Global Creatinine Measurement Market

Market Size in USD Billion

USD

1.86 Billion

USD

4.73 Billion

2025

2033

USD

1.86 Billion

USD

4.73 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.86 Billion | |

| USD 4.73 Billion | |

| % | |

|

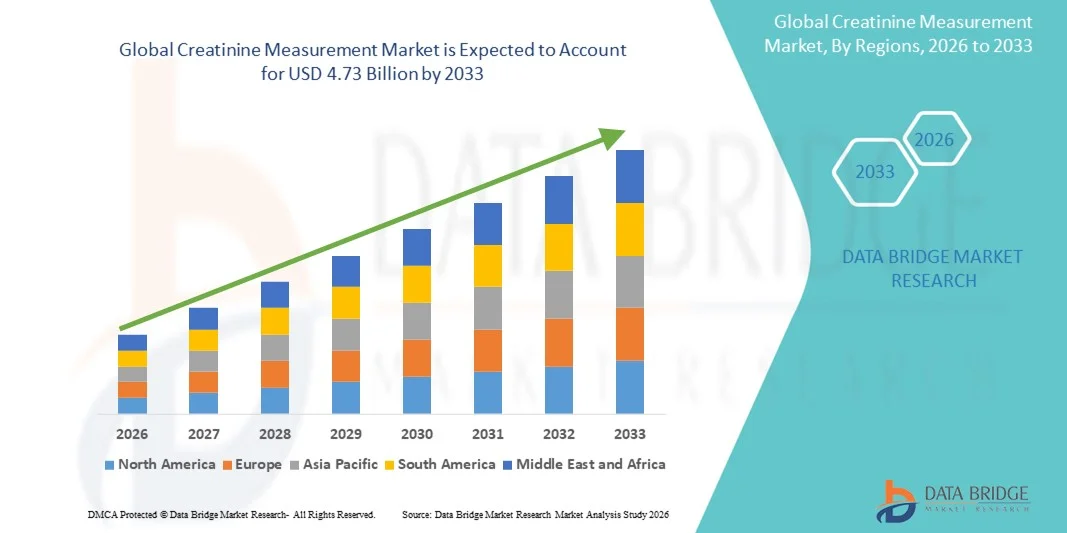

Creatinine Measurement Market Size

- The global creatinine measurement market size was valued at USD 1.86 billion in 2025 and is expected to reach USD 4.73 billion by 2033, at a CAGR of 12.40% during the forecast period

- The market growth is largely fueled by the rising prevalence of chronic kidney disease (CKD), diabetes, and hypertension worldwide, which has significantly increased the need for early and accurate renal function assessment. Advancements in diagnostic technologies, including point-of-care testing, enzymatic assays, and automated analyzers, are further accelerating the adoption of creatinine measurement solutions across clinical and diagnostic settings

- Moreover, the growing demand for reliable, rapid, and cost-effective diagnostic tools in hospitals, laboratories, and home-care environments is positioning creatinine testing as a critical component of routine health monitoring. These combined factors are driving the uptake of creatinine measurement solutions, thereby significantly boosting the overall market growth

Creatinine Measurement Market Analysis

- Creatinine measurement solutions, used for evaluating kidney function through serum, urine, and point-of-care testing, are becoming increasingly essential in hospitals, diagnostic laboratories, and home-care settings due to their accuracy, rapid results, and suitability for early detection of chronic kidney disease (CKD)

- The escalating demand for creatinine measurement systems is primarily driven by the rising global burden of CKD, diabetes, and hypertension, increasing preference for routine renal health monitoring, and the growing shift toward automated, user-friendly, and cost-effective diagnostic tools

- North America dominated the creatinine measurement market with the largest revenue share of 38.7% in 2025, supported by a high incidence of CKD, strong adoption of point-of-care devices, advanced healthcare infrastructure, and the presence of major diagnostic manufacturers. The U.S. shows particularly strong growth due to expanded screening programs and increased integration of automated analyzers in hospitals and clinical labs

- Asia-Pacific is expected to be the fastest-growing region in the creatinine measurement market during the forecast period, projected to expand at a CAGR of 10.5% due to rapid urbanization, rising healthcare expenditure, and growing awareness of early kidney disease detection across India, China, and Southeast Asia

- The serum creatinine segment accounted for the largest market revenue share of 72.3% in 2025, driven by its status as the most widely used and clinically reliable biomarker for assessing kidney function

Report Scope and Creatinine Measurement Market Segmentation

|

Attributes |

Creatinine Measurement Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Creatinine Measurement Market Trends

Shift Toward Rapid, Accurate, and Decentralized Testing

- A significant and accelerating trend in the global Creatinine Measurement market is the shift toward faster, decentralized, and more efficient diagnostic methods, enabling clinicians to assess renal function with greater speed and accuracy in both hospital and non-hospital setting

- For instance, the adoption of point-of-care (POC) creatinine analyzers that deliver results within minutes is rising rapidly, supporting timely diagnosis of acute kidney injury and improving workflow efficiency in emergency departments and outpatient centers

- Advancements in enzymatic assay technologies—offering higher specificity, fewer interferences, and improved analytical precision—are increasingly replacing older Jaffe-based methods across laboratories globally

- The integration of creatinine testing into multi-parameter renal panels and compact handheld analyzers is enhancing diagnostic efficiency by allowing clinicians to evaluate multiple kidney markers simultaneously

- There is also a growing trend toward home-based renal monitoring solutions for chronic kidney disease (CKD) patients, supported by simplified testing kits designed for remote monitoring and telehealth models

- This growing focus on rapid, decentralized, and patient-centric testing is reshaping clinical workflows and driving demand for innovative creatinine measurement solutions worldwide

Creatinine Measurement Market Dynamics

Driver

Increasing Prevalence of Kidney Disease and Routine Monitoring Needs

- The rising global prevalence of chronic kidney disease (CKD), driven by aging populations and increased incidence of diabetes and hypertension, is a primary driver for heightened demand for creatinine testing as part of routine renal function monitoring

- For instance, healthcare systems are expanding screening programs to detect early-stage CKD, increasing the volume of creatinine tests performed in both primary care and specialty settings

- Growing emphasis on early detection and management of acute kidney injury in hospitals and emergency departments is prompting wider adoption of rapid creatinine assays

- Expansion of point-of-care testing capabilities and outpatient monitoring programs supports decentralized care models and reduces burden on central laboratories

- Reimbursement policies and clinical guidelines that recommend regular renal function assessment for at-risk populations further encourage uptake of creatinine measurement technologies

Restraint/Challenge

Variability in Test Accuracy, Standardization, and Reimbursement

- Concerns about analytical variability between point-of-care devices and central laboratory assays can impede clinical trust and broader adoption of some rapid creatinine measurement platforms

- For instance, differences in sample type (capillary vs venous), calibration standards, and assay interference may produce inconsistent results across platforms, complicating longitudinal patient monitoring

- Lack of universal standardization and harmonized reference methods for creatinine measurement poses challenges for clinicians who rely on trend-based interpretation (e.g., eGFR calculations)

- Reimbursement limitations and restrictive coverage policies in some markets can slow adoption of newer POC devices despite clinical need, particularly in outpatient and ambulatory care settings

- High initial acquisition cost for certain automated or cartridge-based platforms and ongoing consumable costs may deter smaller clinics and resource-limited facilities from upgrading from central-lab reliance

- Overcoming these challenges requires greater assay standardization, robust clinical validation studies, clear reimbursement pathways, and education for clinicians on appropriate device selection and result interpretation

Creatinine Measurement Market Scope

The market is segmented on the basis of product, test type, sample, and end user.

- By Product

On the basis of product, the Creatinine Measurement market is segmented into kits and reagents. The kits segment dominated the largest market revenue share of 58.4% in 2025, driven by the high demand for ready-to-use, standardized testing solutions that ensure accuracy and reduce manual preparation errors. Clinical laboratories and hospitals prefer kits because they offer convenience, reproducibility, and compatibility with automated analyzers, enabling faster turnaround times. With the rising incidence of chronic kidney disease and acute kidney injury, the need for rapid, reliable creatinine assessments has surged, further strengthening the demand for diagnostic kits. Additionally, the widespread use of point-of-care testing devices, many of which rely on kit-based formats, has contributed to the dominance of this segment. Kits are also favored for their regulatory approvals, batch consistency, and suitability for high-volume testing environments, reinforcing their leadership in the global market.

The reagents segment is anticipated to witness the fastest CAGR of 10.9% from 2026 to 2033, driven by growing adoption of automated biochemistry systems and increasing test throughput in diagnostic laboratories worldwide. Reagents offer cost advantages for bulk testing and are preferred in large laboratories performing continuous renal function monitoring. The rising shift toward enzymatic assays—requiring high-performance reagents with reduced interference—further accelerates segment growth. Technological advancements enabling enhanced reagent stability, longer shelf-life, and improved precision also contribute to the rapid expansion of this segment during the forecast period.

- By Test Type

On the basis of test type, the Creatinine Measurement market is segmented into the Jaffe method and enzymatic creatinine method. The Jaffe method segment dominated the largest revenue share of 60.7% in 2025, attributed to its long-standing use as the most common and cost-effective method for serum creatinine measurement. Hospitals and diagnostic laboratories heavily rely on the Jaffe method due to its affordability, scalability, and wide availability across automated analyzers. The method’s ability to process high test volumes, especially in regions with limited healthcare budgets, reinforces its dominance. Despite known interferences, improvements in kinetic Jaffe assays have enhanced specificity, enabling continued clinical preference. The widespread inclusion of the Jaffe method in routine renal panels and its historical acceptance in global kidney disease monitoring further support its leading market position.

The enzymatic creatinine method is expected to witness the fastest CAGR of 12.4% from 2026 to 2033, driven by its superior accuracy, reduced susceptibility to interference, and growing adoption in advanced clinical settings. Enzymatic assays are increasingly preferred for pediatric, oncology, and critical care patients where precision is crucial. Technological enhancements such as improved enzymatic stability, multi-parameter analyzer compatibility, and enhanced performance in low-concentration samples further accelerate adoption. The rising shift toward high-quality diagnostics and strict regulatory accuracy requirements are major contributors to this segment’s rapid growth.

- By Sample

On the basis of sample, the Creatinine Measurement market is segmented into serum creatinine and urine. The serum creatinine segment accounted for the largest market revenue share of 72.3% in 2025, driven by its status as the most widely used and clinically reliable biomarker for assessing kidney function. Serum testing is integral to routine metabolic panels, emergency diagnostics, chronic kidney disease monitoring, and pre-surgical evaluations. Hospitals and laboratories favor serum samples for their ease of collection, standardized interpretation, and compatibility with automated chemistry analyzers. The growing global burden of diabetes, hypertension, and cardiovascular diseases—major contributors to renal impairment—further strengthens demand for serum creatinine testing. Its rapid turnaround time and essential role in estimating glomerular filtration rate (eGFR) reinforce its dominance.

The urine sample segment is anticipated to record the fastest CAGR of 9.8% from 2026 to 2033, fueled by increasing utilization of urine creatinine for assessing kidney filtration efficiency, drug tests, and evaluating proteinuria through creatinine ratio measurements. Rising adoption of at-home urine test kits and expanding use in long-term renal monitoring support segment growth. Urine-based testing is non-invasive, cost-effective, and particularly useful in population health screening. Growing research on biomarker discovery using urine matrices also contributes to accelerated market expansion over the forecast period.

- By End User

On the basis of end user, the Creatinine Measurement market is segmented into hospitals, diagnostic laboratories, and others. The hospitals segment dominated the largest revenue share of 49.6% in 2025, driven by the high volume of renal function tests performed in inpatient and emergency care settings. Hospitals require rapid and accurate creatinine testing to diagnose acute kidney injury, monitor drug dosing, and assess renal function in critical patients. The availability of advanced analyzers, integration with electronic health records, and comprehensive renal care units further strengthen hospital dominance. Rising hospitalization rates for chronic diseases and the increased need for preoperative renal evaluation also contribute significantly to segment leadership.

The diagnostic laboratories segment is projected to witness the fastest CAGR of 11.2% from 2026 to 2033, driven by increasing outsourcing of routine tests, expanding laboratory networks, and rising demand for high-throughput renal screening. Laboratories benefit from economies of scale, enabling them to adopt advanced enzymatic assays and automated analyzers. Growing emphasis on preventive healthcare and widespread availability of renal function panels at affordable costs also supports segment expansion. The rise of independent lab chains, home sample collection services, and digital reporting platforms boosts the rapid growth of diagnostic laboratories during the forecast period.

Creatinine Measurement Market Regional Analysis

- North America dominated the creatinine measurement market with the largest revenue share of 38.7% in 2025, supported by the region’s high prevalence of chronic kidney disease (CKD), widespread adoption of point-of-care (POC) diagnostic devices, and strong penetration of automated chemistry analyzers across hospitals and laboratories

- The strong presence of leading diagnostic manufacturers and continuous technological advancements in renal function testing significantly contribute to regional growth

- In addition, expanding kidney disease screening programs and increasing awareness among both clinicians and patients regarding early detection further reinforce North America’s dominant position in the market

U.S. Creatinine Measurement Market Insight

The U.S. creatinine measurement market captured the largest share of 81% within North America in 2025, driven by well-established healthcare infrastructure, increasing CKD incidence, and growing integration of automated analyzers and POC testing platforms in hospitals, outpatient centers, and diagnostic laboratories. The expanding use of creatinine testing in pre-operative assessments, medication dosing decisions, emergency care, and imaging procedures requiring contrast agents further accelerates market growth. Federal initiatives promoting early kidney disease diagnosis also support widespread adoption across clinical settings.

Europe Creatinine Measurement Market Insight

The Europe creatinine measurement market is projected to grow at a substantial CAGR during the forecast period, driven by strong demand for reliable renal function testing and increasing investments in clinical diagnostics. The region’s rising geriatric population—prone to diabetes, hypertension, and CKD—continues to drive the need for routine creatinine assessment across hospitals, diagnostic laboratories, and specialized nephrology centers. Additionally, advancements in automated chemistry platforms, coupled with expanding government-supported screening programs for early kidney disease, are contributing to steady market expansion across Western and Central Europe.

U.K. Creatinine Measurement Market Insight

The U.K. creatinine measurement market is anticipated to grow at a noteworthy CAGR, supported by the rising burden of kidney disorders, increasing adoption of high-precision enzymatic testing methods, and growing demand for reliable renal function monitoring in primary care settings. The country’s strong emphasis on preventive healthcare and early detection of CKD further drives the usage of creatinine tests across NHS facilities and private diagnostic providers.

Germany Creatinine Measurement Market Insight

The Germany creatinine measurement market is expected to expand at a considerable CAGR, fueled by the country’s advanced healthcare system, rapid adoption of automated diagnostic platforms, and high awareness of renal function monitoring. Germany’s strong base of clinical laboratories and continuous innovation in biochemical testing technologies support the growing use of creatinine assays in both inpatient and outpatient settings.

Asia-Pacific Creatinine Measurement Market Insight

The Asia-Pacific creatinine measurement market is projected to grow at the fastest CAGR of 10.5% from 2026 to 2033, driven by rising healthcare expenditure, rapid urbanization, increasing CKD prevalence, and growing awareness about early diagnosis in countries such as India, China, Japan, and South Korea. Government-backed initiatives promoting preventive healthcare, expanding diagnostic laboratory networks, and increasing adoption of POC devices for rapid renal assessment are accelerating the region’s growth.

Japan Creatinine Measurement Market Insight

The Japan creatinine measurement market is witnessing strong growth due to the country’s aging population, high incidence of diabetes and hypertension, and advanced adoption of automated biochemical analyzers in hospitals and clinics. Emphasis on accurate renal function monitoring for elderly patients and those with chronic illnesses is driving continuous demand for both serum and urine creatinine testing.

China Creatinine Measurement Market Insight

The China creatinine measurement market accounted for the largest revenue share within Asia-Pacific in 2025, driven by rapid expansion of diagnostic laboratories, rising CKD burden, and increasing access to affordable creatinine testing kits and reagents. Strong government focus on enhancing healthcare infrastructure and large-scale screening initiatives for kidney diseases support the growth of creatinine measurement across urban and semi-urban regions. The presence of domestic diagnostic manufacturers further boosts market accessibility and affordability.

Creatinine Measurement Market Share

The Creatinine Measurement industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- F. Hoffmann-La Roche (Switzerland)

- Siemens Healthineers (Germany)

- Danaher Corporation (U.S.)

- Thermo Fisher Scientific (U.S.)

- Randox Laboratories (U.K.)

- Diazyme Laboratories (U.S.)

- Sysmex Corporation (Japan)

- Bio-Rad Laboratories (U.S.)

- Pointe Scientific (U.S.)

- Diasys Diagnostic Systems (Germany)

Latest Developments in Global Creatinine Measurement Market

- In November 2021, Siemens Healthcare Diagnostics received FDA 510(k) clearance for its Atellica CH Enzymatic Creatinine_3 (ECre3) assay, enabling accurate enzymatic creatinine measurement in serum, plasma, and urine on the Atellica CH analyzer and expanding automated renal testing capabilities

- In March 2022, Abbott received FDA 510(k) clearance for the Creatinine2 assay for quantitative creatinine determination on the ARCHITECT c system, supporting improved renal function analysis across routine clinical chemistry laboratories

- In March 2022, Nova Biomedical announced CE-marking and the European launch of the Nova Max Pro Creatinine/eGFR meter system, introducing rapid point-of-care kidney function testing for early CKD detection in outpatient and community screening settings

- In October 2022, independent clinical validation studies confirmed the performance accuracy of the Nova Max Creatinine/eGFR handheld system compared to reference laboratory analyzers, supporting its wider adoption in decentralized diagnostic workflows

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.