Global Crimean Congo Haemorrhagic Fever Market

Market Size in USD Million

USD

396.22 Million

USD

567.79 Million

2025

2033

USD

396.22 Million

USD

567.79 Million

2025

2033

| 2026 - 2033 | |

| USD 396.22 Million | |

| USD 567.79 Million | |

| % | |

|

Crimean-Congo Haemorrhagic Fever Market Size

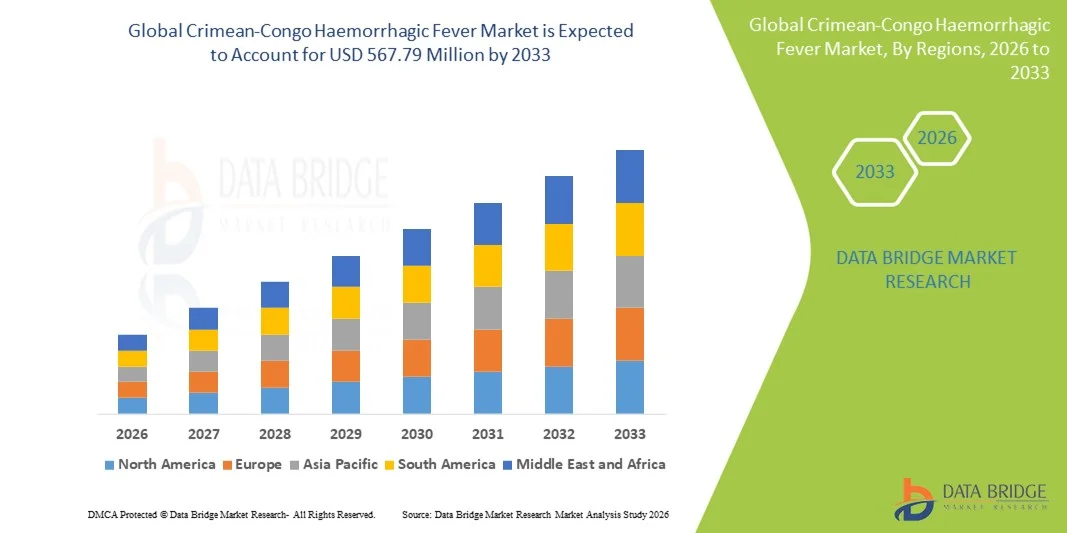

- The global Crimean-Congo haemorrhagic fever market size was valued at USD 396.22 million in 2025 and is expected to reach USD 567.79 million by 2033, at a CAGR of 4.60% during the forecast period

- The market expansion is primarily driven by the rising incidence of tick-borne infections across endemic regions, coupled with the increasing need for effective diagnostic tools, antiviral therapies, and preventive measures to control disease transmission

- Furthermore, growing governmental and international health-agency initiatives to strengthen outbreak preparedness, improve surveillance systems, and support rapid-response treatment is positioning CCHF-focused solutions as a critical component of global infectious disease management. These converging factors are accelerating the adoption of advanced diagnostics and therapeutics, thereby significantly boosting the industry's growth

Crimean-Congo Haemorrhagic Fever Market Analysis

- Crimean-Congo haemorrhagic fever, caused by a tick-borne virus, is increasingly recognized as a critical public health concern in both endemic and non-endemic regions due to its high fatality rate, potential for outbreaks, and lack of widely available vaccines or targeted therapies

- The escalating demand for effective Crimean-Congo haemorrhagic fever management is primarily fueled by the rising prevalence of tick populations, increasing human-livestock interactions, and growing awareness among healthcare providers and governments regarding the importance of rapid diagnosis and supportive care

- North America dominated the Crimean-Congo haemorrhagic fever market with the largest revenue share of 40.7% in 2025, characterized by advanced healthcare infrastructure, well-established surveillance programs, and substantial investment in research and development for antiviral treatments and diagnostics, with the U.S. leading in adoption of rapid testing technologies and antiviral therapy protocols guided by both governmental and private healthcare initiatives

- Asia-Pacific is expected to be the fastest-growing region in the Crimean-Congo haemorrhagic fever market during the forecast period due to expanding livestock farming, increasing public health investments, and rising awareness about vector control measures

- Ribavirin segment dominated the Crimean-Congo haemorrhagic fever market under the treatment category with a market share of 42.8% in 2025, driven by its established role as the primary antiviral therapy, increasing clinical adoption, and supportive government guidelines promoting its use during outbreaks

Report Scope and Crimean-Congo Haemorrhagic Fever Market Segmentation

|

Attributes |

Crimean-Congo Haemorrhagic Fever Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Crimean-Congo Haemorrhagic Fever Market Trends

Advancements in Rapid Point-of-Care Diagnostics

- A significant and accelerating trend in the global Crimean-Congo haemorrhagic fever market is the development and deployment of rapid point-of-care diagnostic kits that enable early detection of infections in remote and high-risk endemic regions

- For instance, the Recombivirus CCHF Rapid Test allows healthcare workers to detect the virus within hours, significantly reducing diagnosis time compared to conventional laboratory assays

- These rapid diagnostic kits are increasingly integrated with digital reporting systems to track outbreaks in real time, facilitating faster public health responses and containment measures

- The trend towards portable, easy-to-use, and highly accurate diagnostic solutions is enabling decentralized testing in clinics and hospitals, improving access to timely treatment and outbreak management

- This trend is reshaping expectations for infectious disease surveillance, encouraging companies such as BioDetect and GenTech to develop AI-assisted diagnostic platforms with enhanced sensitivity and usability

- The demand for rapid and reliable diagnostics is growing across both public and private healthcare sectors, as authorities prioritize early detection and containment of Crimean-Congo haemorrhagic fever outbreaks

- There is an increasing focus on integrating diagnostic solutions with telemedicine platforms to allow remote patient monitoring and timely clinical decision-making

- Partnerships between biotech firms and governmental health agencies to deploy mobile testing units in rural areas are accelerating the reach of CCHF surveillance programs

Crimean-Congo Haemorrhagic Fever Market Dynamics

Driver

Increasing Incidence and Rising Awareness of Tick-Borne Infections

- The growing prevalence of Crimean-Congo haemorrhagic fever in endemic regions, coupled with rising awareness among healthcare providers and governments, is a key driver for market growth

- For instance, in March 2025, the U.S. CDC launched an awareness campaign on tick-borne viruses, highlighting the need for improved surveillance, diagnostics, and antiviral therapies

- As populations in endemic regions encounter higher exposure to tick vectors, the demand for effective treatments such as Ribavirin and supportive care solutions is increasing, encouraging broader clinical adoption

- Governmental programs and international health initiatives are promoting early detection and standardized treatment protocols, further fueling market expansion

- Enhanced public health education, surveillance programs, and training of healthcare professionals are making Crimean-Congo haemorrhagic fever management an essential priority in both hospitals and clinics

- The rising concern over potential outbreaks and fatalities is driving investments in diagnostic tools, antiviral therapies, and outbreak preparedness infrastructure globally

- Expansion of public-private partnerships is enabling faster development and distribution of antiviral drugs and monoclonal antibodies in high-risk areas

- Increasing funding for research on tick ecology and vector control strategies is supporting preventive measures, indirectly boosting demand for CCHF management solutions

Restraint/Challenge

Limited Therapeutic Options and Regulatory Barriers

- The limited availability of approved therapies and vaccines for Crimean-Congo haemorrhagic fever, along with strict regulatory requirements for antiviral drugs, poses a significant challenge to market growth

- For instance, high regulatory scrutiny for novel treatments delays the approval and commercialization of advanced therapies such as monoclonal antibodies and IVIG

- The lack of standardized treatment protocols and limited access to antiviral drugs in remote or resource-constrained regions further restricts market penetration

- While ongoing research is promising, the complexity of conducting clinical trials in high-risk areas and ensuring patient safety presents significant hurdles for pharmaceutical companies

- High costs associated with advanced therapies and specialized diagnostics can limit adoption, particularly in developing countries or low-income healthcare settings

- Overcoming these challenges through streamlined regulatory pathways, expanded clinical research, and government-supported distribution of antiviral therapies is critical for sustainable market growth

- Limited awareness among rural populations about CCHF symptoms and preventive measures contributes to delayed treatment and higher mortality rates

- Logistical challenges in transporting sensitive diagnostic kits and antivirals to remote endemic regions can hinder timely disease management and outbreak control

Crimean-Congo Haemorrhagic Fever Market Scope

The market is segmented on the basis of treatment, diagnosis, transmission, dosage, route of administration, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the market is segmented into Ribavirin, Histamine Receptor Blockers, Steroids, Anti-CCHF Monoclonal Antibodies, Intravenous Immunoglobulin (IVIG), and Others. The Ribavirin segment dominated the market with the largest market revenue share of 42.8% in 2025, driven by its established role as the primary antiviral therapy for Crimean-Congo haemorrhagic fever. Ribavirin is widely adopted due to clinical evidence supporting its efficacy in reducing viral load and improving patient outcomes. Hospitals and clinics in endemic regions often stock Ribavirin as a first-line therapy. Its cost-effectiveness relative to advanced biologics also contributes to sustained demand. Government and NGO guidelines for outbreak management recommend Ribavirin as a standard treatment. In addition, medical professionals are familiar with its administration protocols, further consolidating its dominance.

The Anti-CCHF Monoclonal Antibodies segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by ongoing clinical trials and increasing investment in targeted immunotherapies. Monoclonal antibodies offer high specificity and potential to improve survival rates in severe cases. Rising awareness about biologics and support from health agencies for advanced therapies are accelerating adoption. Their use in combination with standard antiviral therapy is emerging as a promising approach to treat high-risk patients. Technological advancements in monoclonal production are improving efficacy and reducing side effects. The growing focus on personalized medicine in infectious diseases is also supporting this segment’s rapid growth.

- By Diagnosis

On the basis of diagnosis, the market is segmented into ELISA, Serum Neutralization, Antigen Detection, RT-PCR Assay, and Others. The RT-PCR Assay segment dominated the market in 2025, accounting for the largest revenue share, owing to its high sensitivity and specificity for detecting CCHF viral RNA. RT-PCR is widely used in hospitals and reference laboratories for early diagnosis, which is critical in outbreak containment. The rapid turnaround time and reliable results make it the preferred diagnostic tool for clinicians. Governments and public health agencies often prioritize RT-PCR deployment in surveillance programs. Its ability to detect low viral loads enables early intervention, reducing fatality rates. Continuous technological upgrades are enhancing throughput and accuracy, reinforcing its market dominance.

The ELISA segment is anticipated to witness the fastest CAGR from 2026 to 2033 due to its cost-effectiveness, ease of use, and suitability for large-scale screening. ELISA kits are increasingly adopted in resource-limited settings and field diagnostic campaigns. They allow detection of antibodies or antigens and are suitable for retrospective studies and serosurveillance. Rising awareness of serological testing benefits is driving market expansion, particularly in endemic rural regions. ELISA tests are easier to deploy in decentralized locations compared to RT-PCR. Increasing investments in low-cost diagnostic kits are expected to boost adoption.

- By Transmission

On the basis of transmission, the market is segmented into transstadial, transovarial, and others. The Transstadial segment dominated the market in 2025, as the virus persists through tick developmental stages, making it the primary mode of human infection. Awareness of transstadial transmission has driven preventive strategies, including tick control measures and protective guidelines for livestock handlers. Surveillance programs frequently monitor tick populations, emphasizing transstadial transmission as a key focus. This has led to higher demand for associated preventive and diagnostic solutions in endemic regions. Veterinary monitoring programs also highlight transstadial transmission risks, increasing funding for interventions. Research publications and government advisories often cite transstadial transmission as critical in outbreak management, reinforcing its significance.

The Transovarial segment is expected to witness the fastest growth from 2026 to 2033 due to increased research on vertical viral transmission in ticks. Understanding this mode helps in developing improved vector control and vaccination strategies. The rising investment in entomological studies and predictive modeling is driving the growth of solutions targeting transovarial transmission pathways. Awareness campaigns among livestock handlers emphasize the risks of vertical transmission. Expansion of academic research and government-funded programs are creating demand for novel interventions. The segment’s growth is further supported by emerging strategies to block viral transmission at the tick reproduction stage.

- By Dosage

On the basis of dosage, the market is segmented into injection, tablet, capsule, and others. The Injection segment dominated the market in 2025, driven by its primary use for intravenous administration of antiviral therapies such as Ribavirin in hospitalized patients. Injections ensure rapid bioavailability and are preferred in critical care settings. Clinicians often recommend injections for severe cases due to their effectiveness and controlled dosing. Hospitals and specialty clinics stock injectable formulations as part of emergency preparedness kits for outbreaks. IV therapy also allows combination with supportive care, improving treatment efficacy. Regulatory and clinical guidelines often prioritize injection therapy for severe infections, reinforcing its dominant role.

The Tablet segment is expected to witness the fastest growth during 2026–2033, fueled by convenience, ease of distribution, and growing adoption for outpatient or home-based care. Tablets enable self-administration, reducing the burden on healthcare facilities. Rising awareness among patients and caregivers about oral therapies is driving adoption, particularly in endemic rural areas. Tablets are also more suitable for mass prophylaxis in high-risk populations. Manufacturing advancements are improving stability and shelf-life, further supporting growth. Government programs distributing oral antivirals in rural clinics contribute to the expansion of this segment.

- By Route of Administration

On the basis of route of administration, the market is segmented into intravenous, oral, and other. The Intravenous segment dominated the market in 2025, owing to the prevalent use of IV Ribavirin and other hospital-administered therapies for critical patients. IV administration allows rapid systemic delivery and is crucial in severe cases. Hospitals in endemic areas stock IV formulations to manage outbreaks efficiently. Clinical guidelines emphasize intravenous therapy for hospitalized patients, ensuring high adoption rates. Emergency protocols for outbreak management often rely on IV administration, particularly in intensive care settings. Training programs for healthcare staff focus on proper IV administration, reinforcing the segment’s dominance.

The Oral segment is expected to witness the fastest growth rate from 2026 to 2033 due to convenience, ease of use, and suitability for outpatient care. Oral therapies enable broader access to treatment in remote areas and are increasingly recommended for early-stage infections. The rising focus on home-based care solutions is boosting oral therapy adoption globally. Patient adherence is easier with oral routes, improving overall treatment outcomes. Online and retail distribution channels are supporting oral therapy availability. Government initiatives for early intervention in endemic areas further drive this segment’s growth.

- By End-Users

On the basis of end-users, the market is segmented into clinic, hospital, and others. The Hospital segment dominated the market in 2025, accounting for the largest revenue share due to the concentration of severe cases and availability of specialized diagnostic and treatment facilities. Hospitals are equipped with advanced laboratories for RT-PCR testing and intensive care units for antiviral therapy. Clinical management of CCHF often requires hospitalization, ensuring hospitals remain the primary end-user segment. Government and NGO initiatives often target hospitals for outbreak preparedness and treatment delivery. Hospitals also facilitate clinical trials for new therapies, reinforcing market dominance. Centralized healthcare infrastructure in hospitals supports high patient throughput during outbreaks.

The Clinic segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing decentralization of healthcare services and the rising deployment of rapid diagnostic kits in outpatient settings. Clinics play a crucial role in early detection, monitoring mild cases, and providing initial therapy, particularly in rural and semi-urban regions. Adoption of telemedicine-enabled clinics further supports faster patient access and treatment. Growing public-private partnerships are expanding clinic networks. Clinics also provide education and preventive guidance, improving overall disease management. Increasing availability of oral therapies and point-of-care diagnostics enhances clinic adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy segment dominated the market in 2025, due to direct access to critical therapies, diagnostics, and intravenous medications for CCHF management. Hospitals maintain inventory of antiviral drugs, monoclonal antibodies, and supportive care treatments. Hospital pharmacies are also preferred for regulated dispensing and monitoring of dosage protocols, ensuring patient safety. Collaboration with government programs for outbreak response further reinforces dominance. Hospital pharmacies also facilitate emergency stockpiling during outbreaks. Established relationships with suppliers ensure timely procurement and availability of essential drugs.

The Online Pharmacy segment is expected to witness the fastest growth from 2026 to 2033, fueled by increasing e-pharmacy adoption, expanding internet access, and rising demand for home delivery of oral therapies and diagnostic kits. Online platforms enhance accessibility in remote regions and reduce time-to-treatment, making them an increasingly preferred channel for end-users outside major hospitals. Online pharmacies also provide patient education and teleconsultation services. Growing trust in e-pharmacies and digital payments is accelerating adoption. Partnerships with diagnostic kit manufacturers expand reach. Convenience and timely delivery are key factors driving this segment’s rapid growth.

Crimean-Congo Haemorrhagic Fever Market Regional Analysis

- North America dominated the Crimean-Congo haemorrhagic fever market with the largest revenue share of 40.7% in 2025, characterized by advanced healthcare infrastructure, well-established surveillance programs, and substantial investment in research and development for antiviral treatments and diagnostic

- The U.S. and Canada are witnessing increased focus on early detection, outbreak preparedness, and rapid deployment of antiviral treatments, supported by public health agencies and government initiatives

- This widespread adoption is further reinforced by high awareness among healthcare professionals, well-established hospital networks, and the integration of advanced diagnostic technologies such as RT-PCR and rapid point-of-care testing

U.S. Crimean-Congo Haemorrhagic Fever Market Insight

The U.S. Crimean-Congo haemorrhagic fever market captured the largest revenue share of 81% in North America in 2025, driven by advanced healthcare infrastructure and widespread adoption of rapid diagnostic technologies. Hospitals and reference laboratories are increasingly prioritizing RT-PCR and point-of-care testing for early detection. Government agencies, including the CDC, are implementing awareness programs and outbreak preparedness initiatives. Rising investment in antiviral therapies such as Ribavirin and monoclonal antibodies is further supporting market growth. Moreover, the integration of advanced diagnostics with telemedicine platforms is enhancing early intervention and patient monitoring. The strong focus on public health readiness ensures the U.S. remains a key contributor to the regional market.

Europe Crimean-Congo Haemorrhagic Fever Market Insight

The Europe Crimean-Congo haemorrhagic fever market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by public health initiatives and growing awareness of tick-borne viral infections. Countries such as Turkey and Greece are experiencing an increase in preventive surveillance programs and diagnostic adoption. Rising urbanization, along with the need for rapid detection and treatment of infections, is fostering the adoption of antiviral therapies and diagnostic solutions. The region is witnessing significant growth across hospitals, clinics, and research institutions. Government support and cross-border collaboration are accelerating outbreak management efforts. European healthcare providers are also focusing on improving access to monoclonal antibody therapies and supportive care options.

U.K. Crimean-Congo Haemorrhagic Fever Market Insight

The U.K. Crimean-Congo haemorrhagic fever market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness among healthcare professionals and public health authorities regarding tick-borne diseases. Increasing travel to endemic regions and preventive monitoring programs are encouraging the use of advanced diagnostics and antiviral therapies. Hospitals and clinics are adopting RT-PCR and ELISA testing to improve early detection and patient outcomes. Government-led initiatives for surveillance, training, and education are further stimulating market growth. The country’s robust healthcare infrastructure and research capabilities support the development and distribution of novel antiviral treatments. The growing emphasis on outbreak preparedness and infection control is expected to sustain market expansion.

Germany Crimean-Congo Haemorrhagic Fever Market Insight

The Germany Crimean-Congo haemorrhagic fever market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of emerging infectious diseases and advanced public health systems. Hospitals and research institutions are investing in rapid diagnostic technologies and antiviral therapy protocols. Preventive programs targeting livestock and tick populations are also contributing to growth. Germany’s emphasis on scientific research, healthcare innovation, and epidemiological studies supports early detection and treatment. The integration of diagnostics with hospital management systems is improving outbreak response efficiency. Strong government and private sector collaboration continues to drive the adoption of advanced CCHF management solutions.

Asia-Pacific Crimean-Congo Haemorrhagic Fever Market Insight

The Asia-Pacific Crimean-Congo haemorrhagic fever market is poised to grow at the fastest CAGR of 24% during 2026–2033, driven by rising awareness of tick-borne viral infections and expanding healthcare infrastructure in countries such as India, China, and Japan. Increasing surveillance programs, early diagnosis initiatives, and government-supported outbreak preparedness are boosting market adoption. Growing investments in diagnostic kits, oral antiviral therapies, and point-of-care testing are further driving growth. Rising urbanization and improved access to healthcare facilities are increasing demand in both residential and rural regions. In addition, regional public health campaigns are educating populations on preventive measures and early symptom recognition. The emergence of local diagnostic kit manufacturers is enhancing affordability and accessibility.

Japan Crimean-Congo Haemorrhagic Fever Market Insight

The Japan Crimean-Congo haemorrhagic fever market is gaining momentum due to the country’s advanced healthcare infrastructure, focus on infectious disease research, and rapid adoption of diagnostic technologies. Hospitals are increasingly deploying RT-PCR and ELISA assays to ensure early detection and management. The rising trend of telemedicine and mobile healthcare monitoring supports timely patient intervention. Government-led vector control and awareness programs are helping reduce outbreak risks. The adoption of monoclonal antibodies and supportive care therapies is expanding in specialized hospitals. Japan’s preparedness for emerging viral infections is driving demand for both preventive and therapeutic solutions.

India Crimean-Congo Haemorrhagic Fever Market Insight

The India Crimean-Congo haemorrhagic fever market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s large population in endemic regions, increasing public health initiatives, and expanding healthcare infrastructure. Hospitals and clinics are progressively adopting RT-PCR, ELISA, and rapid point-of-care diagnostic kits. Government surveillance programs and awareness campaigns are strengthening outbreak detection and management. The rising availability of oral antivirals, Ribavirin, and supportive therapies is improving treatment access. Expansion of rural healthcare services and telemedicine is enhancing early intervention. In addition, growing investment in research, diagnostics, and outbreak preparedness is driving overall market growth in India.

Crimean-Congo Haemorrhagic Fever Market Share

The Crimean-Congo Haemorrhagic Fever industry is primarily led by well-established companies, including:

- Aurobindo Pharma (India)

- Zydus (U.S.)

- Sandoz AG (Switzerland)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Bausch Health (Canada)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Albany Molecular Research Inc. (U.S.)

- Siegfried Holding AG (Switzerland)

- TRIMAX (India)

- Novartis AG (Switzerland)

- Sanofi (France)

- Pfizer Inc. (U.S.)

- GlaxoSmithKline plc (U.K.)

- Merck KGaA (Germany)

- Sumitomo Corporation (Japan)

- Johnson & Johnson Services, Inc. (India)

- AstraZeneca (U.K.)

- Abbott (U.S.)

- Cipla Inc. (India)

- Bayer AG (Germany)

What are the Recent Developments in Global Crimean-Congo Haemorrhagic Fever Market?

- In June 2025, Iraqi authorities reported 19 deaths from CCHF so far in the year (123 cases), renewing health warnings to livestock workers. The Ministry of Health urged farmers, butchers, and abattoir workers to intensify protective measures, including use of gloves and insect repellents

- In March 2025, WHO highlighted a successful risk communication and community engagement (RCCE) program in Iraq to manage CCHF. The campaign, in partnership with Iraq’s Ministries of Health, Agriculture, and the Iraqi Red Crescent, targeted high risk communities with educational materials and preventive guidance

- In June 2022, the World Health Organization (WHO) confirmed a major CCHF outbreak in Iraq, reporting 212 cases between January and May, of which 97 were laboratory confirmed, and 27 deaths. The outbreak placed considerable strain on health care systems, especially in livestock breeding areas, since nearly half the confirmed patients were butchers or farm workers

- In May 2023, Iraq reported another surge in CCHF, with at least 14 fatalities, prompting renewed public health alerts. The spike was particularly notable in rural regions, especially Dhi Qar governorate, which historically sees high tick livestock interactions

- In May 2022, WHO launched a multisectoral preparedness and response mission in Iraq to fight the outbreak. The mission involved coordination between Iraq’s Ministry of Health and Ministry of Agriculture to improve surveillance, tick control, and community awareness.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.