pacific Craniopharyngioma Treatment Market Insight

The Asia-Pacific craniopharyngioma treatment market is poised to register the fastest growth, recording a CAGR of 10.2% from 2025 to 2032, driven by expanding access to specialized neurosurgical care, rising healthcare investments, and growing awareness of pediatric brain tumor management. The region is witnessing rapid improvements in medical infrastructure and availability of advanced imaging modalities across China, Japan, and India. Government initiatives for rare disease funding, combined with the establishment of neuro-oncology training centers, are boosting diagnosis and treatment capabilities. The rising prevalence of childhood brain tumors and expansion of tertiary care hospitals are further contributing to regional market acceleration.

Japan Craniopharyngioma Treatment Market Insight

The Japan craniopharyngioma treatment market is gaining strong momentum due to the country’s high standards in precision medicine, early diagnosis, and post-treatment rehabilitation. The presence of technologically advanced hospitals, coupled with nationwide rare disease support programs, ensures superior patient management. Research on long-term cognitive and hormonal outcomes after tumor resection is driving therapeutic innovation. Japan’s investment in proton therapy and AI-based diagnostic systems, alongside growing government funding for pediatric oncology, continues to propel its market expansion through the forecast period.

China Craniopharyngioma Treatment Market Insight

The China craniopharyngioma treatment market accounted for the largest revenue share in Asia-Pacific in 2024, fueled by rapid healthcare modernization, expansion of neurosurgical departments in major hospitals, and growing awareness of early tumor intervention. The Chinese government’s emphasis on improving rare disease treatment accessibility and its investment in diagnostic infrastructure are key growth drivers. Moreover, domestic pharmaceutical innovation in hormone therapies, increased clinical research participation, and strategic collaborations with international hospitals are accelerating the country’s leadership within the regional market. With its vast patient pool and strong policy backing, China remains a critical growth engine for the Asia-Pacific

Craniopharyngioma Treatment Market Share

The Craniopharyngioma Treatment industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Merck & Co., Inc. (U.S.)

- Lilly (U.S.)

- Bayer AG (Germany)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

- Amgen Inc. (U.S.)

- Sanofi (France)

- Takeda Pharmaceutical Company Limited (Japan)

- Ipsen Pharma (France)

- Sun Pharmaceutical Industries Ltd. (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

- AbbVie Inc. (U.S.)

- GSK plc (U.K.)

- AstraZeneca plc (U.K.)

- Johnson & Johnson and its affiliates (U.S.)

- Ferring Pharmaceuticals (Switzerland)

- Ono Pharmaceutical Co., Ltd. (Japan)

- Novocure Ltd. (Jersey)

Latest Developments in Global Craniopharyngioma Treatment Market

- In August 2023, a clinical trial reported that the combination of vemurafenib and cobimetinib substantially reduced tumor size in patients with papillary craniopharyngioma harboring the BRAF V600E mutation, allowing many to avoid immediate surgery or radiation

- In December 2024, researchers published a single-cell RNA sequencing study that detailed the tumor microenvironment in both adamantinomatous and papillary craniopharyngioma subtypes, identifying immune signatures and fibroblast-tumor cell interactions that may lead to novel targeted therapies

- In February 2024, a publication recommended a change in surgical strategy for craniopharyngioma management: moving from aggressive total resection toward subtotal resection followed by adjuvant radiation or systemic therapy to preserve hypothalamic and pituitary function, reflecting evolving treatment standards

- In March 2025, a review of ongoing clinical trials highlighted that multiple new systemic therapies — including MEK inhibitors, PD-1 checkpoint inhibitors, and WNT pathway inhibitors — are actively being investigated in craniopharyngioma, marking a shift toward precision-medicine treatment paradigms

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.