Global Cybersecurity Mesh Market

Market Size in USD Billion

USD

2.15 Billion

USD

6.66 Billion

2025

2033

USD

2.15 Billion

USD

6.66 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.15 Billion | |

| USD 6.66 Billion | |

| % | |

|

Cybersecurity Mesh Market Overview

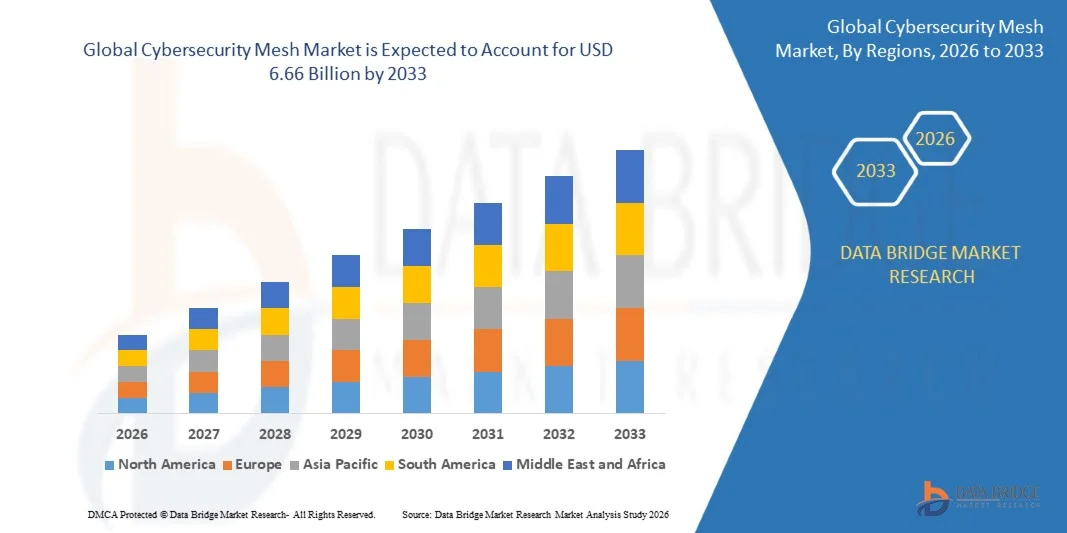

As per Data Bridge Market Research analysis The cybersecurity mesh market was valued at USD 2.15 billion in 2025 and is projected to reach USD 6.66 billion by 2033, growing at a CAGR of 15.20% from 2026 to 2033. The market is experiencing strong growth driven by the increasing complexity of distributed IT environments, rising frequency of cyberattacks, and growing adoption of cloud-based and hybrid work infrastructures.

The rapid expansion of digital transformation initiatives, combined with the widespread use of multi-cloud platforms, remote access systems, and connected devices, is compelling organizations to adopt decentralized and identity-centric security frameworks. Cybersecurity mesh architectures are increasingly replacing traditional perimeter-based security models, enabling unified security management, enhanced threat detection, and consistent policy enforcement across users, devices, applications, and networks in highly distributed enterprise environments.

Market Size & Forecast

- Global Market Value (2025): USD 2.15 Billion

- Expected Market Value (2033): USD 6.66 Billion

- Forecast CAGR (2026–2033): 15.20%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Key Market Trends & Insights

- North America dominated the cybersecurity mesh market with the largest revenue share of 37.92% in 2025, supported by high cybersecurity spending, early adoption of zero-trust frameworks, and the presence of major security technology providers.

- The identity & access management segment led the market with a 39.84% share in 2025, driven by the growing need for identity-centric security frameworks across distributed enterprise environments

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 14.1% from 2026 to 2033, fueled by accelerating digital transformation, expanding cloud adoption, and increasing cybersecurity investments across China, India, Japan, and Southeast Asia.

- Cloud security are the fastest-growing security type, projected to register a CAGR of 14.5%, reflecting the surge in rapid expansion of cloud-native applications and multi-cloud infrastructures.

- The large enterprises segment dominated the enterprise size category with a 64.28% revenue share in 2025, led by complex IT infrastructures, extensive digital assets, and higher cybersecurity spending capabilities.

- Cloud accounted for 61.37% of the market, preferred by its scalability, flexibility, and ability to secure distributed environments efficiently.

- The hybrid segment is the fastest-growing deployment mode category, with a CAGR of 14.2%, driven by the increasing need to secure both on-premises and cloud-based resources simultaneously.

Report Scope and Cybersecurity Mesh Market Segmentation

|

Attributes |

Cybersecurity Mesh Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Palo Alto Networks, Inc. (U.S.) · Cisco Systems, Inc. (U.S.) · Fortinet, Inc. (U.S.) · CrowdStrike, Inc. (U.S.) · Check Point Software Technologies Ltd. (Israel) · Zscaler, Inc. (U.S.) · Okta, Inc. (U.S.) · CyberArk Software Ltd. (Israel) · Trend Micro Incorporated (Japan) · Broadcom Inc. (U.S.) · Microsoft Corporation (U.S.) · IBM Corporation (U.S.) · Sophos Ltd (U.K.) · Trellix (U.S.) · SentinelOne, Inc. (U.S.) · Cloudflare, Inc. (U.S.) · Netskope, Inc. (U.S.) · Qualys, Inc. (U.S.) · Rapid7, Inc. (U.S.) · Tenable, Inc. (U.S.) |

|

Market Opportunities |

· Growing adoption of zero-trust security frameworks across enterprises · The rapid expansion of multi-cloud and hybrid cloud environments · Increasing deployment of Internet of Things (IoT), edge computing, and remote workforce technologies |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Cybersecurity Mesh Market Trends

Trend: Rising Adoption of Zero-Trust Security Architectures

Organizations are increasingly adopting cybersecurity mesh architectures to secure highly distributed digital environments, enabling identity-centric protection across users, devices, applications, and cloud resources without relying on traditional network perimeters. The integration of AI-driven analytics enables continuous risk assessment, automated policy enforcement, and real-time threat detection across interconnected ecosystems. Enterprises are similarly leveraging cybersecurity mesh frameworks to improve security visibility through centralized governance models, while cloud-native technologies create flexible environments that support secure access across hybrid and multi-cloud infrastructures.

For instance, in May 2025, Palo Alto Networks expanded its platform-based security strategy by enhancing AI-powered security operations and zero-trust capabilities, supporting broader adoption of cybersecurity mesh principles across distributed enterprise environments.

Cybersecurity Mesh Market Dynamics

Key Market Driver: Growing Need to Secure Distributed Hybrid and Multi-Cloud Environments

The rapid expansion of hybrid work models and multi-cloud infrastructures has created substantial demand for cybersecurity mesh solutions that can protect identities, applications, and data across decentralized environments impossible to secure through perimeter-based approaches. Enterprises, government agencies, and critical infrastructure operators are deploying cybersecurity mesh architectures as a core component of their security strategy, reducing risks, improving visibility, and strengthening resilience against sophisticated cyber threats.

For instance, in April 2025, Cisco Systems introduced new security innovations focused on unified visibility and zero-trust access controls, reinforcing the growing demand for cybersecurity mesh deployments in complex enterprise networks.

Key Restraint/Challenge: Complexity of Integration Across Diverse Security Ecosystems

A significant restraint in the cybersecurity mesh market is the complexity associated with integrating security tools across diverse IT environments. Modern cybersecurity ecosystems incorporate multiple cloud platforms, endpoint solutions, identity systems, and network security technologies, demanding substantial effort for interoperability, configuration, and ongoing management. The operational burden extends to policy synchronization, security monitoring, and workforce training, making implementation challenging for organizations with limited cybersecurity expertise and fragmented technology infrastructures.

For instance, in 2025, many large enterprises reported challenges associated with consolidating legacy security systems into unified cybersecurity mesh frameworks, reflecting the broader difficulty of achieving seamless interoperability across heterogeneous environments

Key Market Opportunity: Expansion of AI-Driven Security Analytics and Automated Threat Response Platforms

The integration of artificial intelligence in cybersecurity mesh architectures presents a significant market opportunity. AI-enabled platforms can deliver adaptive threat detection, automated incident response, and real-time risk prioritization, while supporting large-scale protection of distributed digital assets. The development of cloud-native security platforms and security-as-a-service models is further democratizing access to advanced cybersecurity capabilities, opening growth opportunities across cost-sensitive markets in Asia-Pacific, Latin America, and the Middle East.

For instance, in June 2025, CrowdStrike expanded AI-powered threat detection and automated security operations capabilities within its platform, highlighting the growing opportunity for intelligent cybersecurity mesh solutions across global enterprises.

Cybersecurity Mesh Market Scope

The cybersecurity mesh market is segmented on the basis of security type, enterprise size, deployment mode, and end user.

- By Security Type

On the basis of security type, the cybersecurity mesh market is segmented into identity & access management (IAM), network security, endpoint security, data security, application security, and cloud security. The identity & access management (IAM) segment dominated the market with a 39.84% share in 2025, owing to the growing need for identity-centric security frameworks across distributed enterprise environments. Organizations are increasingly prioritizing identity verification, multi-factor authentication, privileged access management, and zero-trust strategies to reduce unauthorized access risks. IAM solutions serve as the foundation of cybersecurity mesh architectures by enabling secure access regardless of user location or device type. Rising adoption of remote work models and cloud applications is further driving demand for advanced identity governance capabilities. Regulatory requirements related to data privacy and access control are also encouraging broader deployment. Its critical role in securing digital identities continues to support its leadership position in the market.

The cloud security segment is projected to register the fastest growth at a CAGR of 14.5% from 2026 to 2033, driven by the rapid expansion of cloud-native applications and multi-cloud infrastructures. Organizations are increasingly migrating workloads to public, private, and hybrid cloud environments, creating greater demand for cloud-focused security controls. Cloud security solutions provide visibility, threat detection, compliance monitoring, and workload protection across distributed ecosystems. Continuous growth in SaaS adoption and digital transformation initiatives is accelerating deployment rates. Increasing cyberattacks targeting cloud assets are encouraging organizations to strengthen cloud security investments. Advancements in AI-driven monitoring and automated threat response capabilities are further supporting market expansion. Growing dependence on cloud infrastructure is expected to sustain strong growth throughout the forecast period.

- By Enterprise Size

On the basis of enterprise size, the cybersecurity mesh market is segmented into large enterprises and small & medium enterprises (SMEs). The large enterprises segment dominated the market with a 64.28% share in 2025, driven by complex IT infrastructures, extensive digital assets, and higher cybersecurity spending capabilities. Large organizations typically manage multiple cloud environments, remote workforces, and geographically distributed operations that require advanced security frameworks. Cybersecurity mesh solutions help these enterprises achieve centralized visibility and policy enforcement across diverse systems. Stringent regulatory requirements and increasing exposure to sophisticated cyber threats are further supporting adoption. These organizations also possess the resources needed to implement and maintain advanced security architectures. Their strong focus on business continuity and risk management continues to reinforce segment dominance.

The small & medium enterprises (SMEs) segment is expected to witness the fastest growth at a CAGR of 13.8% from 2026 to 2033, driven by rising awareness of cybersecurity risks and growing digitalization among smaller businesses. SMEs are increasingly becoming targets of ransomware, phishing, and data breach attacks, prompting greater investment in modern security solutions. Cloud-based cybersecurity mesh platforms offer scalable and cost-effective protection without requiring extensive in-house expertise. The availability of managed security services is making advanced security capabilities more accessible to resource-constrained organizations. Government initiatives promoting cybersecurity adoption among SMEs are also contributing to market growth. Increasing reliance on digital commerce and remote operations is further accelerating demand. As cybersecurity becomes a strategic priority, adoption within this segment is expected to rise significantly.

- By Deployment Mode

On the basis of deployment mode, the cybersecurity mesh market is segmented into cloud, on-premises, and hybrid. The Cloud segment dominated the market with a 61.37% share in 2025, owing to its scalability, flexibility, and ability to secure distributed environments efficiently. Organizations are increasingly adopting cloud-based cybersecurity platforms to protect remote users, cloud applications, and geographically dispersed assets. Cloud deployment enables centralized management, faster updates, and lower infrastructure costs compared to traditional security models. The growth of SaaS, hybrid work arrangements, and digital transformation initiatives is further strengthening adoption. Businesses also benefit from rapid deployment and enhanced threat intelligence capabilities. Its ability to support dynamic and evolving security requirements continues to drive market leadership.

The hybrid segment is projected to register the fastest growth at a CAGR of 14.2% from 2026 to 2033, driven by the increasing need to secure both on-premises and cloud-based resources simultaneously. Many organizations are adopting hybrid IT strategies to balance operational flexibility, regulatory compliance, and performance requirements. Hybrid cybersecurity mesh solutions provide unified security controls across diverse environments while maintaining visibility and governance. The growing complexity of enterprise infrastructure is creating demand for integrated security approaches. Organizations seeking gradual cloud migration are particularly favoring hybrid deployments. Advances in interoperability and centralized security orchestration are further accelerating adoption. This deployment model is expected to gain traction as businesses continue modernizing their technology ecosystems.

- By End User

On the basis of end user, the cybersecurity mesh market is segmented into BFSI, IT & telecom, healthcare & life sciences, government & defense, retail & e-commerce, manufacturing, energy & utilities, education, transportation & logistics, and others. The BFSI segment dominated the market with a 24.63% share in 2025, driven by the sector’s need to protect highly sensitive financial and customer information. Financial institutions face persistent threats from cybercriminals targeting digital banking platforms, payment systems, and transactional data. Cybersecurity mesh architectures help strengthen identity management, fraud prevention, and threat detection capabilities across distributed networks. Strict regulatory compliance requirements further encourage investment in advanced security frameworks. The rapid growth of digital banking and fintech services is increasing security demands. High cybersecurity spending and continuous modernization initiatives support the segment’s leading position in the market.

The healthcare & life sciences segment is expected to witness the fastest growth at a CAGR of 15.1% from 2026 to 2033, driven by increasing digitalization of healthcare systems and the growing volume of sensitive patient data. Hospitals, clinics, and research organizations are becoming frequent targets of ransomware and data breach attacks. Cybersecurity mesh solutions help secure electronic health records, connected medical devices, and cloud-based healthcare platforms. Regulatory requirements surrounding patient privacy and data protection are accelerating implementation. The expansion of telehealth services and remote healthcare delivery is creating additional security challenges that require advanced protection mechanisms. Growing investments in healthcare IT infrastructure are further supporting adoption. The need to safeguard critical healthcare operations is expected to drive strong growth throughout the forecast period.

Cybersecurity Mesh Market Regional Analysis

North America dominated the cybersecurity mesh market with the largest revenue share of 37.92% in 2025, supported by high cybersecurity spending, early adoption of zero-trust frameworks, and the presence of major security technology providers. The region also benefits from stringent data protection regulations, strong implementation of zero-trust security frameworks, and growing deployment of cybersecurity mesh architectures across BFSI, healthcare, government, and technology sectors. Increasing frequency of sophisticated cyberattacks and rising investments in AI-powered security platforms continue to accelerate market adoption. Growing focus on securing distributed workforces, multi-cloud environments, and critical digital infrastructure continues to strengthen North America’s leadership position in the global market.

U.S. Cybersecurity Mesh Market Insight

The U.S. cybersecurity mesh market is witnessing strong growth due to rising investments in advanced cybersecurity frameworks, zero-trust initiatives, and cloud security technologies. The country’s mature digital ecosystem, along with increasing adoption of AI-powered security analytics, identity-centric security solutions, and cloud-native platforms, is driving demand across BFSI, healthcare, government, and technology sectors. In addition, growing emphasis on protecting critical infrastructure and mitigating sophisticated cyber threats is accelerating cybersecurity mesh adoption across enterprises and public sector organizations.

Europe Cybersecurity Mesh Market Insight

The Europe cybersecurity mesh market remains a major contributor to global revenue, driven by strong regulatory compliance requirements, technological innovation, and high demand for advanced cybersecurity solutions. The widespread adoption of cybersecurity mesh architectures across financial services, healthcare, government, and manufacturing industries is supporting market expansion throughout the region. Increasing investments in cloud security technologies, coupled with stringent data protection regulations and growing digital transformation initiatives, continue to enhance the adoption of cybersecurity mesh solutions across Europe.

U.K. Cybersecurity Mesh Market Insight

The U.K. cybersecurity mesh market is experiencing steady growth, supported by rising adoption of zero-trust security frameworks, cloud computing technologies, and digital transformation strategies. Increasing investments in advanced cybersecurity infrastructure and growing demand for scalable, identity-centric security solutions are contributing to market growth. Furthermore, integration of AI, automation, and threat intelligence technologies is improving security effectiveness and operational efficiency, positioning the U.K. as a key innovation hub in the cybersecurity mesh industry.

Germany Cybersecurity Mesh Market Insight

The Germany cybersecurity mesh market is expanding steadily due to the country’s strong industrial base, advanced technology capabilities, and increasing adoption of next-generation cybersecurity architectures. Enterprises, government agencies, and critical infrastructure operators are increasingly utilizing cybersecurity mesh solutions for identity protection, threat detection, and security management activities. Continuous advancements in AI-driven security analytics, cloud security technologies, and zero-trust frameworks, along with strong government focus on digital resilience and data protection, are further driving market growth in Germany.

Asia-Pacific Cybersecurity Mesh Market Insight

The Asia-Pacific cybersecurity mesh market is expected to witness rapid growth, driven by increasing digitalization, expanding cloud adoption, and rising investments in cybersecurity infrastructure across countries such as China, India, and Japan. Growing awareness regarding cyber risks, rising adoption of advanced security technologies, and increasing demand for scalable and cost-effective security solutions are supporting regional market expansion. In addition, the growing presence of digital enterprises and cloud-based services is accelerating cybersecurity mesh adoption across commercial and public sector organizations.

Japan Cybersecurity Mesh Market Insight

The Japan cybersecurity mesh market is witnessing consistent growth due to rising investments in advanced cybersecurity technologies, digital innovation, and data protection initiatives. Enterprises, financial institutions, and government organizations are increasingly adopting cybersecurity mesh solutions for threat prevention, risk management, and security modernization purposes. Moreover, increasing integration of AI-driven security platforms and the country’s focus on secure and resilient digital infrastructure are further contributing to market growth.

China Cybersecurity Mesh Market Insight

The China cybersecurity mesh market is growing rapidly, driven by increasing digital transformation, expanding cloud infrastructure, and rising government focus on cybersecurity and data governance. Growing adoption of AI-enabled security platforms and cloud-based cybersecurity solutions across financial, industrial, and technology sectors is significantly boosting market demand. In addition, rising investments in cybersecurity infrastructure, increasing awareness regarding cyber resilience, and rapid technological advancements are positioning China as one of the fastest-growing markets for cybersecurity mesh solutions globally.

Cybersecurity Mesh Market Share

The cybersecurity mesh industry is primarily led by well-established companies, including:

- Palo Alto Networks, Inc. (U.S.)

- Cisco Systems, Inc. (U.S.)

- Fortinet, Inc. (U.S.)

- CrowdStrike, Inc. (U.S.)

- Check Point Software Technologies Ltd. (Israel)

- Zscaler, Inc. (U.S.)

- Okta, Inc. (U.S.)

- CyberArk Software Ltd. (Israel)

- Trend Micro Incorporated (Japan)

- Broadcom Inc. (U.S.)

- Microsoft Corporation (U.S.)

- IBM Corporation (U.S.)

- Sophos Ltd (U.K.)

- Trellix (U.S.)

- SentinelOne, Inc. (U.S.)

- Cloudflare, Inc. (U.S.)

- Netskope, Inc. (U.S.)

- Qualys, Inc. (U.S.)

- Rapid7, Inc. (U.S.)

- Tenable, Inc. (U.S.)

Latest Developments in Cybersecurity Mesh Market

- In June 2025, Cisco announced major enhancements to its security portfolio with new Hybrid Mesh Firewall capabilities and Universal Zero Trust Network Access (ZTNA) solutions designed for the AI era. The launch strengthens identity-driven security, improves visibility across hybrid environments, and simplifies policy management, reinforcing cybersecurity mesh architectures for distributed enterprises

- In April 2025, Google Cloud introduced Google Unified Security, an integrated security platform that combines threat intelligence, security operations, cloud security, and AI-powered security agents into a unified environment. The development enables organizations to secure complex hybrid and multi-cloud infrastructures more effectively, supporting cybersecurity mesh principles through centralized visibility and coordinated protection

- In April 2025, Check Point Software Technologies and Illumio announced a strategic partnership to integrate their security platforms, enabling organizations to accelerate zero-trust adoption through AI-powered threat prevention and microsegmentation. The collaboration improves breach containment, prevents lateral movement across hybrid and multi-cloud environments, and strengthens cybersecurity mesh deployments

- In May 2024, Palo Alto Networks launched Prisma SASE 3.0, introducing AI-powered data security, an integrated enterprise browser, and enhanced Zero Trust capabilities for managed and unmanaged devices. The platform improves secure access, application performance, and centralized security management, supporting enterprises adopting cybersecurity mesh and distributed security architectures

- In January 2024, Zscaler announced the launch of Zero Trust SASE, an AI-powered single-vendor Secure Access Service Edge (SASE) platform integrating Zero Trust SD-WAN with cloud-native security services. The solution simplifies secure connectivity across users, devices, branches, and workloads while strengthening cybersecurity mesh deployments through unified policy enforcement and identity-based protection

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.