Global Craniosynostosis Treatment Market

Market Size in USD Million

USD

567.37 Million

USD

918.04 Million

2024

2032

USD

567.37 Million

USD

918.04 Million

2024

2032

| 2025 - 2032 | |

| USD 567.37 Million | |

| USD 918.04 Million | |

| % | |

|

Craniosynostosis Treatment Market Size

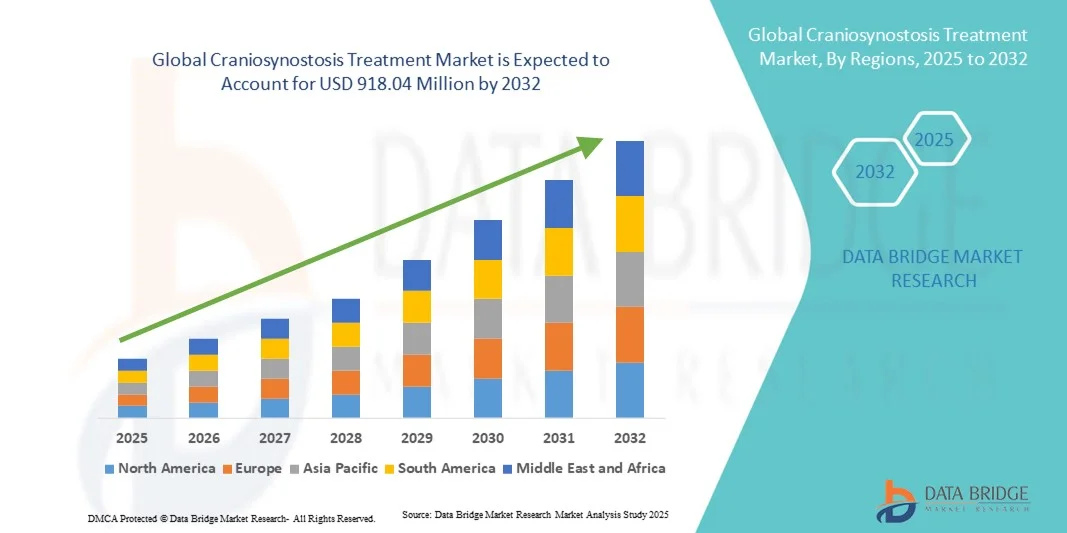

- The global craniosynostosis treatment market size was valued at USD 567.37 Million in 2024 and is expected to reach USD 918.04 Million by 2032, at a CAGR of 6.20% during the forecast period

- The market growth is largely fueled by increasing awareness, early diagnosis, and technological advancements in surgical and non-surgical treatment options for craniosynostosis. Improvements in minimally invasive surgical techniques, 3D imaging, and cranial remodeling devices are enhancing treatment outcomes, driving significant growth within the craniosynostosis treatment market

- Furthermore, rising collaborations between healthcare providers, research institutions, and medical device companies are accelerating the development of innovative treatment solutions. Growing investment in pediatric healthcare, supportive government initiatives, and better access to specialized craniofacial care are further contributing to market expansion. These converging factors are establishing craniosynostosis treatment as a critical area of focus in pediatric healthcare, thereby significantly boosting the industry’s growth

Craniosynostosis Treatment Market Analysis

- Craniosynostosis Treatment, involving surgical interventions and innovative therapeutic techniques to correct premature fusion of cranial sutures, is increasingly vital in improving functional and aesthetic outcomes in affected children. Advancements in minimally invasive procedures, endoscopic surgeries, and patient-specific surgical planning have enhanced treatment safety and effectiveness

- The escalating demand for craniosynostosis treatment is primarily fueled by rising awareness among parents, increased prenatal and postnatal screening, growing healthcare infrastructure, and advancements in pediatric neurosurgery and craniofacial surgery techniques

- North America dominated the craniosynostosis treatment market with the largest revenue share of 41.3% in 2024, supported by advanced healthcare infrastructure, high adoption of minimally invasive surgical procedures, and the presence of leading pediatric neurosurgery centers. The U.S. accounted for the majority of the market growth, driven by technological innovations in image-guided surgery and 3D surgical planning, as well as increased public and private funding for rare craniofacial disorder treatments

- Asia-Pacific is expected to be the fastest-growing region in the craniosynostosis treatment market during the forecast period, with a projected CAGR from 2025 to 2032, due to increasing urbanization, rising disposable incomes, expansion of pediatric healthcare facilities, and growing awareness of early cranial deformity diagnosis and intervention

- The Surgery segment dominated the market with 82.1% share in 2024, as corrective surgical procedures remain the primary treatment for craniosynostosis

Report Scope and Craniosynostosis Treatment Market Segmentation

|

Attributes |

Craniosynostosis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Craniosynostosis Treatment Market Trends

Enhanced Convenience Through Advanced Treatment Approaches

- A significant and accelerating trend in the global craniosynostosis treatment market is the increasing adoption of advanced therapeutic approaches, including minimally invasive surgical techniques, precision cranial reconstruction, and regenerative medicine. These innovations are significantly improving patient outcomes, reducing recovery times, and enhancing overall treatment efficiency

- For instance, the use of endoscopic-assisted cranial surgery allows surgeons to correct cranial deformities with smaller incisions and minimal blood loss, offering patients faster healing and reduced hospitalization periods. Similarly, the development of patient-specific cranial implants and 3D-printed surgical guides provides more accurate and personalized treatment solutions

- Integration of advanced imaging techniques and computational modeling in preoperative planning enables surgeons to better predict outcomes, reduce complications, and optimize cranial reconstruction procedures. For example, 3D CT and MRI-based surgical planning allow precise evaluation of cranial sutures and skull shape, improving surgical accuracy. Furthermore, regenerative therapies such as stem cell applications and bone graft substitutes are facilitating tissue regeneration and long-term cranial stability in affected patients

- The implementation of multidisciplinary treatment teams combining neurosurgery, craniofacial surgery, and pediatric care allows for coordinated management of complex craniosynostosis cases. Through comprehensive planning and follow-up, patients benefit from integrated care pathways that reduce treatment risks and enhance recovery

- This trend toward more advanced, precise, and patient-centered treatment strategies is fundamentally reshaping expectations in craniofacial care. Consequently, hospitals and specialty centers are increasingly adopting innovative craniosynostosis treatment protocols that combine surgical precision, advanced imaging, and regenerative techniques

- The demand for these advanced craniosynostosis treatment solutions is growing rapidly across both pediatric and adult patient populations, as healthcare providers increasingly prioritize treatment effectiveness, safety, and long-term outcomes

Craniosynostosis Treatment Market Dynamics

Driver

Growing Need Due to Rising Awareness and Advancements in Surgical Techniques

- The increasing prevalence of cranial deformities among infants, coupled with growing awareness among parents and healthcare providers, is a significant driver for the heightened demand for craniosynostosis treatment

- For instance, in April 2024, a leading pediatric hospital announced the successful implementation of minimally invasive endoscopic cranial reconstruction combined with patient-specific implant technology, demonstrating improved outcomes in early-stage craniosynostosis cases. Such advancements by key healthcare institutions are expected to drive the craniosynostosis treatment industry growth in the forecast period

- As patients and caregivers become more aware of the benefits of early intervention, advanced surgical techniques, and precision treatment planning, craniosynostosis treatment solutions are increasingly preferred over traditional corrective approaches

- Furthermore, the growing focus on multidisciplinary care and the increasing availability of specialized craniofacial centers are making advanced craniosynostosis treatments more accessible to a wider patient population

- The ability to achieve optimal cranial symmetry, minimize complications, and improve aesthetic outcomes are key factors propelling the adoption of advanced craniosynostosis treatments. The trend towards early diagnosis through advanced imaging and patient-specific surgical planning further contributes to market growth

Restraint/Challenge

Concerns Regarding Treatment Costs and Limited Access to Specialized Care

- The relatively high cost of advanced craniosynostosis treatments, including minimally invasive surgeries and custom implants, poses a significant challenge to broader market penetration. Many patients, especially in developing regions, may not have access to specialized craniofacial centers or insurance coverage for complex procedures

- For instance, the expense associated with 3D-printed cranial implants or advanced regenerative therapies can limit accessibility for price-sensitive families, slowing adoption in certain regions

- Addressing these challenges through government support, insurance coverage expansion, and development of cost-effective treatment solutions is crucial for improving patient access. Leading hospitals and research institutions are focusing on optimizing surgical workflows and reducing material costs to make advanced treatments more affordable

- In addition, the limited number of trained craniofacial surgeons and specialized facilities in certain regions can hinder timely treatment, emphasizing the need for healthcare infrastructure development and training programs

- While treatment costs are gradually decreasing with technology advancements, affordability remains a critical barrier, particularly in low- and middle-income countries

- Overcoming these challenges through expanded access to care, cost optimization, and patient education will be vital for sustained growth in the craniosynostosis treatment market

Craniosynostosis Treatment Market Scope

The market is segmented on the basis of disease type, cause, product type, treatment type, end user, and distribution channel.

- By Disease Type

On the basis of disease type, the market is segmented into Sagittal Synostosis, Coronal Craniosynostosis, Metopic Synostosis, and Lambdoid Synostosis. The Sagittal Synostosis segment dominated the largest market revenue share of 39.5% in 2024, driven by its higher prevalence among craniosynostosis cases. The segment benefits from increasing awareness about early diagnosis, improved surgical procedures like cranial vault remodeling and endoscopic strip craniectomy, and advancements in patient-specific implants. Hospitals and specialty clinics prefer sagittal synostosis surgeries due to predictable outcomes, reduced operative time, and shorter post-operative recovery. Rising adoption of minimally invasive techniques has further strengthened this segment. North America continues to lead this market, with state-of-the-art pediatric neurosurgery centers and strong healthcare infrastructure. Research collaborations between universities and hospitals are driving innovation in surgical planning and post-operative care. Insurance coverage and government support in key countries also contribute to its dominance. In addition, digital imaging, 3D modeling, and navigation-assisted surgeries improve surgical accuracy and patient outcomes.

The Coronal Craniosynostosis segment is anticipated to witness the fastest CAGR of 10.2% from 2025 to 2032, driven by increasing prenatal diagnosis and parental awareness. This form often requires more complex surgical planning, and the rising adoption of 3D-printed cranial implants and navigation-assisted surgeries supports market growth. The segment benefits from technological advancements such as intraoperative imaging and patient-specific surgical guides, which enhance outcomes for single and multi-suture coronal cases. Expansion in emerging markets is fueled by the establishment of specialized pediatric neurosurgery centers. Government initiatives for rare congenital disorders and improved post-operative care protocols also contribute to faster growth. Early detection programs and collaborations between genetic testing centers and hospitals help in timely intervention. Surgeons increasingly prefer minimally invasive endoscopic procedures combined with postoperative helmet therapy, enhancing aesthetic and functional results.

- By Cause

On the basis of cause, the market is segmented into Syndromic Craniosynostosis and Nonsyndromic Craniosynostosis. The Nonsyndromic Craniosynostosis segment dominated the market with a revenue share of 61.4% in 2024, due to the high incidence of single-suture cases that are easier to treat surgically. Hospitals and specialty clinics favor this segment because it allows for standardized surgical procedures with predictable recovery timelines. Minimally invasive surgeries, including endoscopic strip craniectomy, are widely adopted for nonsyndromic cases. North America leads the market, supported by advanced pediatric neurosurgery facilities and established post-operative care systems. The segment benefits from increased awareness campaigns and early screening programs in major healthcare markets. Technological adoption, including intraoperative navigation and 3D cranial modeling, supports higher success rates and patient satisfaction. Partnerships between medical device companies and hospitals for cranial implants also strengthen the segment’s dominance. Rising healthcare expenditure and insurance coverage enhance treatment accessibility globally.

The Syndromic Craniosynostosis segment is expected to register the fastest CAGR of 11.0% from 2025 to 2032, driven by rising identification of genetic syndromes, complex multi-suture involvement, and growing demand for specialized care. This segment benefits from multidisciplinary surgical approaches and innovations like patient-specific implants and robotic-assisted surgeries. Expansion in Asia-Pacific and Latin America is fueled by improved healthcare access and awareness. Genetic testing centers increasingly collaborate with hospitals for early detection, enabling timely surgical intervention. Emerging telemedicine applications allow monitoring post-surgery, supporting faster adoption. Government and private funding for rare disorders enhance treatment availability. Advanced craniofacial centers and training programs for surgeons accelerate market growth.

- By Product Type

On the basis of product type, the market is segmented into Single Suture, Double Suture, and Complex Multi Suture. The Single Suture segment dominated the market with a revenue share of 46.8% in 2024, driven by the high occurrence of single-suture involvement and straightforward surgical correction. Hospitals and specialty clinics prefer single-suture procedures due to lower complication rates and faster recovery. Minimally invasive techniques, endoscopic surgeries, and 3D surgical planning are widely applied, improving patient outcomes. North America and Europe are the key markets, supported by advanced pediatric neurosurgery infrastructure. Partnerships between research institutions and hospitals enhance innovation in patient-specific implants and surgical instruments. Insurance coverage and government health programs provide better treatment access. Parental awareness and early diagnosis programs contribute to higher adoption. Standardized protocols and surgical guidelines improve treatment success rates. Technological adoption, including digital imaging and navigation-assisted procedures, strengthens dominance.

The Complex Multi Suture segment is expected to witness the fastest CAGR of 10.5% from 2025 to 2032, driven by advancements in surgical planning and customized implants for multi-suture involvement. Growth is supported by rising syndromic craniosynostosis cases, especially in emerging regions. Patient-specific 3D-printed implants, intraoperative imaging, and multidisciplinary surgical approaches enhance outcomes. Expansion of pediatric craniofacial centers in Asia-Pacific contributes to adoption. Genetic testing and early diagnosis initiatives improve treatment success. Surgeons increasingly use minimally invasive endoscopic techniques combined with postoperative helmet therapy. Government and private funding for rare disorders facilitate market growth. Partnerships between medical device companies and hospitals accelerate innovation. Awareness campaigns for parents and caregivers promote early intervention.

- By Treatment Type

On the basis of treatment type, the market is segmented into Surgery and Drugs. The Surgery segment dominated the market with 82.1% share in 2024, as corrective surgical procedures remain the primary treatment for craniosynostosis. Hospitals and specialty clinics favor surgical intervention due to effective functional and aesthetic outcomes. Adoption of minimally invasive surgery, cranial vault remodeling, and navigation-assisted procedures has increased success rates. North America and Europe lead due to strong pediatric neurosurgery infrastructure and highly skilled surgeons. Research on patient-specific implants and pre-surgical 3D planning continues to improve results. Insurance coverage supports higher treatment adoption. Parental awareness, early diagnosis programs, and post-operative care protocols strengthen the segment. Multidisciplinary surgical teams enhance outcomes and reduce complications. Telemedicine and follow-up care facilitate broader treatment access. Technological advances in imaging and surgical navigation improve precision and recovery.

The Drugs segment is expected to register the fastest CAGR of 9.3% from 2025 to 2032, primarily driven by adjunctive medications for post-surgical recovery and management of syndromic conditions. Growth is fueled by increasing awareness of supportive therapies and pharmaceutical innovations. Emerging markets are witnessing higher adoption due to improved healthcare access. Hospital pharmacies and specialty clinics play a key role in distribution. Clinical trials and research initiatives for supportive drugs enhance market growth. Rising parental awareness about post-operative care and rehabilitation contributes to adoption. Telemedicine platforms allow monitoring drug efficacy remotely. Combination therapies with surgery improve patient outcomes. Government health programs and insurance schemes facilitate access.

- By End User

On the basis of end user, the market is segmented into Hospitals, Specialty Clinics, and Others. The Hospitals segment dominated the market with 69.2% share in 2024, due to advanced surgical facilities, multidisciplinary teams, and comprehensive post-operative care for craniosynostosis patients. Hospitals handle the majority of complex surgeries, including multi-suture and syndromic cases. North America and Europe dominate due to infrastructure and availability of skilled pediatric neurosurgeons. High adoption of minimally invasive and endoscopic techniques improves outcomes. Early diagnosis programs and parental awareness initiatives increase patient inflow. Insurance coverage facilitates treatment access. Partnerships between hospitals and research institutions drive innovation in surgical instruments and implants. Technological adoption, such as 3D surgical planning, enhances precision. Standardized post-operative care protocols improve patient satisfaction. Expansion of hospital networks in emerging economies supports dominance.

The Specialty Clinics segment is expected to witness the fastest CAGR of 10.7% from 2025 to 2032, driven by the establishment of dedicated craniofacial centers and personalized treatment approaches. Growth is fueled by telemedicine integration, early diagnosis programs, and increasing parental awareness. Clinics provide multidisciplinary care, including genetic counseling, surgery, and rehabilitation. Emerging regions in Asia-Pacific and Latin America are witnessing rapid adoption. Specialized surgical teams and advanced imaging technologies enhance treatment outcomes. Partnerships with research institutions support innovation. Government initiatives for rare congenital disorders improve access. Adoption of minimally invasive and navigation-assisted surgeries increases clinic preference. Training programs for surgeons expand capacity and improve outcomes.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Direct Tender, Retail Sales, and Others. The Direct Tender segment dominated with 52.5% share in 2024, as hospitals and government institutions procure surgical instruments, implants, and cranial orthoses through institutional tenders. Large-scale procurement ensures availability of advanced surgical tools and implants for both single-suture and multi-suture cases. North America and Europe lead due to structured government procurement systems. Partnerships between suppliers and healthcare institutions improve supply chain efficiency. Hospitals benefit from bulk procurement, reducing costs and ensuring timely delivery. Adoption of advanced surgical instruments and implants supports dominance. Awareness programs for caregivers and healthcare providers increase tender utilization. Training programs for surgeons ensure effective use of instruments. Insurance coverage enables institutional procurement. Emerging markets are gradually increasing reliance on direct tenders for craniosynostosis treatments.

The Retail Sales segment is expected to register the fastest CAGR of 9.8% from 2025 to 2032, driven by increasing availability of cranial orthoses and post-surgical care devices for home use. Caregivers and parents are adopting retail solutions for helmet therapy and rehabilitation. Growth is fueled by rising parental awareness, e-commerce penetration, and improved distribution networks in emerging markets. Specialty medical stores provide access to post-operative devices. Telemedicine support ensures proper device usage and monitoring. Expansion of pediatric care centers encourages adoption. Government health programs support retail availability. Technological innovations in orthoses improve comfort and effectiveness. Online platforms provide convenient access, boosting growth.

Craniosynostosis Treatment Market Regional Analysis

- North America dominated the craniosynostosis treatment market with the largest revenue share of 41.3% in 2024

- Supported by advanced healthcare infrastructure, high adoption of minimally invasive surgical procedures, and the presence of leading pediatric neurosurgery centers

- The market accounted for the majority of the market growth, driven by technological innovations in image-guided surgery and 3D surgical planning, as well as increased public and private funding for rare craniofacial disorder treatments

U.S. Craniosynostosis Treatment Market Insight

The U.S craniosynostosis treatment market captured the largest revenue share in North America in 2024, fueled by rapid advancements in surgical techniques, increased availability of specialized pediatric craniofacial centers, and the integration of preoperative planning technologies. Hospitals and specialty clinics are increasingly adopting minimally invasive endoscopic procedures and patient-specific cranial implants to enhance surgical precision and reduce recovery time. Growing awareness among parents and caregivers regarding early diagnosis and intervention is further propelling market growth.

Europe Craniosynostosis Treatment Market Insight

The Europe craniosynostosis treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by well-established healthcare infrastructure, increasing investments in pediatric surgical programs, and rising awareness of craniofacial disorders. Countries such as Germany, France, and the U.K. are witnessing increased adoption of advanced surgical procedures and multidisciplinary treatment approaches. The region is experiencing significant growth across hospitals and specialty clinics, with early diagnosis and precision surgery becoming increasingly standard in both new and existing healthcare facilities.

U.K. Craniosynostosis Treatment Market Insight

The U.K. craniosynostosis treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the growing emphasis on early diagnosis, enhanced surgical capabilities, and improved access to specialized pediatric care. Rising awareness among healthcare professionals and parents regarding cranial deformities is encouraging the adoption of minimally invasive and image-guided surgical interventions. The U.K.’s well-established healthcare system and collaborative research initiatives are expected to continue supporting market growth.

Germany Craniosynostosis Treatment Market Insight

The Germany craniosynostosis treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by the presence of advanced healthcare infrastructure, high investment in pediatric neurosurgery, and the increasing adoption of precision cranial reconstruction techniques. Germany’s emphasis on innovation, patient safety, and multidisciplinary care promotes the availability of advanced treatment options for craniofacial disorders. Hospitals and specialty clinics are integrating 3D imaging, preoperative modeling, and minimally invasive approaches to optimize outcomes for patients.

Asia-Pacific Craniosynostosis Treatment Market Insight

The Asia-Pacific craniosynostosis treatment market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing urbanization, rising disposable incomes, expansion of pediatric healthcare facilities, and growing awareness of early cranial deformity diagnosis and intervention. Countries such as China, Japan, and India are witnessing rapid development in specialized pediatric centers, enhanced access to advanced surgical technologies, and greater emphasis on early detection programs. The region’s improving healthcare infrastructure and government initiatives supporting rare disease treatment are significantly contributing to market growth.

Japan Craniosynostosis Treatment Market Insight

The Japan craniosynostosis treatment market is gaining momentum due to the country’s advanced healthcare infrastructure, rapid urbanization, and growing focus on early diagnosis and intervention. The increasing availability of specialized pediatric craniofacial centers and adoption of minimally invasive surgical techniques are supporting market growth. Japan’s aging population, combined with heightened parental awareness, is expected to drive demand for safer, precise, and effective craniosynostosis treatment solutions in both hospital and clinic settings.

China Craniosynostosis Treatment Market Insight

The China craniosynostosis treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, supported by the country’s expanding healthcare infrastructure, increasing number of pediatric hospitals, rising disposable incomes, and growing awareness of early cranial deformity diagnosis and intervention. Technological advancements in surgical planning, regenerative therapies, and precision cranial reconstruction, along with government initiatives to improve rare disease care, are key factors propelling market growth in China.

Craniosynostosis Treatment Market Share

The Craniosynostosis Treatment industry is primarily led by well-established companies, including:

• Stryker (U.S.)

• Medtronic (Ireland)

• Zimmer Biomet Holdings, Inc. (U.S.)

• KLS Martin Group (Germany)

• DePuy Synthes (U.S.)

• Aesculap, Inc. (Germany)

• Integra LifeSciences Holdings Corporation (U.S.)

• Johnson & Johnson and its afiliates (U.S.)

• Orthofix Medical Inc. (U.S.)

• Canon Medical Systems Corporation (Japan)

• Baxter (U.S.)

• B. Braun SE (Germany)

• NuVasive, Inc. (U.S.)

• Planmeca Oy (Finland)

Latest Developments in Global Craniosynostosis Treatment Market

- In March 2025, Connecticut Children's Medical Center introduced a minimally invasive surgical approach for craniosynostosis treatment, known as endoscopic strip craniectomy. This technique offers shorter recovery times and excellent outcomes, marking a significant advancement in pediatric neurosurgery

- In July 2025, Cho Lab received a one-year State Economic Engagement & Development (SEED) fund grant from the University of Wisconsin–Madison to develop "CranioSure," an app designed to screen infant head shapes during primary care visits. This tool aims to distinguish between benign head shape differences and more serious conditions like craniosynostosis, facilitating timely referrals and interventions

- In January 2025, the Children's Hospital of Philadelphia (CHOP) Research Institute launched the "Advancing Craniofacial Treatment with Genomics and Gene Therapy (ACTG)" program. This initiative focuses on integrating genomics and gene therapy to enhance craniosynostosis treatment, reflecting a significant step towards personalized medicine in craniofacial car

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.