Global Cutaneous Anthrax Treatment Market

Market Size in USD Billion

USD

434.30 Billion

USD

797.92 Billion

2025

2033

USD

434.30 Billion

USD

797.92 Billion

2025

2033

| 2026 - 2033 | |

| USD 434.30 Billion | |

| USD 797.92 Billion | |

| % | |

|

Cutaneous Anthrax Treatment Market Size

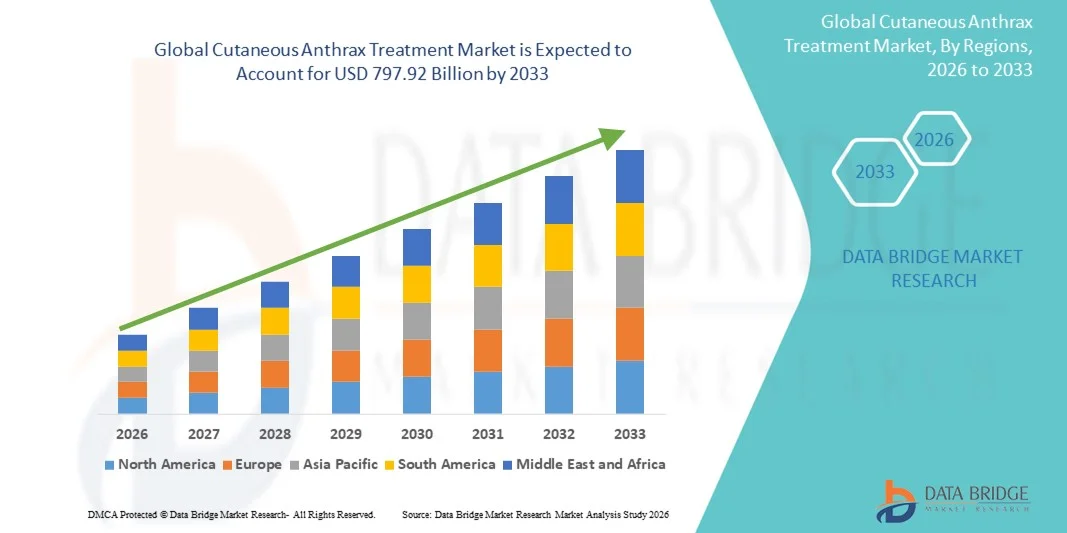

- The global Cutaneous Anthrax Treatment market size was valued at USD 434.3 billion in 2025 and is expected to reach USD 797.92 billion by 2033, at a CAGR of 7.90% during the forecast period

- The market growth is largely fueled by the increasing prevalence of anthrax in livestock and humans, rising awareness of zoonotic diseases, and advancements in pharmaceutical and preventive measures, including antibiotics and vaccines, leading to better disease management across clinical and community settings

- Furthermore, the growing emphasis on early diagnosis, rapid treatment, and standardized therapeutic protocols, alongside government initiatives and WHO recommendations for anthrax control, is significantly driving the adoption of Cutaneous Anthrax Treatment solutions, thereby enhancing overall market expansion

Cutaneous Anthrax Treatment Market Analysis

- Cutaneous Anthrax Treatment, including antibiotics, vaccines, and supportive therapies, is increasingly vital in managing Bacillus anthracis infections due to its severity if untreated and the risk of outbreaks in humans and livestock

- The escalating demand for cutaneous anthrax treatment is primarily fueled by rising awareness of zoonotic infections, government initiatives promoting early detection, growing access to healthcare services, and adoption of standardized treatment protocols across clinical and community healthcare centers

- North America dominated the cutaneous anthrax treatment market with the largest revenue share of 38.9% in 2025, supported by strong diagnostic infrastructure, high awareness of rare infectious diseases, robust healthcare spending, and active research collaborations, with the U.S. leading due to wide access to antibiotics, vaccination programs, and specialized infectious disease centers

- Asia-Pacific is expected to be the fastest-growing region in the cutaneous anthrax treatment market during the forecast period, projected to grow at a CAGR of 8.2% from 2026 to 2033, driven by increasing anthrax incidence, expansion of healthcare access, development of diagnostic and treatment facilities, and government initiatives for early detection and prevention in countries such as China, India, Japan, and South Korea

- The Adult segment dominated the largest market revenue share of 61.4% in 2025, reflecting higher occupational exposure, environmental risk, and overall prevalence

Report Scope and Cutaneous Anthrax Treatment Market Segmentation

|

Attributes |

Cutaneous Anthrax Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Cutaneous Anthrax Treatment Market Trends

Increasing Adoption of Combination Therapies and Optimized Treatment Protocols

- A significant and accelerating trend in the global cutaneous anthrax treatment market is the increasing adoption of combination therapies and optimized treatment protocols to enhance patient outcomes

- For instance, in 2023, several hospitals in the U.S. integrated rapid diagnostic kits with standard antibiotic regimens to reduce treatment initiation time

- Clinicians are focusing on personalized treatment strategies involving antibiotics, topical agents, and supportive care to minimize complications and improve recovery time

- Rising awareness among healthcare providers about early diagnosis and intervention has led to more standardized treatment approaches, ensuring faster response and reduced morbidity

- Research initiatives are increasingly exploring novel therapeutic options, including adjunctive therapies and immunomodulators, to improve treatment effectiveness and reduce hospital stay

- Implementation of new clinical guidelines and treatment frameworks in endemic regions is further standardizing patient care and optimizing clinical outcomes

- The trend towards integrating diagnostic testing with treatment planning allows for quicker identification of high-risk patients and timely administration of targeted therapies

- Enhanced supply chain management and availability of treatment kits in rural areas are contributing to wider accessibility and prompt disease management

Cutaneous Anthrax Treatment Market Dynamics

Driver

Increasing Prevalence and Awareness About Cutaneous Anthrax

- The rising incidence of cutaneous anthrax infections in agricultural, veterinary, and laboratory-exposed populations is a major driver for market growth

- For instance, in 2022, outbreaks in livestock-handling regions of India prompted immediate deployment of cutaneous anthrax treatment kits in local clinics

- Growing awareness among healthcare professionals and public health authorities about rapid treatment protocols is encouraging adoption of standardized therapeutic regimens

- Government initiatives and vaccination campaigns in high-risk areas are creating supportive conditions for timely treatment and reduced disease severity

- Expansion of healthcare infrastructure in rural and semi-urban regions has improved accessibility to antibiotics and adjunctive therapies for affected patients

- Increased investments in research and development for safer and more effective topical and systemic therapies are driving market growth

- Awareness programs and training for early identification of cutaneous anthrax cases among veterinarians and farmers are facilitating prompt treatment initiation

Restraint/Challenge

Concerns Regarding Treatment Costs and Limited Awareness in Remote Areas

- High costs associated with combination therapies and hospital-based treatment protocols can limit adoption, particularly in developing countries or rural regions

- For instance, in some African and Asian regions, limited access to advanced treatment kits has resulted in delayed therapy and higher complication rates\

- Lack of awareness among at-risk populations about early symptoms and treatment requirements poses a challenge to market growth

- Ensuring the availability of essential antibiotics and therapeutic agents in remote and low-resource areas remains a critical barrier

- Regulatory challenges and the need for compliance with local guidelines can delay the introduction of new treatment formulations

- Overcoming these challenges through government support, patient education, and distribution of affordable treatment kits is crucial for sustained market growth

- Efforts to improve supply chain efficiency, community outreach, and healthcare worker training will further mitigate these restraints

Cutaneous Anthrax Treatment Market Scope

The market is segmented on the basis of drug type, treatment type, diagnosis, demographic, route of administration, end‑users, and distribution channel.

- By Drug Type

On the basis of drug type, the Cutaneous Anthrax Treatment market is segmented into Penicillin, Tetracycline, Ciprofloxacin, Clindamycin, and Amoxicillin. The Penicillin segment dominated the largest market revenue share of 44.5% in 2025, owing to its proven efficacy, affordability, and long-established use as the first-line therapy in anthrax management. Penicillin is widely prescribed due to its high effectiveness in eradicating Bacillus anthracis infections and its compatibility with both inpatient and outpatient treatment protocols. Hospitals and clinics prefer Penicillin for severe and uncomplicated cases alike because of its predictable pharmacokinetics and well-understood side-effect profile. Additionally, Penicillin’s broad availability in generic forms ensures cost-effectiveness and accessibility for low-resource settings. The established clinical guidelines support Penicillin as a standard treatment, contributing to its dominant adoption. High patient compliance, minimal drug interactions, and rapid bacterial clearance reinforce its preference among clinicians. It is commonly used across adult and pediatric populations, ensuring extensive market penetration. Integration of Penicillin in combination therapies with supportive care further strengthens its position. The segment also benefits from strong insurance coverage in most regions, enhancing affordability. Overall, Penicillin remains the cornerstone of Cutaneous Anthrax management, maintaining clinical trust and widespread usage.

The Ciprofloxacin segment is expected to witness the fastest CAGR of 18.2% from 2026 to 2033, driven by its broad-spectrum activity and increasing role in both prophylactic and therapeutic settings. Ciprofloxacin’s flexibility in oral and intravenous forms enables its use in diverse clinical scenarios, including severe systemic infections. It is increasingly employed in bioterrorism preparedness and emergency protocols due to rapid action against resistant Bacillus anthracis strains. The growing prevalence of antibiotic-resistant anthrax cases necessitates more widespread use of Ciprofloxacin. Its inclusion in national and international anthrax treatment guidelines is enhancing adoption across hospitals and clinics. Public health initiatives promoting awareness of effective antibiotics for high-risk populations contribute to growth. Improved formulations, including extended-release and pediatric-friendly versions, support market expansion. Ciprofloxacin’s strong pharmacological profile, including high bioavailability and favorable safety, encourages clinician preference. Expanded access through hospital and retail pharmacies further accelerates uptake. The segment also benefits from rising government stockpiling for epidemic preparedness. Integration into combination therapy regimens improves therapeutic outcomes, solidifying its role as an emerging market driver.

- By Treatment Type

On the basis of treatment type, the market is segmented into Antibiotics, Antitoxins, and Vaccine. The Antibiotics segment held the largest market revenue share of 52.1% in 2025, as antibiotics remain essential for eliminating Bacillus anthracis and preventing systemic complications. Standard regimens including Penicillin and Ciprofloxacin are widely adopted, providing predictable outcomes and high patient adherence. Hospitals and clinics rely on antibiotics as the primary intervention for both confirmed and suspected anthrax cases. Strong clinical validation, cost-effectiveness, and widespread availability ensure its dominance. Inclusion in international treatment guidelines reinforces consistent usage patterns. The segment supports treatment across both adults and pediatric populations, facilitating broad market coverage. Antibiotics are employed for prophylactic purposes in high-risk occupational groups, further increasing demand. Their administration via oral or IV routes provides flexibility for inpatient and outpatient care. Extensive physician training and long-term clinical experience contribute to sustained confidence in outcomes. Integration of antibiotics with supportive care, such as hydration and topical therapies, enhances treatment efficacy. Market adoption is further supported by government and NGO programs supplying essential antibiotics in endemic areas. Overall, antibiotics maintain a central role in standard anthrax management.

The Vaccine segment is expected to witness the fastest CAGR of 19.5% from 2026 to 2033, supported by preventive immunization initiatives in endemic and high-risk regions. Improved vaccine formulations, including single-dose and adjuvant-enhanced types, increase efficacy and patient compliance. National public health programs promoting anthrax vaccination for military, agricultural, and laboratory personnel drive adoption. Ongoing research into combination vaccines and novel delivery systems enhances market attractiveness. Government and NGO-backed vaccination drives, particularly in developing countries, support rapid expansion. Rising awareness about preventive strategies among healthcare providers and the public fosters growth. Vaccines are increasingly integrated into occupational safety protocols and outbreak preparedness plans. Enhanced cold-chain logistics and distribution systems improve accessibility in rural and remote areas. Vaccine education campaigns contribute to broader acceptance, especially among at-risk populations. Collaboration between pharmaceutical companies and health authorities accelerates development and deployment. Pediatric and adult formulations address diverse demographic needs, ensuring widespread coverage. Overall, vaccines are emerging as a rapidly growing segment due to preventive healthcare focus.

- By Diagnosis

On the basis of diagnosis, the market is segmented into Skin testing, Blood tests, CT scan, X-ray, Lumbar puncture, and Others. Blood tests dominated the largest market revenue share of 45.3% in 2025, due to their accuracy, rapid results, and ability to detect bacteremia effectively. Blood tests are widely preferred in hospitals and clinics for early confirmation of infection, enabling prompt treatment initiation. The technique supports both routine and emergency scenarios, making it a standard diagnostic tool. High reliability, minimal invasiveness, and established clinical protocols drive preference among healthcare providers. Blood tests allow monitoring of therapy effectiveness and adjustment of antibiotic regimens. Standardization across laboratory networks ensures consistent quality and results interpretation. Blood tests are compatible with both adult and pediatric populations. Integration with electronic health records improves patient management and follow-up care. Availability in both public and private healthcare settings ensures accessibility. Cost-effectiveness and quick turnaround time contribute to dominance. The segment benefits from regular training programs and awareness campaigns for clinicians. Strong adoption in outbreak surveillance and epidemiological monitoring further reinforces market leadership.

The CT scan segment is expected to witness the fastest CAGR of 17.8% from 2026 to 2033, driven by increasing use in identifying systemic involvement and complications in severe anthrax infections. Advanced imaging capabilities provide detailed visualization of tissue damage, aiding in treatment planning. Rising availability of CT facilities in hospitals and diagnostic centers supports uptake. CT scans complement laboratory tests and allow early intervention in high-risk patients. Growing recognition of their value in monitoring anthrax-related complications drives adoption. Enhanced imaging resolution improves diagnostic confidence. Integration with hospital information systems ensures efficient workflow. Physicians are increasingly trained in CT-based diagnosis of rare infections. Improved insurance coverage and affordability contribute to market expansion. Rising investments in healthcare infrastructure in developing regions support growth. Overall, CT scans are becoming a key diagnostic tool in complex anthrax management.

- By Demographic

On the basis of demographic, the market is segmented into Children and Adults. The Adult segment dominated the largest market revenue share of 61.4% in 2025, reflecting higher occupational exposure, environmental risk, and overall prevalence. Adults require targeted antibiotic regimens, often with combination therapy, ensuring consistent demand across hospitals and clinics. Structured treatment guidelines and strong clinician awareness support market leadership. Adults represent a majority of hospital admissions for severe cases. Wide geographic coverage, from urban to rural areas, ensures extensive adoption. High adherence to standardized treatment protocols maintains therapeutic effectiveness. Adults frequently receive both prophylactic and therapeutic interventions. Insurance coverage supports sustained usage. Integration of diagnostics and treatment in adults is more streamlined. Public health campaigns target adult populations in endemic regions, reinforcing market share. The segment benefits from comprehensive monitoring and follow-up care.

The Children segment is expected to witness the fastest CAGR of 15.6% from 2026 to 2033, driven by increasing pediatric-focused programs, vaccination campaigns, and early intervention initiatives. Pediatric formulations of antibiotics and vaccines improve compliance and treatment outcomes. Outpatient management and school-based preventive measures expand adoption. Growing awareness among parents and caregivers fosters early diagnosis and therapy. Development of child-friendly dosing regimens supports safer administration. Government-backed pediatric health programs accelerate market penetration. Clinics and community healthcare centers contribute to accessible care. Improved supply chains for pediatric medications enhance reach. Training programs for pediatric healthcare providers further drive growth. The segment benefits from increased focus on preventive care. Overall, children represent a rapidly expanding demographic in anthrax management.

- By Route of Administration

On the basis of route of administration, the market is segmented into Intramuscular, Intravenous, and Oral. Oral administration dominated the largest market revenue share of 48.2% in 2025, due to convenience, high patient compliance, and suitability for outpatient therapy. Oral antibiotics and supportive drugs enable self-administration, reducing hospital stays and improving adherence. This route is widely preferred in endemic areas for both adults and children. Oral therapies integrate easily with combination regimens, providing effective treatment outcomes. Healthcare providers favor oral administration for its cost-effectiveness and minimal resource requirements. The availability of multiple oral formulations enhances flexibility. Patient preference strongly supports dominance. Established clinical protocols reinforce consistent usage. Distribution through retail and hospital pharmacies ensures accessibility. Patient education programs encourage adherence. Oral administration remains central in standard anthrax care.

The Intravenous segment is expected to witness the fastest CAGR of 18.9% from 2026 to 2033, driven by its critical role in severe systemic infections requiring rapid drug delivery. IV administration allows precise dosing and faster therapeutic action. Hospitals and specialized clinics increasingly adopt IV therapy for acute cases. Infrastructure improvements, including infusion equipment and trained personnel, support segment growth. IV protocols are standardized in emergency anthrax care guidelines. Rising incidence of severe infections necessitates IV usage. Combination therapy often requires IV antibiotics alongside supportive care. Insurance coverage supports broader adoption. Enhanced clinical awareness improves timely intervention. Continuous monitoring during IV administration ensures safety and efficacy. IV administration is projected to gain traction in tertiary care centers. Overall, IV therapy represents a rapidly expanding route for severe disease management.

- By End-Users

On the basis of end-users, the market is segmented into Clinic, Hospital, and Others. Hospitals dominated the largest market revenue share of 55.6% in 2025, due to their capacity to provide comprehensive care including IV therapy, diagnostics, and emergency management. Hospitals handle severe cases, systemic infections, and high-risk patients, making them central to anthrax management. Availability of multidisciplinary teams, imaging, and laboratory services supports treatment effectiveness. Hospitals are equipped to administer both standard and combination therapies. Geographic coverage from urban to semi-urban areas ensures accessibility. Hospitals follow structured treatment protocols enhancing consistency. High patient throughput contributes to revenue dominance. Training programs for healthcare professionals reinforce adherence to guidelines. Insurance support facilitates affordability. Hospitals also serve as hubs for research and surveillance. Overall, hospitals remain the primary treatment centers in the market.

The Clinic segment is expected to witness the fastest CAGR of 16.7% from 2026 to 2033, driven by the increasing role of outpatient services, follow-up care, and community-based management for mild or moderate cases. Clinics offer convenience, shorter wait times, and easier access for preventive and maintenance therapy. Expansion of clinic networks in endemic and peri-urban regions supports growth. Outpatient antibiotic administration and vaccine delivery are increasingly conducted at clinics. Telemedicine and remote consultation integration enhance clinic adoption. Patient education initiatives improve adherence in community settings. Government and NGO-supported programs often use clinics as distribution points. Clinics provide targeted pediatric care, increasing relevance. Cost-effectiveness and lower operational complexity favor adoption. Clinics are emerging as rapidly growing end-users for anthrax treatment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. Retail pharmacies dominated the largest market revenue share of 46.8% in 2025, due to accessibility, familiarity, and efficient dispensing of antibiotics and supportive medications. Retail pharmacies enable repeat prescriptions, high patient engagement, and broad coverage across urban and semi-urban regions. Their wide network ensures timely access to essential drugs. Retail channels facilitate adherence programs and counseling. Pharmacies support both adult and pediatric populations. Established inventory management ensures uninterrupted supply. Insurance partnerships enhance affordability. Community trust and brand recognition reinforce dominance. Retail pharmacies are central to outpatient treatment models. Integration with local healthcare providers strengthens adoption. Overall, retail pharmacies maintain market leadership due to accessibility and reliability.

The Online Pharmacy segment is expected to witness the fastest CAGR of 21.5% from 2026 to 2033, driven by growing digital health adoption, e-commerce penetration, and home delivery of prescription medications. Online channels allow patients in remote or underserved areas to access essential antibiotics and vaccines conveniently. Telemedicine integration and digital prescription validation streamline the process. Home delivery ensures adherence for chronic or preventive therapy. Rising smartphone and internet penetration facilitate platform adoption. COVID-19 and other public health initiatives have increased online pharmacy usage. Partnerships with hospitals and clinics expand reach. Subscription and refill models encourage repeat usage. Cost-competitiveness and promotional strategies attract new users. Online pharmacies also support secure patient data management. Overall, online distribution is the fastest-growing segment in the market.

Cutaneous Anthrax Treatment Market Regional Analysis

- North America dominated the cutaneous anthrax treatment market with the largest revenue share of 38.9% in 2025, supported by strong diagnostic infrastructure, high awareness of rare infectious diseases, robust healthcare spending, and active research collaborations

- Consumers in the region highly value access to antibiotics, vaccination programs, and specialized infectious disease centers for timely treatment and prevention

- This widespread adoption is further supported by increasing government initiatives, availability of antitoxins, and the growing focus on early detection and prophylactic care, establishing advanced treatment solutions as a preferred choice for both clinical and hospital settings

U.S. Cutaneous Anthrax Treatment Market Insight

The U.S. cutaneous anthrax treatment market captured the largest revenue share in 2025 within North America. The market growth is fueled by wide access to antibiotics, vaccination programs, and specialized infectious disease centers. Robust healthcare infrastructure and strong public health initiatives enhance early detection and effective management of anthrax cases. High awareness among healthcare professionals and the general population supports timely diagnosis and administration of Penicillin, Ciprofloxacin, Tetracycline, Clindamycin, and Amoxicillin. Hospitals and clinics provide specialized treatment pathways for severe and high-risk cases, while active participation in research programs and clinical trials drives adoption of new antitoxins and vaccine therapies. Hospital, retail, and online pharmacies ensure widespread availability of therapeutic options, and government-led vaccination programs further strengthen market growth. Increasing funding and insurance coverage improve access to treatment for at-risk populations, while public awareness campaigns promote early treatment adherence, reducing anthrax-related morbidity and mortality.

Europe Cutaneous Anthrax Treatment Market Insight

The Europe cutaneous anthrax treatment market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing awareness of infectious diseases and robust healthcare systems. Improved access to diagnostic tools, including skin testing, blood tests, CT scans, and X-rays, supports early detection and effective treatment. Government initiatives and public health programs encourage widespread vaccination and antibiotic administration, while hospitals, clinics, and specialty care centers experience significant growth. Collaboration between research institutions and healthcare providers fosters innovative treatment adoption across the region.

U.K. Cutaneous Anthrax Treatment Market Insight

The U.K. cutaneous anthrax treatment market is anticipated to grow at a noteworthy CAGR during the forecast period due to increasing healthcare access and heightened awareness of anthrax prevention. Government-led vaccination campaigns and public health initiatives strengthen disease control. The availability of multiple antibiotic options ensures effective case management across clinics and hospitals, and the country’s robust healthcare and pharmacy infrastructure facilitates access to treatments through hospital, retail, and online channels.

Germany Cutaneous Anthrax Treatment Market Insight

The Germany cutaneous anthrax treatment market is expected to expand at a considerable CAGR, fueled by advanced diagnostic facilities and strong healthcare spending. Patients have access to specialized infectious disease centers and trained healthcare professionals, while public and private healthcare programs encourage early treatment with antibiotics and antitoxins. Germany’s focus on innovation and research promotes the introduction of vaccines and novel therapeutics, supporting overall market growth.

Asia-Pacific Cutaneous Anthrax Treatment Market Insight

The Asia-Pacific cutaneous anthrax treatment market is poised to grow at the fastest CAGR of 8.2% during 2026–2033, driven by increasing anthrax incidence, expansion of healthcare access, and government initiatives for early detection and prevention. Rising availability of diagnostic and treatment facilities improves case management in countries such as China, India, Japan, and South Korea. Growing healthcare infrastructure, increasing geriatric and at-risk populations, and vaccination programs contribute to higher treatment adoption. Hospital, clinic, and pharmacy networks are expanding to meet rising demand for antibiotics and antitoxins.

Japan Cutaneous Anthrax Treatment Market Insight

The Japan cutaneous anthrax treatment market is gaining momentum due to high healthcare access and a strong focus on infectious disease prevention. Government programs for vaccination and early diagnosis are driving treatment adoption, while hospitals and clinics provide specialized care for anthrax cases, including antibiotics and antitoxin therapies.

China Cutaneous Anthrax Treatment Market Insight

The China cutaneous anthrax treatment market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to increasing anthrax incidence, expanding healthcare access, and government-led vaccination initiatives. Advanced diagnostics, wide availability of antibiotics and antitoxins, and strong domestic pharmaceutical manufacturing ensure effective early treatment and growing market demand.

Cutaneous Anthrax Treatment Market Share

The Cutaneous Anthrax Treatment industry is primarily led by well-established companies, including:

• Pfizer (U.S.)

• GlaxoSmithKline (U.K.)

• Novartis (Switzerland)

• Merck & Co. (U.S.)

• Cipla (India)

• Sanofi (France)

• Bayer (Germany)

• Astellas Pharma (Japan)

• Fort Dodge Animal Health (U.S.)

• Sigma-Aldrich (U.S.)

• Teva Pharmaceuticals (Israel)

• Dr. Reddy’s Laboratories (India)

• BioThrax (Emergent BioSolutions) (U.S.)

• Abbott Laboratories (U.S.)

• Celgene (U.S.)

• Janssen Pharmaceuticals (Belgium)

• Amgen (U.S.)

• Hikma Pharmaceuticals (Jordan)

• Sinovac Biotech (China)

• Mitsubishi Tanabe Pharma (Japan)

Latest Developments in Global Cutaneous Anthrax Treatment Market

- In November 2023, GC Biopharma submitted a marketing application to South Korea’s regulatory body for GC1109 — a recombinant anthrax vaccine based on protective antigen proteins — which, if approved, would become the world’s first genetically engineered anthrax vaccine

- In April 2025, South Korea’s Ministry of Food and Drug Safety approved BARYTHRAX, a recombinant protein–based anthrax vaccine developed by GC Biopharma and the Korea Disease Control and Prevention Agency; this innovation uses only the protective antigen of B. anthracis, reducing toxin-related risks compared to older vaccines

- In March 2025, researchers from Northeastern University and NovoBiotic demonstrated that the antibiotic teixobactin is highly effective against Bacillus anthracis in vitro, with no detectable resistance, offering promising potential for a novel, more resilient therapeutic option

- In November 2025, GC Biopharma announced Phase 2 clinical trial data for BARYTHRAX showing strong immunogenicity — the vaccine induced toxin-neutralizing antibodies above protective thresholds in 240 healthy adults, with only mild and transient side-effects, confirming a favorable safety profile

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.