Global Data Center Chip Market

Market Size in USD Billion

USD

17.50 Billion

USD

41.93 Billion

2025

2033

USD

17.50 Billion

USD

41.93 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 17.50 Billion |

Market Size (Forecast Year) |

USD 41.93 Billion |

CAGR |

% |

Major Markets Players |

|

Data Center Chip Market Overview

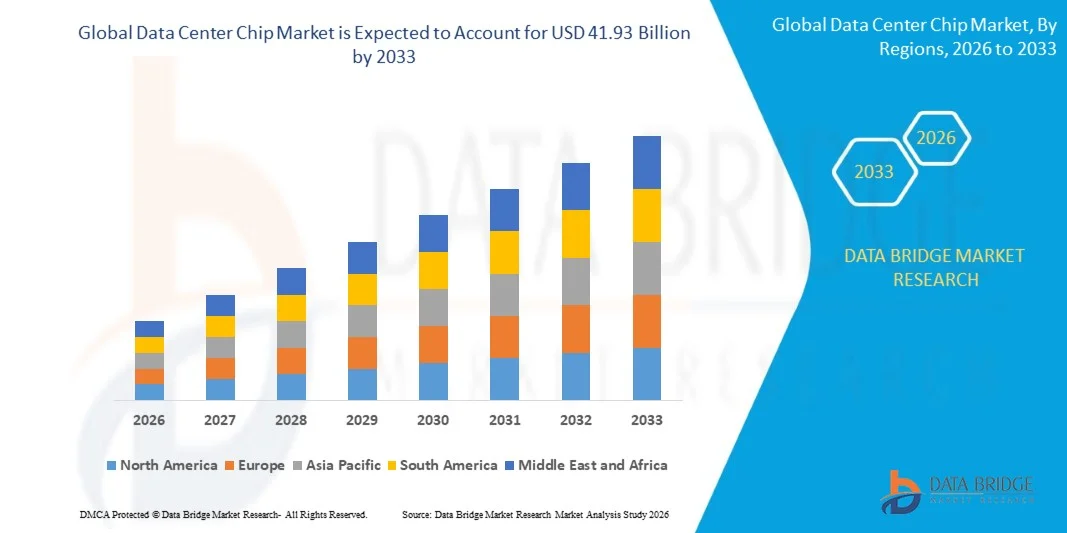

As per Data Bridge Market Research Analysis, the Data Center Chip Market was valued at USD 17.50 billion in 2025 and is projected to reach USD 41.93 billion by 2033, growing at a CAGR of 41.93% from 2026 to 2033. The market is experiencing extraordinary growth driven by the explosive demand for artificial intelligence (AI) and machine learning (ML) workloads, rapid expansion of cloud computing infrastructure, and increasing data generation across industries. Data center chips serve as the foundational processing units powering hyperscale and enterprise data centers, enabling computation, storage, and networking functions that support the modern digital economy. These specialized semiconductors—encompassing processors, memory units, accelerators, and networking components—are optimized for performance, energy efficiency, and data throughput. The market's expansion is further propelled by the global rollout of 5G infrastructure, edge computing deployments, and the accelerating digital transformation across sectors. According to industry estimates, global data creation is expected to exceed 180 zettabytes by 2025, underscoring the massive computational power required to manage, store, and process such unprecedented data volumes. Furthermore, the ongoing evolution of semiconductor fabrication technologies, including advanced process nodes and chiplet architectures, is enabling higher performance and greater energy efficiency in data center chip designs.

Key Market Trends & Insights

- Asia-Pacific emerged as the dominant regional market for data center chips in 2025, driven by rapid cloud infrastructure expansion, substantial government investments in digital initiatives, and the presence of major hyperscalers such as Alibaba Cloud, Tencent, and Huawei.

- North America is expected to be the fastest-growing region, fueled by aggressive AI infrastructure spending, strong presence of leading semiconductor vendors including NVIDIA, AMD, and Intel, and continued hyperscaler investments across the United States.

- The Graphics Processing Unit (GPU) segment led the market in 2025, driven by widespread adoption in AI training, deep learning, and high-performance computing applications.

- Application-Specific Integrated Circuits (ASICs) emerged as the fastest-growing chip type, reflecting surging demand for custom silicon optimized for specific AI inference and training workloads.

- The Artificial Intelligence & Machine Learning application segment dominated the market, supported by rapid AI adoption across industries and massive hyperscaler investments in AI infrastructure.

- Hyperscale data centers accounted for the largest market share, driven by continued expansion of major cloud service providers and their massive infrastructure deployment requirements.

- Growing adoption of heterogeneous computing architectures, combining CPUs, GPUs, and accelerators, is reshaping data center chip design and procurement strategies.

- Increasing focus on energy efficiency and sustainability is driving demand for power-optimized chip designs and advanced cooling solutions in data center operations.

Market Size & Forecast

- Global Market Value (2025): USD 17.50 Billion

- Expected Market Value (2033): USD 41.93 Billion

- Forecast CAGR (2026–2033): 41.93%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: North America

Scope and Data Center Chip Market Segmentation

|

Attributes |

Data Center Chip Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· NVIDIA Corporation (USA) · Advanced Micro Devices Inc. (USA) · Intel Corporation (USA) · Broadcom Inc. (USA) · Qualcomm Incorporated (USA) · Samsung Electronics Co. Ltd. (South Korea) · SK Hynix Inc. (South Korea) · Micron Technology Inc. (USA) · Taiwan Semiconductor Manufacturing Company (Taiwan) · Arm Holdings (UK) · Huawei Technologies Co. Ltd. (China) · Alibaba Group (China) · Tencent Holdings (China) · Amazon Web Services (USA) · Google (USA) · Microsoft Corporation (USA) · Marvell Technology Inc. (USA) · Xilinx Inc. (USA) · MediaTek Inc. (Taiwan) |

|

Market Opportunities |

· Rising demand for custom AI accelerators and specialized chips for inference and training workloads · Growing adoption of chiplet-based and heterogeneous computing architectures · Expansion of edge computing infrastructure requiring specialized low-power chips · Increasing focus on sustainable and energy-efficient data center chip designs |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Data Center Chip Market Trends

Trend: Shift Toward Heterogeneous and Specialized Computing

Modern data centers are undergoing an architectural transformation driven by a convergence of compute, memory, and accelerator technologies. Increasingly heterogeneous compute environments demand specialized silicon to support AI workloads, large-scale analytics, and real-time streaming applications. The proliferation of domain-specific accelerators has redirected R&D investment away from general-purpose chips toward optimized solutions for machine learning inference and training. Chiplet modularity and advanced interconnects are enabling tailored performance-density trade-offs, influencing server form factors and deployment models. The surging requirement for energy efficiency and performance has led to the re-emergence of application-specific integrated circuits (ASICs), which serve only one application. This shift toward specialization is compelling systems architects to rethink integration patterns and thermal envelopes as accelerators introduce distinct power and cooling profiles.

Data Center Chip Market Dynamics

Key Market Driver: Surging Demand for AI and Machine Learning Workloads

The primary driver of the data center chip market is the explosive growth in artificial intelligence and machine learning applications across industries. Businesses leveraging AI and ML technologies require advanced, high-performance chips capable of managing extensive data workloads. The trend of migrating IT infrastructure to cloud-based solutions is compelling organizations to seek data center chips that can support the high-performance computing and processing needs of these applications. Global data center processor market is projected to grow from $147 billion in 2024 to $372 billion by 2030, reflecting the rapid expansion of generative AI. Hyperscalers like Amazon Web Services, Google Cloud, and Microsoft Azure continue to expand their global data center footprints, driving requirement for advanced CPUs, GPUs, and AI accelerators. Data center semiconductor revenue totaled $112 billion in 2024, up from $64.8 billion in 2023.

Key Restraint/Challenge: Supply Chain Constraints and Geopolitical Tensions

A significant challenge facing the data center chip market is the persistent supply chain disruptions and geopolitical trade constraints affecting semiconductor availability. Tariff adjustments and trade policy decisions have tangible ripple effects across design choices, sourcing strategies, and supplier relationships within the semiconductor value chain. The soaring demand for memory chips driven by artificial intelligence is leading to significant shortages that are affecting various industries, including automotive and smartphone production. Chipmakers are switching away from consumer-grade memory to the more intensive version used in AI infrastructure, with every high-end chip displacing more than one regular memory and storage chip. When duties or export controls alter the relative cost of imported components, procurement teams reassess vendor selection, negotiate longer-term contracts, or accelerate nearshoring initiatives to preserve margins and continuity. The high design costs associated with advanced chip development further compound these challenges, particularly for smaller players.

Key Market Opportunity: Custom AI Accelerators and Specialized Chips

The rising demand for custom AI accelerators and specialized chips presents a significant growth opportunity in the data center chip market. As hyperscalers and cloud providers increasingly design their own silicon optimized for specific workloads, the market for custom ASICs and domain-specific accelerators is expanding rapidly. Marvell and its larger rival Broadcom help cloud companies design custom chips tuned to their AI data center needs, a work that has grown into substantial business for them. Broadcom has said that XPU demand is booming, with purchase orders worth $6 billion from two customers. Marvell expects its custom chip revenues to grow by 20% year-on-year in fiscal year 2027, with a target of $10 billion by FY29. Open architectures and emerging instruction set paradigms are creating a more modular ecosystem in which software portability and hardware abstraction layers play decisive roles in adoption. These trends are creating new avenues for innovation, partnerships, and market entry for both established players and emerging semiconductor companies.

Data Center Chip Market Scope

The data center chip market is segmented on the basis of chip type, application, data center size, and end user.

-

By Chip Type

On the basis of chip type, the Data Center Chip Market is segmented into central processing units (CPUs), graphics processing units (GPUs), application-specific integrated circuits (ASICs), field-programmable gate arrays (FPGAs), memory chips and networking chips. The GPU segment led the market in 2025, driven by widespread adoption in AI training, deep learning, and high-performance computing applications. The increasing integration of GPU and FPGA technologies into data center frameworks has revolutionized performance efficiency, allowing for higher throughput and reduced latency in data-heavy operations. The ASICs segment is projected to register the fastest growth from 2026 to 2033, reflecting surging demand for custom silicon optimized for specific AI inference and training workloads. Memory chips, including DRAM and NAND, continue to hold significant market share, driven by growing data storage requirements and the need for high-bandwidth memory in AI applications.

-

By Application

On the basis of application, the Data Center Chip Market is segmented into artificial intelligence & machine learning, cloud computing, big data analytics, high-performance computing, edge computing and others. The AI & Machine Learning segment dominated the market in 2025, supported by rapid AI adoption across industries and massive hyperscaler investments in AI infrastructure. Cloud computing continues to drive substantial demand, as organizations increasingly migrate IT infrastructure to cloud-based solutions. Edge computing represents a fast-growing segment, driven by the deployment of 5G infrastructure and the need for low-latency processing at the network edge.

-

By Data Center Size

On the basis of data center size, the Data Center Chip Market is segmented into hyperscale data centers, large data centers and small & medium data centers. Hyperscale data centers dominated the market in 2025, driven by continued expansion of major cloud service providers including Amazon Web Services, Google Cloud, and Microsoft Azure. These facilities require massive quantities of advanced chips to support their extensive computing and storage infrastructure. Large data centers represent a significant and growing market segment, while small and medium data centers are increasingly adopting advanced chips to support specialized workloads and edge computing applications.

-

By End User

On the basis of end user, the Data Center Chip Market is segmented into IT & telecommunications, BFSI, healthcare, government & defense, retail & e-commerce, manufacturing, media & entertainment and others. The IT & Telecommunications segment dominates the market, driven by extensive cloud service provider and telecom infrastructure investments. The BFSI sector is experiencing significant growth due to increasing adoption of AI-driven analytics, fraud detection, and high-frequency trading applications. Healthcare is emerging as a fast-growing segment, supported by rising adoption of AI-driven diagnostics, electronic health records, telemedicine, and digital health services.

Data Center Chip Market Regional Analysis

Asia-Pacific Data Center Chip Market Insight

Asia-Pacific emerged as the dominant regional market for data center chips in 2025, driven by rapid cloud infrastructure expansion, substantial government investments in digital initiatives, and the presence of major hyperscalers such as Alibaba Cloud, Tencent, and Huawei. China's East Data, West Compute initiative aims to balance data processing capabilities across the country, promoting the development of data centers in less-developed western regions. Such initiatives underscore Asia-Pacific's strategic approach to becoming a global leader in data center infrastructure and chip technology. Countries including China, India, Japan, South Korea, and Singapore are witnessing significant investments in data center infrastructure, driving demand for advanced chip solutions across the region.

North America Data Center Chip Market Insight

North America is expected to be the fastest-growing region in the data center chip market, fueled by aggressive AI infrastructure spending, strong presence of leading semiconductor vendors including NVIDIA, AMD, and Intel, and continued hyperscaler investments across the United States. The U.S. data center chips market is estimated at $25.9 billion in 2025, with the country maintaining its leadership position in semiconductor innovation and data center infrastructure. The region's mature cloud ecosystem, robust venture capital funding for AI startups, and favorable regulatory environment for technology innovation are further accelerating market growth. The Data Center IT semiconductor and component market is on track for triple-digit growth in 2026, driven by elevated DRAM pricing, continued hyperscaler AI investments, and growing adoption of AI-related infrastructure components.

Europe Data Center Chip Market Insight

Europe represents a mature and strategically important market for data center chips, supported by strong regulatory frameworks governing data privacy, increasing cloud adoption across industries, and significant investments in digital infrastructure. The region benefits from the presence of major technology companies, established semiconductor research centers, and a strong focus on innovation and sustainability. Continuous investments in sovereign cloud initiatives and AI research, along with growing demand for energy-efficient computing solutions, are driving market growth across Western and Eastern European countries.

Data Center Chip Market Share

The Data Center Chip industry is primarily led by well-established companies, including:

- NVIDIA Corporation (USA)

- Advanced Micro Devices Inc. (USA)

- Intel Corporation (USA)

- Broadcom Inc. (USA)

- Qualcomm Incorporated (USA)

- Samsung Electronics Co. Ltd. (South Korea)

- SK Hynix Inc. (South Korea)

- Micron Technology Inc. (USA)

- Taiwan Semiconductor Manufacturing Company (Taiwan)

- Arm Holdings (UK)

- Huawei Technologies Co. Ltd. (China)

- Alibaba Group (China)

- Tencent Holdings (China)

- Amazon Web Services (USA)

- Google (USA)

- Microsoft Corporation (USA)

- Marvell Technology Inc. (USA)

- Xilinx Inc. (USA)

- MediaTek Inc. (Taiwan)

Latest Developments in Data Center Chip Market

- In June 2026, Qualcomm forecast $15 billion in data center chip sales by 2029, unveiling new processors specifically designed for AI data centers. The company announced that Microsoft and Meta Platforms will use its new AI chips, and that it will make custom chips for two other unnamed hyperscalers. Qualcomm's data center chief said the company has won two major hyperscaler customers for custom chips, with revenue starting before the end of the calendar year. The company also announced a $4 billion all-stock deal for AI software startup Modular, positioning itself against NVIDIA's proprietary CUDA software.

- In June 2026, the Data Center IT semiconductor and component market demonstrated 116% revenue growth in the first quarter, with the segment on track for triple-digit growth for the full year, driven by elevated DRAM pricing and continued hyperscaler AI investments. The total computing power of AI chips is doubling roughly every 7 months, with shortages for non-AI chips growing exponentially.

- In June 2026, Broadcom reported that XPU (custom AI accelerator) demand is booming, with purchase orders worth $6 billion from two customers. Marvell expects its custom chip revenues to grow by 20% year-on-year in fiscal year 2027, with a target of $10 billion by FY29, as cloud companies construct data centers and build in-house processors.

- In June 2026, global data center AI server compute ASIC shipments are projected to cross the 15-million mark in 2028, surpassing data center GPU shipments, indicating a significant shift toward custom silicon for AI workloads.

- In January 2026, AMD CEO Lisa Su showcased the company's advanced MI455 AI processors at the CES trade show in Las Vegas, which are components in data center server racks being sold to firms including ChatGPT-maker OpenAI. The company also announced that Oracle will put 50,000 of AMD's semiconductors in data center computers starting in the third quarter of 2026.

- In November 2025, Arm Holdings announced plans to start incorporating NVIDIA's NVLink technology into chip designs for AI data centers, tightening the relationship between two influential semiconductor companies. Arm will add the interface to its Neoverse platform, enabling seamless integration of third-party chips into NVIDIA GPU-based data centers.

- In October 2025, Qualcomm unveiled its AI200 chip to rival NVIDIA in the AI accelerator market, with the first customer being Saudi Arabia's AI startup Humain, which plans to deploy 200 megawatts of computing based on the new chips starting in 2026. The AI200 will be offered as a standalone component, add-in cards, or as part of a full rack of servers.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Data Center Chip Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Data Center Chip Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Data Center Chip Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.