Global Cushings Disease Market

Market Size in USD Billion

USD

478.84 Billion

USD

985.36 Billion

2025

2033

USD

478.84 Billion

USD

985.36 Billion

2025

2033

| 2026 - 2033 | |

| USD 478.84 Billion | |

| USD 985.36 Billion | |

| % | |

|

Cushing’s Disease Market Size

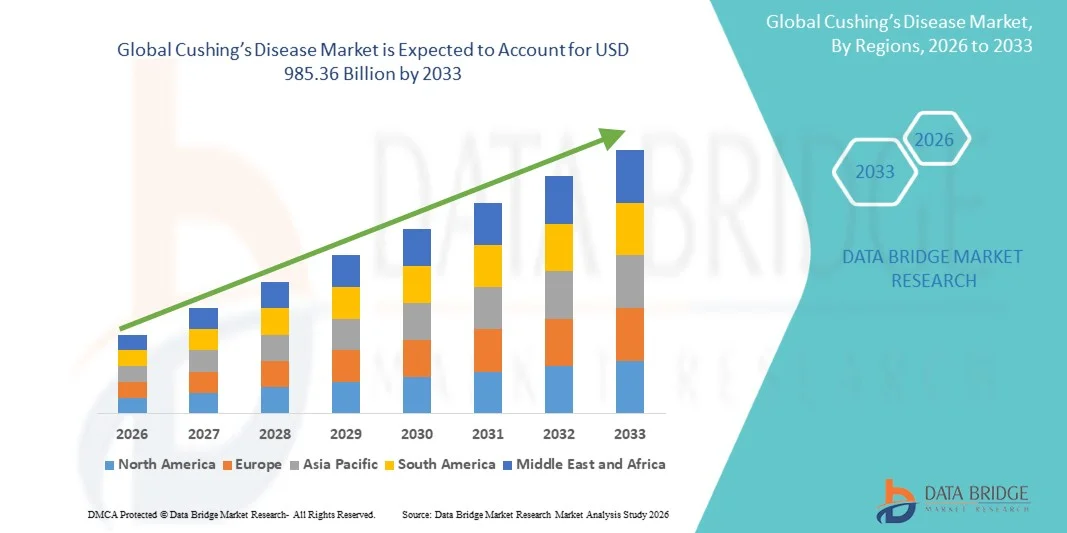

- The global Cushing’s disease market size was valued at USD 478.84 billion in 2025and is expected to reach USD 985.36 billion by 2033, at a CAGR of 9.44% during the forecast period

- The market growth is largely driven by increasing prevalence of endocrine disorders, improved diagnostic rates, and advancements in targeted pharmacological therapies and surgical interventions for hypercortisolism

- Furthermore, rising awareness among healthcare providers and patients regarding early diagnosis, coupled with expanding access to specialized endocrinology care and novel drug approvals, is strengthening treatment adoption. These converging factors are accelerating the uptake of advanced Cushing’s disease management solutions, thereby significantly boosting the industry’s growth

Cushing’s Disease Market Analysis

- Cushing’s disease is a rare endocrine disorder characterized by chronic excess cortisol production, with the market encompassing treatment options such as surgery, radiation therapy, pharmacological drugs, and other supportive management approaches, alongside diagnostic techniques and monitoring tools used in endocrinology care settings

- The market growth is primarily driven by increasing detection rates of pituitary disorders, advancements in hormonal and imaging diagnostics, rising availability of targeted medical therapies, and growing clinical preference for multidisciplinary treatment approaches combining surgery and long-term drug management

- North America dominated the Cushing’s disease market with the largest revenue share of 42.6% in 2025, supported by advanced endocrine specialty care infrastructure, high diagnostic awareness, strong adoption of novel therapies, and the presence of leading research institutions focused on pituitary and adrenal disorders

- Asia-Pacific is expected to be the fastest growing region during the forecast period due to improving access to specialized diagnostic facilities, rising healthcare investments, and increasing awareness of rare hormonal and endocrine diseases in developing healthcare systems

- The surgery segment dominated the market with a market share of 46.8% in 2025, driven by transsphenoidal surgery being the primary and most effective treatment for pituitary adenoma cases

Report Scope and Cushing’s Disease Market Segmentation

|

Attributes |

Cushing’s Disease Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Growing development of next-generation pituitary-targeted therapies and cortisol synthesis inhibitors · Expansion of AI-driven diagnostic imaging and biomarker-based screening tools |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Cushing’s Disease Market Trends

“Advancements in Targeted Therapy and Precision Endocrinology”

- A significant and accelerating trend in the global Cushing’s disease market is the growing shift toward targeted pharmacological therapies and precision-based endocrinology approaches aimed at improving cortisol control and reducing disease recurrence in complex patient populations

- For instance, in 2025, the increasing clinical use of selective cortisol synthesis inhibitors and pituitary-directed therapies is improving outcomes in patients with persistent or recurrent Cushing’s disease after surgery

- Advancements in drug development are enabling more specific mechanisms of action that directly target adrenal steroidogenesis and pituitary tumor activity, leading to improved biochemical control and reduced systemic side effects compared to older treatment options

- Furthermore, the integration of personalized treatment pathways based on tumor subtype, hormonal profile, and genetic markers is supporting more effective long-term disease management and reducing dependency on repeat surgical interventions

- Increasing use of AI-assisted imaging and advanced MRI techniques is improving tumor localization accuracy, enabling earlier intervention and more precise surgical planning in pituitary-related cases

- This trend towards more precise, targeted, and patient-specific treatment strategies is fundamentally reshaping clinical expectations for Cushing’s disease management, as companies and research institutions focus on improving efficacy and safety profiles of emerging therapies

Cushing’s Disease Market Dynamics

Driver

“Growing Need Due to Rising Diagnosis Rates and Improved Endocrine Awareness”

- The increasing recognition of rare endocrine disorders, coupled with improved diagnostic capabilities and expanding awareness among healthcare professionals, is a significant driver for the rising demand for Cushing’s disease treatment and diagnostic solutions

- For instance, in 2025, expanded use of advanced hormonal testing and MRI-based pituitary imaging is enabling earlier and more accurate identification of Cushing’s disease cases across specialized endocrine centers

- As clinicians become more aware of subtle clinical symptoms and biochemical markers, more patients are being correctly diagnosed, leading to higher treatment initiation rates and increased adoption of both surgical and pharmacological therapies

- Furthermore, the growing availability of specialized endocrine care facilities and multidisciplinary treatment approaches is improving patient access to effective disease management options across developed and emerging healthcare systems

- Rising investment in rare disease research and government-supported endocrine disorder programs is further strengthening diagnostic infrastructure and accelerating patient identification rates

- The increasing use of minimally invasive transsphenoidal surgery and long-term oral drug therapies is further propelling treatment uptake in both newly diagnosed and recurrent Cushing’s disease cases

Restraint/Challenge

“Limited Diagnosis Rates and Complex Disease Management Barriers”

- Concerns surrounding underdiagnosis, complex symptom presentation, and delayed clinical detection pose a significant challenge to broader market penetration in the global Cushing’s disease market

- For instance, many patients experience long diagnostic delays due to overlapping symptoms with other metabolic and endocrine disorders, leading to late-stage identification and complicated treatment pathways

- The rarity of the disease and limited awareness among general healthcare providers contribute to misdiagnosis or delayed referral to specialized endocrine centers, restricting timely treatment initiation

- Furthermore, managing Cushing’s disease requires long-term multidisciplinary care involving surgery, radiation, and chronic pharmacological therapy, which increases treatment complexity and healthcare burden

- High treatment costs associated with advanced therapies and repeated interventions further limit access, particularly in low- and middle-income healthcare systems

- Addressing these challenges through improved clinical education, expanded screening protocols, and better access to specialized endocrine diagnostics will be vital for sustained market growth

Cushing’s Disease Market Scope

The market is segmented on the basis of treatment type, diagnosis, route of administration, end-users, and distribution channel.

- By Treatment Type

On the basis of treatment type, the Cushing’s disease market is segmented into surgery, radiation therapy, drugs, and others. The surgery segment dominated the market with the largest revenue share of 46.8% in 2025, driven by transsphenoidal surgery being the primary and most effective treatment for pituitary adenomas causing Cushing’s disease. It is widely preferred in early and operable cases due to its potential for long-term remission and rapid cortisol normalization. Hospitals with advanced neurosurgical capabilities strongly support its adoption. High success rates in well-localized tumors further reinforce its dominance. Increasing availability of minimally invasive techniques is also improving patient outcomes. Overall, surgery remains the first-line curative approach in most clinical guidelines.

The drugs segment is expected to witness the fastest growth rate of 17.9% from 2026 to 2033, driven by increasing use in recurrent, inoperable, or residual disease cases. Pharmacological therapies are gaining traction due to the rising approval of cortisol-lowering agents and pituitary-targeted drugs. Patients unfit for surgery or radiation increasingly rely on long-term medical management. Growing research in selective steroidogenesis inhibitors is expanding treatment options. Improved oral formulations are enhancing patient compliance and accessibility. Overall, drug therapy is emerging as a key long-term disease control strategy.

- By Diagnosis

On the basis of diagnosis, the Cushing’s disease market is segmented into petrosal sinus sampling, saliva test, urine and blood tests, and imaging tests. The urine and blood tests segment dominated the market with the largest revenue share of 39.5% in 2025, driven by their widespread use as first-line screening tools for cortisol level detection. These tests are cost-effective, minimally invasive, and widely available across diagnostic laboratories and hospitals. They play a crucial role in initial endocrine evaluation before confirmatory testing. Repeated testing capability improves diagnostic accuracy in suspected cases. High adoption in both developed and emerging healthcare systems supports dominance. Overall, they remain the foundation of Cushing’s disease diagnosis.

The petrosal sinus sampling segment is expected to witness the fastest growth rate of 16.4% from 2026 to 2033, driven by its high diagnostic precision in differentiating pituitary from ectopic ACTH secretion. It is increasingly used in complex or ambiguous cases where imaging results are inconclusive. Growing availability of advanced interventional radiology facilities is supporting adoption. Its role in treatment planning for surgery is becoming more critical. Increasing referrals to tertiary endocrine centers is further boosting utilization. Overall, it is emerging as a gold-standard confirmatory diagnostic tool in complex cases.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, and others. The oral segment dominated the market with the largest revenue share of 58.2% in 2025, driven by the widespread use of oral cortisol-lowering medications for long-term disease management. Oral drugs are preferred due to ease of administration and improved patient compliance in chronic therapy settings. They are especially important for patients with persistent or recurrent Cushing’s disease. Expanding availability of targeted oral inhibitors is further strengthening adoption. Outpatient-based management significantly supports oral drug usage. Overall, oral therapy remains the backbone of pharmacological treatment.

The parenteral segment is expected to witness the fastest growth rate of 15.8% from 2026 to 2033, driven by increasing use of injectable formulations in severe or rapidly progressing cases. Parenteral drugs offer faster therapeutic action in acute hypercortisolism management. They are increasingly used in hospital-based endocrine emergencies. Advancements in long-acting injectable formulations are improving treatment effectiveness. Rising hospitalization rates for complicated cases further support demand. Overall, parenteral therapy is gaining importance in critical care settings.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, specialty clinics, homecare, and others. The hospitals segment dominated the market with the largest revenue share of 52.3% in 2025, driven by the availability of advanced diagnostic infrastructure, neurosurgical facilities, and multidisciplinary endocrine care. Hospitals are the primary centers for both diagnosis and surgical treatment of Cushing’s disease. They also support complex procedures such as pituitary surgery and petrosal sinus sampling. Strong patient inflow and referral systems reinforce hospital dominance. Availability of intensive post-operative care further supports usage. Overall, hospitals remain the core treatment hub for disease management.

The specialty clinics segment is expected to witness the fastest growth rate of 18.6% from 2026 to 2033, driven by increasing preference for specialized endocrine consultation and long-term disease monitoring. These clinics offer focused care for hormonal disorders with faster diagnosis and personalized treatment plans. Rising awareness of rare diseases is boosting patient visits to specialty centers. Improved accessibility compared to large hospitals supports growth. Integration with diagnostic labs enhances efficiency and care delivery. Overall, specialty clinics are emerging as key outpatient management centers.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The hospital pharmacy segment dominated the market with the largest revenue share of 61.4% in 2025, driven by the high dependence on hospital-based dispensing of specialized endocrine drugs and post-surgical medications. Most Cushing’s disease treatments are initiated and monitored in hospital settings. Controlled dispensing ensures proper dosage and patient safety. Availability of critical and high-cost medications further strengthens hospital pharmacy dominance. Integration with inpatient care pathways supports seamless treatment delivery. Overall, hospital pharmacies remain the primary distribution channel.

The online pharmacy segment is expected to witness the fastest growth rate of19.2% from 2026 to 2033, driven by increasing digital healthcare adoption and improved access to chronic disease medications. Online platforms offer convenience for long-term prescription refills and home delivery. Rising telemedicine consultations are further boosting online prescriptions. Patients in remote areas benefit from improved drug accessibility. Expanding regulatory acceptance of e-pharmacies supports market expansion. Overall, online pharmacies are emerging as a growing channel for long-term endocrine therapy management.

Cushing’s Disease Market Regional Analysis

- North America dominated the Cushing’s disease market with the largest revenue share of 42.6% in 2025, supported by advanced endocrine specialty care infrastructure, high diagnostic awareness, strong adoption of novel therapies, and the presence of leading research institutions focused on pituitary and adrenal disorders

- Patients in the region benefit from early access to advanced diagnostic tools such as hormonal assays, MRI imaging, and petrosal sinus sampling, which significantly improve disease detection and management outcomes

- This widespread leadership is further supported by high healthcare expenditure, strong clinical research activity in rare endocrine disorders, and rapid adoption of novel pharmacological therapies, establishing North America as the key hub for Cushing’s disease treatment

U.S. Cushing’s Disease Market Insight

The U.S. Cushing’s disease market captured the largest revenue share of 79% in 2025 within North America, fueled by high diagnosis rates, advanced endocrine care infrastructure, and strong availability of specialized pituitary treatment centers. Patients increasingly benefit from early access to sophisticated diagnostic tools such as hormonal assays, MRI imaging, and petrosal sinus sampling. The growing adoption of targeted pharmacological therapies and minimally invasive transsphenoidal surgery further strengthens treatment outcomes. Moreover, strong clinical research activity and rapid uptake of novel endocrine drugs are significantly contributing to market expansion.

Europe Cushing’s Disease Market Insight

The Europe Cushing’s disease market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of rare endocrine disorders and strong healthcare systems supporting early diagnosis. The region benefits from well-established endocrinology networks and access to advanced imaging and hormonal testing facilities. Growing emphasis on standardized clinical guidelines is improving treatment consistency across countries. Furthermore, rising investment in rare disease research and increasing availability of targeted therapies are fostering market growth across both hospital and specialty care settings.

U.K. Cushing’s Disease Market Insight

The U.K. Cushing’s disease market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by improved diagnostic capabilities and increasing recognition of endocrine disorders among healthcare professionals. Rising patient referrals to specialized endocrine centers are supporting early and accurate diagnosis. The country’s strong public healthcare system enables broader access to advanced imaging and hormonal testing. In addition, growing use of minimally invasive surgical procedures and expanding availability of novel drug therapies are further supporting market growth across the treatment landscape.

Germany Cushing’s Disease Market Insight

The Germany Cushing’s disease market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure and strong focus on precision medicine and early disease detection. Increasing adoption of high-resolution imaging and endocrine biomarker testing is improving diagnostic accuracy. Germany’s emphasis on innovation in medical technologies is supporting the use of minimally invasive pituitary surgery and targeted pharmacological therapies. Furthermore, strong integration of research institutions with clinical practice is accelerating the adoption of new treatment approaches for rare endocrine disorders.

Asia-Pacific Cushing’s Disease Market Insight

The Asia-Pacific Cushing’s disease market is poised to grow at the fastest CAGR of 22% during 2026 to 2033, driven by improving healthcare infrastructure, rising awareness of rare diseases, and increasing access to endocrine diagnostics. Growing investments in hospital modernization and expanding availability of MRI and hormonal testing are enhancing early detection rates. Government initiatives to strengthen healthcare systems are further supporting market expansion. In addition, increasing adoption of advanced therapies and rising medical tourism in the region are contributing to accelerated growth across both public and private healthcare sectors.

Japan Cushing’s Disease Market Insight

The Japan Cushing’s disease market is gaining momentum due to the country’s advanced healthcare system, high focus on precision diagnostics, and strong emphasis on early disease detection. Widespread use of advanced imaging technologies and hormonal assays is improving diagnostic accuracy for pituitary disorders. The integration of multidisciplinary care approaches in hospitals is supporting better treatment outcomes. Furthermore, increasing adoption of minimally invasive neurosurgical techniques and growing availability of targeted drug therapies are driving market expansion in both inpatient and outpatient care settings.

India Cushing’s Disease Market Insight

The India Cushing’s disease market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to improving healthcare access, expanding diagnostic infrastructure, and rising awareness of endocrine disorders. Increasing availability of affordable MRI and hormonal testing facilities is enabling better disease identification. Growth in specialty endocrine clinics and expanding hospital networks is supporting treatment adoption. Furthermore, rising healthcare expenditure, increasing penetration of advanced pharmacological therapies, and gradual improvement in rare disease awareness are key factors propelling market growth in the country.

Cushing’s Disease Market Share

The Cushing’s Disease industry is primarily led by well-established companies, including:

- Corcept Therapeutics Incorporated (U.S.)

- Novartis AG (Switzerland)

- Recordati S.p.A. (Italy)

- Pfizer Inc. (U.S.)

- Ipsen S.A. (France)

- Xeris Biopharma Holdings, Inc. (U.S.)

- Crinetics Pharmaceuticals, Inc. (U.S.)

- Amryt Pharma plc (Ireland)

- H. Lundbeck A/S (Denmark)

- Merck & Co., Inc. (U.S.)

- Novo Nordisk A/S (Denmark)

- AstraZeneca (U.K.)

- Bristol Myers Squibb Company (U.S.)

- AbbVie Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Sanofi (France)

- HRA Pharma (France)

- Strongbridge Biopharma plc (Ireland)

What are the Recent Developments in Global Cushing’s Disease Market?

- In January 2026, Major updated clinical recommendations for Cushing’s disease management were published, emphasizing a shift toward personalized treatment strategies, long-term medical therapy optimization, and combination approaches for recurrent cases. The update highlights increasing reliance on pharmacological interventions when surgery is not fully curative and strengthens standardized monitoring of cortisol levels for relapse prevention

- In March 2025, Clinical adoption of osilodrostat (Isturisa) continued to expand in 2025 as real-world evidence supported its effectiveness in controlling excess cortisol production in endogenous C ushing’s disease. The drug demonstrated strong biochemical response rates in patients with persistent or recurrent disease after surgery

- In June 2024, Regulatory refinements in 2024 supported continued clinical use of mifepristone (Korlym) for patients with Cushing’s syndrome and related hypercortisolism conditions. The drug remained an important option for patients with comorbid type 2 diabetes or glucose intolerance who are not eligible for surgery

- In October 2022, The FDA expanded treatment options with the approval of levoketoconazole (Recorlev), a next-generation oral steroidogenesis inhibitor for endogenous Cushing’s syndrome. The therapy showed improved cortisol suppression compared to earlier ketoconazole-based treatments. It became an important option for patients with persistent disease or those unsuitable for surgery

- In August 2021, Clinical use of pasireotide (Signifor) expanded in 2021 as an important therapy for patients with persistent or recurrent Cushing’s disease. It works by inhibiting ACTH secretion from pituitary tumors, directly targeting disease pathology. Despite its effectiveness, metabolic side effects such as hyperglycemia influenced patient selection and monitoring strategies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.