Global Dc Charging Market

Market Size in USD Billion

USD

20.90 Billion

USD

64.38 Billion

2025

2033

USD

20.90 Billion

USD

64.38 Billion

2025

2033

| 2026 - 2033 | |

| USD 20.90 Billion | |

| USD 64.38 Billion | |

| % | |

|

DC Charging Market Overview

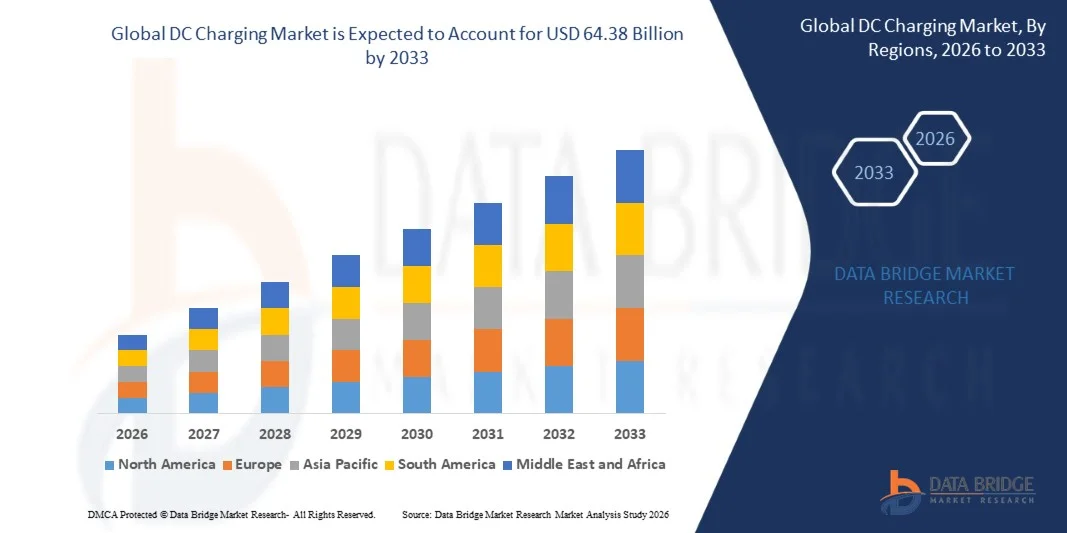

As per Data Bridge Market Research Analysis, the DC Charging Market was valued at USD 20.90 billion in 2025 and is projected to reach USD 64.38 billion by 2033, growing at a CAGR of 15.10% from 2026 to 2033. Direct current (DC) charging technology enables high-power external conversion and direct battery charging, allowing electric vehicles to achieve significant range increases in a short period. As battery capacities grow and vehicle use increases, especially in commercial and highway scenarios, higher power transfer capability becomes essential to cut charging times and keep vehicles available. The market is undergoing rapid expansion, driven by the need to eliminate range anxiety and support long-distance EV travel.

DC chargers allow direct high-voltage power delivery to the battery, bypassing onboard charger restrictions, which enables much faster charging rates and supports continuous vehicle operation. Macro tailwinds contributing to this optimistic outlook include stringent emission regulations, substantial public and private investments in charging infrastructure development, and technological advancements enhancing charger efficiency and interoperability.

Market Size & Forecast

- Global Market Value (2025): USD 20.90 Billion

- Expected Market Value (2033): USD 64.38 Billion

- Forecast CAGR (2026–2033): 15.10%

- Leading Region in 2025: Asia-Pacific (China)

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- China dominates the DC Charging Market, driven by aggressive government policies, massive infrastructure investments, and the world's largest EV fleet.

- Ultra-fast charging is the fastest-growing segment, reflecting the growing demand for high-power charging solutions that minimize downtime.

- Megawatt charging systems are gaining traction, driven by the electrification of heavy-duty commercial vehicles, including trucks and buses.

- Commercial charging is expected to account for the largest share of the application segment during the forecast period, as fleet operators and businesses increasingly adopt DC fast charging infrastructure.

- The GB/T Fast connector type is expected to witness strong growth, driven by the rapid expansion of charging infrastructure in China.

- North America and Europe are leading markets due to favorable government policies and high EV adoption rates, with significant investments in ultra-fast charging networks.

- Asia-Pacific shows strong growth potential due to increasing urbanization, improving charging infrastructure, and the presence of major EV manufacturers.

- Bidirectional charging and vehicle-to-grid capabilities are starting to influence system design, procurement strategies, and long-term infrastructure planning.

- Charging-as-a-Service models are gaining traction, shifting revenue toward recurring, software-enabled streams.

Report Scope and DC Charging Market Segmentation

|

Attributes |

DC Charging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Tesla, Inc. (U.S.) · ABB Ltd. (Switzerland) · Siemens AG (Germany) · BYD Company Ltd. (China) · Delta Electronics, Inc. (Taiwan) · ChargePoint Holdings, Inc. (U.S.) · Blink Charging Co. (U.S.) · Schneider Electric SE (France) · Robert Bosch GmbH (Germany) · State Grid Corporation of China (China) · Allego N.V. (Netherlands) · InstaVolt Ltd. (UK) · Powerdot S.A. (Portugal) · SparkCharge Inc. (U.S.) · Noodoe Corporation (Taiwan) |

|

Market Opportunities |

· Expansion of ultra-fast and megawatt charging networks for long-haul electric trucks and commercial fleets · Integration of bidirectional charging and vehicle-to-grid (V2G) technologies · Growing demand for Charging-as-a-Service (CaaS) and software-enabled revenue models · Standardization of charging protocols and interoperability across regions · Deployment of high-power charging infrastructure in emerging Asia-Pacific markets |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

DC Charging Market Trends

Trend: Rapid Deployment of Ultra-Fast and Megawatt Charging Infrastructure

The growing deployment of ultra-fast DC chargers and megawatt charging systems is increasing demand for higher power density architectures, better thermal management, and modular power stack designs. This trend is driven by advances in high-voltage vehicle platforms, improved efficiency of power semiconductors, and increasing needs for high-throughput charging infrastructure. Commercial vehicle electrification, particularly for long-haul trucks and buses, is a key driver of megawatt charging development. The ultra-fast charging and megawatt charging segments are expected to record robust growth during the forecast period, reflecting the growing demand for high-power charging solutions.

DC Charging Market Dynamics

Key Market Driver: Escalating Global EV Sales and Infrastructure Demand

The primary driver of the DC charging market is the escalating global sales of electric vehicles, necessitating a widespread and efficient charging ecosystem. The rapid evolution within the electric vehicle market, coupled with increasing consumer demand for faster charging solutions, is a fundamental catalyst. Governments worldwide are implementing aggressive policies and incentives to boost EV adoption and expand electric vehicle charging infrastructure, including subsidies for charger installations and mandates for new buildings to include charging points. This proactive regulatory environment significantly de-risks investment in DC charging networks.

Key Restraint/Challenge: Grid Constraints and Infrastructure Costs

A significant challenge facing the DC charging market is the grid constraints and high infrastructure costs associated with deploying ultra-fast and megawatt charging stations. The growing deployment of high-power DC chargers places substantial demands on electrical grids, requiring upgrades to transformers, substations, and distribution networks. The integration of renewable energy sources and energy storage systems is essential to mitigate grid impact and ensure reliable operation. Additionally, the high capital expenditure for ultra-fast charging equipment and installation poses a barrier to entry for smaller operators and limits deployment in rural and remote areas.

Key Market Opportunity: Commercial Fleet Electrification and Megawatt Charging

The electrification of commercial vehicle fleets presents a significant growth opportunity for the DC charging market. Megawatt charging systems, designed for heavy-duty trucks and buses, are projected to grow at a strong CAGR during the forecast period. Fleet operators are increasingly adopting DC fast charging infrastructure to reduce operational costs, meet sustainability targets, and comply with emissions regulations. The development of dedicated charging hubs for commercial fleets, along with government incentives for fleet electrification, is expected to drive significant investment in high-power DC charging infrastructure.

DC Charging Market Scope

The DC charging market is segmented based on charging type, power output, connector type, application, and end user.

- By Charging Type

On the basis of charging type, the DC Charging Market is segmented into slow DC charging, fast DC charging and ultra-fast DC charging. The ultra-fast DC charging segment is projected to record the highest CAGR during the forecast period, driven by the growing demand for rapid charging solutions that minimize downtime for EV owners and fleet operators. Ultra-fast chargers, typically rated above 150 kW, are increasingly deployed along highways and at commercial charging hubs to support long-distance travel. The fast DC charging segment (50–150 kW) continues to hold significant market share, serving both public and commercial applications. Advances in high-voltage vehicle platforms and power semiconductor efficiency are enabling higher-capacity charging stations that meet the evolving demands of electric mobility. The deployment of ultra-fast chargers is also supported by government incentives and the need to reduce range anxiety among EV users. As battery technology improves and vehicles adopt higher voltage architectures, the demand for ultra-fast charging solutions is expected to accelerate further.

- By Power Output

On the basis of power output, the DC Charging Market is segmented into below 50 kW, 50–150 kW and above 150 kW. The above 150 kW segment is expected to witness the fastest growth, driven by the deployment of ultra-fast and megawatt charging systems for passenger EVs and commercial vehicles. The 50–150 kW segment remains the dominant power range for public charging stations, offering a balance between charging speed and infrastructure cost. The below 50 kW segment primarily serves residential and workplace charging applications, where overnight charging is sufficient. The growth of the above 150 kW segment is supported by the increasing availability of EVs with 800V battery architectures, which enable faster charging speeds. Fleet operators and commercial charging networks are investing in higher-power chargers to reduce vehicle downtime and improve operational efficiency.

- By Connector Type

On the basis of connector type, the DC Charging Market is segmented into CCS, CHAdeMO, GB/T, NACS and others. CCS (Combined Charging System) is the dominant connector standard in Europe and North America, offering compatibility across a wide range of EV models. GB/T is the standard connector type in China and is expected to be the fastest-growing segment. NACS (North American Charging Standard), adopted by Tesla and increasingly by other automakers, is gaining traction in North America. CHAdeMO remains relevant in Japan and for certain commercial applications, though its market share is declining. The evolution of connector standards is reshaping the competitive landscape, with industry-wide collaboration on open charging protocols expected to accelerate deployment and reduce fragmentation. The adoption of NACS by major automakers is expected to drive further standardization in North America.

- By Application

On the basis of application, the DC Charging Market is segmented into public charging stations, commercial charging, fleet charging and residential charging. Commercial charging is expected to account for the largest share of the application segment during the forecast period, driven by the rapid expansion of charging networks at retail locations, workplace parking, and highway rest stops. Public charging stations represent the most visible segment, with governments and private operators investing heavily in accessible charging infrastructure. Fleet charging is the fastest-growing application, driven by the electrification of commercial vehicle fleets, including delivery vans, trucks, and buses. The growth of fleet charging is supported by the increasing adoption of electric buses and trucks in urban logistics and public transportation. Residential charging, while currently limited to slow charging applications, is expected to grow as home charging solutions become more sophisticated.

- By End User

On the basis of end user, the DC Charging Market is segmented into automotive OEMs, charging network operators, commercial fleet operators and residential users. Charging Network Operators represent the largest end-user segment, as they deploy and manage public and commercial charging infrastructure. Automotive OEMs are increasingly investing in proprietary charging networks, such as Tesla Supercharger, to enhance the ownership experience of their EV customers. Commercial Fleet Operators are the fastest-growing segment, driven by the need to electrify their vehicle fleets and reduce operational costs. Residential users represent a growing segment, particularly in markets with high EV adoption rates and government incentives for home charging installation. The expansion of charging networks and the development of innovative business models are expected to drive growth across all end-user segments.

DC Charging Market Regional Analysis

Asia-Pacific DC Charging Market Insight

Asia-Pacific is expected to account for the largest share of the global market, with China holding the dominant position. China's aggressive government policies, massive infrastructure investments, and the world's largest EV fleet are the primary drivers of this dominance. The GB/T Fast connector type is expected to be the fastest-growing segment in the region. Countries including India, Japan, South Korea, and Southeast Asian nations are also witnessing significant investments in DC charging infrastructure, driven by rising EV adoption and government incentives. The Asia-Pacific region is expected to witness the highest growth during the forecast period. The Chinese government's 14th Five-Year Plan prioritizes new energy infrastructure, including EV charging networks, while India's FAME-II scheme supports the deployment of fast-charging stations across major cities and highways. Japan and South Korea are also investing heavily in ultra-fast charging networks to support their domestic EV markets and reduce dependence on fossil fuels.

North America DC Charging Market Insight

North America is expected to account for a significant share of the global market, supported by favorable government policies, high EV adoption rates, and substantial investments in ultra-fast charging networks. The United States is at the forefront of DC charging development, with the adoption of NACS (North American Charging Standard) gaining momentum. Key players such as Tesla, ChargePoint, and Blink Charging are expanding their networks across the region. The U.S. government's infrastructure investments and incentives for EV charging deployment are expected to accelerate market growth. The National Electric Vehicle Infrastructure (NEVI) Formula Program is providing significant funding for DC fast charging stations along major highway corridors, supporting the deployment of ultra-fast charging infrastructure. Canada is also investing in charging infrastructure through its Zero Emission Vehicle Infrastructure Program, further strengthening the North American market.

Europe DC Charging Market Insight

Europe represents a mature and technologically advanced market for DC charging, supported by strong regulatory frameworks, significant investments in charging infrastructure, and high EV adoption rates. The European Union's ambitious targets for EV adoption and the deployment of alternative fuel infrastructure are driving market growth. Key players such as ABB, Siemens, and Allego are strengthening their presence in the region. The integration of smart charging technologies, renewable energy sources, and grid management systems is shaping the European DC charging landscape. The EU's Alternative Fuels Infrastructure Regulation (AFIR) mandates the deployment of fast-charging stations along major transport corridors, ensuring comprehensive coverage across member states. Germany, France, the U.K., and the Netherlands are leading the charge with substantial investments in ultra-fast charging networks and innovative business models such as Charging-as-a-Service.

Latin America DC Charging Market Insight

Latin America represents an emerging market for DC charging, with growing demand driven by increasing EV adoption, government incentives, and urbanization. Countries such as Brazil, Mexico, and Argentina are witnessing significant investments in EV charging infrastructure, supported by policies promoting sustainable transportation and reducing emissions. The region's expanding middle class and growing awareness of environmental issues are driving consumer interest in electric vehicles and charging solutions. Brazil is leading the region with its national electric mobility strategy, while Mexico is benefiting from its proximity to the U.S. market and the adoption of similar charging standards. However, market growth is currently constrained by limited consumer awareness, higher vehicle costs compared to traditional internal combustion engine vehicles, and fragmented regulatory frameworks. The development of regional supply chains and partnerships with global charging infrastructure providers is expected to accelerate market growth.

Middle East & Africa DC Charging Market Insight

The Middle East and Africa region represents an emerging market for DC charging infrastructure, with demand primarily concentrated in the GCC countries and South Africa. Governments across the region are increasing investments in electric mobility to reduce carbon emissions and diversify transportation systems. The UAE has established one of the region's most advanced public charging networks, while Saudi Arabia is expanding EV infrastructure through Vision 2030 initiatives and large-scale smart city developments such as NEOM. South Africa is gradually expanding charging infrastructure to support the growing adoption of electric passenger vehicles and commercial fleets. Increasing investments from global charging equipment manufacturers and utility providers are improving infrastructure availability across major urban centers. However, relatively low EV penetration, limited charging density outside metropolitan areas, and high installation costs continue to restrain market growth. Continued policy support, infrastructure partnerships, and growing private sector investment are expected to accelerate DC charging deployment across the region during the forecast period.

DC Charging Market Share

The DC Charging industry is primarily led by well-established companies, including:

- Tesla, Inc. (U.S.)

- ABB Ltd. (Switzerland)

- Siemens AG (Germany)

- BYD Company Ltd. (China)

- Delta Electronics, Inc. (Taiwan)

- ChargePoint Holdings, Inc. (U.S.)

- Blink Charging Co. (U.S.)

- Schneider Electric SE (France)

- Robert Bosch GmbH (Germany)

- State Grid Corporation of China (China)

- Allego N.V. (Netherlands)

- InstaVolt Ltd. (UK)

- Powerdot S.A. (Portugal)

- SparkCharge Inc. (U.S.)

- Noodoe Corporation (Taiwan)

Latest Developments in DC Charging Market

- In January 2026, the California Energy Commission announced $79 million in grant opportunities under the National Electric Vehicle Infrastructure (NEVI) Formula Program to expand EV charging infrastructure along major travel routes. The funding supports the installation of high-powered DC fast chargers along designated Alternative Fuel Corridors. The NEVI program provides $5 billion through FY2026 to build out DC fast charging stations across the U.S..

- In November 2025, ChargePoint Holdings, Inc. announced a new ultra-fast EV charging site in Canton, Michigan, owned and operated by the Dabaja Brothers Development Group, with additional sites planned in Dearborn and Lavonia. Each site will feature ChargePoint Express Plus fast charging stations, with Dabaja Brothers intending to deploy more than 40 charging ports across its locations.

- In October 2025, Tesla reported the addition of over 3,500 net new Supercharging stalls in Q3 2025, marking an 18% increase in network capacity year-over-year. The number of supercharger stations reached 7,753, representing a 16% year-on-year increase, with connectors totaling 73,817. The company also expanded its network to new regions.

- In September 2025, ABB Ltd. launched its Terra 360 modular charger, capable of delivering up to 360 kW of power and providing 100 km of range in less than three minutes. The charger is designed to charge up to four vehicles simultaneously with dynamic power distribution. The launch aligned with ABB's plans to float its EV charging business, which could be valued around $3 billion.

- In June 2025, Delta Electronics, Inc. showcased an ultra-fast 350 kW DC charger at an exhibition, enabling EV owners to travel between Taipei and Kaohsiung in just 20 to 30 minutes. The charger features a maximum charging current of up to 540 amps and dual-output charging connectors. Delta also demonstrated its 50 kW DC fast charger designed for densely populated urban environments.

- In March 2025, BYD Company Ltd. officially unveiled its Super e-Platform on March 17, supporting a 1,000V battery system and 1,000A peak current, delivering megawatt-level charging (1,000 kW). The platform enables a five-minute flash charge for 400 kilometers of driving range, effectively matching the time it takes to refuel a traditional gasoline car. BYD also developed Megawatt Flash Charging stations with a maximum output of 1,360 kW.

- In February 2025, Siemens AG announced it had been awarded a five-year contract by Aral pulse to deploy Electrification X for its Aral e-mobility brand. The cloud-based system will centrally operate, optimize, and secure Aral's ultra-fast EV charging stations across Germany. The partnership aims to make charging as quick as refueling with conventional fuels.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.