Global Cystinuria Treatment Market

Market Size in USD Million

USD

120.17 Million

USD

191.53 Million

2024

2032

USD

120.17 Million

USD

191.53 Million

2024

2032

| 2025 - 2032 | |

| USD 120.17 Million | |

| USD 191.53 Million | |

| % | |

|

Cystinuria Treatment Market Size

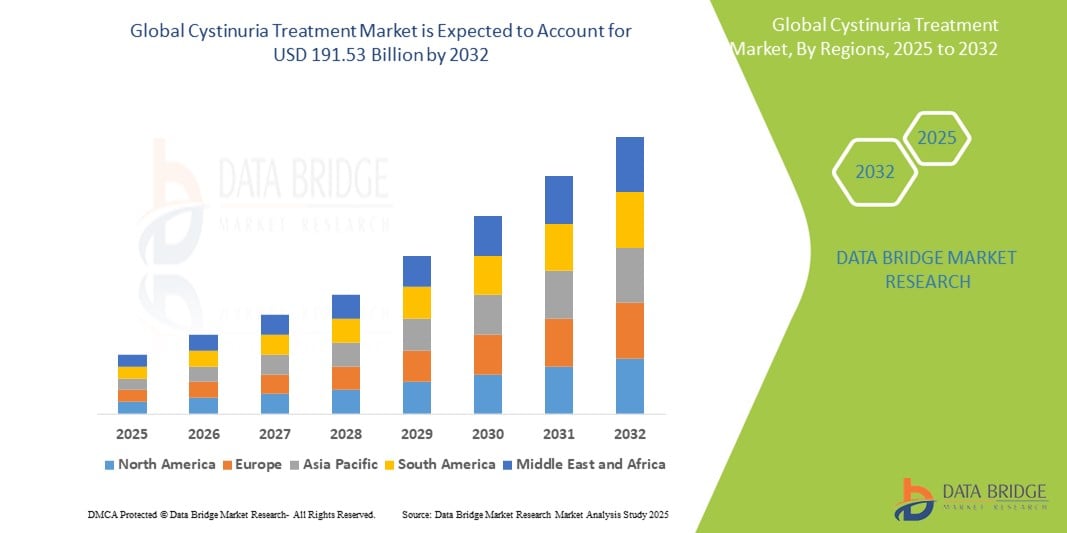

- The global cystinuria treatment market size was valued at USD 120.17 Million in 2024 and is expected to reach USD 191.53 billion by 2032, at a CAGR of 6.00% during the forecast period

- The global cystinuria treatment market growth is largely fueled by the increasing prevalence of cystinuria and rising healthcare expenditure, alongside growing strategic collaborations among market players and a surge in research and development activities for novel therapeutic agents, leading to increased demand for condition-specific treatments in both developed and developing regions

- Furthermore, increasing awareness of cystinuria and the availability of advanced diagnostic tools are establishing conservative management, pharmacotherapy (e.g., thiols, alkalinizing agents), and surgical intervention as the preferred treatment approaches. These converging factors are accelerating the adoption of personalized treatment strategies, thereby significantly boosting the global cystinuria treatment market's growth

Cystinuria treatment Market Analysis

- Cystinuria treatments, encompassing conservative management (e.g., increased hydration, dietary modifications), pharmacotherapy (e.g., thiol-based drugs, alkalinizing agents), and surgical interventions, are increasingly vital components of managing this rare genetic disorder in various patient populations due to their potential for preventing stone formation, alleviating symptoms, and improving patient outcomes

- The escalating demand for effective cystinuria treatments is primarily fueled by a greater understanding of the disease, advancements in diagnostic tools (e.g., genetic testing, advanced imaging), and a growing emphasis on multidisciplinary patient management

- North America holds a significant revenue share in the global cystinuria treatment market in 2025, characterized by early adoption of advanced therapies, high healthcare expenditure, and a strong presence of key research institutions and specialized hospitals, with the U.S. experiencing substantial growth in the adoption of personalized treatment approaches, particularly in specialized nephrology clinics and academic medical facilities, driven by innovations in drug development and improved diagnostic capabilities

- Asia-Pacific is expected to be the fastest-growing region in the global cystinuria treatment market during the forecast period due to increasing healthcare access, rising awareness of rare genetic disorders, and growing investments in healthcare infrastructure

- The Pharmacotherapy segment (by Treatment) is expected to be a significant segment in the global cystinuria treatment market in 2025, driven by the inherent need for effective systemic agents to reduce cystine excretion and improve its solubility in urine, thereby preventing recurrent stone formation

Report Scope and Cystinuria Treatment Market Segmentation

|

Attributes |

Cystinuria Treatment Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Cystinuria Treatment Market Trends

“Enhanced Treatment Precision Through Advanced Diagnostics and Personalized Approaches”

- A significant and accelerating trend in the global cystinuria treatment market is the deepening integration with advanced diagnostic technologies and personalized treatment strategies, informed by genetic profiling and biochemical monitoring innovations. This fusion of technologies is significantly enhancing treatment precision and improving patient outcomes

- For instance, advanced genetic testing for SLC3A1 and SLC7A9 mutations is increasingly being used to identify the specific type of cystinuria and to understand the underlying genetic defect, allowing clinicians to tailor treatment plans based on individual patient characteristics. Similarly, precise 24-hour urine cystine analysis and monitoring of urinary pH are crucial for guiding therapeutic adjustments and optimizing medication dosages

- Integration of sophisticated diagnostics in cystinuria treatment enables features such as identifying patients who may benefit most from specific pharmacological agents and predicting their response to treatment, leading to more intelligent clinical decision-making. For instance, understanding the specific genetic mutation might influence the choice of a thiol-binding drug or indicate suitability for future gene therapies

- The seamless integration of diagnostic insights with various treatment modalities facilitates a more coordinated and effective approach to managing this complex genetic disorder.Through a unified treatment plan, specialists can integrate dietary modifications, urine alkalinization, pharmacotherapy (e.g., thiol-binding agents), and, when necessary, surgical interventions, creating a comprehensive and individualized patient experience. Furthermore, continuous monitoring through remote tools and telemedicine offers patients maximized stone prevention with minimized burden.

- This trend towards more precise, targeted, and interconnected treatment strategies is fundamentally reshaping expectations for cystinuria management. Consequently, research institutions and pharmaceutical companies are developing novel therapies based on molecular targets and exploring innovative combination strategies with existing conservative treatments.

- The demand for cystinuria treatments that offer seamless integration of advanced diagnostics and personalized approaches is growing rapidly across both specialized nephrology clinics and research institutions, as clinicians increasingly prioritize efficacy, reduced stone recurrence, and improved patient quality of life.

Cystinuria Treatment Market Dynamics

Driver

“Growing Need Due to Rising Cystinuria Prevalence and Advanced Diagnostic and Therapeutic Approaches”

- The increasing prevalence of cystinuria, a rare genetic disorder characterized by recurrent kidney stone formation due to impaired cystine transport, along with the growing focus on early detection and precision medicine, is a significant driver for the heightened demand in the global cystinuria treatment market

- For instance, innovations in genetic testing and advanced urinary amino acid analysis are increasingly being utilized to accurately diagnose various types of cystinuria (Cystinuria Type I, Cystinuria Type II, Cystinuria Type III), supporting efforts to personalize treatment and management strategies. Such diagnostic advancements are expected to drive the growth of the cystinuria market over the forecast period

- As healthcare professionals become more attuned to the clinical presentation and long-term complications of cystinuria, there is a rising demand for enhanced diagnostic accuracy and effective therapies. Advanced tools now enable early detection through molecular analysis, and therapeutic monitoring through biomarkers and targeted approaches such as pharmacogenomic profiling

- Furthermore, the growing interest in gene therapy and precision pharmacotherapy (Gene Therapy, Pharmacotherapy, Copper Injection Therapy), combined with expanding access to patient-centric care in diverse settings (Hospitals, Homecare, Specialty Clinics, Others), is positioning these advanced solutions as essential components of the cystinuria care continuum. These developments are facilitating integration into multidisciplinary care models and boosting overall market penetration

- The benefit of early diagnosis, identification of gene mutations responsible for cystinuria, and tailored treatment plans using drugs such as Penicillamine, Tiopronin, and Captopril (By Drugs: Penicillamine, Tiopronin, Captopril, Others) are pivotal factors driving the adoption of modern treatment strategies. Additionally, the increasing preference for both Oral and Injectable (By Route of Administration: Oral, Injectable) modalities and the expanding reach of Hospital, Online, and Retail Pharmacies (By Distribution Channel: Hospital Pharmacy, Online Pharmacy, Retail Pharmacy, Others) are further enhancing market accessibility and growth

Restraint/Challenge

“Concerns Regarding Diagnostic Complexity and Treatment Costs”

- Concerns surrounding the diagnostic complexity and genetic heterogeneity of cystinuria pose a significant challenge to broader market understanding and effective management. As cystinuria presents with varying severity, onset ages, and response to treatment based on genetic subtypes (Cystinuria Type I, Type II, and Type III), accurate diagnosis and long-term disease monitoring can be challenging, raising concerns among healthcare professionals regarding optimal treatment planning and patient outcomes

- For instance, differentiating cystinuria from other causes of recurrent nephrolithiasis, especially in pediatric and adolescent populations, often requires comprehensive metabolic panels and genetic testing—procedures that are not universally available or standardized across healthcare systems. The lack of widespread awareness and consistent diagnostic protocols for cystinuria further contributes to delayed or missed diagnoses

- Addressing these diagnostic challenges through improved access to genetic screening, standardized urine amino acid testing, and awareness campaigns is crucial to enhance early detection and management. Leading academic and specialty centers advocate for multidisciplinary nephrology and urology collaboration in managing such rare disorders, offering integrated care pathways and personalized treatment plans. Additionally, the relatively high cost associated with long-term pharmacotherapy (e.g., Penicillamine, Tiopronin), dietary management, and potential surgical interventions—compared to symptomatic treatment can be a barrier to comprehensive care, especially in low-resource settings or where insurance coverage is limited

- While treatment costs may be mitigated through reimbursement programs in certain regions, the perception of cystinuria as a lifelong, resource-intensive condition can still hinder proactive care planning and timely intervention, particularly for patients from underserved communities or with limited financial resources

- Overcoming these challenges through collaborative research to refine diagnostic standards, the development of more affordable therapeutic options (e.g., cost-effective generics or biosimilars), and expanded access to specialty care networks will be essential to improve patient outcomes and support sustained growth in the cystinuria treatment market

Cystinuria Treatment Market Scope

The market is segmented on the basis of type, therapy type, drugs, route of administration, end users, and distribution channel.

By Therapy type

On the basis of therapy type, the cystinuria treatment market is segmented into gene therapy, pharmacotherapy, and copper injection therapy. The pharmacotherapy segment dominates the largest market revenue share, driven by its established role in managing cystine stone formation and its accessibility as the primary line of treatment across diverse healthcare settings. Drugs such as penicillamine and tiopronin are frequently prescribed to reduce cystine concentration in urine, directly targeting the biochemical root of the disease and lowering the risk of stone recurrence. Healthcare professionals often prioritize pharmacological interventions due to their ability to provide long-term management of this chronic condition, especially in patients who are not candidates for more invasive therapies.

The gene therapy and copper injection therapy segments are also significant due to their growing relevance in personalized medicine and targeted treatment approaches for genetically defined metabolic disorders like cystinuria. Gene therapy holds long-term promise in correcting the underlying genetic mutations, potentially offering curative outcomes, while copper injection therapies may support metabolic stabilization in select patient populations. Although still under development or limited to specific use cases, these therapies reflect a broader trend toward precision treatment and innovation in rare disease management. The rising number of clinical studies and targeted R&D investments are expected to further expand the adoption of these advanced therapeutic modalities in the forecast period.

By Drugs

On the basis of drugs, the cystinuria treatment market is segmented into penicillamine, tiopronin, captopril, and others. The penicillamine and tiopronin segments collectively held a significant market revenue share in the historical period, driven by their established use in reducing cystine concentrations in urine and preventing recurrent kidney stone formation. These medications function as thiol-binding agents, which enhance cystine solubility and are widely prescribed as part of long-term pharmacological management in cystinuria patients.

The captopril and others segments are also crucial and are anticipated to witness steady growth, supported by their adjunctive role in managing specific cases of cystinuria, especially among patients with contraindications to primary therapies or who require combination treatment strategies. These drugs may offer additional clinical benefits in terms of blood pressure control and stone prevention, contributing to their continued use in targeted treatment regimens. The ongoing research into optimizing dosage, reducing side effects, and improving patient adherence is further supporting the role of these therapies in the broader cystinuria treatment landscape.

By Route of Administration

On the basis of route of administration, the cystinuria treatment market is segmented into oral and injectable. The oral segment held the largest market revenue share in the historical period, driven by the widespread use of oral pharmacotherapies such as penicillamine and tiopronin, which are considered first-line treatments for managing cystine levels and preventing stone recurrence. Oral administration is preferred due to its ease of use, non-invasiveness, and suitability for long-term outpatient management, making it the most accessible and patient-compliant option.

The injectable segment is also significant and is anticipated to witness steady growth, supported by its role in administering specific therapies, such as experimental gene therapies or adjunct treatments where oral formulations are either ineffective or contraindicated. Injectable therapies may offer faster onset of action in certain clinical scenarios and are increasingly considered in more severe or complex cases of cystinuria. Advances in drug delivery systems and growing interest in precision medicine approaches are contributing to the evolving role of injectable options within the cystinuria treatment landscape.

By End Users

On the basis of end users, the cystinuria treatment market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment held the largest market revenue share in the historical period, driven by the comprehensive diagnostic capabilities, access to multidisciplinary care teams, and availability of advanced treatment infrastructure within hospital settings. Hospitals are often the primary point of care for initial diagnosis, acute management of stone episodes, and surgical interventions, making them central to the overall cystinuria treatment pathway.

The homecare, specialty clinics, and others segments are also significant and are anticipated to witness steady growth, supported by the rising trend toward decentralized care and chronic disease management in more accessible settings. Specialty clinics offer tailored nephrology and urology services, while homecare is increasingly preferred for medication administration and dietary monitoring, especially in stable patients requiring long-term follow-up. The continued expansion of outpatient care models and integration of telehealth solutions are further enhancing the role of these end-user segments in the cystinuria treatment ecosystem

Cystinuria Treatment Market Regional Analysis

- North America holds a notable position in the cystinuria treatment market with a significant revenue share, driven by a strong diagnostic infrastructure, early adoption of rare disease management strategies, and increasing patient awareness of genetic and metabolic conditions.

- Healthcare professionals in the region highly value access to advanced metabolic testing, genetic screening services, and established pharmacological treatments such as tiopronin and penicillamine for long-term cystinuria management.

- This focus on early diagnosis and personalized therapy is further supported by active research institutions, dedicated urology and nephrology centers, and growing patient support organizations, positioning North America as a key hub for innovative and standardized care approaches in both hospital-based and outpatient settings.

U.S. Cystinuria Treatment Market Insight

The U.S. cystinuria treatment market captured a significant revenue share within North America, fueled by the growing emphasis on early diagnosis and the long-term management of rare genetic and metabolic disorders. Healthcare professionals are increasingly prioritizing improved patient outcomes through advanced diagnostic tools such as amino acid analysis, genetic testing, and individualized pharmacological interventions. The expanding role of multidisciplinary care teams, coupled with the widespread availability of specialized nephrology and urology centers and strong clinical research efforts, further supports the evolution of the cystinuria treatment landscape. Moreover, the rising adoption of patient-specific treatment regimens, including the use of thiol-based drugs and ongoing exploration of gene therapy, is significantly contributing to innovation and market growth in the United States

Europe Cystinuria Treatment Insight

The European cystinuria treatment market is projected to expand at a notable CAGR throughout the forecast period, primarily driven by a well-developed healthcare infrastructure and increasing awareness of cystinuria as a manageable genetic disorder. The rise in diagnostic capabilities, including access to genetic testing and specialized metabolic screening, is supporting the early identification and classification of cystinuria cases. European healthcare providers are also emphasizing improved patient outcomes and quality of life through personalized and multidisciplinary treatment approaches. The region is witnessing notable progress in both pharmacotherapy (e.g., tiopronin, captopril) and emerging innovations such as gene therapy, with these treatments being incorporated across leading nephrology centers and rare disease clinics

U.K. Cystinuria Treatment Market Insight

The U.K. cystinuria treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing focus on early diagnosis and specialized management of genetic and metabolic disorders. Additionally, the growing recognition of cystinuria as a treatable condition is encouraging both healthcare providers and research institutions to adopt advanced diagnostic and therapeutic solutions. The U.K.’s commitment to healthcare innovation, alongside its well-established network of nephrology centers and specialized urology clinics, is expected to continue stimulating market growth in the management of cystinuria. With the increasing availability of genetic testing, pharmacotherapies, and emerging treatment options like gene therapy, the U.K. is positioned to lead advancements in the management of this rare condition.

Germany Cystinuria Treatment Market Insight

The German cystinuria treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of the potential for effective long-term management and the demand for advanced, evidence-based therapies. Germany’s well-developed healthcare system, combined with its focus on research and patient-centric care, encourages the adoption of innovative diagnostic and therapeutic strategies for cystinuria, particularly in specialized nephrology centers and academic hospitals. The integration of advanced genetic testing, along with the continued use of pharmacotherapies such as penicillamine and tiopronin, is driving significant progress in patient management and offering new treatment options for patients with this rare genetic disorder.

Asia-Pacific Cystinuria Treatment Market Insight

The Asia-Pacific cystinuria treatment market is expected to grow at a notable CAGR during the forecast period, driven by increasing awareness of rare metabolic disorders and the demand for more effective treatment options. The region’s rapidly advancing healthcare systems, combined with improving access to specialized care and diagnostic technologies, are fostering the adoption of advanced treatments for cystinuria. Healthcare providers in Asia-Pacific are increasingly focusing on early diagnosis, personalized treatment plans, and the integration of genetic testing and pharmacotherapies. The growing presence of specialized nephrology centers and the expansion of research initiatives are also contributing to market growth. Additionally, the introduction of newer therapies, such as gene therapy, and the increasing use of existing pharmacological treatments like tiopronin and penicillamine, are expected to further enhance the treatment landscape for cystinuria in the region

Japan Cystinuria Treatment Market Insight

The Japan cystinuria treatment market is gaining attention due to the country’s advanced medical infrastructure, rapidly aging population, and emphasis on high-quality care for rare genetic disorders. Japan places significant focus on accurate diagnostic methods and effective treatments for cystinuria, with an increasing adoption of advanced technologies like genetic screening and metabolic testing. The growing number of specialized nephrology centers and research initiatives is driving the integration of cutting-edge diagnostic tools and pharmacological treatments, including tiopronin and penicillamine, in treatment plans. Moreover, Japan’s aging population is likely to spur demand for comprehensive and personalized care solutions in both hospital and academic settings, as early diagnosis and long-term management of cystinuria become more critical in improving patient outcomes. The country’s strong emphasis on precision medicine and research-driven care is expected to continue fostering growth in the cystinuria treatment market.

China Cystinuria Treatment Market Insight

The China cystinuria treatment market accounted for a notable revenue share in the Asia Pacific region, driven by the country’s increasing healthcare expenditure, rapid urbanization, and growing focus on rare disease management. China’s rapidly expanding healthcare infrastructure is making specialized treatments for cystinuria more accessible, especially in major hospitals and nephrology centers. The push towards improving diagnostic capabilities, such as genetic screening and metabolic testing, along with the growing adoption of pharmacological treatments like tiopronin and penicillamine, is a key driver for the market. Moreover, increased awareness among healthcare professionals, coupled with ongoing research efforts and improved patient access to healthcare services, is expected to continue propelling growth in the cystinuria treatment market in China.

Cystinuria Treatment Market Share

The cystinuria treatment industry is primarily led by well-established companies, including:

- Incepta Pharmaceuticals Ltd. (Bangladesh)

- Aktis Pharma India Pvt Ltd. (India)

- Mankind Pharma (India)

- Taro Pharmaceutical Industries Ltd. (Israel)

- Teva Pharmaceutical Industries Ltd. (Israel)

- ANI Pharmaceuticals, Inc. (United States)

- Amneal Pharmaceuticals LLC (United States)

- Abbott (United States)

- Aurobindo Pharma (India)

- Mylan N.V. (now part of Viatris Inc.) (United States)

- Bausch Health Companies Inc. (Canada)

- Zhejiang Huahai Pharmaceutical Co., Ltd. (China)

- WOCKHARDT (India)

- Amerigen Pharmaceuticals Limited (United States)

- Travere Therapeutics, Inc. (United States)

- F. Hoffmann-La Roche Ltd (Switzerland)

- AstraZeneca (United Kingdom)

- Pfizer Inc. (United States)

- Mission Pharmacal Company (United States)

- Dr. Reddy's Laboratories Ltd. (India)

- Advicenne (France)

- Viatris Inc. (United States)

- AdvaCare Pharma (Australia)

- Camber Pharmaceuticals, Inc. (United States)

- Panacea Biotec (India)

- Lupin Limited (India)

- Cycle Pharmaceuticals Limited (United Kingdom)

- Orsini Specialty Pharmacy (United States)

- Revive Therapeutics Ltd. (Canada)

- Recordati Rare Diseases Inc. (United States)

- Mission Therapeutics Ltd. (United Kingdom)

- Enterome Bioscience (France)

- Horizon Therapeutics plc (Ireland)

- Arcturus Therapeutics Holdings Inc. (United States)

- Codexis, Inc. (United States)

- Mito Pharmaceuticals, Inc. (United States)

- BridgeBio Pharma Inc. (United States)

- Bellvitge Biomedical Research Institute (Spain)

- Spyre Therapeutics Inc. (United States)

- Synlogic Inc. (United States)

- PharmaKrysto Ltd. (United Kingdom)

- Avanzanite Bioscience (United States)

Latest Developments in Global Cystinuria Treatment Market

- In March 2025, Cycle Pharmaceuticals Ltd. announced the launch of VENXXIVA™ (tiopronin) delayed-release tablets in the U.S. for patients with severe homozygous cystinuria unresponsive to standard measures. This FDA-approved treatment is available in 100 mg and 300 mg doses and is indicated for the prevention of cystine stone formation in adults and pediatric patients aged 9 years and older. A 2020 study demonstrated that patients on tiopronin therapy reported improved health-related quality of life, including better scores in social, emotional, disease, and vitality impact

- In February 2025, Advicenne received Orphan Drug Designation (ODD) from the U.S. FDA for ADV7103, a novel formulation of potassium sodium hydrogen citrate for cystinuria treatment. This designation aims to expedite the development and regulatory review of ADV7103, potentially enhancing treatment options for patients with cystinuria

- In January 2024, Travere Therapeutics announced positive top-line results from its Phase 3 clinical trial of sparsentan for the treatment of adults with cystinuria. Sparsentan is an orally administered dual endothelin receptor antagonist, and these results support its potential as a therapeutic option for cystinuria patient

- In May 2024, AstraZeneca initiated a Phase 2 clinical trial of its investigational drug, AZD9829, for the treatment of cystinuria. AZD9829 is a novel small molecule inhibitor of cystine transport, and this trial aims to evaluate its safety and efficacy in cystinuria patients

- In July 2024, Pfizer Inc. announced the acquisition of Arena Pharmaceuticals, a biopharmaceutical company with a focus on developing therapies for inflammatory diseases. This acquisition expands Pfizer's portfolio in the area of rare diseases, including cystinuria, potentially accelerating the development of new treatment options for patients

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.