Global Custom Pulses Market

Market Size in USD Billion

USD

67.88 Billion

USD

93.05 Billion

2025

2033

USD

67.88 Billion

USD

93.05 Billion

2025

2033

| 2026 - 2033 | |

| USD 67.88 Billion | |

| USD 93.05 Billion | |

| % | |

|

Custom Pulses Market Overview

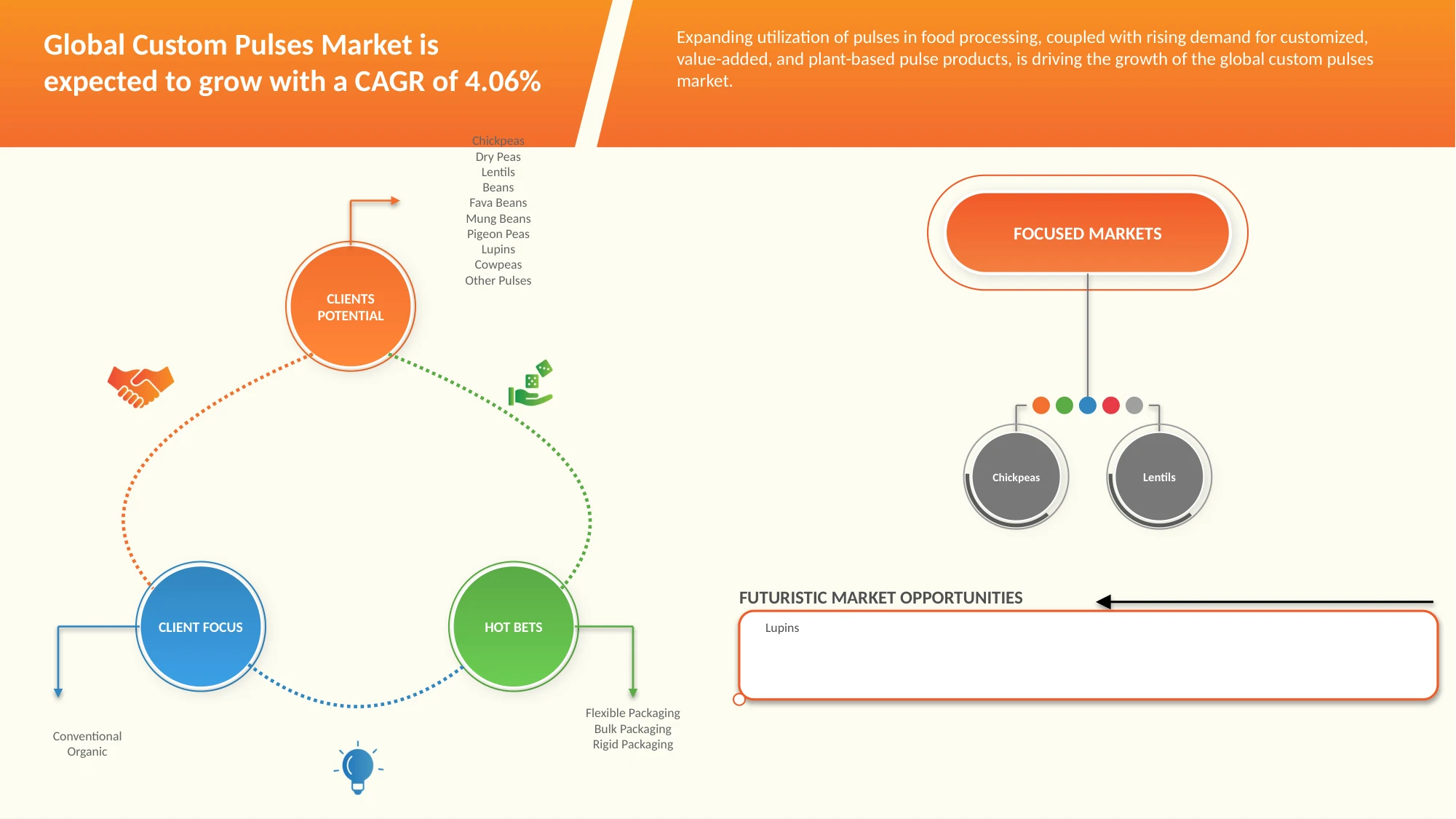

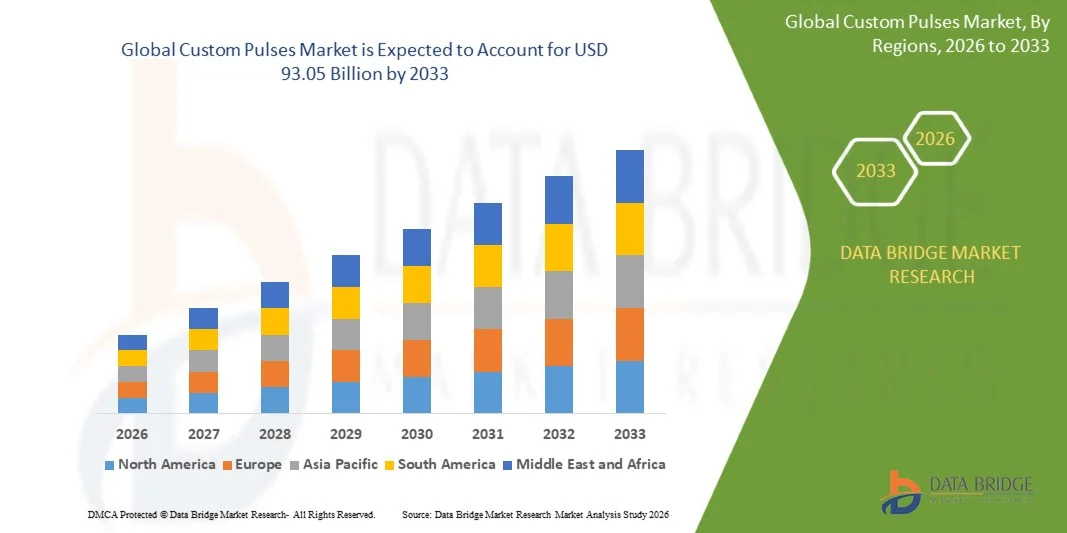

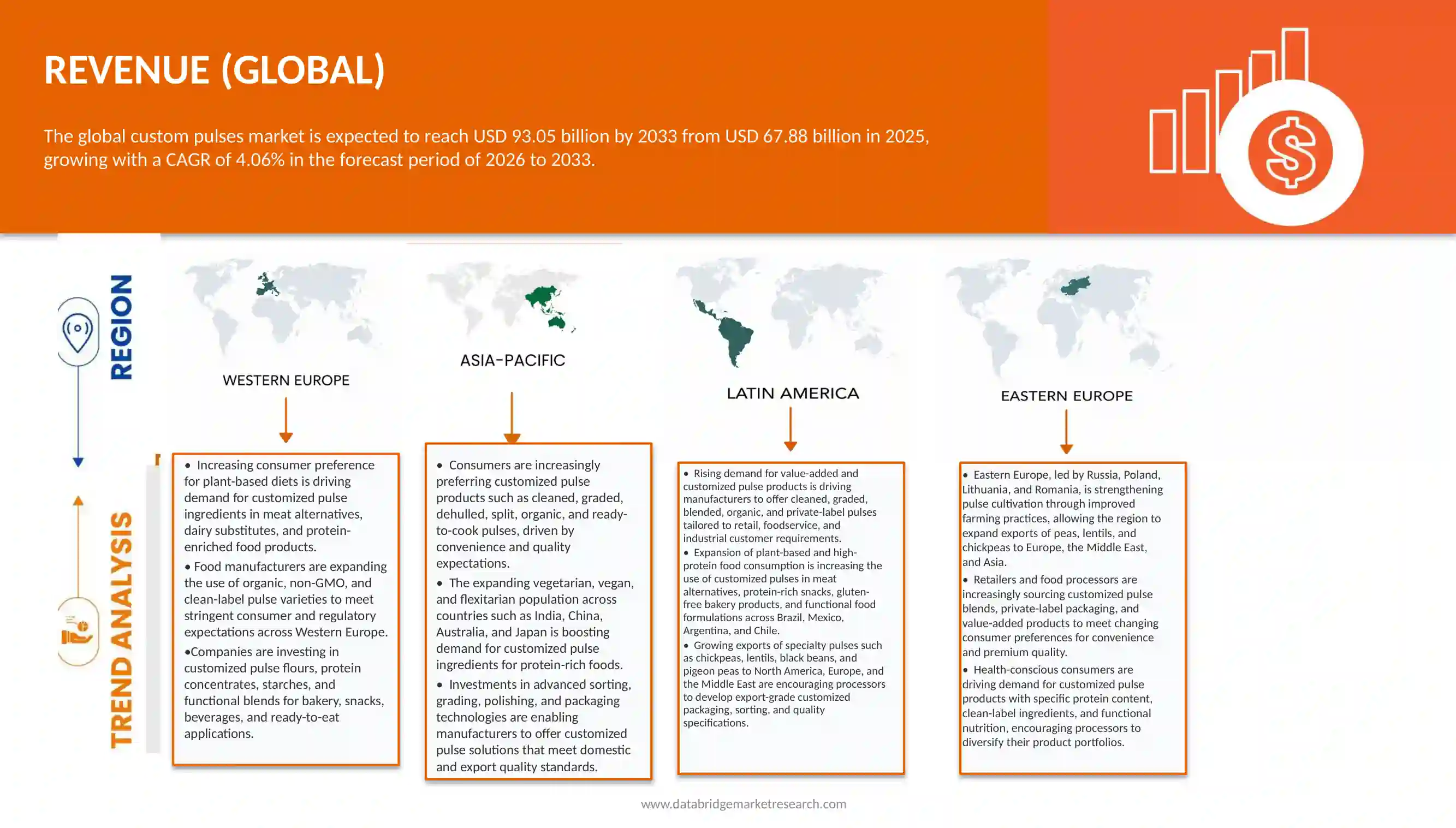

The custom pulses market was valued at USD 67.88 billion in 2025 and is projected to reach USD 93.05 billion by 2033, growing at a CAGR of 4.06% from 2026 to 2033. The increasing implementation of regulations aimed at reducing plastic packaging waste is driving demand in the custom pouches market. Rapid adoption of recyclable, mono-material, and lightweight pouch packaging across food & beverage, pharmaceuticals, personal care, and household products is encouraging manufacturers to replace conventional rigid plastic packaging with more sustainable custom pouch solutions.

At the same time, stringent environmental regulations and circular economy initiatives are accelerating the shift toward eco-friendly packaging materials. Major packaging companies are investing in recyclable films, bio-based materials, and advanced pouch technologies while expanding sustainable packaging portfolios to meet evolving regulatory requirements. Countries such as the United States, Germany, China, Japan, and India are emerging as key markets for custom pouches due to strong sustainability initiatives, growing consumer preference for environmentally responsible packaging, and increasing investments in flexible packaging innovations.

Market Size & Forecast

- Market Value (2025): USD 67.88 Billion

- Expected Market Value (2033): USD 93.05 Billion

- Forecast CAGR (2026–2033): 4.06%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- Asia-Pacific dominated the custom pulses market with the largest revenue share of 56.87% in 2025, driven by its position as one of the world's largest producers and consumers of pulses, extensive agricultural base, rising demand for customized pulse blends, expanding food processing industry, and growing consumption of protein-rich foods. Increasing investments in value-added pulse processing, favorable government initiatives supporting pulse cultivation, and rising exports of customized pulse products further strengthened the country's market leadership.

- The chickpeas segment led the market with a 17.08% share in 2025, owing to its widespread consumption across households and foodservice, high nutritional value, versatility in traditional and processed food applications, and increasing demand for protein-rich ingredients. Strong utilization in flour, snacks, ready-to-cook products, and customized pulse blends, along with expanding export demand, reinforced the segment's dominant position.

- Asia-Pacific is expected to be the fastest-growing region, registering a CAGR of 4.23% during 2026–2033, supported by increasing health awareness, growing preference for plant-based proteins, rising urbanization, expansion of organized retail, and rapid growth of the food processing sector. Government support for pulse production, technological advancements in sorting and processing, and increasing demand for customized pulse products from domestic and international markets are expected to further accelerate market growth.

- The chickpeas segment is projected to be the fastest-growing pulse type, with a CAGR of 5.05% during the forecast period, reflecting increasing consumer demand for nutritious, gluten-free, and high-protein foods. Expanding applications in plant-based foods, functional ingredients, ready-to-eat meals, and healthy snack products are further driving demand for customized chickpea products.

- The conventional segment dominated the category segment with 82.67% revenue share in 2025, driven by its broad availability, cost competitiveness, established cultivation practices, and widespread acceptance across household, foodservice, and industrial applications. Consistent supply chains, stable pricing, and strong demand from traditional food manufacturers have reinforced the segment's leading position across the

- The mass market segment accounted for 64.29% of the market in 2025, supported by high consumer demand for affordable staple foods, extensive distribution through supermarkets, traditional retail outlets, and wholesale channels, along with increasing consumption of customized pulse products by mainstream households. Competitive pricing and large-scale production capabilities continue to support the segment's dominance.

- The specialty / value-added segment is anticipated to be the fastest-growing category, registering a CAGR of 4.78% during 2026–2033, driven by increasing demand for premium-quality, organic, fortified, sprouted, and customized pulse products. Rising consumer preference for clean-label, functional, and plant-based nutrition, coupled with innovations in pulse processing, packaging, and value-added product development, is expected to accelerate growth across the custom pulses market.

Report Scope and Custom Pulses Market Segmentation

|

Attributes |

Custom Pulses Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

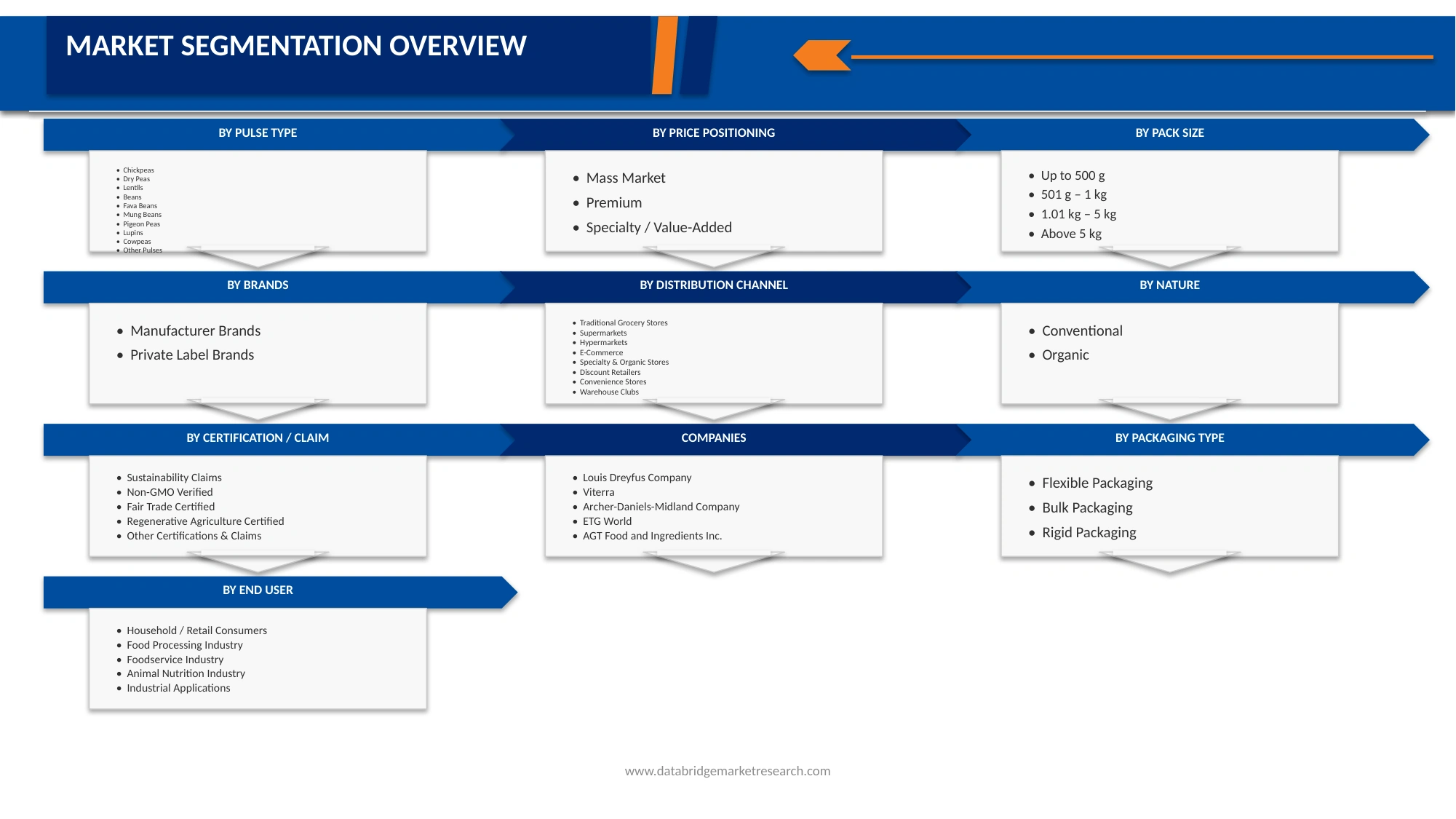

· China · India · Japan · Australia · South Korea · Indonesia · Thailand · Vietnam · Malaysia · Philippines · Rest Of Asia Pacific Western Europe · Germany · U.K. · France · Italy · Spain · Netherlands · Belgium · Switzerland · Austria · Portugal Eastern Europe · Poland · Czech Republic · Romania · Hungary · Slovakia · Bulgaria · Croatia · Serbia · Slovenia Latin America · Brazil · Mexico · Argentina · Chile · Colombia · Peru · Ecuador · Uruguay · Paraguay |

|

Key Market Players |

· AGT FOOD AND INGREDIENTS INC. (Canada) · ARCHER-DANIELS-MIDLAND COMPANY (U.S.) · Arya Pulses Australia (Pty) Ltd (Australia) · Bean Growers Australian LTD (Australia) · Rapunzel Naturkost GmbH (Germany) · Louis Dreyfus Company (Netherlands) · ARMADA GIDA TICARET SANAYI A.Ş. (Türkiye) · BONDUELLE SCA (France) · CAMIL ALIMENTOS S.A. (Brazil) · DURU BULGUR (Türkiye) · Conserve Italia Soc. Coop. Agricola (Italy) · Goya Foods, Inc. (U.S.) · La Costeña (Mexico) · Kicaldo Alimentos (Brazil) · Verde Valle, S.A. de C.V. (Mexico) · Ziegler & Co. GmbH (Germany) · BroadGrain Commodities Inc. (Canada) · Gino Girolomoni Cooperativa Agricola (Italy) · Monte Castello (Brazil) · Olam Agri Holdings Pte Ltd. (Singapore) · ETG WORLD (United Arab Emirates) · NATURAL GIDA A.Ş. (Türkiye) · La Ferme Parthiot (France) · Sandhurst Fine Foods (Australia) · Mckenzie Foods (HSK Ward Group) (Australia) · SABAROT WASSNER S.A.S. (France) · Alnatura (part of Alnatura Produktions- und Handels GmbH) (Germany) · Viterra (Netherlands) · Yayla Agro Gıda (Türkiye) · ESSANTIS (formerly Unigrain) (Australia) |

|

Market Opportunities |

· Upcoming Advancements In Seed Technologies And Modern Agricultural Practices · Government Initiatives Promoting Pulse Cultivation To Enhance Food Security And Sustainable Agriculture |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Custom Pulses Market Trends

Trend: Government Initiatives Promoting Pulse Cultivation To Enhance Food Security And Sustainable Agriculture

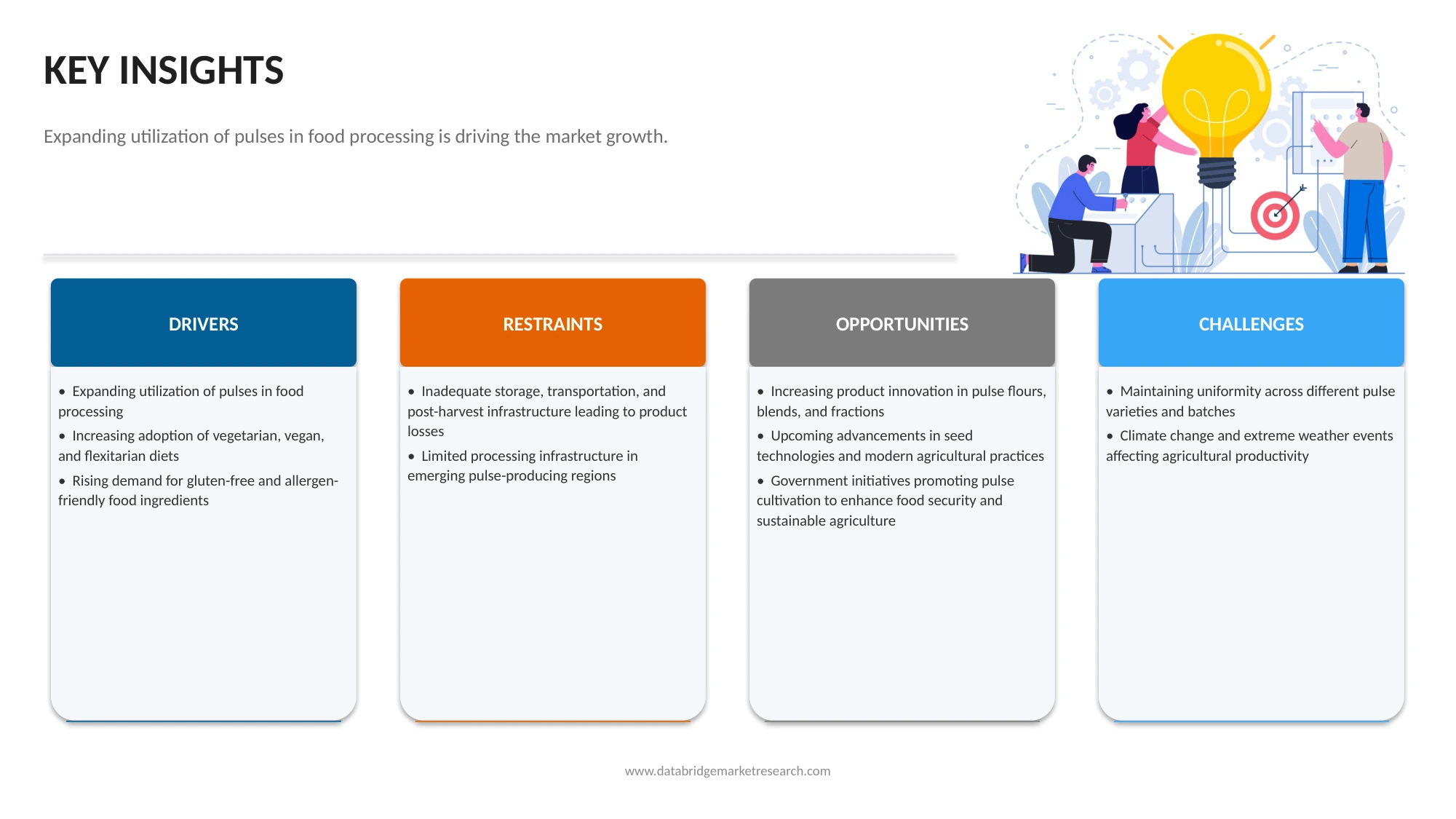

The custom pulses market is gaining a major opportunity from government initiatives that promote pulse cultivation as part of food security, import reduction, farmer income support, and sustainable agriculture goals. Across major pulse-producing and pulse-consuming countries, governments are increasingly treating pulses not only as staple crops but also as strategic commodities that can improve protein availability, strengthen domestic food systems, and reduce dependence on imported protein sources. This is creating favorable conditions for the custom pulses market because policy support at the farm level ultimately expands the raw material base available for value-added pulse processing. Governments are supporting pulse cultivation through seed distribution programs, minimum support and procurement mechanisms, cluster-based pulse missions, crop diversification incentives, expansion of pulse cultivation into rice fallows and other suitable lands, extension support, and investments in processing and storage infrastructure. These initiatives are especially important for chickpeas, lentils, peas, pigeon peas, and black gram, which are widely used in customized pulse flours, protein ingredients, starches, fibers, and blended formulations. In addition, pulses are increasingly being promoted in public policy because they contribute to soil fertility through nitrogen fixation, require relatively lower inputs than many other protein crops, and align with climate-resilient and sustainable farming objectives. As governments intensify their support for pulse production and supply chains, the custom pulses market stands to benefit from a stronger, more reliable, and more scalable raw material pipeline.

For instances,

- In October 2025, India approved the Mission for Aatmanirbharta in Pulses with a financial outlay of Rs 11,440 crore (about USD 1.37 billion) for 2025–26 to 2030–31. The mission targets 35 lakh additional hectares under pulses and aims to raise production to 350 lakh tonnes by 2030–31, directly supporting food security, reducing import dependence, and creating a larger raw-material base for customized pulse products.

- In May 2024, the U.S. House Agriculture Committee’s Farm, Food, and National Security Act of 2024 received support from the USA Dry Pea & Lentil Council because it proposed a meaningful increase in reference prices and Marketing Assistance Loans for dry peas, lentils, and chickpeas. While the release did not publish a dollar figure in the summary, the measure is important because it uses federal support tools to protect growers, improve planting confidence, and strengthen long-term pulse cultivation in the U.S.

- In February 2024, FAO used World Pulses Day 2024 to push governments and food-system stakeholders to integrate pulses more actively into sustainable agriculture and food-security strategies. At the event, FAO emphasized that pulses can improve soil health, reduce hunger and malnutrition, and support climate-resilient farming, while nearly 1,000 participants joined the celebration. Although it is not a subsidy program, it is a policy-support initiative that encourages wider pulse cultivation and adoption across regions.

In conclusion, Government initiatives promoting pulse cultivation are opening a major opportunity for the custom pulses market by strengthening domestic production, supporting farmer participation, and improving the long-term availability of pulses for processing and food use. Through procurement schemes, cultivation missions, policy support, research programs, and sustainability-focused agricultural initiatives, governments are helping expand pulse acreage and reinforce food security goals. As this policy support continues, the custom pulses market is likely to benefit from a stronger supply base, reduced import dependence in key regions, and improved momentum for value-added pulse processing.

Custom Pulses Market Dynamics

Key Market Driver: Expanding Utilization Of Pulses In Food Processing

The custom pulses market is increasingly being driven by the expanding utilization of pulses in food processing, as pulses are moving beyond traditional household consumption and becoming important functional ingredients in a wide range of packaged and value-added foods. Food processors are using chickpeas, lentils, peas, beans, and other pulses in the form of flours, proteins, starches, fibers, grits, and customized blends to improve the nutritional profile, texture, and formulation flexibility of processed foods. In bakery and confectionery, pulse ingredients are being incorporated into gluten-free flour blends, biscuits, cookies, crackers, and protein-enriched baked products. In snacks and savory products, they are used in roasted snacks, chips, extruded products, and pulse-based puffs. Pulses are also increasingly used in plant-based patties, nuggets, meat extenders, ready meals, soup mixes, sauces, breakfast cereals, and nutritional products. Their high protein and fiber content, along with their suitability for clean-label and gluten-free formulations, is encouraging food manufacturers to integrate them into mainstream food processing, thereby supporting the long-term growth of the custom pulses market.

For instances,

- In March 2026, Louis Dreyfus Company started commissioning its pea protein isolate facility in Canada to produce pea protein isolates, fiber, and starch for plant-based foods and nutrition products. This shows how pulses are increasingly being processed into specialized food ingredients rather than sold only in raw form. LDC also reported USD 383 million in group capex commitments in 2025.

- In April 2022, BENEO announced a USD 54 million pulse-processing plant in Germany to produce faba bean protein concentrate, starch-rich flour, and hulls for food applications. The investment highlights how pulses are being increasingly converted into functional ingredients for bakery, plant-based foods, and nutritional products, strengthening the role of custom pulses in food processing.

- In June 2024, Agriculture and Agri-Food Canada reported that in 2023, plant-based protein ingredient demand in Canada reached 18.4 thousand tonnes, with 77.1% used in processed meat and seafood substitutes, 21.3% in baked goods, and 13.8% in snacks. The report also valued retail sales of meat and seafood substitutes at USD 311 million.

In conclusion, the growing use of pulses in food processing is becoming a strong driver for the custom pulses market, as pulses are increasingly being transformed into value-added ingredients such as flours, proteins, starches, fibers, and customized blends for bakery, snacks, plant-based foods, ready meals, and nutrition products. This shift is moving pulses beyond traditional staple consumption and positioning them as functional ingredients in modern food manufacturing. As food processors continue to demand nutritionally rich, versatile, and application-specific pulse ingredients, the role of custom pulses in food processing is expected to strengthen further.

Key Restraint/Challenge: Inadequate Storage, Transportation, And Post-Harvest Infrastructure Leading To Product Losses

The custom pulses market continues to face an important restraint in the form of inadequate storage, transportation, and post-harvest infrastructure, which leads to avoidable quantity and quality losses across the pulse value chain. Pulses may appear less perishable than fruits or vegetables, but they remain highly vulnerable after harvest if drying, cleaning, grading, storage, and transport conditions are not properly managed. High moisture levels, delayed drying, poor warehouse conditions, pest infestation, mold growth, and rough handling during loading, unloading, and transit can all reduce grain quality, lower recovery during milling, and increase product rejection in food processing applications. In many pulse-producing regions, especially in developing markets, farmers and aggregators still rely on traditional storage systems, fragmented transport networks, and limited scientific post-harvest handling, which weakens the consistency of supply for processors and exporters. FAO and CGIAR-linked post-harvest assessments have repeatedly highlighted that cereals and pulses can experience meaningful storage-stage losses, while broader food systems in emerging economies continue to suffer from infrastructure gaps in warehousing, drying, packaging, and logistics. For custom pulse suppliers, this is a major challenge because value-added pulse products depend heavily on consistent raw material quality, stable moisture control, and timely delivery. As a result, weak post-harvest infrastructure continues to raise operational costs, reduce usable output, and constrain the efficient expansion of the custom pulses market.

For instances,

- In July 2025, India’s Ministry of Food Processing Industries said a NABCONS post-harvest loss study found pulse losses of 5.65%–6.74% during the post-harvest chain, with losses linked to weak harvesting, handling, storage, and transportation systems. For the custom pulses market, this matters because poor storage and logistics reduce usable quality and recovery, directly affecting processors that need clean, consistent raw pulses for value-added applications.

- In April 2024, a CGIAR post-harvest management brief highlighted that storage losses in cereals and pulses can reach up to 22% in developing markets where drying, storage, and handling infrastructure remain weak. The report links these losses to inadequate storage structures, moisture control problems, pest infestation, and poor post-harvest practices. This is a major restraint for custom pulses because processors depend on stable quality, moisture levels, and reliable supply.

- In June 2022, the FAO’s Technical Platform on Food Loss and Waste noted that reducing post-harvest losses in grains and pulses remains a priority in sub-Saharan Africa, where infrastructure gaps across storage, handling, and transport continue to weaken food security and marketable supply. For the custom pulses market, this highlights a broader structural problem: even where pulse production exists, inadequate post-harvest systems can limit the availability of quality raw material for processing and export.

In conclusion, Inadequate storage, transportation, and post-harvest infrastructure remains a key restraint for the custom pulses market because it reduces usable output, affects grain quality, and weakens the consistency of raw material supply needed for value-added processing. Losses linked to poor drying, storage, handling, and logistics directly impact the availability of clean, stable, and food-grade pulses for milling, fractionation, and customized ingredient production. Unless post-harvest systems improve across major pulse-producing regions, this structural weakness will continue to raise costs and limit the efficient expansion of the custom pulses market.

Key Market Opportunity: Increasing Product Innovation In Pulse Flours, Blends, And Fractions

The custom pulses market is opening up a strong opportunity through increasing product innovation in pulse flours, blends, and fractions, as food manufacturers look for ingredients that can deliver nutrition, functionality, and cleaner labels in a wide range of applications. Pulses such as chickpeas, lentils, peas, faba beans, and dry beans are no longer being used only in whole or split form; they are increasingly being processed into pulse flours, protein concentrates and isolates, starch fractions, fiber fractions, and customized multi-pulse blends for targeted food formulations. This innovation is widening the use of pulses across gluten-free bakery, snacks, pasta, breakfast cereals, dairy alternatives, meat substitutes, soups, sauces, and sports nutrition products. What makes this a major opportunity for the custom pulses market is that pulse fractions can be designed for specific performance needs such as protein enrichment, texture improvement, emulsification, water binding, thickening, and better nutritional fortification. Public-sector and industry-backed programs are also supporting this shift: USDA-backed projects in North Dakota are funding research on pulse protein fractions and dry bean bakery products, while FAO has highlighted pulse flours, proteins, starch, and fiber as important value-added pathways for the pulse economy. As ingredient innovation advances, custom pulse suppliers have a growing opportunity to move beyond commodity sales and capture higher-value demand through application-specific, premium pulse ingredients for the food industry.

For instances,

- In August 2025, USDA’s Pulse Crop Health Initiative funded multiple projects specifically aimed at improving pulse flours, protein fractions, and ingredient functionality for food use. This included USD 180,461 for improving pulse flour quality, USD 99,856 for studying extraction methods in lentils and dry beans, and USD 93,000 for isolating protein fractions from black beans and lentils. These investments show how public research is actively pushing innovation in pulse flours, fractions, and value-added ingredients.

- In November 2024, research highlighted by the Canadian Light Source showed that pulse flour innovation is moving toward “specific flour for a specific product,” with scientists studying how particle size affects the performance of chickpea, lentil, bean, and pea flours in foods such as brownies, vegan meat, and dressings. This is important for the custom pulses market because it supports more targeted flour design for different food applications rather than one generic pulse flour format.

- In August 2021 (active through December 2024), a USDA-backed Cornell project focused on supercritical fluid extrusion to improve the flavor and functionality of pulse flours and protein concentrates. The project aimed to remove off-flavors and improve ingredient performance, which is a key step for expanding pulse flours and protein fractions into mainstream food products. This reflects how innovation is increasingly focused on making pulse-based ingredients more commercially viable and versatile.

In conclusion, increasing product innovation in pulse flours, blends, and fractions represents a major opportunity for the custom pulses market, as it allows suppliers to move beyond commodity pulses and serve growing demand for specialized, value-added food ingredients. Innovation in protein fractions, starches, fiber fractions, and application-specific pulse blends is expanding the role of pulses across bakery, snacks, meat alternatives, pasta, dairy alternatives, and nutrition products. As research and ingredient development continue to improve functionality, taste, and commercial viability, the custom pulses market is expected to benefit from higher-value product differentiation and broader food industry adoption.

Custom Pulses Market Scope

The custom pulses market is segmented into nine notable segments based on the pulse type, nature, price positioning/claim, pack size, packaging type, brands, end user, distribution channel.

By PulseType

On the basis of pulse type, the market is segmented into chickpeas, dry peas, lentils, beans, fava beans, mung beans, pigeon peas, lupins, cowpeas and other pulses. In 2025, the chickpeas segment is expected to dominate the custom pulses market with a market share of 17.08%, due to its widespread consumer acceptance, high nutritional value, and versatility across multiple culinary applications. Chickpeas are widely used in salads, snacks, spreads such as hummus, bakery products, soups, and plant-based protein formulations, making them a preferred ingredient for both household and industrial use. Their rich protein and fiber content, combined with strong demand for vegetarian and vegan diets, further supports segment dominance across Western Europe.

The chickpeas segment is also expected to experience the fastest growth at a CAGR of 5.05% from 2026 to 2033, driven by rising demand for plant-based protein ingredients and the increasing shift toward sustainable and alternative protein sources. Dry peas are gaining strong traction in the food industry due to their versatility and wide application in pulse flours, protein isolates, snacks, soups, and meat alternative formulations. .

By Nature

On the basis of Nature, the custom pulses market is segmented into conventional and organic. In 2026, the conventional segment is expected to dominate the custom pulses market with a market share of 82.60% due to its widespread cultivation, higher production volumes, established supply chains, and cost-effectiveness compared to organic alternatives. Its extensive use across household consumption, food processing, foodservice, and industrial applications continues to drive strong demand in both developed and emerging markets.

Organic segment is expected to experience the fastest growth at a CAGR of 4.49% from 2026 to 2033. The organic segment is gaining momentum due to increasing consumer preference for chemical-free, non-GMO, and sustainably produced pulses. Rising health awareness, expanding organic retail networks, supportive certification programs, and growing demand for clean-label, plant-based foods are encouraging manufacturers to expand their portfolios of certified organic custom pulse products.

By Price Positioning

On the basis of Price Positioning, the custom pulses market is segmented into Mass Market, Premium, Specialty / Value-Added. In 2026, the Mass Market segment is anticipated to dominate the market with a market share of 64.16%.

The specialty/value-added segment is expected to experience the fastest growth at a CAGR of 4.78% from 2026 to 2033, driven by rising demand for premium, fortified, sprouted, pre-cleaned, and customized pulse products. Consumers increasingly seek convenient, nutritious, and functional foods, while food manufacturers invest in innovative processing, quality enhancement, and differentiated offerings to capture higher-value market opportunities.

By Certification / Claim

On the basis of certification / claim, the custom pulses market is segmented into sustainability claims, non-GMO verified, fair trade certified, regenerative agriculture certified, other certifications & claims. In 2026, the sustainability claims segment is expected to dominate the market with a market share of 39.71% . Demand for sustainability-claimed pulse products is increasing as consumers prioritize environmentally responsible food choices. Manufacturers are adopting sustainable sourcing, lower-carbon production methods, recyclable packaging, and transparent supply chains to strengthen brand trust, comply with evolving regulations, and meet retailer sustainability commitments.

Regenerative agriculture certified segment is expected to experience the fastest growth at a CAGR of 4.75% from 2026 to 2033. The regenerative agriculture certified segment is expanding as food companies focus on improving soil health, biodiversity, and long-term agricultural resilience. Growing consumer awareness of sustainable farming practices, corporate ESG commitments, and retailer demand for traceable agricultural products are driving adoption of regenerative-certified custom pulses.

By Pack Size

On the basis of Pack Size, the custom pulses market is segmented into 1.01 Kg – 5 Kg, 501 G – 1 Kg, Up To 500 G, Above 5 Kg. In 2026, the 1.01 Kg – 5 Kg segment is expected to dominate the market with a market share of 42.94% The 1.01–5 kg pack size is driven by bulk purchasing among families, foodservice operators, and institutional buyers seeking better value and reduced shopping frequency. Larger packs also provide cost savings, ensure product availability, and meet the regular consumption requirements of pulse-based diets.

Up To 500 G segment is expected to experience the fastest growth at a CAGR of 4.61% from 2026 to 2033. The up to 500 g segment is growing due to rising demand from small households, urban consumers, and first-time buyers. Compact packaging offers affordability, convenience, easier storage, reduced food waste, and suitability for premium, specialty, and trial-sized custom pulse products.

By Packaging Type

On the basis of Packaging Type, the custom pulses market is segmented into coated, Flexible Packaging, Bulk Packaging, Rigid Packaging. In 2026, the Flexible Packaging segment is expected to dominate the market with a market share of 57.27% segment is expected to experience the fastest growth at a CAGR of 4.24% from 2026 to 2033. Flexible packaging is widely adopted because it provides lightweight handling, excellent moisture protection, extended shelf life, and lower transportation costs. Its superior printability, resealable options, and reduced material consumption support product freshness while aligning with consumer convenience and sustainability objectives.

By Brands

On the basis of brands, the custom pulses market is segmented into manufacturer brands, private label brands. In 2026, the manufacturer brands segment is expected to dominate the market with a market share of 78.94% Manufacturer brands maintain strong demand through established product quality, consistent supply, trusted certifications, and broad distribution networks. Continuous product innovation, investment in branding, premium positioning, and consumer confidence in recognized food manufacturers contribute significantly to sustained market growth.

Private label brands segment is expected to experience the fastest growth at a CAGR of 4.51% from 2026 to 2033. Private label brands are expanding rapidly as retailers offer competitively priced, quality-assured custom pulse products. Increasing retailer investments, improving product quality, expanding premium private-label ranges, and growing consumer acceptance of store brands continue to strengthen this market segment.

By end user

On the basis of end user, the custom pulses market is segmented into household / retail consumers, food processing industry, foodservice industry, animal nutrition industry, industrial applications. In 2026, the household / retail consumers segment is expected to dominate the market with a market share of 42.74%. Household and retail consumers represent the largest demand base due to increasing health consciousness, higher consumption of plant-based proteins, and regular use of pulses in daily diets. Rising disposable incomes, expanding modern retail, and demand for convenient packaged products further support growth.

Foodservice Industry segment is expected to experience the fastest growth at a CAGR of 4.80% from 2026 to 2033. The foodservice industry is experiencing steady growth as restaurants, hotels, institutional kitchens, and catering services increasingly utilize customized pulse products for diverse menu offerings. Rising demand for nutritious, plant-based meals, bulk purchasing, and standardized ingredient quality continues to drive segment expansion.

Custom Pulses Market Regional Analysis

Asia-Pacific dominated the custom pulses market with the largest revenue share of 56.87% in 2025, The Asia-Pacific custom pulses market is expanding due to rising health consciousness, increasing consumption of plant-based proteins, rapid urbanization, and growing food processing activities. Strong agricultural production, expanding retail networks, demand for premium pulse products, and government support for food security continue to drive regional market growth.

India Custom Pulses Market Insight

India leads the market owing to its position as the world's largest producer and consumer of pulses. Rising demand for customized pulse blends, expanding food processing industries, supportive government initiatives, increasing exports, and growing preference for protein-rich diets are accelerating market expansion across both domestic and international markets.

China Custom Pulses Market Insight

China's custom pulses market is growing steadily due to increasing health awareness, rising demand for functional and plant-based foods, expanding food manufacturing industries, and growing imports of high-quality pulses. Urbanization, higher disposable incomes, and demand for convenient, nutritious food products further support market development.

Australia Custom Pulses Market Insight

Australia's custom pulses market is driven by strong pulse production, export-oriented agriculture, and increasing demand for premium-quality lentils, chickpeas, and beans. Sustainable farming practices, advanced agricultural technologies, growing plant-based food manufacturing, and expanding exports to Asian countries continue to support long-term market growth.

U.K. Custom Pulses Market Insight

U.K. custom pulses market is growing steadily due to rising demand for plant-based proteins and clean-label food products. Increasing vegan and vegetarian populations are driving adoption of customized pulse ingredients in meat alternatives, snacks, soups, and bakery applications. Strong supermarket penetration and rapid expansion of online grocery platforms further enhance product accessibility. Food manufacturers are increasingly focusing on sustainable and allergen-free formulations, supporting innovation in pulse-based products. Additionally, advancements in food processing technologies and growing consumer preference for high-protein, nutritious, and environmentally friendly foods are strengthening overall market growth across retail and foodservice channels.

Italy Custom Pulses Market Insight

Italy custom pulses market is driven by growing adoption of plant-based nutrition within traditional Mediterranean diets. Pulses are widely used in soups, pasta dishes, salads, bakery items, and ready-to-eat meals, supporting consistent domestic demand. Increasing awareness of health benefits such as high protein, fiber content, and digestive wellness is further boosting consumption. The country’s strong food processing sector encourages innovation in pulse-based ingredients and formulations. Additionally, rising demand for clean-label, organic, and natural foods is strengthening market growth across both retail and foodservice channels.

Eastern Europe Custom Pulses Market Insight

Eastern Europe custom pulses market is growing steadily due to increasing demand for protein-rich and plant-based food products, expanding food processing industries, and rising consumer preference for healthy and functional ingredients. Growing investments in food manufacturing, increasing adoption of customized pulse blends by food manufacturers, and expanding regional trade further support market development.

Poland Custom Pulses Market Insight

Poland dominated the Eastern Europe custom pulses market with the largest revenue share of 29.84% in 2025, The custom pulses market is expanding due to the country's strong pulse cultivation, advanced food processing infrastructure, and increasing demand for plant-based protein ingredients. Growing exports of customized pulse products, rising investments in sustainable food manufacturing, and increasing adoption of clean-label and functional food products further support market growth. Strong government support for agriculture and an established supply chain continue to reinforce Poland's leading position.

Romania Custom Pulses Market Insight

Romania custom pulses market is growing steadily due to rising demand for protein-rich, plant-based foods and increasing awareness of healthy dietary habits. Expanding food processing and bakery industries are incorporating customized pulse flours, blends, and protein concentrates into various applications. Strong agricultural output and favorable climatic conditions support domestic pulse production, while improving supply chains enhance availability for manufacturers. Additionally, growing retail modernization and increasing penetration of clean-label and functional food products are supporting market expansion. Government initiatives promoting sustainable farming practices and rural development further contribute to the growth of the custom pulses market in Romania.

Hungary Custom Pulses Market Insight

Hungary custom pulses market is driven by increasing consumer preference for nutritious and plant-based food products, along with rising demand from the food processing sector. The country’s well-developed agricultural base supports steady pulse production, enabling consistent raw material supply for customized applications. Growing use of pulse-based ingredients in bakery, snacks, soups, and meat alternatives is strengthening market demand. Additionally, rising health awareness, expansion of retail channels, and adoption of innovative food formulations are encouraging manufacturers to develop value-added pulse products. Government support for sustainable agriculture and food innovation further enhances market growth prospects.

Latin America Custom Pulses Market Insight

Latin America custom pulses market is growing steadily due to increasing demand for protein-rich and plant-based food products, expanding food processing industries, and rising consumer awareness of healthy dietary choices. Growing cultivation and exports of pulses, increasing adoption of customized pulse blends by food manufacturers, and rising investments in value-added food products continue to support market development.

Brazil Custom Pulses Market Insight

Brazil leads the Latin America custom pulses market owing to its strong agricultural sector and expanding food processing industry. Rising demand for customized pulse ingredients in processed and functional foods, increasing production and exports of pulses, growing consumer preference for nutritious and plant-based diets, and continued investments in food manufacturing are accelerating market expansion.

Custom Pulses Market Share

The custom pulses industry is primarily led by well-established companies, including:

- AGT FOOD AND INGREDIENTS INC. (Canada)

- ARCHER-DANIELS-MIDLAND COMPANY (U.S.)

- Arya Pulses Australia (Pty) Ltd (Australia)

- Bean Growers Australian LTD (Australia)

- Rapunzel Naturkost GmbH (Germany)

- Louis Dreyfus Company (Netherlands)

- ARMADA GIDA TICARET SANAYI A.Ş. (Türkiye)

- BONDUELLE SCA (France)

- CAMIL ALIMENTOS S.A. (Brazil)

- DURU BULGUR (Türkiye)

- Conserve Italia Soc. Coop. Agricola (Italy)

- Goya Foods, Inc. (U.S.)

- La Costeña (Mexico)

- Kicaldo Alimentos (Brazil)

- Verde Valle, S.A. de C.V. (Mexico)

- Ziegler & Co. GmbH (Germany)

- BroadGrain Commodities Inc. (Canada)

- Gino Girolomoni Cooperativa Agricola (Italy)

- Monte Castello (Brazil)

- Olam Agri Holdings Pte Ltd. (Singapore)

- ETG WORLD (United Arab Emirates)

- NATURAL GIDA A.Ş. (Türkiye)

- La Ferme Parthiot (France)

- Sandhurst Fine Foods (Australia)

- Mckenzie Foods (HSK Ward Group) (Australia)

- SABAROT WASSNER S.A.S. (France)

- Alnatura (part of Alnatura Produktions- und Handels GmbH) (Germany)

- Viterra (Netherlands)

- Yayla Agro Gıda (Türkiye)

- ESSANTIS (formerly Unigrain) (Australia)

Latest Developments in Custom Pulses Market

- In August 2024, Louis Dreyfus Company announced the creation of a dedicated Pulses Business Unit to expand its presence in the plant-based protein market. The new business unit will focus on the sourcing, trading, and commercialization of yellow peas, chickpeas, red lentils, faba beans, and pigeon peas across key producing and consuming regions. This initiative strengthens LDC's position in the pulses value chain.

- In August 2025, Bunge and Viterra completed their long-awaited merger, creating a premier agribusiness solutions company focused on food, feed, and fuel. The combination brings together the companies’ complementary grain origination, storage, processing, logistics, and trading networks across major agricultural production and consumption regions, strengthening their ability to serve farmers and customers worldwide. The merger significantly expands the combined company’s footprint, enhances supply chain efficiency, and creates a stronger platform to capture growth opportunities across agricultural commodity and food ingredient markets.

- In May 2026, Archer Daniels Midland (ADM) announced the launch of eight new soy and pea protein ingredients across North America and Europe, including additions to its ProFam and Arcon product lines. The new solutions are designed to support a wide range of applications such as plant-based meat alternatives, dairy alternatives, beverages, bakery products, snacks, and specialized nutrition products. This product expansion strengthens ADM’s plant-based protein portfolio, enhances its ability to meet growing consumer demand for diverse protein sources, and supports long-term growth in the

- In February 2026, ETG unveiled Nusrico as the new identity for its Food and Food Ingredients business, formerly known as Nutrisco. The rebranding reflects the evolution of the business into a diversified platform spanning cocoa, cashew, sesame, rice, edible nuts, and value-added food ingredients, while bringing together ETG’s integrated sourcing, processing, and distribution operations under a unified brand. The rebrand strengthens Nusrico’s market presence, enhances brand recognition across food ingredient value chains, and supports the company’s long-term growth strategy in international agricultural and food markets..

- In April 2026, AGT Food and Ingredients partnered with Sweet Nutrition on a CA$3.9 million innovation project to develop next-generation pulse-based ingredients from peas, lentils, and faba beans. The collaboration focuses on enhancing the functionality of pulse proteins, starches, and fibers for use in cereals, baking mixes, snacks, and other value-added food applications. This initiative strengthens AGT’s pulse ingredient portfolio, expands its capabilities in value-added plant-based ingredients, and supports growth in the rapidly expanding protein and functional foods market.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF GLOBAL CUSTOM PULSES MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATIONS

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 DBMR TRIPOD DATA VALIDATION MODEL

2.5 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.6 DBMR MARKET POSITION GRID

2.7 VENDOR SHARE ANALYSIS

2.8 MULTIVARIATE MODELING

2.9 PRODUCT TIMELINE CURVE

2.1 MARKET END USE INDUSTRY COVERAGE GRID

2.11 SECONDARY SOURCES

2.12 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PORTER’S FIVE FORCES ANALYSIS

4.1.1 INTRODUCTION

4.1.2 INTENSITY OF COMPETITIVE RIVALRY (HIGH)

4.1.3 BARGAINING POWER OF BUYERS (HIGH)

4.1.4 THREAT OF NEW ENTRANTS (MODERATE)

4.1.5 THREAT OF SUBSTITUTE PRODUCTS (MODERATE)

4.1.6 BARGAINING POWER OF SUPPLIERS (MODERATE)

4.1.7 CONCLUSION

4.2 VALUE CHAIN ANALYSIS

4.2.1 RAW MATERIAL CULTIVATION, SOURCING & AGGREGATION (32%–35%)

4.2.2 PRIMARY PROCESSING: CLEANING, GRADING, DEHULLING & MILLING (22%–27%)

4.2.3 CUSTOMIZATION, VALUE-ADDED PROCESSING & FORMULATION (18%–22%)

4.2.4 PACKAGING, DISTRIBUTION & END-USE APPLICATION (20%–25%)

4.2.5 CONCLUSION

4.3 CLIMATE CHANGE AND SUSTAINABILITY SCENARIO

4.3.1 INTRODUCTION

4.3.2 ENVIRONMENTAL CONCERNS

4.3.3 INDUSTRY RESPONSE

4.3.4 GOVERNMENT’S ROLE

4.3.5 ANALYST RECOMMENDATIONS

4.3.6 CONCLUSION

4.4 INDUSTRY ECOSYSTEM ANALYSIS

4.4.1 PROMINENT COMPANIES

4.4.2 SMALL & MEDIUM SIZE COMPANIES

4.4.3 END USERS

4.5 CONSUMER BUYING BEHAVIOUR

4.6 COST ANALYSIS BREAKDOWN

4.6.1 RAW MATERIAL, SEED PROCUREMENT & CULTIVATION COST

4.6.2 CONTRACT FARMING, CROP PROTECTION & HARVESTING COST

4.6.3 PROCESSING, GRADING & QUALITY ASSURANCE COST

4.6.4 PACKAGING, STORAGE & LOGISTICS COST

4.6.5 TECHNOLOGY, SUSTAINABILITY & REGULATORY COMPLIANCE COST

4.6.6 ADMINISTRATIVE OVERHEADS & PROFIT MARGIN

4.7 SUPPLY CHAIN ANALYSIS

4.7.1 INTRODUCTION

4.7.2 RAW MATERIAL SUPPLIERS

4.7.3 PULSE MANUFACTURERS & PROCESSORS

4.7.4 DISTRIBUTORS & LOGISTICS PROVIDERS

4.7.5 BUYERS / END USERS

4.7.6 CONCLUSION

4.8 PROFIT MARGINS SCENARIO

4.8.1 INTRODUCTION

4.8.2 EVOLUTION OF PROFITABILITY ACROSS THE CUSTOM PULSES VALUE CHAIN

4.8.3 PULSE TYPE-WISE PROFITABILITY ANALYSIS

4.8.4 ORGANIC VS CONVENTIONAL PROFIT MARGIN DIFFERENTIAL

4.8.5 ROLE OF PLANT-BASED FOODS IN MARGIN EXPANSION

4.8.6 CONCLUSION

4.9 TECHNOLOGICAL ADVANCEMENTS

4.9.1 AI-DRIVEN SEED SELECTION AND CROP OPTIMIZATION

4.9.2 PRECISION AGRICULTURE AND SMART FARMING TECHNOLOGIES

4.9.3 ADVANCED SORTING AND OPTICAL GRADING SYSTEMS

4.9.4 INNOVATIVE PULSE PROCESSING AND FRACTIONATION TECHNOLOGIES

4.9.5 SUSTAINABLE PACKAGING AND SHELF-LIFE ENHANCEMENT SOLUTIONS

4.9.6 CONCLUSION

4.1 VENDOR SELECTION CRITERIA

4.10.1 PRODUCT QUALITY AND CONSISTENCY

4.10.2 CUSTOMIZATION AND PROCESSING CAPABILITIES

4.10.3 SUPPLY CHAIN RELIABILITY AND SOURCING NETWORK

4.10.4 COST COMPETITIVENESS AND PRICING FLEXIBILITY

4.10.5 FOOD SAFETY, REGULATORY COMPLIANCE, AND SUSTAINABILITY

4.10.6 TECHNICAL SUPPORT AND INNOVATION CAPABILITIES

4.11 RAW MATERIAL COVERAGE

4.11.1 INTRODUCTION

4.11.2 RAW MATERIAL COVERAGE FRAMEWORK FOR CUSTOM PULSES

4.11.3 BEANS

4.11.4 CHICKPEAS

4.11.5 LENTILS

4.11.6 DRY PEAS

4.11.7 PIGEON PEAS

4.11.8 MUNG BEANS

4.11.9 COWPEAS

4.11.10 FAVA BEANS

4.11.11 LUPINS

4.11.12 OTHER PULSES

4.11.13 ORGANIC AND CERTIFIED RAW MATERIALS

4.11.14 CONCLUSION

4.12 BRAND OUTLOOK

4.12.1 INTRODUCTION

4.12.2 BRAND POSITIONING STRATEGIES IN THE GLOBAL CUSTOM PULSES MARKET

4.12.3 QUALITY AS THE FOUNDATION OF BRAND VALUE

4.12.4 SUSTAINABILITY AS A BRAND DIFFERENTIATOR

4.12.5 CUSTOMIZATION AND APPLICATION-SPECIFIC BRANDING

4.12.6 CONVENIENCE-DRIVEN BRAND DEVELOPMENT

4.12.7 BRAND OUTLOOK AND FUTURE COMPETITIVE LANDSCAPE

4.12.8 CONCLUSION

4.13 INNOVATION TRACKER AND STRATEGIC ANALYSIS

4.13.1 INTRODUCTION

4.13.2 MAJOR DEALS AND STRATEGIC ALLIANCES ANALYSIS

4.13.2.1 JOINT VENTURES

4.13.3 MERGERS AND ACQUISITIONS

4.13.4 LICENSING AND PARTNERSHIP

4.13.5 TECHNOLOGY COLLABORATIONS

4.13.6 STRATEGIC DIVESTMENTS

4.13.7 NUMBER OF PRODUCTS IN DEVELOPMENT

4.13.8 STAGE OF DEVELOPMENT

4.13.9 TIMELINES AND MILESTONES

4.13.10 INNOVATION STRATEGIES AND METHODOLOGIES

4.13.11 RISK ASSESSMENT AND MITIGATION

4.13.12 FUTURE OUTLOOK

4.13.13 CONCLUSION

4.14 IMPACT OF WAR ON SUPPLY CHAIN, GEOGRAPHIC FOOTPRINT & STRUCTURAL SHIFTS AND ADAPTIVE STRATEGIES

4.14.1 INTRODUCTION

4.14.2 SUPPLY CHAIN RESILIENCE

4.14.2.1 STRATEGIC DECISIONS

4.14.2.1.1 DIVERSIFICATION OF RAW MATERIAL AND COMPONENT SOURCING ACROSS MULTIPLE GEOGRAPHIC REGIONS

4.14.2.1.2 REDUCTION OF DEPENDENCY ON SINGLE-COUNTRY SUPPLIERS FOR CRITICAL INPUTS AND COMMODITIES

4.14.2.1.3 STRATEGIC PARTNERSHIPS WITH REGIONAL AND GLOBAL SUPPLIERS TO ENSURE STABLE SUPPLY CONTINUITY

4.14.2.1.4 DEVELOPMENT OF ALTERNATIVE LOGISTICS ROUTES AND TRANSPORTATION CORRIDORS TO MITIGATE SHIPPING DISRUPTIONS

4.14.2.1.5 EXPANSION OF REGIONAL MANUFACTURING, PROCESSING, AND STORAGE FACILITIES TO STRENGTHEN SUPPLY SECURITY

4.14.2.1.6 STRENGTHENING SUPPLIER NETWORKS AND INCREASING SAFETY STOCK LEVELS FOR CRITICAL INPUTS

4.14.3 ENERGY & OPERATIONAL COST RISK

4.14.3.1 STRATEGIC DECISIONS

4.14.3.1.1 VOLATILITY IN FUEL, ELECTRICITY, AND NATURAL GAS PRICES IMPACTING PRODUCTION AND PROCESSING COSTS

4.14.3.1.2 INCREASED OPERATIONAL EXPENSES FOR ENERGY-INTENSIVE MANUFACTURING AND INDUSTRIAL OPERATIONS

4.14.3.1.3 LONG-TERM ENERGY PROCUREMENT AGREEMENTS TO STABILIZE PRODUCTION AND OPERATIONAL COSTS

4.14.3.1.4 OPTIMIZATION OF PRODUCTION PROCESSES TO REDUCE ENERGY CONSUMPTION AND IMPROVE EFFICIENCY

4.14.3.1.5 INVESTMENT IN ENERGY-EFFICIENT TECHNOLOGIES, EQUIPMENT, AND PROCESS IMPROVEMENTS

4.14.3.1.6 INTEGRATION OF RENEWABLE AND ALTERNATIVE ENERGY SOURCES INTO INDUSTRIAL OPERATIONS

4.14.4 GEOGRAPHIC FOOTPRINT REASSESSMENT

4.14.4.1 STRATEGIC DECISIONS

4.14.4.1.1 EXPANSION OF PRODUCTION AND MANUFACTURING FACILITIES IN POLITICALLY STABLE REGIONS

4.14.4.1.2 RELOCATION OF MANUFACTURING CLOSER TO RAW MATERIAL SOURCES AND KEY END-USE MARKETS

4.14.4.1.3 DIVERSIFICATION OF GLOBAL PRODUCTION HUBS ACROSS ASIA-PACIFIC, NORTH AMERICA, EUROPE, AND THE MIDDLE EAST

4.14.4.1.4 DEVELOPMENT OF REGIONAL SUPPLY AND DISTRIBUTION HUBS TO REDUCE CROSS-BORDER DEPENDENCY

4.14.4.1.5 ADOPTION OF DECENTRALIZED MANUFACTURING STRATEGIES TO REDUCE GEOPOLITICAL AND TRADE RISKS

4.14.5 SCENARIO PLANNING & RISK MANAGEMENT

4.14.5.1 STRATEGIC DECISIONS

4.14.5.1.1 CREATION OF STRATEGIC RESERVES FOR CRITICAL RAW MATERIALS, COMMODITIES, AND INDUSTRIAL INPUTS

4.14.5.1.2 IMPLEMENTATION OF REAL-TIME SUPPLY CHAIN MONITORING AND RISK ASSESSMENT SYSTEMS

4.14.5.1.3 MULTI-SOURCE PROCUREMENT STRATEGIES FOR KEY PRODUCTION INPUTS AND MATERIALS

4.14.5.1.4 DEVELOPMENT OF CONTINGENCY LOGISTICS PLANS TO ADDRESS TRANSPORTATION AND TRADE DISRUPTIONS

4.14.5.1.5 STRENGTHENING REGULATORY COMPLIANCE, SAFETY PROTOCOLS, AND OPERATIONAL RISK MANAGEMENT FRAMEWORKS

4.14.6 CASH & FINANCIAL PROTECTION

4.14.6.1 STRATEGIC DECISIONS

4.14.6.1.1 HEDGING STRATEGIES TO MITIGATE VOLATILITY IN COMMODITY, RAW MATERIAL, AND ENERGY PRICES

4.14.6.1.2 DIVERSIFICATION OF REVENUE STREAMS ACROSS MULTIPLE MARKETS AND END-USE INDUSTRIES

4.14.6.1.3 COST OPTIMIZATION THROUGH AUTOMATION, OPERATIONAL EFFICIENCY, AND DIGITALIZATION INITIATIVES

4.14.6.1.4 LONG-TERM SUPPLY AGREEMENTS WITH KEY CUSTOMERS AND STRATEGIC PARTNERS

4.14.6.1.5 IMPROVED WORKING CAPITAL MANAGEMENT AND INVENTORY OPTIMIZATION STRATEGIES

4.14.7 TECHNOLOGY ADOPTION & INDUSTRIAL AUTOMATION

4.14.7.1 STRATEGIC DECISIONS

4.14.7.1.1 ADOPTION OF AUTOMATION TECHNOLOGIES TO IMPROVE EFFICIENCY IN MANUFACTURING, PROCESSING, AND PRODUCTION OPERATIONS

4.14.7.1.2 INTEGRATION OF SMART MANUFACTURING SYSTEMS AND INDUSTRIAL IOT (IIOT) FOR REAL-TIME MONITORING AND OPERATIONAL CONTROL

4.14.7.1.3 IMPLEMENTATION OF ADVANCED PROCESS CONTROL SYSTEMS TO ENHANCE PRODUCTIVITY AND REDUCE DOWNTIME

4.14.7.1.4 DEPLOYMENT OF ROBOTICS AND AUTOMATED HANDLING SYSTEMS IN MANUFACTURING PLANTS, WAREHOUSES, AND DISTRIBUTION CENTERS

4.14.7.1.5 INVESTMENT IN PREDICTIVE MAINTENANCE TECHNOLOGIES TO IMPROVE EQUIPMENT RELIABILITY AND REDUCE OPERATIONAL DISRUPTIONS

4.14.7.1.6 DIGITAL INTEGRATION OF SUPPLY CHAIN, PRODUCTION, AND LOGISTICS OPERATIONS THROUGH CENTRALIZED MANAGEMENT PLATFORMS

4.14.7.1.7 IMPLEMENTATION OF DIGITAL TWIN TECHNOLOGIES TO SIMULATE PRODUCTION PROCESSES AND OPTIMIZE OPERATIONAL PERFORMANCE

4.14.7.1.8 ADOPTION OF AI-DRIVEN QUALITY CONTROL AND INSPECTION SYSTEMS TO IMPROVE PRODUCT CONSISTENCY AND REDUCE DEFECTS

4.14.7.1.9 INTEGRATION OF AUTOMATED WAREHOUSE MANAGEMENT AND SMART LOGISTICS SYSTEMS TO ENHANCE DISTRIBUTION EFFICIENCY

4.14.8 NEW BUSINESS & EMERGING REVENUE OPPORTUNITIES & FUTURE OUTLOOK

4.14.8.1 GROWTH IN REGIONAL MANUFACTURING ECOSYSTEMS AND LOCALIZED SUPPLY CHAINS

4.14.8.2 EXPANSION OF SUSTAINABLE AND LOW-CARBON PRODUCTION TECHNOLOGIES

4.14.8.3 RISING DEMAND FOR RESOURCE-EFFICIENT PRODUCTS, MATERIALS, AND INDUSTRIAL SOLUTIONS

4.14.8.4 INCREASED INVESTMENT IN RECYCLING TECHNOLOGIES AND CIRCULAR ECONOMY INITIATIVES

4.14.8.5 DEVELOPMENT OF ALTERNATIVE RAW MATERIALS AND NEXT-GENERATION INDUSTRIAL PRODUCTS

4.14.8.6 GROWING DEMAND DRIVEN BY INFRASTRUCTURE DEVELOPMENT, ENERGY TRANSITION, AND INDUSTRIAL MODERNIZATION

4.14.9 CONCLUSION

5 PRICING ANALYSIS

6 TARIFFS & IMPACT

6.1 INTRODUCTION

6.2 CURRENT TARIFF RATE(S) IN TOP-5 COUNTRY MARKETS

6.3 OUTLOOK: LOCAL PRODUCTION V/S IMPORT RELIANCE

6.4 VENDOR SELECTION CRITERIA DYNAMICS

6.5 IMPACT ON SUPPLY CHAIN

6.5.1 RAW MATERIAL PROCUREMENT

6.5.2 MANUFACTURING AND PRODUCTION

6.5.3 LOGISTICS AND DISTRIBUTION

6.5.4 PRICE PITCHING AND POSITION OF MARKET

6.6 INDUSTRY PARTICIPANTS: PROACTIVE MOVES

6.6.1 SUPPLY CHAIN OPTIMIZATION

6.6.2 JOINT VENTURE ESTABLISHMENTS

6.7 IMPACT ON PRICES

6.8 REGULATORY INCLINATION

6.8.1 GEOPOLITICAL SITUATION

6.8.2 TRADE PARTNERSHIPS BETWEEN THE COUNTRIES

6.8.2.1 FREE TRADE AGREEMENTS

6.8.2.2 ALLIANCE ESTABLISHMENTS

6.8.3 STATUS ACCREDITATION (INCLUDING MFN)

6.8.4 DOMESTIC COURSE OF CORRECTION

6.8.4.1 INCENTIVE SCHEMES TO BOOST PRODUCTION OUTPUTS

6.8.4.2 ESTABLISHMENT OF SPECIAL ECONOMIC ZONES / INDUSTRIAL PARKS

6.9 CONCLUSION

7 REGULATION COVERAGE

7.1 INTRODUCTION

7.2 PRODUCT CODES

7.3 CERTIFIED STANDARDS

7.4 SAFETY STANDARDS

7.4.1 MATERIAL HANDLING & STORAGE

7.4.2 TRANSPORT & PRECAUTIONS

7.4.3 HAZARD IDENTIFICATION

7.5 CONCLUSION

8 MARKET OVERVIEW

8.1 DRIVERS

8.1.1 EXPANDING UTILIZATION OF PULSES IN FOOD PROCESSING

8.1.2 INCREASING ADOPTION OF VEGETARIAN, VEGAN, AND FLEXITARIAN DIETS

8.1.3 RISING DEMAND FOR GLUTEN-FREE AND ALLERGEN-FRIENDLY FOOD INGREDIENTS

8.2 RESTRAINTS

8.2.1 INADEQUATE STORAGE, TRANSPORTATION, AND POST-HARVEST INFRASTRUCTURE LEADING TO PRODUCT LOSSES

8.2.2 LIMITED PROCESSING INFRASTRUCTURE IN EMERGING PULSE-PRODUCING REGIONS

8.3 OPPORTUNITIES

8.3.1 INCREASING PRODUCT INNOVATION IN PULSE FLOURS, BLENDS, AND FRACTIONS

8.3.2 UPCOMING ADVANCEMENTS IN SEED TECHNOLOGIES AND MODERN AGRICULTURAL PRACTICES

8.3.3 GOVERNMENT INITIATIVES PROMOTING PULSE CULTIVATION TO ENHANCE FOOD SECURITY AND SUSTAINABLE AGRICULTURE

8.4 CHALLENGES

8.4.1 MAINTAINING UNIFORMITY ACROSS DIFFERENT PULSE VARIETIES AND BATCHES

8.4.2 CLIMATE CHANGE AND EXTREME WEATHER EVENTS AFFECTING AGRICULTURAL PRODUCTIVITY

9 GLOBAL CUSTOM PULSES MARKET, BY PULSE TYPE

9.1 OVERVIEW

9.2 GLOBAL CUSTOM PULSES MARKET, BY PULSE TYPE, 2018-2033 (USD MILLION)

9.2.1 CHICKPEAS

9.2.2 DRY PEAS

9.2.3 LENTILS

9.2.4 BEANS

9.2.5 FAVA BEANS

9.2.6 MUNG BEANS

9.2.7 PIGEON PEAS

9.2.8 LUPINS

9.2.9 COWPEAS

9.2.10 OTHER PULSES

9.3 GLOBAL CHICKPEAS IN CUSTOM PULSES MARKET, BY TYPE, 2018-2033 (USD MILLION)

9.3.1 KABULI CHICKPEAS

9.3.2 DESI CHICKPEAS

9.4 GLOBAL CHICKPEAS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

9.4.1 ASIA-PACIFIC

9.4.2 WESTERN EUROPE

9.4.3 LATIN AMERICA

9.4.4 EASTERN EUROPE

9.5 GLOBAL DRY PEAS IN CUSTOM PULSES MARKET, BY TYPE, 2018-2033 (USD MILLION)

9.5.1 YELLOW PEAS

9.5.2 GREEN PEAS

9.5.3 OTHER DRY PEAS

9.6 GLOBAL DRY PEAS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

9.6.1 ASIA-PACIFIC

9.6.2 WESTERN EUROPE

9.6.3 LATIN AMERICA

9.6.4 EASTERN EUROPE

9.7 GLOBAL LENTILS IN CUSTOM PULSES MARKET, BY TYPE, 2018-2033 (USD MILLION)

9.7.1 RED LENTILS

9.7.2 GREEN LENTILS

9.7.3 BROWN LENTILS

9.7.4 BLACK LENTILS

9.7.5 YELLOW LENTILS

9.7.6 OTHER LENTILS

9.8 GLOBAL LENTILS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

9.8.1 ASIA-PACIFIC

9.8.2 WESTERN EUROPE

9.8.3 LATIN AMERICA

9.8.4 EASTERN EUROPE

9.9 GLOBAL BEANS IN CUSTOM PULSES MARKET, BY TYPE, 2018-2033 (USD MILLION)

9.9.1 KIDNEY BEANS

9.9.2 BLACK BEANS

9.9.3 PINTO BEANS

9.9.4 NAVY BEANS

9.9.5 GREAT NORTHERN BEANS

9.9.6 OTHER BEANS

9.1 GLOBAL BEANS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

9.10.1 ASIA-PACIFIC

9.10.2 WESTERN EUROPE

9.10.3 LATIN AMERICA

9.10.4 EASTERN EUROPE

9.11 GLOBAL FAVA BEANS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

9.11.1 ASIA-PACIFIC

9.11.2 WESTERN EUROPE

9.11.3 LATIN AMERICA

9.11.4 EASTERN EUROPE

9.12 GLOBAL MUNG BEANS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

9.12.1 ASIA-PACIFIC

9.12.2 WESTERN EUROPE

9.12.3 LATIN AMERICA

9.12.4 EASTERN EUROPE

9.13 GLOBAL PIGEON PEAS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

9.13.1 ASIA-PACIFIC

9.13.2 WESTERN EUROPE

9.13.3 LATIN AMERICA

9.13.4 EASTERN EUROPE

9.14 GLOBAL LUPINS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

9.14.1 ASIA-PACIFIC

9.14.2 WESTERN EUROPE

9.14.3 LATIN AMERICA

9.14.4 EASTERN EUROPE

9.15 GLOBAL COWPEAS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

9.15.1 ASIA-PACIFIC

9.15.2 WESTERN EUROPE

9.15.3 LATIN AMERICA

9.15.4 EASTERN EUROPE

9.16 GLOBAL OTHER PULSES IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

9.16.1 ASIA-PACIFIC

9.16.2 WESTERN EUROPE

9.16.3 LATIN AMERICA

9.16.4 EASTERN EUROPE

10 GLOBAL CUSTOM PULSES MARKET, BY NATURE

10.1 OVERVIEW

10.2 GLOBAL CUSTOM PULSES MARKET, BY NATURE, 2018-2033 (USD MILLION)

10.2.1 CONVENTIONAL

10.2.2 ORGANIC

10.3 GLOBAL CONVENTIONAL IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

10.3.1 ASIA-PACIFIC

10.3.2 WESTERN EUROPE

10.3.3 LATIN AMERICA

10.3.4 EASTERN EUROPE

10.4 GLOBAL ORGANIC IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

10.4.1 ASIA-PACIFIC

10.4.2 WESTERN EUROPE

10.4.3 LATIN AMERICA

10.4.4 EASTERN EUROPE

11 GLOBAL CUSTOM PULSES MARKET, BY PRICE POSITIONING

11.1 OVERVIEW

11.2 GLOBAL CUSTOM PULSES MARKET, BY PRICE POSITIONING, 2018-2033 (USD MILLION)

11.2.1 MASS MARKET

11.2.2 PREMIUM

11.2.3 SPECIALTY / VALUE-ADDED

11.3 GLOBAL MASS MARKET IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

11.3.1 ASIA-PACIFIC

11.3.2 WESTERN EUROPE

11.3.3 LATIN AMERICA

11.3.4 EASTERN EUROPE

11.4 GLOBAL PREMIUM IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

11.4.1 ASIA-PACIFIC

11.4.2 WESTERN EUROPE

11.4.3 LATIN AMERICA

11.4.4 EASTERN EUROPE

11.5 GLOBAL SPECIALTY / VALUE-ADDED IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

11.5.1 ASIA-PACIFIC

11.5.2 WESTERN EUROPE

11.5.3 LATIN AMERICA

11.5.4 EASTERN EUROPE

12 GLOBAL CUSTOM PULSES MARKET, BY CERTIFICATION / CLAIM

12.1 OVERVIEW

12.2 GLOBAL CUSTOM PULSES MARKET, BY CERTIFICATION / CLAIM, 2018-2033 (USD MILLION)

12.2.1 SUSTAINABILITY CLAIMS

12.2.2 NON-GMO VERIFIED

12.2.3 FAIR TRADE CERTIFIED

12.2.4 REGENERATIVE AGRICULTURE CERTIFIED

12.2.5 OTHER CERTIFICATIONS & CLAIMS

12.3 GLOBAL SUSTAINABILITY CLAIMS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

12.3.1 ASIA-PACIFIC

12.3.2 WESTERN EUROPE

12.3.3 LATIN AMERICA

12.3.4 EASTERN EUROPE

12.4 GLOBAL NON-GMO VERIFIED IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

12.4.1 ASIA-PACIFIC

12.4.2 WESTERN EUROPE

12.4.3 LATIN AMERICA

12.4.4 EASTERN EUROPE

12.5 GLOBAL FAIR TRADE CERTIFIED IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

12.5.1 ASIA-PACIFIC

12.5.2 WESTERN EUROPE

12.5.3 LATIN AMERICA

12.5.4 EASTERN EUROPE

12.6 GLOBAL REGENERATIVE AGRICULTURE CERTIFIED IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

12.6.1 ASIA-PACIFIC

12.6.2 WESTERN EUROPE

12.6.3 LATIN AMERICA

12.6.4 EASTERN EUROPE

12.7 GLOBAL OTHER CERTIFICATIONS & CLAIMS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

12.7.1 ASIA-PACIFIC

12.7.2 WESTERN EUROPE

12.7.3 LATIN AMERICA

12.7.4 EASTERN EUROPE

13 GLOBAL CUSTOM PULSES MARKET, BY PACK SIZE

13.1 OVERVIEW

13.2 GLOBAL CUSTOM PULSES MARKET, BY PACK SIZE, 2018-2033 (USD MILLION)

13.2.1 1.01 KG – 5 KG

13.2.2 501 G – 1 KG

13.2.3 UP TO 500 G

13.2.4 ABOVE 5 KG

13.3 GLOBAL 1.01 KG – 5 KG IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

13.3.1 ASIA-PACIFIC

13.3.2 WESTERN EUROPE

13.3.3 LATIN AMERICA

13.3.4 EASTERN EUROPE

13.4 GLOBAL 501 G – 1 KG IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

13.4.1 ASIA-PACIFIC

13.4.2 WESTERN EUROPE

13.4.3 LATIN AMERICA

13.4.4 EASTERN EUROPE

13.5 GLOBAL UP TO 500 G IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

13.5.1 ASIA-PACIFIC

13.5.2 WESTERN EUROPE

13.5.3 LATIN AMERICA

13.5.4 EASTERN EUROPE

13.6 GLOBAL ABOVE 5 KG IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

13.6.1 ASIA-PACIFIC

13.6.2 WESTERN EUROPE

13.6.3 LATIN AMERICA

13.6.4 EASTERN EUROPE

14 GLOBAL CUSTOM PULSES MARKET, BY PACKAGING TYPE

14.1 OVERVIEW

14.2 GLOBAL CUSTOM PULSES MARKET, BY PACKAGING TYPE, 2018-2033 (USD MILLION)

14.2.1 FLEXIBLE PACKAGING

14.2.2 BULK PACKAGING

14.2.3 RIGID PACKAGING

14.3 GLOBAL FLEXIBLE PACKAGING IN CUSTOM PULSES MARKET, BY TYPE, 2018-2033 (USD MILLION)

14.3.1 POUCHES

14.3.2 PLASTIC BAGS

14.3.3 PAPER BAGS

14.4 GLOBAL FLEXIBLE PACKAGING IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

14.4.1 ASIA-PACIFIC

14.4.2 WESTERN EUROPE

14.4.3 LATIN AMERICA

14.4.4 EASTERN EUROPE

14.5 GLOBAL BULK PACKAGING IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

14.5.1 ASIA-PACIFIC

14.5.2 WESTERN EUROPE

14.5.3 LATIN AMERICA

14.5.4 EASTERN EUROPE

14.6 GLOBAL RIGID PACKAGING IN CUSTOM PULSES MARKET, BY TYPE, 2018-2033 (USD MILLION)

14.6.1 CARTONS

14.6.2 JARS

14.6.3 CANS

14.7 GLOBAL RIGID PACKAGING IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

14.7.1 ASIA-PACIFIC

14.7.2 WESTERN EUROPE

14.7.3 LATIN AMERICA

14.7.4 EASTERN EUROPE

15 GLOBAL CUSTOM PULSES MARKET, BY BRANDS

15.1 OVERVIEW

15.2 GLOBAL CUSTOM PULSES MARKET, BY BRANDS, 2018-2033 (USD MILLION)

15.2.1 MANUFACTURER BRANDS

15.2.2 PRIVATE LABEL BRANDS

15.3 GLOBAL MANUFACTURER BRANDS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

15.3.1 ASIA-PACIFIC

15.3.2 WESTERN EUROPE

15.3.3 LATIN AMERICA

15.3.4 EASTERN EUROPE

15.4 GLOBAL PRIVATE LABEL BRANDS IN CUSTOM PULSES MARKET, BY PULSE TYPE, 2018-2033 (USD MILLION)

15.4.1 CHICKPEAS

15.4.2 DRY PEAS

15.4.3 LENTILS

15.4.4 BEANS

15.4.5 FAVA BEANS

15.4.6 MUNG BEANS

15.4.7 PIGEON PEAS

15.4.8 LUPINS

15.4.9 COWPEAS

15.4.10 OTHER PULSES

15.5 GLOBAL CHICKPEAS IN CUSTOM PULSES MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD MILLION)

15.5.1 TRADITIONAL GROCERY STORES

15.5.2 SUPERMARKETS

15.5.3 HYPERMARKETS

15.5.4 E-COMMERCE

15.5.5 SPECIALTY & ORGANIC STORES

15.5.6 DISCOUNT RETAILERS

15.5.7 CONVENIENCE STORES

15.5.8 WAREHOUSE CLUBS

15.6 GLOBAL DRY PEAS IN CUSTOM PULSES MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD MILLION)

15.6.1 TRADITIONAL GROCERY STORES

15.6.2 SUPERMARKETS

15.6.3 HYPERMARKETS

15.6.4 E-COMMERCE

15.6.5 SPECIALTY & ORGANIC STORES

15.6.6 DISCOUNT RETAILERS

15.6.7 CONVENIENCE STORES

15.6.8 WAREHOUSE CLUBS

15.7 GLOBAL LENTILS IN CUSTOM PULSES MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD MILLION)

15.7.1 TRADITIONAL GROCERY STORES

15.7.2 SUPERMARKETS

15.7.3 HYPERMARKETS

15.7.4 E-COMMERCE

15.7.5 SPECIALTY & ORGANIC STORES

15.7.6 DISCOUNT RETAILERS

15.7.7 CONVENIENCE STORES

15.7.8 WAREHOUSE CLUBS

15.8 GLOBAL BEANS IN CUSTOM PULSES MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD MILLION)

15.8.1 TRADITIONAL GROCERY STORES

15.8.2 SUPERMARKETS

15.8.3 HYPERMARKETS

15.8.4 E-COMMERCE

15.8.5 SPECIALTY & ORGANIC STORES

15.8.6 DISCOUNT RETAILERS

15.8.7 CONVENIENCE STORES

15.8.8 WAREHOUSE CLUBS

15.9 GLOBAL FAVA BEANS IN CUSTOM PULSES MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD MILLION)

15.9.1 TRADITIONAL GROCERY STORES

15.9.2 SUPERMARKETS

15.9.3 HYPERMARKETS

15.9.4 E-COMMERCE

15.9.5 SPECIALTY & ORGANIC STORES

15.9.6 DISCOUNT RETAILERS

15.9.7 CONVENIENCE STORES

15.9.8 WAREHOUSE CLUBS

15.1 GLOBAL MUNG BEANS IN CUSTOM PULSES MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD MILLION)

15.10.1 TRADITIONAL GROCERY STORES

15.10.2 SUPERMARKETS

15.10.3 HYPERMARKETS

15.10.4 E-COMMERCE

15.10.5 SPECIALTY & ORGANIC STORES

15.10.6 DISCOUNT RETAILERS

15.10.7 CONVENIENCE STORES

15.10.8 WAREHOUSE CLUBS

15.11 GLOBAL PIGEON PEAS IN CUSTOM PULSES MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD MILLION)

15.11.1 TRADITIONAL GROCERY STORES

15.11.2 SUPERMARKETS

15.11.3 HYPERMARKETS

15.11.4 E-COMMERCE

15.11.5 SPECIALTY & ORGANIC STORES

15.11.6 DISCOUNT RETAILERS

15.11.7 CONVENIENCE STORES

15.11.8 WAREHOUSE CLUBS

15.12 GLOBAL LUPINS IN CUSTOM PULSES MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD MILLION)

15.12.1 TRADITIONAL GROCERY STORES

15.12.2 SUPERMARKETS

15.12.3 HYPERMARKETS

15.12.4 E-COMMERCE

15.12.5 SPECIALTY & ORGANIC STORES

15.12.6 DISCOUNT RETAILERS

15.12.7 CONVENIENCE STORES

15.12.8 WAREHOUSE CLUBS

15.13 GLOBAL COWPEAS IN CUSTOM PULSES MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD MILLION)

15.13.1 TRADITIONAL GROCERY STORES

15.13.2 SUPERMARKETS

15.13.3 HYPERMARKETS

15.13.4 E-COMMERCE

15.13.5 SPECIALTY & ORGANIC STORES

15.13.6 DISCOUNT RETAILERS

15.13.7 CONVENIENCE STORES

15.13.8 WAREHOUSE CLUBS

15.14 GLOBAL OTHER PULSES IN CUSTOM PULSES MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD MILLION)

15.14.1 TRADITIONAL GROCERY STORES

15.14.2 SUPERMARKETS

15.14.3 HYPERMARKETS

15.14.4 E-COMMERCE

15.14.5 SPECIALTY & ORGANIC STORES

15.14.6 DISCOUNT RETAILERS

15.14.7 CONVENIENCE STORES

15.14.8 WAREHOUSE CLUBS

15.15 GLOBAL PRIVATE LABEL BRANDS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

15.15.1 ASIA-PACIFIC

15.15.2 WESTERN EUROPE

15.15.3 LATIN AMERICA

15.15.4 EASTERN EUROPE

16 GLOBAL CUSTOM PULSES MARKET, BY END-USER

16.1 OVERVIEW

16.2 GLOBAL CUSTOM PULSES MARKET, BY END-USER, 2018-2033 (USD MILLION)

16.2.1 HOUSEHOLD / RETAIL CONSUMERS

16.2.2 FOOD PROCESSING INDUSTRY

16.2.3 FOODSERVICE INDUSTRY

16.2.4 ANIMAL NUTRITION INDUSTRY

16.2.5 INDUSTRIAL APPLICATIONS

16.3 GLOBAL HOUSEHOLD / RETAIL CONSUMERS IN CUSTOM PULSES MARKET, BY PULSE TYPE, 2018-2033 (USD MILLION)

16.3.1 CHICKPEAS

16.3.2 LENTILS

16.3.3 BEANS

16.3.4 DRY PEAS

16.3.5 MUNG BEANS

16.3.6 PIGEON PEAS

16.3.7 FAVA BEANS

16.3.8 COWPEAS

16.3.9 LUPINS

16.3.10 OTHER PULSES

16.4 GLOBAL HOUSEHOLD / RETAIL CONSUMERS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

16.4.1 ASIA-PACIFIC

16.4.2 WESTERN EUROPE

16.4.3 LATIN AMERICA

16.4.4 EASTERN EUROPE

16.5 GLOBAL FOOD PROCESSING INDUSTRY IN CUSTOM PULSES MARKET, BY END-USER, 2018-2033 (USD MILLION)

16.5.1 PLANT-BASED FOODS & MEAT ALTERNATIVES

16.5.2 SNACKS & SAVORY PRODUCTS

16.5.3 BAKERY & CONFECTIONERY

16.5.4 READY MEALS & CONVENIENCE FOODS

16.5.5 BREAKFAST CEREALS & NUTRITIONAL PRODUCTS

16.5.6 SOUPS, SAUCES & SEASONINGS

16.5.7 OTHER PROCESSED FOODS

16.6 GLOBAL FOOD PROCESSING INDUSTRY IN CUSTOM PULSES MARKET, BY PULSE TYPE, 2018-2033 (USD MILLION)

16.6.1 DRY PEAS

16.6.2 CHICKPEAS

16.6.3 LENTILS

16.6.4 BEANS

16.6.5 FAVA BEANS

16.6.6 MUNG BEANS

16.6.7 LUPINS

16.6.8 PIGEON PEAS

16.6.9 COWPEAS

16.6.10 OTHER PULSES

16.7 GLOBAL FOOD PROCESSING INDUSTRY IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

16.7.1 ASIA-PACIFIC

16.7.2 WESTERN EUROPE

16.7.3 LATIN AMERICA

16.7.4 EASTERN EUROPE

16.8 GLOBAL FOODSERVICE INDUSTRY IN CUSTOM PULSES MARKET, BY END-USER, 2018-2033 (USD MILLION)

16.8.1 RESTAURANTS

16.8.2 QUICK SERVICE RESTAURANTS (QSRS)

16.8.3 HOTELS & HOSPITALITY

16.8.4 INSTITUTIONAL CATERING

16.9 GLOBAL FOODSERVICE INDUSTRY IN CUSTOM PULSES MARKET, BY PULSE TYPE, 2018-2033 (USD MILLION)

16.9.1 CHICKPEAS

16.9.2 LENTILS

16.9.3 BEANS

16.9.4 DRY PEAS

16.9.5 MUNG BEANS

16.9.6 FAVA BEANS

16.9.7 PIGEON PEAS

16.9.8 COWPEAS

16.9.9 LUPINS

16.9.10 OTHER PULSES

16.1 GLOBAL FOODSERVICE INDUSTRY IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

16.10.1 ASIA-PACIFIC

16.10.2 WESTERN EUROPE

16.10.3 LATIN AMERICA

16.10.4 EASTERN EUROPE

16.11 GLOBAL ANIMAL NUTRITION INDUSTRY IN CUSTOM PULSES MARKET, BY END-USER, 2018-2033 (USD MILLION)

16.11.1 LIVESTOCK FEED

16.11.2 AQUACULTURE FEED

16.11.3 PET FOOD

16.12 GLOBAL ANIMAL NUTRITION INDUSTRY IN CUSTOM PULSES MARKET, BY PULSE TYPE, 2018-2033 (USD MILLION)

16.12.1 DRY PEAS

16.12.2 BEANS

16.12.3 CHICKPEAS

16.12.4 LENTILS

16.12.5 FAVA BEANS

16.12.6 LUPINS

16.12.7 COWPEAS

16.12.8 PIGEON PEAS

16.12.9 MUNG BEANS

16.12.10 OTHER PULSES

16.13 GLOBAL ANIMAL NUTRITION INDUSTRY IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

16.13.1 ASIA-PACIFIC

16.13.2 WESTERN EUROPE

16.13.3 LATIN AMERICA

16.13.4 EASTERN EUROPE

16.14 GLOBAL INDUSTRIAL APPLICATIONS IN CUSTOM PULSES MARKET, BY END-USER, 2018-2033 (USD MILLION)

16.14.1 PULSE PROTEIN INGREDIENTS

16.14.2 FUNCTIONAL FOOD INGREDIENTS

16.14.3 NUTRACEUTICAL INGREDIENTS

16.14.4 OTHER INDUSTRIAL APPLICATIONS

16.15 GLOBAL INDUSTRIAL APPLICATIONS IN CUSTOM PULSES MARKET, BY PULSE TYPE, 2018-2033 (USD MILLION)

16.15.1 DRY PEAS

16.15.2 CHICKPEAS

16.15.3 FAVA BEANS

16.15.4 LENTILS

16.15.5 LUPINS

16.15.6 BEANS

16.15.7 MUNG BEANS

16.15.8 COWPEAS

16.15.9 PIGEON PEAS

16.15.10 OTHER PULSES

16.16 GLOBAL INDUSTRIAL APPLICATIONS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

16.16.1 ASIA-PACIFIC

16.16.2 WESTERN EUROPE

16.16.3 LATIN AMERICA

16.16.4 EASTERN EUROPE

17 GLOBAL CUSTOM PULSES MARKET, BY DISTRIBUTION CHANNEL

17.1 OVERVIEW

17.2 GLOBAL CUSTOM PULSES MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD MILLION)

17.2.1 TRADITIONAL GROCERY STORES

17.2.2 SUPERMARKETS

17.2.3 HYPERMARKETS

17.2.4 E-COMMERCE

17.2.5 SPECIALTY & ORGANIC STORES

17.2.6 DISCOUNT RETAILERS

17.2.7 CONVENIENCE STORES

17.2.8 WAREHOUSE CLUBS

17.3 GLOBAL TRADITIONAL GROCERY STORES IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

17.3.1 ASIA-PACIFIC

17.3.2 WESTERN EUROPE

17.3.3 LATIN AMERICA

17.3.4 EASTERN EUROPE

17.4 GLOBAL SUPERMARKETS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

17.4.1 ASIA-PACIFIC

17.4.2 WESTERN EUROPE

17.4.3 LATIN AMERICA

17.4.4 EASTERN EUROPE

17.5 GLOBAL HYPERMARKETS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

17.5.1 ASIA-PACIFIC

17.5.2 WESTERN EUROPE

17.5.3 LATIN AMERICA

17.5.4 EASTERN EUROPE

17.6 GLOBAL E-COMMERCE IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

17.6.1 ASIA-PACIFIC

17.6.2 WESTERN EUROPE

17.6.3 LATIN AMERICA

17.6.4 EASTERN EUROPE

17.7 GLOBAL SPECIALTY & ORGANIC STORES IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

17.7.1 ASIA-PACIFIC

17.7.2 WESTERN EUROPE

17.7.3 LATIN AMERICA

17.7.4 EASTERN EUROPE

17.8 GLOBAL DISCOUNT RETAILERS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

17.8.1 ASIA-PACIFIC

17.8.2 WESTERN EUROPE

17.8.3 LATIN AMERICA

17.8.4 EASTERN EUROPE

17.9 GLOBAL CONVENIENCE STORES IN CONVENIENCE STORES IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

17.9.1 ASIA-PACIFIC

17.9.2 WESTERN EUROPE

17.9.3 LATIN AMERICA

17.9.4 EASTERN EUROPE

17.1 GLOBAL WAREHOUSE CLUBS IN CUSTOM PULSES MARKET, BY REGION, 2018-2033 (USD MILLION)

17.10.1 ASIA-PACIFIC

17.10.2 WESTERN EUROPE

17.10.3 LATIN AMERICA

17.10.4 EASTERN EUROPE

18 GLOBAL CUSTOM PULSES MARKET, BY REGION

18.1 OVERVIEW

18.2 ASIA-PACIFIC

18.2.1 INDIA

18.2.2 CHINA

18.2.3 AUSTRALIA

18.2.4 INDONESIA

18.2.5 THAILAND

18.2.6 VIETNAM

18.2.7 JAPAN

18.2.8 SOUTH KOREA

18.2.9 MALAYSIA

18.2.10 PHILIPPINES

18.2.11 REST OF ASIA-PACIFIC

18.3 WESTERN EUROPE

18.3.1 GERMANY

18.3.2 UNITED KINGDOM

18.3.3 FRANCE

18.3.4 ITALY

18.3.5 SPAIN

18.3.6 NETHERLAND

18.3.7 BELGIUM

18.3.8 SWITZERLAND

18.3.9 AUSTRIA

18.3.10 PORTUGAL

18.4 LATIN AMERICA

18.4.1 BRAZIL

18.4.2 MEXICO

18.4.3 ARGENTINA

18.4.4 COLOMBIA

18.4.5 PERU

18.4.6 CHILE

18.4.7 ECUADOR

18.4.8 URUGUAY

18.4.9 PARAGUAY

18.5 EASTERN EUROPE

18.5.1 POLAND

18.5.2 ROMANIA

18.5.3 HUNGARY

18.5.4 CZECH REPUBLIC

18.5.5 SERBIA

18.5.6 BULGARIA

18.5.7 SLOVAKIA

18.5.8 CROATIA

18.5.9 SLOVENIA

19 GLOBAL CUSTOM PULSES MARKET: COMPANY LANDSCAPE

19.1 COMPANY SHARE ANALYSIS: GLOBAL

19.2 COMPANY SHARE ANALYSIS: ASIA-PACIFIC

19.3 COMPANY SHARE ANALYSIS: EUROPE

19.4 COMPANY SHARE ANALYSIS: LATIN AMERICA

20 SWOT ANALYSIS

21 COMPANY PROFILE

21.1 LOUIS DREYFUS COMPANY

21.1.1 COMPANY SNAPSHOT

21.1.2 COMPANY SHARE ANALYSIS

21.1.3 PRODUCT PORTFOLIO

21.1.4 RECENT DEVELOPMENT

21.2 VITERRA

21.2.1 COMPANY SNAPSHOT

21.2.2 COMPANY SHARE ANALYSIS

21.2.3 PRODUCT PORTFOLIO

21.2.4 RECENT DEVELOPMENT

21.3 ARCHER-DANIELS-MIDLAND CO

21.3.1 COMPANY SNAPSHOT

21.3.2 REVENUE ANALYSIS

21.3.3 COMPANY SHARE ANALYSIS

21.3.4 PRODUCT PORTFOLIO

21.3.5 RECENT DEVELOPMENT

21.4 ETC GROUP

21.4.1 COMPANY SNAPSHOT

21.4.2 COMPANY SHARE ANALYSIS

21.4.3 PRODUCT PORTFOLIO

21.4.4 RECENT DEVELOPMENT

21.5 AGT FOOD AND INGREDIENTS INC.

21.5.1 COMPANY SNAPSHOT

21.5.2 REVENUE ANALYSIS

21.5.3 COMPANY SHARE ANALYSIS

21.5.4 PRODUCT PORTFOLIO

21.5.5 RECENT DEVELOPMENT

21.6 ALNATURA PRODUKTIONS- UND HANDELS GMBH

21.6.1 COMPANY SNAPSHOT

21.6.2 PRODUCT PORTFOLIO

21.6.3 RECENT DEVELOPMENT

21.7 ARMADA GIDA TICARET SANAYI A.Ş.

21.7.1 COMPANY SNAPSHOT

21.7.2 REVENUE ANALYSIS

21.7.3 PRODUCT PORTFOLIO

21.7.4 RECENT DEVELOPMENT

21.8 ARYA PULSES AUSTRALIA (PTY) LTD

21.8.1 COMPANY SNAPSHOT

21.8.2 PRODUCT PORTFOLIO

21.8.3 RECENT UPDATES

21.9 BEAN GROWERS AUSTRALIAN LTD

21.9.1 COMPANY SNAPSHOT

21.9.2 PRODUCT PORTFOLIO

21.9.3 RECENT UPDATES

21.1 BONDUELLE SCA

21.10.1 COMPANY SNAPSHOT

21.10.2 REVENUE ANALYSIS

21.10.3 PRODUCT PORTFOLIO

21.10.4 RECENT UPDATES

21.11 BOUTIQUE SABAROT

21.11.1 COMPANY SNAPSHOT

21.11.2 PRODUCT PORTFOLIO

21.11.3 RECENT DEVELOPMENT

21.12 BROADGRAIN

21.12.1 COMPANY SNAPSHOT

21.12.2 PRODUCT PORTFOLIO

21.12.3 RECENT UPDATE

21.13 CAMIL ALIMENTOS S.A.

21.13.1 COMPANY SNAPSHOT

21.13.2 PRODUCT PORTFOLIO

21.13.3 RECENT UPDATES

21.14 CONSERVE ITALIA SOC. COOP. AGRICOLA

21.14.1 COMPANY SNAPSHOT

21.14.2 PRODUCT PORTFOLIO

21.14.3 RECENT UPDATES

21.15 DURU BULGUR

21.15.1 COMPANY SNAPSHOT

21.15.2 PRODUCT PORTFOLIO

21.15.3 RECENT DEVELOPMENT

21.16 ESSANTIS

21.16.1 COMPANY SNAPSHOT

21.16.2 PRODUCT PORTFOLIO

21.16.3 RECENT DEVELOPMENT

21.17 GINO GIROLOMONI

21.17.1 COMPANY SNAPSHOT

21.17.2 PRODUCT PORTFOLIO

21.17.3 RECENT UPDATE

21.18 GOYA FOODS INC.

21.18.1 COMPANY SNAPSHOT

21.18.2 PRODUCT PORTFOLIO

21.18.3 RECENT UPDATE

21.19 KICALDO ALIMENTOS

21.19.1 COMPANY SNAPSHOT

21.19.2 PRODUCT PORTFOLIO

21.19.3 RECENT UPDATES

21.2 LA COSTENA

21.20.1 COMPANY SNAPSHOT

21.20.2 PRODUCT PORTFOLIO

21.20.3 RECENT UPDATE

21.21 LA FERME PARTHIOT

21.21.1 COMPANY SNAPSHOT

21.21.2 PRODUCT PORTFOLIO

21.21.3 RECENT DEVELOPMENT

21.22 MCKENZIE FOODS (PART OF HSK WARD GROUP)

21.22.1 COMPANY SNAPSHOT

21.22.2 PRODUCT PORTFOLIO

21.22.3 RECENT DEVELOPMENT

21.23 MONTE CASTELLO

21.23.1 COMPANY SNAPSHOT

21.23.2 PRODUCT PORTFOLIO

21.23.3 RECENT UPDATE

21.24 NATURAL GIDA SANAYI VE TICARET A.Ş.

21.24.1 COMPANY SNAPSHOT

21.24.2 PRODUCT PORTFOLIO

21.24.3 RECENT DEVELOPMENT

21.25 OLAM AGRI HOLDINGS PTE LTD.

21.25.1 COMPANY SNAPSHOT

21.25.2 PRODUCT PORTFOLIO

21.25.3 RECENT DEVELOPMENT

21.26 RAPUNZEL NATURKOST GMBH

21.26.1 COMPANY SNAPSHOT

21.26.2 PRODUCT PORTFOLIO

21.26.3 RECENT UPDATES

21.27 SANDHURST FINE FOODS PTY LTD

21.27.1 COMPANY SNAPSHOT

21.27.2 PRODUCT PORTFOLIO

21.27.3 RECENT DEVELOPMENT

21.28 VERDE VALLE

21.28.1 COMPANY SNAPSHOT

21.28.2 PRODUCT PORTFOLIO

21.28.3 RECENT UPDATE

21.29 YAYLA AGRO FOOD

21.29.1 COMPANY SNAPSHOT

21.29.2 PRODUCT PORTFOLIO

21.29.3 RECENT UPDATE

21.3 ZIEGLER & CO GMBH

21.30.1 COMPANY SNAPSHOT

21.30.2 PRODUCT PORTFOLIO

21.30.3 RECENT UPDATE

22 QUESTIONNAIRE

23 RELATED REPORTS

List of Table

TABLE 1 CLIMATE CHANGE IMPACT AREAS IN THE GLOBAL CUSTOM PULSES MARKET

TABLE 2 CONSUMER BUYING BEHAVIOR