Global Dairy Products Transport Market

Market Size in USD Billion

USD

11.01 Billion

USD

18.62 Billion

2024

2032

USD

11.01 Billion

USD

18.62 Billion

2024

2032

| 2025 - 2032 | |

| USD 11.01 Billion | |

| USD 18.62 Billion | |

| % | |

|

Dairy Products Transport Market Size

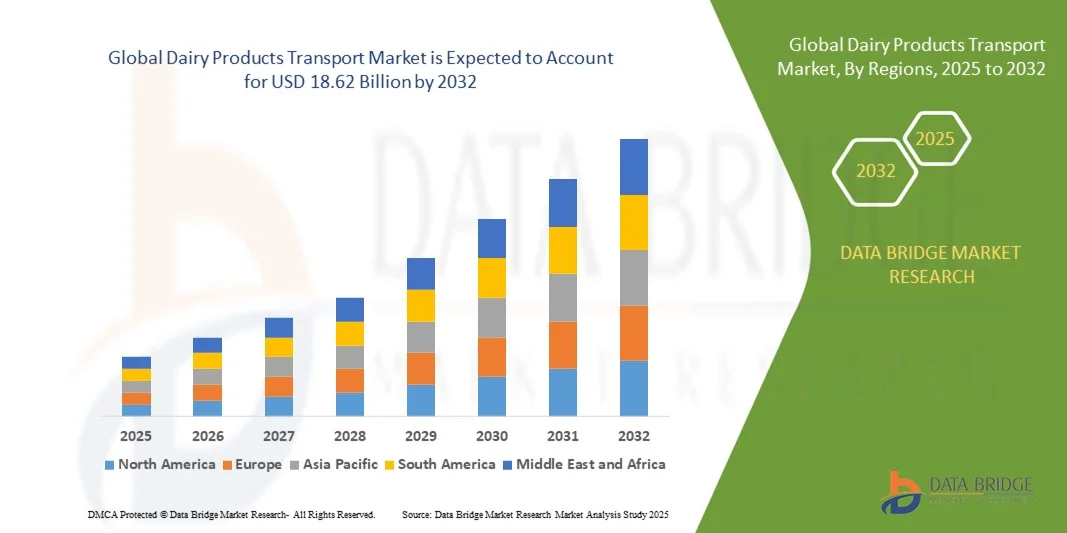

- The global dairy products transport market size was valued at USD 11.01 billion in 2024 and is expected to reach USD 18.62 billion by 2032, at a CAGR of 6.79% during the forecast period

- The market growth is largely fueled by the increasing demand for temperature-controlled logistics and advancements in cold-chain technologies, ensuring the safe transport of perishable dairy products such as milk, cheese, butter, and ice cream across long distances. The rise in global dairy trade, coupled with expanding distribution networks and export activities, is further accelerating investment in refrigerated transport infrastructure.

- Furthermore, growing consumer preference for packaged, processed, and frozen dairy items, alongside stringent food safety regulations, is prompting logistics providers to adopt advanced monitoring systems and energy-efficient refrigeration solutions. These factors collectively drive the expansion and modernization of the dairy products transport market

Dairy Products Transport Market Analysis

- Dairy products transport plays a critical role in maintaining product quality, safety, and freshness through temperature-controlled logistics systems that ensure uninterrupted cold-chain integrity from production to retail. The industry’s growth is strongly supported by the rising consumption of value-added dairy products and expanding international trade, which demand efficient, compliant transport solutions.

- The increasing integration of digital tracking technologies, electric refrigerated vehicles, and eco-friendly refrigerants is transforming the market, improving transparency and sustainability in operations. As a result, the dairy products transport sector is becoming a vital enabler of global food security and efficiency in the broader dairy supply chain

- North America dominated the dairy products transport market with a share of 33.98% in 2024, due to the extensive presence of dairy producers, advanced cold-chain infrastructure, and strong demand for perishable dairy exports

- Asia-Pacific is expected to be the fastest growing region in the dairy products transport market during the forecast period due to rapid urbanization, expanding dairy production, and modernization of cold-chain infrastructure

- Frozen food segment dominated the market with a market share of 34.6% in 2024, due to the rising preference for ready-to-cook and frozen dairy-based meals that demand continuous refrigeration throughout transit. Dairy products such as butter, cheese, and cream used in frozen food manufacturing require precise temperature control to prevent bacterial contamination. The surge in urbanization and busy lifestyles has significantly boosted frozen food consumption, compelling logistics providers to enhance their temperature-controlled fleets. Growing export activities for frozen dairy goods have also increased the reliance on reliable refrigerated transport networks

Report Scope and Dairy Products Transport Market Segmentation

|

Attributes |

Dairy Products Transport Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Dairy Products Transport Market Trends

Adoption of Electric and Energy-Efficient Refrigerated Transport

- The dairy products transport market is witnessing a major transformation driven by the increased adoption of electric and energy-efficient refrigerated vehicles. Global logistics providers are prioritizing eco-friendly cooling technologies and low-emission transport solutions to reduce their carbon footprint while maintaining strict temperature control for perishable dairy goods

- For instance, Carrier Transicold has introduced electric transport refrigeration units such as the Vector eCool system, offering zero direct emissions during operation. These systems combine energy efficiency with precise cooling management, enabling sustainable distribution of milk, cheese, and yogurt over long distances without compromising freshness

- The shift toward electric and hybrid refrigeration systems is supported by government incentives promoting cleaner commercial vehicle fleets and enhanced energy standards. These advancements are helping logistics companies lower fuel consumption, reduce greenhouse gas emissions, and comply with both regional and international environmental regulations

- In addition, technological innovation in battery efficiency and thermal storage is enhancing the reliability of refrigerated trucks used in dairy transport. These systems maintain stable temperature ranges through optimized energy management, ensuring product integrity throughout multi-stop supply chains

- The adoption of digital telematics and IoT-based temperature monitoring is improving real-time visibility and control during transit. Transport operators are leveraging these tools to track power usage, minimize temperature deviations, and achieve predictive maintenance for better delivery efficiency

- The overall movement toward electric and energy-efficient refrigerated transport signifies a long-term commitment by the dairy logistics sector to achieve sustainability targets while improving cold chain reliability. This trend strengthens both operational resilience and regulatory compliance, fostering environmental and economic stability across the supply chain

Dairy Products Transport Market Dynamics

Driver

Rising Demand for Frozen and Packaged Dairy Products

- The increasing consumption of frozen and packaged dairy goods such as cheese, butter, ice cream, and ready-to-drink milk products is significantly driving demand for reliable cold chain transportation. Changing consumer lifestyles, urbanization, and expanding retail networks are elevating the need for temperature-controlled logistics capable of preserving quality during extended distribution cycles

- For instance, logistics solutions providers such as Lineage Logistics have expanded specialized cold storage and refrigerated fleets to support large-scale distribution for leading dairy brands. Their temperature-controlled warehouses and transport systems ensure optimal moisture retention, microbial safety, and product freshness from processing plants to retail centers

- Growing awareness of food safety and hygiene standards has made consumers more conscious of the quality of dairy products during storage and transit. Hence, producers and distributors are prioritizing refrigerated logistics technologies that maintain precise temperatures and humidity levels for extended shelf stability

- In addition, the rise of e-commerce grocery platforms and doorstep delivery services for dairy products is strengthening demand for advanced cold-chain vehicles equipped with multi-compartment refrigeration. These systems allow the efficient delivery of products at varied temperature requirements within a single route

- As dairy consumption continues to rise across emerging and developed markets, the reliance on robust cold chain networks for frozen and packaged goods will remain a pivotal growth driver. This sustained demand for reliable temperature-controlled distribution is poised to expand the transport capacity and infrastructure investments across the dairy logistics industry

Restraint/Challenge

High Costs of Temperature-Controlled Logistics

- High installation, maintenance, and operational costs associated with refrigerated transport systems pose a major challenge for dairy logistics providers. The requirement for specialized temperature management equipment, insulated containers, and energy-intensive cooling systems significantly elevates overall transport expenses

- For instance, companies such as Americold Logistics incur substantial investments in maintaining refrigeration equipment, energy-efficient fleets, and temperature sensors to meet stringent quality standards for dairy transport. These costs are compounded by ongoing expenses related to fuel or electric power consumption and system calibration

- The complex setup of refrigeration units increases dependency on skilled technicians and regular preventive maintenance to prevent breakdowns during long-haul transportation. Such operational demands raise service costs and limit scalability for smaller transport providers with constrained budgets

- In addition, the volatility of energy prices directly impacts the cost-efficiency of temperature-controlled logistics operations. Maintaining consistent cooling performance across varying climatic conditions further intensifies cost pressures, particularly in regions with underdeveloped cold chain infrastructure

- Overcoming these financial constraints will require industry collaboration to develop energy-efficient cooling systems, adopt renewable power sources, and standardize modular refrigeration units. Long-term affordability and operational optimization will be critical in ensuring sustained growth and accessibility of the dairy products transport market across global supply chains

Dairy Products Transport Market Scope

The market is segmented on the basis of product type, application, and packaging type.

- By Product Type

On the basis of product type, the dairy products transport market is segmented into cheese, yoghurt, butter, buttermilk, ice cream, lactose-free milk, cream and frozen, and others. The cheese segment dominated the market with the largest revenue share in 2024, attributed to the high global demand for processed and specialty cheeses, coupled with the need for strict cold-chain maintenance during transportation. Cheese requires consistent refrigeration to prevent spoilage and maintain texture and flavor integrity, driving the demand for temperature-controlled logistics. Moreover, the expansion of cheese exports from major producers such as the U.S., France, and New Zealand has further strengthened the segment’s dominance, supported by rising consumption in fast food and ready-to-eat meals.

The ice cream segment is projected to witness the fastest growth rate from 2025 to 2032, driven by increasing global consumption of frozen desserts and the rapid expansion of premium and artisanal ice cream brands. Transporting ice cream requires ultra-low temperature logistics and advanced insulated containers to prevent melting and maintain quality throughout the supply chain. The growth of e-commerce grocery delivery platforms and convenience stores offering doorstep delivery of frozen treats has also boosted demand for specialized refrigerated transport vehicles. In addition, technological innovations in cold chain monitoring systems ensure quality assurance, further accelerating market growth for this segment.

- By Application

On the basis of application, the market is segmented into frozen food, bakery and confectionery, clinical nutrition, and others. The frozen food segment dominated the market with a share of 34.6% in 2024 due to the rising preference for ready-to-cook and frozen dairy-based meals that demand continuous refrigeration throughout transit. Dairy products such as butter, cheese, and cream used in frozen food manufacturing require precise temperature control to prevent bacterial contamination. The surge in urbanization and busy lifestyles has significantly boosted frozen food consumption, compelling logistics providers to enhance their temperature-controlled fleets. Growing export activities for frozen dairy goods have also increased the reliance on reliable refrigerated transport networks.

The clinical nutrition segment is anticipated to grow at the fastest CAGR during the forecast period, fueled by the increasing global demand for medical-grade dairy-based nutritional formulations and supplements. Products such as lactose-free milk and protein-enriched dairy solutions require hygienic and temperature-stable transportation to retain their nutritional value and safety. The expansion of healthcare logistics infrastructure and growth in hospitals, elder care facilities, and home healthcare services have further amplified transport demand in this segment. The need for compliance with pharmaceutical-grade cold chain standards is also driving innovation in specialized dairy transport systems.

- By Packaging Type

Based on packaging type, the dairy products transport market is segmented into bottles, cans, pouches, boxes, and others. The bottles segment held the largest market share in 2024, primarily driven by their extensive use in transporting milk, yoghurt, and liquid dairy beverages. Bottles offer superior protection against contamination and leakage, while being compatible with various automated filling and cooling systems used in large-scale dairy logistics. Their reusability and ease of handling in both refrigerated trucks and vending systems make them a preferred choice for transporters. The rising adoption of sustainable, recyclable bottle materials such as PET and glass further enhances their dominance.

The pouches segment is expected to register the fastest growth from 2025 to 2032, owing to their lightweight, flexible, and cost-efficient nature, which reduces overall transport costs and storage space requirements. Pouches are increasingly being adopted for milk, buttermilk, and yoghurt distribution in emerging economies where affordability and quick distribution are key. The growing focus on eco-friendly and biodegradable packaging materials has also strengthened the adoption of pouch-based transport systems. Their compatibility with cold storage and quick-chill logistics solutions further positions this segment for rapid growth during the forecast period.

Dairy Products Transport Market Regional Analysis

- North America dominated the dairy products transport market with the largest revenue share of 33.98% in 2024, driven by the extensive presence of dairy producers, advanced cold-chain infrastructure, and strong demand for perishable dairy exports

- The region benefits from well-developed refrigerated logistics networks and technological integration in temperature-controlled transport

- High consumer demand for packaged and specialty dairy items such as cheese, butter, and ice cream continues to support market growth. Rising focus on food safety regulations and the use of real-time monitoring systems further reinforce North America’s leadership in this sector

U.S. Dairy Products Transport Market Insight

The U.S. dairy products transport market accounted for the largest share of the North American market share in 2024, supported by the country’s large-scale dairy production and extensive distribution networks. The rise in domestic dairy consumption, coupled with growing exports to Asia and Latin America, is driving refrigerated logistics investments. Advanced cold-storage technologies and automation in transport fleets enhance efficiency and product quality. The U.S. market also benefits from sustainability-driven shifts toward energy-efficient vehicles and eco-friendly refrigerants in dairy transport operations.

Europe Dairy Products Transport Market Insight

The Europe dairy products transport market is projected to expand steadily during the forecast period, propelled by stringent food safety standards, cross-border trade within the EU, and increasing consumer demand for high-quality dairy products. The region’s focus on reducing food waste and improving cold-chain management systems promotes modernization in dairy logistics. Growth in cheese and yoghurt exports from countries such as France, Germany, and the Netherlands supports steady demand for refrigerated transportation solutions across the region.

Germany Dairy Products Transport Market Insight

The Germany dairy products transport market is expected to witness strong growth, driven by its position as one of Europe’s leading dairy producers and exporters. The country’s emphasis on product quality, sustainability, and technology integration in cold-chain logistics contributes significantly to market expansion. Germany’s advanced transport infrastructure and widespread use of smart sensors for temperature tracking enhance efficiency in long-distance dairy distribution across Europe.

U.K. Dairy Products Transport Market Insight

The U.K. dairy products transport market is anticipated to grow at a notable CAGR during the forecast period, fueled by rising consumption of dairy-based snacks and convenience foods. Increasing imports and exports of processed dairy items such as cheese and butter drive demand for reliable cold-chain logistics. The U.K.’s push toward sustainable transport and investment in electric refrigerated vehicles also supports the market’s evolution.

Asia-Pacific Dairy Products Transport Market Insight

The Asia-Pacific dairy products transport market is poised to grow at the fastest CAGR from 2025 to 2032, fueled by rapid urbanization, expanding dairy production, and modernization of cold-chain infrastructure. Growing demand for packaged dairy products and frozen desserts, particularly in China, India, and Japan, is driving the need for advanced refrigerated transport. Government initiatives promoting food safety and cold-chain efficiency, along with the expansion of organized retail and e-commerce food delivery, are key factors supporting market acceleration.

China Dairy Products Transport Market Insight

The China dairy products transport market captured the largest share in Asia-Pacific in 2024, driven by a booming dairy industry and rising middle-class consumption. Increased investment in cold storage facilities and digital logistics systems ensures efficient transport of perishable dairy goods across vast distances. China’s strong manufacturing base for refrigerated transport vehicles and rapid e-commerce penetration further propel market growth.

India Dairy Products Transport Market Insight

The India dairy products transport market is projected to grow at the fastest rate across the region, supported by the country’s expanding dairy sector and government efforts to modernize cold-chain logistics. Rising demand for milk, curd, and ice cream in urban areas, along with the emergence of organized dairy cooperatives and private players, is transforming transport infrastructure. Enhanced investment in refrigerated vehicles and temperature monitoring systems is expected to boost the efficiency and reliability of dairy logistics nationwide.

Dairy Products Transport Market Share

The dairy products transport industry is primarily led by well-established companies, including:

- Agri-Dairy Products, Inc. (U.S.)

- DACHSER (Germany)

- Dairy.com (U.S.)

- T.C. Jacoby & Co. (U.S.)

- Interfood (Netherlands)

- DB Schenker (Germany)

- Breeze Logistics (Australia)

- Fonterra Co-operative Group (New Zealand)

- KUEHNE + NAGEL (Switzerland)

- Agri-Best (U.S.)

- Kotahi - Global Freight Solutions (New Zealand)

- Cargill, Incorporated (U.S.)

- Burris Logistics (U.S.)

- Dairy Fresh (U.S.)

- DTL (U.K.)

- OIA Global (U.S.)

- WEL Companies (U.S.)

- W.J. Byrnes & Co. of Los Angeles, Inc. (U.S.)

- ZIM Integrated Shipping Services Ltd. (Israel)

Latest Developments in Global Dairy Products Transport Market

- In September 2025, Arla Foods and Maersk expanded their partnership by establishing a new state-of-the-art cold-store facility in Taulov, Denmark, designed specifically for temperature-controlled dairy logistics. This advanced warehouse, equipped with automated guided vehicles (AGVs) and dual temperature zones, enhances efficiency and minimizes product spoilage. The development strengthens Europe’s cold-chain capacity and supports sustainable, large-scale dairy exports across the region

- In July 2025, Razco Foods in Kenya expanded its cold-chain transport fleet with the acquisition of five new refrigerated trucks equipped with enhanced insulation and cooling systems. This investment significantly boosts the company’s ability to ensure temperature stability across long-distance dairy deliveries, particularly for ice cream and frozen milk products. The move reflects growing investment in reliable refrigerated logistics within Africa’s emerging dairy sector

- In May 2025, FrieslandCampina launched its electric milk transport initiative in partnership with Melkweg | Fritom in the Netherlands, marking a major step toward low-emission dairy logistics. The deployment of fully electric milk collection trucks, supported by fast-charging stations, reduces carbon output while maintaining consistent cold-chain performance. This innovation demonstrates a growing trend toward sustainable logistics solutions in the European dairy industry

- In March 2025, Fonterra introduced New Zealand’s first all-electric refrigerated milk collection truck in collaboration with TIL Logistics Group. The new eCanter truck operates in the Waikato region and aims to lower fuel consumption and greenhouse gas emissions across Fonterra’s transport fleet. This milestone highlights the industry’s shift toward electrification and its focus on greener, more efficient dairy collection systems

- In September 2024, Carrier Transicold unveiled its Vector HE 19 semi-trailer refrigeration unit using low-GWP refrigerant technology at the IAA Transportation Expo. Designed for enhanced energy efficiency, the system reduces emissions while maintaining precise temperature control for dairy transport. This product launch sets a benchmark for sustainable refrigerated logistics, supporting global goals for eco-friendly dairy distribution

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Dairy Products Transport Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Dairy Products Transport Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Dairy Products Transport Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.