Global Ct Simulators Market

Market Size in USD Billion

USD

309.30 Billion

USD

492.97 Billion

2025

2033

USD

309.30 Billion

USD

492.97 Billion

2025

2033

| 2026 - 2033 | |

| USD 309.30 Billion | |

| USD 492.97 Billion | |

| % | |

|

Computed Tomography (CT) Simulators Market Overview

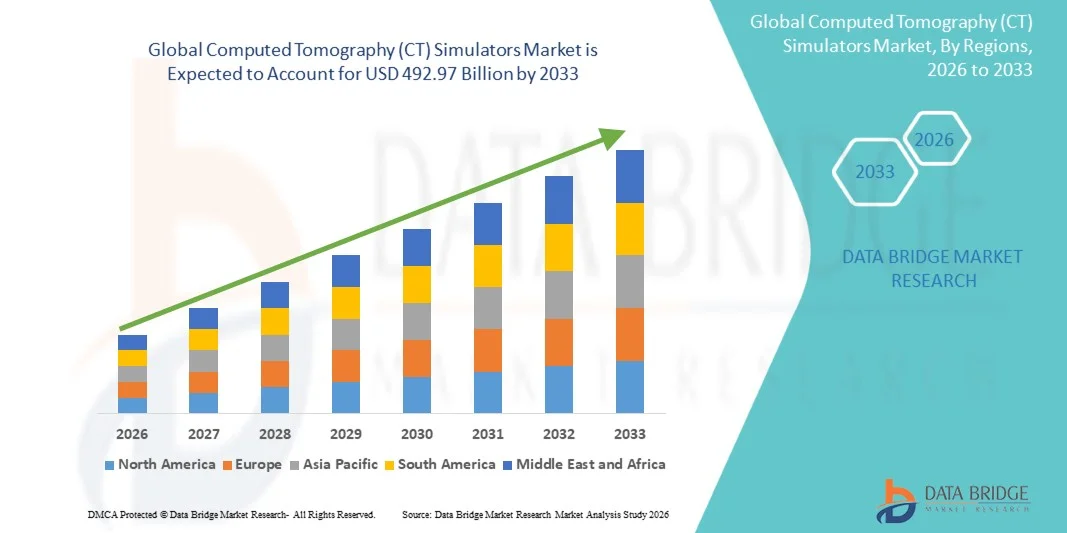

The Computed Tomography (CT) Simulators Market was valued at USD 309.30 billion in 2025 and is projected to reach USD 492.97 billion by 2033, growing at a CAGR of 6.00% from 2026 to 2033. The Computed Tomography (CT) Simulators Market is experiencing consistent growth driven by rising demand for high-precision medical imaging training, increasing adoption of simulation-based education in radiology, and expanding applications in hospitals, diagnostic centers, and medical training institutions.

The growing prevalence of chronic diseases and cancer, combined with increasing demand for accurate and early diagnosis, is compelling healthcare providers and academic institutions to adopt advanced CT simulation technologies for training radiologists and improving diagnostic accuracy. AI-integrated and software-based CT simulators are increasingly replacing traditional training methods, offering cost-effective, risk-free, and highly realistic virtual imaging environments for skill development, treatment planning, and workflow optimization in modern healthcare systems.

Key Market Trends & Insights

- North America dominated the Computed Tomography (CT) Simulators Market with the largest revenue share of 36.28% in 2025, supported by advanced healthcare infrastructure and strong adoption of radiology training, oncology planning, and image-guided simulation technologies.

- The Multi-Slice CT Simulators segment led the market with a 41.55% share in 2025, driven by superior imaging resolution, high diagnostic accuracy, and widespread use in radiation therapy planning and clinical training applications.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.2% from 2026 to 2033, fueled by rising healthcare infrastructure development, increasing cancer burden, and growing adoption of advanced diagnostic and simulation technologies in China, India, and Japan.

- 4D CT Simulation systems are the fastest-growing technology type, projected to register a CAGR of 7.0%, driven by increasing demand for motion-adaptive imaging in radiation therapy and organ movement analysis.

- The Hospitals segment dominates the end user category with a 41.71% revenue share in 2025, led by high adoption of CT simulators for oncology treatment planning, radiology training, and advanced diagnostic procedures.

- Direct Tender distribution channel accounts for 59.68% of the market, preferred by hospitals, government healthcare systems, and large oncology centers due to bulk procurement and cost efficiency.

- The Image-Guided Radiation Therapy (IGRT) application segment is the fastest-growing, with a CAGR of 6.8%, driven by rising demand for highly precise cancer treatment planning and real-time imaging-based therapy delivery systems.

- The Standalone segment dominated the market with a 32% revenue share in 2025, owing to its high imaging capability, advanced system integration, and widespread use in hospitals and specialty cancer centers

Market Size & Forecast

- Global Market Value (2025): USD 309.30 Billion

- Expected Market Value (2033): USD 492.97 Billion

- Forecast CAGR (2026–2033): 6.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Computed Tomography (CT) Simulators Market Segmentation

|

Attributes |

Computed Tomography (CT) Simulators Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Siemens Healthineers (Germany) |

|

Market Opportunities |

· Integration of AI-Driven Adaptive Treatment Planning Systems · Rising Demand for Advanced Radiation Therapy in Cancer Care · Expansion of Healthcare Infrastructure in Emerging Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Computed Tomography (CT) Simulators Market Trends

Trend: Growth in AI-Driven Medical Training & Precision Oncology Simulation

Healthcare institutions and medical universities are increasingly adopting high-fidelity Computed Tomography (CT) Simulators to enhance radiology training, improve tumor visualization, and support precision-based radiation therapy planning. The integration of real-time imaging reconstruction and advanced patient-specific modeling enables highly accurate simulation of anatomical structures, improving diagnostic confidence and treatment outcomes. Medical training centers are also leveraging CT simulators to standardize radiology education, while AI and advanced visualization technologies create highly realistic virtual imaging environments that closely replicate clinical scanning conditions. Leading companies such as Siemens Healthineers, GE HealthCare, and Elekta are actively integrating AI-enabled CT simulation platforms to improve workflow efficiency and support personalized cancer treatment planning.

Computed Tomography (CT) Simulators Market Dynamics

Key Market Driver: Rising Adoption in Cancer Diagnosis and Radiation Therapy Planning

The rapid increase in global cancer incidence and growing demand for precise, non-invasive diagnostic and treatment planning solutions have significantly driven the adoption of Computed Tomography (CT) Simulators. These systems are widely used in Image-Guided Radiation Therapy (IGRT), 3D Conformal Radiation Therapy, and brachytherapy planning to ensure accurate tumor targeting and minimize damage to surrounding healthy tissues. Hospitals and oncology centers are increasingly integrating CT simulation systems into radiology departments to improve treatment precision and workflow efficiency. For instance, leading cancer treatment institutions in the U.S., Europe, and Japan are extensively using multi-slice and large bore CT simulators to enhance radiotherapy planning accuracy and reduce treatment errors.

Key Restraint/Challenge: High Capital Investment and Operational Complexity

A significant restraint in the Computed Tomography (CT) Simulators Market is the high initial investment required for advanced imaging and simulation systems. Modern CT simulators incorporate high-resolution imaging hardware, advanced reconstruction software, and radiation planning integration tools, which significantly increase procurement and installation costs. In addition, ongoing expenses related to maintenance, software upgrades, and skilled operator training further add to the total cost of ownership. This limits adoption among small hospitals, diagnostic centers, and healthcare facilities in cost-sensitive regions, particularly in emerging economies where budget constraints remain a key barrier.

Key Market Opportunity: Integration of AI, Cloud Platforms, and Personalized Radiotherapy Planning

The integration of artificial intelligence, cloud-based imaging platforms, and advanced radiotherapy planning systems presents a major growth opportunity in the CT simulators market. AI-enabled CT simulation tools can automatically generate contouring, enhance image segmentation, and optimize radiation dose planning, significantly improving treatment efficiency and accuracy. Cloud-based deployment models are also enabling remote access to imaging data and collaborative treatment planning across multiple healthcare facilities. Leading medical technology companies such as Siemens Healthineers, Philips Healthcare, and Varian Medical Systems are actively investing in AI-driven CT simulation solutions to support personalized cancer therapy and improve clinical decision-making across global oncology networks.

Computed Tomography (CT) Simulators Market Scope

The Computed Tomography (CT) Simulators market is segmented on the basis of product type, technology, modality, application, end user, and distribution channel.

By Product Type

On the basis of product type, the Computed Tomography (CT) Simulators Market is segmented into Large Bore CT Simulators and Multi-Slice CT Simulators. The Multi-Slice CT Simulators segment dominated the market with a 41.55% share in 2025 due to superior imaging resolution, faster scanning capabilities, and high accuracy in radiotherapy planning and diagnostic training applications. These systems are widely adopted in hospitals and oncology centers for precise tumor localization and treatment simulation. Increasing integration of advanced imaging software and AI-based reconstruction tools is further enhancing segment dominance. In addition, rising demand for high-performance imaging in cancer diagnosis and radiation therapy planning is driving adoption across developed healthcare systems. Strong utilization in Image-Guided Radiation Therapy (IGRT) is further supporting market leadership. Continuous technological upgrades by key medical imaging companies are strengthening market penetration.

The 4D CT Simulation segment is expected to witness the fastest growth with a CAGR of 7.0% from 2026 to 2033, driven by its ability to capture real-time organ motion and respiratory cycle variations during imaging. This makes it highly effective for radiation therapy planning in lung, thoracic, and abdominal cancers. Increasing adoption of motion-adaptive radiotherapy techniques is significantly boosting demand. Hospitals are increasingly integrating 4D simulation systems to improve treatment accuracy and reduce radiation exposure to healthy tissues. Growing use of AI-enabled motion tracking and reconstruction algorithms is further accelerating segment growth. Rising cancer prevalence globally is supporting adoption. Expansion of advanced oncology centers in emerging markets is also contributing to growth.

By Technology

On the basis of technology, the market is segmented into 3D CT Simulation and 4D CT Simulation. The 3D CT Simulation segment dominated the market with a 59.68% revenue share in 2025, owing to its widespread use in radiation therapy planning, anatomical visualization, and clinical training applications. It provides highly detailed cross-sectional imaging essential for tumor mapping and dose planning. Hospitals and diagnostic centers prefer 3D systems due to their reliability and cost-effectiveness. Increasing adoption in Image-Guided Radiation Therapy (IGRT) and conformal radiation therapy is further strengthening demand. Strong compatibility with existing radiology infrastructure is supporting large-scale deployment. Continuous software advancements are improving image reconstruction quality. Growing demand for precise diagnostic workflows is reinforcing segment leadership.

The 4D CT Simulation segment is expected to register the fastest growth with a CAGR of 7.0% from 2026 to 2033, driven by increasing demand for dynamic imaging that captures organ movement over time. It is particularly important in respiratory-gated radiation therapy and adaptive treatment planning. Rising prevalence of lung and abdominal cancers is boosting adoption. Hospitals are increasingly investing in advanced motion-based imaging systems for higher precision. Integration of AI-based motion correction and predictive imaging is enhancing clinical outcomes. Growing focus on personalized cancer treatment is further supporting segment expansion. Increasing R&D in radiology innovation is accelerating technology adoption.

By Modality

On the basis of modality, the market is segmented into Standalone and Tabletop systems. The Standalone segment dominated the market with a 61.32% revenue share in 2025, owing to its high imaging capability, advanced system integration, and widespread use in hospitals and specialty cancer centers. These systems are preferred for large-scale diagnostic and radiotherapy planning applications. They offer superior imaging performance and better workflow integration with oncology departments. Increasing demand for high-capacity imaging systems in tertiary care hospitals is driving growth. Strong adoption in developed healthcare infrastructure is reinforcing dominance. Continuous technological upgrades in standalone CT systems are enhancing efficiency. Growing cancer treatment demand is further strengthening adoption globally.

The Tabletop segment is expected to witness the fastest growth with a CAGR of 6.8% from 2026 to 2033, driven by rising demand for compact, cost-effective imaging solutions in small hospitals and diagnostic centers. These systems are easier to install and require lower infrastructure investment. Increasing adoption in emerging economies is boosting growth. Expansion of outpatient diagnostic services is further supporting demand. Technological improvements are enhancing image quality in compact systems. Rising need for decentralized healthcare delivery is accelerating adoption. Growing use in training institutions is also contributing to segment expansion.

By Application

On the basis of application, the market is segmented into Image-Guided Radiation Therapy (IGRT), Three-Dimensional Conformal Radiation Therapy, Brachytherapy, Interventional Cardiology Procedure, and Others. The Image-Guided Radiation Therapy (IGRT) segment dominated the market with a 38.74% revenue share in 2025, driven by its high precision in tumor targeting and ability to improve radiation therapy outcomes. It is widely used in hospitals and oncology centers for real-time imaging-based treatment planning. Increasing cancer prevalence is significantly boosting demand. Strong adoption of advanced radiotherapy techniques is supporting segment growth. Integration of CT simulation with treatment planning systems is improving efficiency. Continuous technological advancements are enhancing imaging accuracy. Rising investment in oncology infrastructure is reinforcing market dominance.

The Interventional Cardiology Procedure segment is expected to witness the fastest growth with a CAGR of 6.9% from 2026 to 2033, driven by increasing use of CT simulation in cardiovascular diagnostics and minimally invasive procedures. Rising incidence of cardiovascular diseases is boosting demand. Hospitals are adopting advanced imaging systems for real-time procedural guidance. Growing preference for non-invasive diagnostic methods is supporting adoption. Integration of CT simulation with cardiac imaging systems is improving procedural accuracy. Technological advancements in imaging resolution are enhancing clinical outcomes. Expansion of cardiac care centers globally is accelerating growth.

By End User

On the basis of end user, the market is segmented into Hospitals, Specialty Centers, Ambulatory Surgical Centers, and Others. The Hospitals segment dominated the market with a 41.71% revenue share in 2025, due to high patient inflow, strong adoption of advanced imaging systems, and widespread use in oncology and radiology departments. Hospitals are key centers for radiation therapy planning and CT-based diagnostics. Increasing cancer burden is driving demand for advanced imaging solutions. Strong healthcare infrastructure in developed regions supports segment dominance. Continuous investment in hospital modernization is boosting adoption. Integration of CT simulators with treatment planning systems is enhancing workflow efficiency. Rising demand for precision medicine is further strengthening growth.

The Ambulatory Surgical Centers segment is expected to witness the fastest growth with a CAGR of 6.9% from 2026 to 2033, driven by rising demand for outpatient diagnostic and treatment services. ASCs are increasingly adopting compact CT simulation systems for cost-effective imaging solutions. Growing shift toward decentralized healthcare delivery is supporting adoption. Increasing preference for minimally invasive procedures is boosting demand. Expansion of private healthcare facilities is accelerating growth. Technological advancements are improving system accessibility. Rising healthcare affordability initiatives in emerging markets are further supporting expansion.

By Distribution Channel

On the basis of distribution channel, the market is segmented into Direct Tender and Retail Sales. The Direct Tender segment dominated the market with a 59.68% revenue share in 2025, driven by large-scale procurement by hospitals, government healthcare systems, and oncology centers. Bulk purchasing contracts ensure cost efficiency and standardized equipment deployment. Strong government healthcare funding programs are supporting segment growth. Hospitals prefer direct procurement for advanced imaging systems. Long-term vendor partnerships are reinforcing dominance. Increasing investment in oncology infrastructure is further boosting demand. Established procurement frameworks in developed regions are strengthening market leadership.

The Retail Sales segment is expected to witness the fastest growth with a CAGR of 6.8% from 2026 to 2033, driven by increasing demand from private diagnostic centers and specialty clinics. Growing accessibility through distributors and medical equipment suppliers is supporting adoption. Rising privatization of healthcare services is boosting demand. Expansion of small and mid-sized diagnostic centers is accelerating growth. Increasing affordability of advanced CT simulation systems is further supporting adoption. Growing awareness of early cancer detection is driving demand. Expansion in emerging markets is also contributing significantly to segment growth.

Computed Tomography (CT) Simulators Market Regional Analysis

North America dominated the Computed Tomography (CT) Simulators Market and accounted for the largest revenue share of 36.28% in 2025, supported by advanced healthcare infrastructure and strong adoption of radiology training, oncology planning, and image-guided simulation technologies. The region also benefits from well-established hospital networks, high investment in medical imaging systems, and early adoption of advanced CT simulation platforms for radiation therapy planning and diagnostic applications. Increasing focus on precision medicine, cancer treatment optimization, and technologically advanced healthcare systems continues to strengthen North America’s leadership position in the global market.

U.S. Computed Tomography (CT) Simulators Market Insight

The U.S. Computed Tomography (CT) Simulators market is witnessing strong growth due to rising incidence of cancer, increasing demand for advanced radiology training, and rapid adoption of image-guided radiation therapy systems. The country’s highly developed healthcare ecosystem, along with strong presence of leading medical imaging companies and oncology centers, is driving demand across hospitals and specialty clinics. In addition, increasing integration of AI-powered imaging tools, 3D/4D simulation technologies, and digital radiotherapy planning systems is further enhancing diagnostic accuracy and treatment outcomes, accelerating simulator adoption across healthcare institutions.

Europe Computed Tomography (CT) Simulators Market Insight

The Europe Computed Tomography (CT) Simulators market remains a major contributor to global revenue, driven by strong government healthcare support, advanced oncology infrastructure, and widespread adoption of radiotherapy planning systems. Hospitals and cancer research centers across the region are increasingly utilizing CT simulation technologies for precise tumor targeting and treatment planning. In addition, growing investments in digital healthcare transformation, combined with strict regulatory standards for radiation safety and treatment accuracy, are supporting steady market expansion across Europe.

U.K. Computed Tomography (CT) Simulators Market Insight

The U.K. Computed Tomography (CT) Simulators market is experiencing steady growth, supported by increasing demand for advanced cancer diagnostics, expansion of oncology departments, and rising adoption of precision radiotherapy systems. Hospitals and specialized cancer centers are investing in modern CT simulation technologies to improve treatment accuracy and workflow efficiency. Furthermore, integration of AI-based imaging tools and digital radiology platforms is enhancing clinical decision-making and strengthening the country’s position in advanced medical imaging adoption.

Germany Computed Tomography (CT) Simulators Market Insight

The Germany Computed Tomography (CT) Simulators market is expanding steadily due to the country’s strong healthcare infrastructure, advanced radiology research capabilities, and high adoption of innovative medical imaging technologies. Hospitals and oncology centers are increasingly deploying CT simulators for radiation therapy planning, image-guided interventions, and clinical training. Continuous technological advancements in 3D and 4D imaging systems, along with strong government support for healthcare innovation, are further driving market growth in Germany.

Asia-Pacific Computed Tomography (CT) Simulators Market Insight

The Asia-Pacific Computed Tomography (CT) Simulators market is expected to witness rapid growth, driven by rising healthcare infrastructure development, increasing cancer prevalence, and growing demand for advanced diagnostic imaging systems across countries such as China, India, and Japan. Expanding hospital networks and increasing investment in oncology care are significantly supporting market expansion. In addition, rising awareness regarding early disease detection and growing adoption of cost-effective CT simulation technologies are accelerating regional growth.

Japan Computed Tomography (CT) Simulators Market Insight

The Japan Computed Tomography (CT) Simulators market is witnessing consistent growth due to advanced healthcare systems, high adoption of precision radiotherapy, and strong focus on cancer treatment innovation. Hospitals and research institutions are increasingly integrating CT simulation technologies for accurate treatment planning and diagnostic imaging. Moreover, the country’s emphasis on technological advancement in medical imaging and increasing use of AI-enhanced radiology solutions are further supporting market development.

China Computed Tomography (CT) Simulators Market Insight

The China Computed Tomography (CT) Simulators market is growing rapidly, driven by expanding healthcare infrastructure, rising cancer burden, and strong government initiatives to improve diagnostic and treatment capabilities. Hospitals and oncology centers are increasingly adopting advanced CT simulation systems for radiation therapy planning and image-guided diagnostics. In addition, growing investment in digital healthcare technologies, rapid urbanization, and increasing access to modern medical facilities are positioning China as one of the fastest-growing markets for CT simulators globally.

Computed Tomography (CT) Simulators Market Share

The Computed Tomography (CT) Simulators industry is primarily led by well-established companies, including:

- Siemens Healthineers (Germany)

- GE HealthCare Technologies Inc. (U.S.)

- Philips Healthcare (Netherlands)

- Canon Medical Systems Corporation (Japan)

- FUJIFILM Healthcare (Japan)

- Shimadzu Corporation (Japan)

- Elekta AB (Sweden)

- Varian Medical Systems (U.S.)

- Accuray Incorporated (U.S.)

- Eizo Corporation (Japan)

- IBA Dosimetry GmbH (Germany)

- RaySearch Laboratories AB (Sweden)

- Sun Nuclear Corporation (U.S.)

- Mirada Medical (U.K.)

- LAP GmbH Laser Applikationen (Germany)

- Brainlab AG (Germany)

- Medtronic plc (Ireland)

- Hitachi Medical Systems (Japan)

- United Imaging Healthcare Co., Ltd. (China)

- ViewRay Technologies (U.S.)

- Neusoft Medical Systems (China)

- Shenzhen Anke High-tech Co., Ltd. (China)

- Samsung Medison (South Korea)

- Carestream Health (U.S.)

- Ziehm Imaging GmbH (Germany)

- Agfa HealthCare (Belgium)

- Planmed Oy (Finland)

- Orfit Industries (Belgium)

- Eckert & Ziegler BEBIG (Germany)

- Mobilis Healthcare (France)

Latest Developments in Computed Tomography (CT) Simulators Market

- In March 2021, Siemens Healthineers announced advancements in its CT simulation workflow solutions for radiation therapy planning through its SOMATOM go.Sim platform, integrating AI-powered automation to improve CT-based treatment preparation. The solution enables automated patient positioning, contouring support, and optimized imaging protocols to enhance efficiency in radiotherapy planning workflows. This development highlights the growing integration of AI-driven technologies in CT simulation systems for oncology applications

- In June 2022, Siemens Healthineers introduced enhancements in its CT simulation portfolio with advanced large-bore CT imaging systems designed for radiotherapy planning applications. The upgraded systems improved tumor visualization accuracy, patient positioning capabilities, and imaging workflow efficiency through enhanced reconstruction algorithms. This development reflects continuous innovation in CT simulation systems supporting precision oncology treatment planning

- In November 2023, clinical research and industry adoption of 4D CT simulation expanded significantly, particularly for motion-adaptive radiotherapy planning in lung and abdominal cancer treatments. The technology enabled time-resolved imaging to capture respiratory motion and improve tumor targeting accuracy. This development strengthened the shift toward dynamic CT simulation techniques in advanced radiation therapy workflows

- In October 2024, research institutions and healthcare technology developers advanced immersive CT simulation training systems designed to improve patient preparation and imaging experience. These solutions integrate virtual CT room environments and simulation-based patient guidance tools to enhance scan readiness and reduce anxiety. This development reflects increasing adoption of immersive and patient-centric CT simulation approaches in clinical environments

- In May 2025, Siemens Healthineers advanced its photon-counting CT and AI-assisted imaging technologies to enhance CT simulation accuracy for radiotherapy and diagnostic applications. The next-generation CT systems improved image resolution, reduced scan time, and lowered radiation exposure while supporting high-precision treatment planning workflows. This development underscores the transition toward AI-enabled and ultra-high-resolution CT simulation systems in oncology and cardiovascular imaging

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.