Global Custom Healthcare Software Market

Market Size in USD Billion

USD

18.42 Billion

USD

43.68 Billion

2025

2033

USD

18.42 Billion

USD

43.68 Billion

2025

2033

| 2026 - 2033 | |

| USD 18.42 Billion | |

| USD 43.68 Billion | |

| % | |

|

Custom Healthcare Software Market Overview

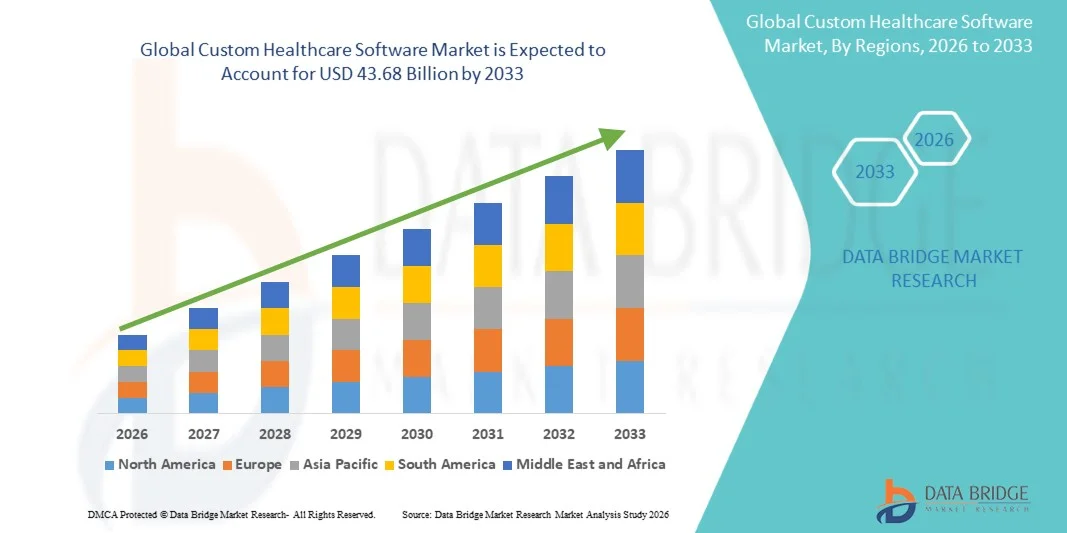

As per Data Bridge Market Research analysis The custom healthcare software market was valued at USD 18.42 billion in 2025 and is projected to reach USD 43.68 billion by 2033, growing at a CAGR of 11.40% from 2026 to 2033. The market is experiencing substantial growth driven by the increasing digitalization of healthcare systems, rising demand for personalized healthcare solutions, and the growing need for efficient management of clinical, administrative, and patient-related data.

The rapid adoption of electronic health records (EHRs), telehealth platforms, remote patient monitoring systems, and healthcare analytics solutions is encouraging healthcare providers to invest in customized software tailored to their operational requirements. In addition, evolving regulatory compliance standards, increasing focus on interoperability, and the need for enhanced patient engagement are accelerating demand for custom healthcare software across hospitals, clinics, diagnostic centers, and healthcare payer organizations. These solutions offer improved workflow efficiency, data security, scalability, and seamless integration with existing healthcare infrastructure, making them an essential component of modern healthcare transformation initiatives worldwide.

Market Size & Forecast

- Global Market Value (2025): USD 18.42 Billion

- Expected Market Value (2033): USD 43.68 Billion

- Forecast CAGR (2026–2033): 11.40%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Key Market Trends & Insights

- North America dominated the custom healthcare software market with the largest revenue share of 38.62% in 2025, supported by widespread healthcare IT adoption, strong digital health investments, and the presence of leading software developers and healthcare providers.

- The Electronic Health Records (EHR) & Electronic Medical Records (EMR) segment led the market with a 31.84% share in 2025, driven by increasing regulatory requirements for digital recordkeeping and the widespread adoption of healthcare information technologies.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 9.1% from 2026 to 2033, fueled by expanding healthcare digitization initiatives, increasing healthcare expenditures, and rising adoption of customized software solutions across China, India, and Southeast Asia.

- Telehealth & Telemedicine Software are the fastest-growing software type, projected to register a CAGR of 9.4%, reflecting the surge in demand for virtual healthcare services and remote patient engagement.

- The Cloud-Based segment dominated the deployment mode category with a 44.83% revenue share in 2025, led by its scalability, flexibility, and cost-effectiveness.

- Clinical Management accounted for 28.76% of the market, preferred by the increasing need for efficient healthcare delivery and workflow optimization.

- The Healthcare Analytics & Reporting segment is the fastest-growing application category, with a CAGR of 9.0%, driven by demand for data-driven decision-making is encouraging healthcare organizations to invest in advanced analytics solutions

Report Scope and Custom Healthcare Software Market Segmentation

|

Attributes |

Custom Healthcare Software Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Oracle Corporation (U.S.) · Epic Systems Corporation (U.S.) · Veradigm LLC (U.S.) · athenahealth, Inc. (U.S.) · eClinicalWorks LLC (U.S.) · NextGen Healthcare, Inc. (U.S.) · Greenway Health, LLC (U.S.) · Medical Information Technology, Inc. (U.S.) · NXGN Management, LLC (U.S.) · AdvancedMD, Inc. (U.S.) · Intersystems Corporation (U.S.) · Dedalus Group (Italy) · CompuGroup Medical SE & Co. KGaA (Germany) · TPP (U.K.) · Sectra AB (Sweden) · Altera Digital Health Inc. (U.S.) · WellSky Corporation (U.S.) · TELUS Health (Canada) · Cegedim SA (France) · Cambio Healthcare Systems AB (Sweden) |

|

Market Opportunities |

· Growing demand for interoperable healthcare ecosystems · The rapid expansion of AI-driven clinical decision support and predictive analytics · Increasing adoption of value-based care models |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Custom Healthcare Software Market Trends

Trend: Growing Adoption of Personalized and Patient-Centric Digital Healthcare Solutions

Healthcare providers are increasingly adopting custom healthcare software to deliver personalized patient experiences, streamline clinical workflows, and improve care coordination across multiple touchpoints. The integration of artificial intelligence, predictive analytics, and patient engagement tools enables healthcare organizations to tailor treatment plans, automate administrative processes, and enhance clinical decision-making. Hospitals, specialty clinics, and healthcare networks are similarly leveraging customized platforms to address unique operational requirements, while cloud computing and mobile health technologies create connected ecosystems that support continuous patient monitoring and real-time access to healthcare information.

For instance, in March 2025, Oracle Health expanded its healthcare technology capabilities with enhanced AI-powered clinical workflow solutions, supporting more personalized and data-driven patient care delivery.

Custom Healthcare Software Market Dynamics

Key Market Driver: Increasing Digital Transformation Across Healthcare Organizations

The rapid digital transformation of healthcare systems and the growing adoption of electronic health records, telehealth platforms, and data analytics solutions have created substantial demand for custom healthcare software that can address organization-specific requirements. Hospitals, healthcare providers, and payer organizations are deploying customized software as a core component of their digital strategy, improving operational efficiency, strengthening patient engagement, and ensuring compliance with evolving healthcare regulations while enabling seamless interoperability across diverse healthcare environments.

For instance, in February 2025, Epic Systems Corporation introduced new interoperability and AI-driven healthcare management enhancements, enabling providers to improve data exchange and patient care coordination across integrated healthcare networks.

Key Restraint/Challenge: High Development and Integration Costs of Custom Healthcare Software

A significant restraint in the global custom healthcare software market is the high investment required for software development, system integration, and ongoing maintenance. Modern healthcare platforms incorporate advanced analytics, cybersecurity frameworks, interoperability standards, and regulatory compliance features, demanding substantial expenditure on development, deployment, and continuous upgrades. The total cost of ownership extends to staff training, infrastructure modernization, and technical support, making adoption challenging for smaller healthcare facilities, independent clinics, and resource-constrained organizations.

For instance, in January 2025, several regional healthcare providers across North America delayed large-scale software modernization initiatives due to rising implementation expenses and integration complexities associated with legacy healthcare systems.

Key Market Opportunity: Expansion of AI-Driven Healthcare Analytics and Clinical Decision Support

The integration of artificial intelligence in custom healthcare software presents a significant market opportunity. AI-enabled platforms can deliver predictive analytics, automate clinical documentation, enhance diagnostic accuracy, and support personalized treatment recommendations. The development of cloud-native healthcare applications and interoperable digital health ecosystems is further expanding access to advanced healthcare technologies, creating growth opportunities across hospitals, clinics, and emerging healthcare markets throughout Asia-Pacific, Latin America, and the Middle East.

For instance, in April 2025, Microsoft Cloud for Healthcare expanded its AI healthcare capabilities to support advanced clinical insights, care management, and data-driven decision-making across healthcare organizations.

Custom Healthcare Software Market Scope

The custom healthcare software market is segmented on the basis of software type, deployment mode, application, and end user.

- By Software Type

On the basis of software type, the custom healthcare software market is segmented into Electronic Health Records (EHR) & Electronic Medical Records (EMR), Hospital Information Systems (HIS), Practice Management Software, Revenue Cycle Management (RCM), Telehealth & Telemedicine Software, Healthcare Analytics Software, Patient Engagement Software, Laboratory Information Management Systems (LIMS), and Pharmacy Management Software. The Electronic Health Records (EHR) & Electronic Medical Records (EMR) segment dominated the market with a 31.84% share in 2025, driven by increasing regulatory requirements for digital recordkeeping and the widespread adoption of healthcare information technologies. Healthcare providers rely on customized EHR and EMR platforms to improve patient data management, streamline clinical workflows, and enhance care coordination. These solutions enable real-time access to patient information across multiple departments and facilities. Growing demand for interoperability and secure health information exchange is further supporting adoption. Continuous investments in healthcare digitization initiatives are strengthening market penetration. Their central role in modern healthcare infrastructure continues to reinforce segment dominance globally.

The Telehealth & Telemedicine Software segment is projected to register the fastest growth at a CAGR of 9.4% from 2026 to 2033, driven by the increasing demand for virtual healthcare services and remote patient engagement. Healthcare organizations are investing in customized telehealth platforms to improve accessibility and reduce care delivery costs. These solutions support video consultations, remote monitoring, and digital care coordination. Advancements in cloud computing, mobile health applications, and connected medical devices are enhancing functionality and user experience. Rising acceptance of virtual healthcare among patients and providers is accelerating adoption. Expanding healthcare access in underserved and rural regions is further contributing to segment growth.

- By Deployment Mode

On the basis of deployment mode, the custom healthcare software market is segmented into cloud-based, on-premises, and hybrid. The Cloud-Based segment accounted for the largest market share of 44.83% in 2025, owing to its scalability, flexibility, and cost-effectiveness. Healthcare organizations increasingly prefer cloud-based custom software solutions due to lower infrastructure requirements and simplified maintenance. These platforms enable seamless data access across multiple locations and support remote healthcare delivery models. Growing adoption of software-as-a-service (SaaS) solutions is further strengthening demand. Enhanced cybersecurity measures and compliance capabilities are improving confidence in cloud deployments. The ability to rapidly deploy updates and integrate emerging technologies continues to support segment leadership.

The Hybrid segment is expected to witness the fastest growth at a CAGR of 8.8% from 2026 to 2033, driven by the need to balance security, compliance, and operational flexibility. Hybrid deployment models allow healthcare organizations to maintain sensitive patient information on-premises while leveraging cloud resources for scalability and collaboration. This approach supports gradual digital transformation without disrupting existing infrastructure. Increasing concerns regarding data privacy and regulatory compliance are encouraging adoption. Healthcare providers are also utilizing hybrid systems to optimize performance and disaster recovery capabilities. Growing demand for customized and interoperable healthcare ecosystems is accelerating market expansion.

- By Application

On the basis of application, the custom healthcare software market is segmented into clinical management, patient management, telehealth & remote patient monitoring, billing & revenue cycle management, healthcare analytics & reporting, inventory & supply chain management, compliance & regulatory management, and other applications. The Clinical Management segment dominated the market with a 28.76% share in 2025, driven by the increasing need for efficient healthcare delivery and workflow optimization. Custom clinical management software helps healthcare providers automate documentation, treatment planning, and patient care coordination. These solutions improve clinical decision-making through real-time access to patient information and evidence-based insights. Hospitals and healthcare systems continue to invest heavily in customized clinical platforms to improve outcomes and operational efficiency. Growing patient volumes and increasing complexity of healthcare services are further supporting adoption. The segment remains critical to healthcare digital transformation initiatives worldwide.

The Healthcare Analytics & Reporting segment is projected to be the fastest-growing application segment at a CAGR of 9.0% from 2026 to 2033. Rising demand for data-driven decision-making is encouraging healthcare organizations to invest in advanced analytics solutions. These platforms enable predictive modeling, population health management, and performance monitoring. Artificial intelligence and machine learning technologies are significantly enhancing analytical capabilities. Healthcare providers are increasingly using analytics to improve resource allocation, reduce costs, and enhance patient outcomes. The growing importance of value-based care models is further accelerating demand. Continuous growth in healthcare data volumes is creating substantial opportunities for expansion.

- By End User

On the basis of end user, the custom healthcare software market is segmented into hospitals, clinics, ambulatory surgical centers, diagnostic & imaging centers, pharmaceutical & biotechnology companies, healthcare payers, and government healthcare organizations. The Hospitals segment led the market with a 42.18% revenue share in 2025, driven by extensive investments in healthcare IT infrastructure and digital transformation initiatives. Hospitals require customized software solutions to manage complex clinical, administrative, and financial operations. These organizations utilize integrated platforms for patient records management, workflow automation, telehealth services, and analytics. Increasing patient volumes and the need for coordinated care delivery continue to support adoption. Regulatory compliance requirements and interoperability demands are also contributing to market growth. The segment benefits from substantial healthcare technology spending globally.

The Pharmaceutical & Biotechnology Companies segment is anticipated to register the fastest growth at a CAGR of 9.2% from 2026 to 2033, driven by increasing investments in research, clinical trials, and drug development activities. Custom healthcare software enables efficient management of research data, regulatory documentation, and clinical study workflows. These organizations are increasingly adopting advanced analytics and artificial intelligence tools to accelerate innovation and improve decision-making. Growing demand for personalized medicine and precision healthcare is further supporting software adoption. Enhanced collaboration across research ecosystems is creating additional opportunities. Expanding biopharmaceutical development activities worldwide continue to fuel rapid segment growth.

Custom Healthcare Software Market Regional Analysis

North America dominated the custom healthcare software market with the largest revenue share of 38.62% in 2025, supported by widespread healthcare IT adoption, strong digital health investments, and the presence of leading software developers and healthcare providers. The region also benefits from stringent healthcare compliance requirements, high adoption of cloud-based and AI-enabled healthcare platforms, and growing use of customized software across hospitals, clinics, and payer organizations. Increasing focus on interoperability, patient-centered care, and data-driven clinical decision-making continues to strengthen North America’s leadership position in the global market.

U.S. Custom Healthcare Software Market Insight

The U.S. custom healthcare software market is witnessing strong growth due to rising investments in healthcare digitalization initiatives, patient-centered care programs, and advanced health information management technologies. The country’s mature healthcare ecosystem, along with increasing adoption of AI-powered, cloud-based, and interoperable software solutions, is driving demand across hospitals, clinics, and payer organizations. In addition, growing emphasis on improving clinical outcomes, enhancing operational efficiency, and meeting regulatory compliance requirements is accelerating custom healthcare software adoption across healthcare providers and life sciences companies.

Europe Custom Healthcare Software Market Insight

The Europe custom healthcare software market remains a major contributor to global revenue, driven by strong government support, healthcare modernization efforts, and high demand for advanced digital healthcare solutions. The widespread use of customized software in hospitals, healthcare networks, and public health systems is supporting market expansion across the region. Increasing investments in healthcare interoperability technologies, coupled with strict data protection regulations and a highly skilled healthcare workforce, continue to enhance the adoption of custom healthcare software throughout Europe.

U.K. Custom Healthcare Software Market Insight

The U.K. custom healthcare software market is experiencing steady growth, supported by rising adoption of digital health technologies in patient management, clinical operations, and healthcare administration. Increasing investments in healthcare IT infrastructure and growing demand for scalable, secure, and customized software solutions are contributing to market growth. Furthermore, integration of artificial intelligence, cloud computing, and healthcare analytics technologies is improving operational efficiency and patient care delivery, positioning the U.K. as a key innovation hub in the custom healthcare software industry.

Germany Custom Healthcare Software Market Insight

The Germany custom healthcare software market is expanding steadily due to the country’s advanced healthcare infrastructure, strong technological capabilities, and increasing adoption of next-generation healthcare software solutions. Healthcare providers, research institutions, and payer organizations are increasingly utilizing customized platforms for patient management, clinical workflows, and data analytics activities. Continuous advancements in AI integration, cloud technologies, and healthcare interoperability standards, along with strong government focus on healthcare modernization and efficiency, are further driving market growth in Germany.

Asia-Pacific Custom Healthcare Software Market Insight

The Asia-Pacific custom healthcare software market is expected to witness rapid growth, driven by increasing healthcare expenditures, expanding digital health infrastructure, and rising investments in healthcare technology across countries such as China, India, and Japan. Growing awareness regarding efficient healthcare delivery, rising adoption of cloud-based healthcare solutions, and increasing demand for scalable and cost-effective software platforms are supporting regional market expansion. In addition, the growing presence of healthcare innovation centers and digital transformation initiatives is accelerating software adoption across healthcare providers and research organizations.

Japan Custom Healthcare Software Market Insight

The Japan custom healthcare software market is witnessing consistent growth due to rising investments in healthcare digital transformation, medical technology innovation, and patient care optimization initiatives. Healthcare providers, pharmaceutical companies, and research institutions are increasingly adopting customized software solutions for clinical management, healthcare analytics, and operational efficiency purposes. Moreover, increasing integration of artificial intelligence technologies and the country’s focus on efficient and high-quality healthcare delivery are further contributing to market growth.

China Custom Healthcare Software Market Insight

The China custom healthcare software market is growing rapidly, driven by increasing healthcare modernization efforts, expanding healthcare infrastructure, and rising government focus on digital health transformation and patient care improvement. Growing adoption of AI-enabled and cloud-based healthcare software platforms across hospitals, clinics, and healthcare networks is significantly boosting market demand. In addition, rising investments in healthcare IT, increasing awareness regarding data-driven healthcare management, and rapid technological advancements are positioning China as one of the fastest-growing markets for custom healthcare software globally.

Custom Healthcare Software Market Share

The custom healthcare software industry is primarily led by well-established companies, including:

- Oracle Corporation (U.S.)

- Epic Systems Corporation (U.S.)

- Veradigm LLC (U.S.)

- athenahealth, Inc. (U.S.)

- eClinicalWorks LLC (U.S.)

- NextGen Healthcare, Inc. (U.S.)

- Greenway Health, LLC (U.S.)

- Medical Information Technology, Inc. (U.S.)

- NXGN Management, LLC (U.S.)

- AdvancedMD, Inc. (U.S.)

- Intersystems Corporation (U.S.)

- Dedalus Group (Italy)

- CompuGroup Medical SE & Co. KGaA (Germany)

- TPP (U.K.)

- Sectra AB (Sweden)

- Altera Digital Health Inc. (U.S.)

- WellSky Corporation (U.S.)

- TELUS Health (Canada)

- Cegedim SA (France)

- Cambio Healthcare Systems AB (Sweden)

Latest Developments in Custom Healthcare Software Market

- In March 2025, Oracle Health announced the expanded availability of its Clinical AI Agent across more than 30 medical specialties. The AI-powered assistant automates clinical documentation, reduces physician documentation time by nearly 30%, and streamlines clinical workflows through multimodal voice and screen-driven interactions. The development strengthens AI integration into custom healthcare software for hospitals and health systems

- In January 2025, Tempus AI announced the national launch of "olivia," an AI-enabled personal health concierge application. The platform integrates with over 1,000 electronic health record (EHR) systems, allowing patients to centralize health data, receive AI-generated summaries, and improve engagement through personalized healthcare insights. The launch highlights growing demand for customized, AI-driven patient engagement software

- In October 2024, Oracle Health unveiled its next-generation cloud-native Electronic Health Record (EHR) platform. Built on Oracle Cloud Infrastructure, the solution embeds AI across clinical workflows to simplify documentation, enhance interoperability, improve patient care, and streamline administrative operations. The platform represents a major advancement in customizable healthcare software solutions

- In June 2024, Oracle announced the general availability of Oracle Clinical Digital Assistant for ambulatory clinics in the United States. The AI-powered solution combines generative AI, voice recognition, and clinical intelligence to automate documentation, reduce administrative burden, and improve physician productivity through seamless integration with Oracle Health EHR systems

- In September 2022, Oracle Corporation completed its acquisition of Cerner Corporation, creating Oracle Health and significantly expanding its healthcare software portfolio. The acquisition accelerated the development of cloud-based EHRs, AI-enabled clinical applications, interoperability solutions, and customized healthcare software for providers, payers, and life sciences organizations worldwide

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.