Global Ddos Protection And Mitigation Security Market

Market Size in USD Billion

USD

4.99 Billion

USD

13.45 Billion

2024

2032

USD

4.99 Billion

USD

13.45 Billion

2024

2032

| 2025 - 2032 | |

| USD 4.99 Billion | |

| USD 13.45 Billion | |

| % | |

|

DDoS Protection and Mitigation Security Market Size

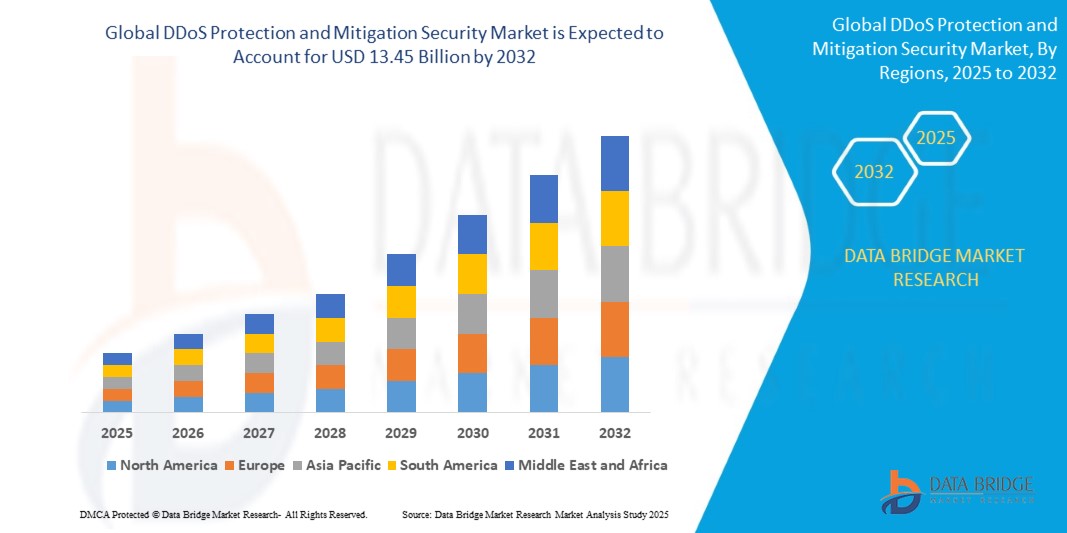

- Global DDOS protection and mitigation security market size was valued at USD 4.99 Billion in 2024 and is projected to reach USD 13.45 Billion by 2032, with a CAGR of 13.20% during the forecast period of 2025 to 2032.

- The DDOS protection and mitigation security market is experiencing significant growth due to the increasing frequency and sophistication of cyberattacks, especially Distributed Denial of Service (DDoS) attacks

- Drivers include the rising adoption of cloud-based services, growing digital transformation across industries, and the critical need for robust network security infrastructure. Restraints are primarily related to the high costs of advanced DDoS protection solutions and the lack of awareness among SMEs regarding cybersecurity risks

DDoS Protection and Mitigation Security Market Analysis

- The DDoS protection and mitigation security market is witnessing rapid expansion driven by the rising frequency and complexity of cyberattacks, particularly Distributed Denial of Service (DDoS) attacks.

- The increasing frequency of cyberattacks, particularly Distributed Denial of Service (DDoS) attacks, poses a significant threat to organizations globally, highlighting the urgent need for effective cybersecurity measures

- As businesses continue to digitize their operations and expand their online presence, they become more vulnerable to malicious actors who exploit these digital channels to launch attacks

- Cybercriminals are utilizing sophisticated techniques to overwhelm targeted systems with massive traffic, often resulting in downtime, loss of revenue, and damage to brand reputation. Furthermore, the rise of automated attack tools and the proliferation of IoT devices have made it easier for attackers to coordinate large-scale DDoS assaults, leading to more frequent and severe incidents

- North America dominated the DDoS protection and mitigation security market with the largest revenue share of 39.6% in 2024, driven by the rising frequency of large-scale cyberattacks and the strong presence of leading cybersecurity vendors

- The Asia-Pacific market is forecasted to grow at the fastest CAGR of 9.98% from 2025 to 2032, driven by surging internet traffic, the rapid expansion of e-commerce, and escalating cyberattack volumes in China, Japan, and India

- The cloud-based segment dominated the market with the largest revenue share of 48.6% in 2024, driven by the growing adoption of SaaS platforms, scalability benefits, and reduced infrastructure costs

Report Scope and Global DDoS Protection and Mitigation Security Market Segmentation

|

Atrributes |

DDoS Protection and Mitigation Security Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

DDoS Protection and Mitigation Security Market Trends

Growing Number of DDoS Attacks

- The increasing frequency and complexity of Distributed Denial of Service (DDoS) attacks are major factors propelling the growth of the DDoS protection and mitigation security market. Organizations across sectors—including finance, healthcare, e-commerce, and public services—are becoming prime targets for sophisticated, large-scale attacks aimed at disrupting services and overwhelming digital infrastructure

- Modern DDoS attacks often use multi-vector strategies, combining volumetric, protocol, and application-layer attacks to bypass traditional defenses. In addition, the rapid proliferation of Internet of Things (IoT) devices has significantly expanded the attack surface. Many of these devices lack proper security configurations, making them easy targets for botnet recruitment, which amplifies the scale and impact of DDoS campaigns

- As businesses become increasingly dependent on online platforms, even brief service outages can result in substantial financial losses, operational downtime, brand damage, and diminished customer trust. This evolving threat landscape has prompted organizations to invest in advanced DDoS mitigation solutions that offer real-time monitoring, automated response, and adaptive threat intelligence

- In response to these challenges, the market is seeing heightened demand for cloud-based and AI-driven DDoS protection services that offer scalability, speed, and precision—helping organizations ensure business continuity and safeguard critical digital assets

DDoS Protection and Mitigation Security Market Dynamics

Drivers

Growing Adoption of Cloud Services

- The growing adoption of cloud services is significantly reshaping the landscape of IT infrastructure, offering organizations scalable, flexible, and cost-effective solutions for their operational needs. As businesses increasingly migrate their applications and data to the cloud, they benefit from enhanced accessibility and collaboration, enabling remote work and seamless integration across global teams

- However, this shift also exposes organizations to a heightened risk of cyber threats, particularly Distributed Denial of Service (DDoS) attacks, as attackers target cloud-based services to disrupt operations and demand ransom

- The dynamic nature of cloud environments, combined with the reliance on shared resources, can make it challenging to implement robust security measures, thus necessitating advanced DDoS protection solutions

- As a result, service providers and enterprises asuch as are prioritizing the implementation of sophisticated security strategies to safeguard their cloud infrastructure, ensuring uninterrupted service availability and protecting sensitive data from potential breaches

- This drives the demand for DDoS mitigation services and encourages the development of innovative solutions tailored to meet the security challenges posed by cloud computing

Restraints/Challenges

High Costs of Advanced Solutions

- The high costs of advanced DDoS protection solutions present a significant barrier for many organizations, particularly small and medium-sized enterprises (SMEs) that may have limited budgets for cybersecurity investments

- Implementing sophisticated DDoS mitigation technologies often requires substantial financial resources for both initial setup and ongoing maintenance, including hardware, software, and skilled personnel to manage the systems

- Moreover, as cyber threats become more complex, the need for continuous upgrades and enhancements to existing security protocols further escalates costs. This financial burden can lead organizations to delay or forgo essential DDoS protection measures, leaving them vulnerable to potential attacks that could result in costly downtime, data breaches, and damage to their reputation

- In addition, the lack of awareness about the potential impact of DDoS attacks can hinder decision-making, causing businesses to underestimate the necessity of investing in advanced security solutions

- Consequently, the high costs associated with DDoS protection create a challenging landscape where many organizations struggle to strike a balance between securing their digital assets and managing their financial resources effectively

DDoS Protection and Mitigation Security Market Scope

The market is segmented on the basis of deployment mode, component, organization size, application and industry.

• By Deployment Mode

On the basis of deployment mode, the market is segmented into on-premise, cloud-based, and hybrid. The cloud-based segment dominated the market with the largest revenue share of 48.6% in 2024, driven by the growing adoption of SaaS platforms, scalability benefits, and reduced infrastructure costs. Cloud-based solutions are widely favored by enterprises seeking real-time updates, remote accessibility, and faster deployment models without heavy upfront investment. Integration with AI-driven threat detection further boosts its popularity.

The hybrid segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by organizations seeking a balance between security, flexibility, and compliance. Hybrid deployment offers businesses the advantage of retaining sensitive data on-premise while leveraging cloud scalability for analytics and automation. Increasing data privacy regulations and rising multi-cloud strategies are further supporting hybrid adoption across BFSI, healthcare, and government institutions.

• By Component

On the basis of component, the market is segmented into hardware, software, and services. The software segment accounted for the largest revenue share of 42.3% in 2024, driven by increasing demand for security platforms providing advanced features such as real-time monitoring, AI-based threat detection, and automated response. Continuous updates and the integration of machine learning capabilities ensure high adoption among enterprises.

The services segment is expected to witness the fastest CAGR from 2025 to 2032, as businesses increasingly rely on consulting, training, and managed services to handle complex security requirements. The surge in managed security services (MSS) is particularly strong due to the shortage of skilled cybersecurity professionals and the need for 24/7 monitoring. Hardware demand remains steady, particularly for firewalls and intrusion detection systems, but the shift toward software-defined and service-based models will continue reshaping this segment’s growth trajectory.

• By Organization Size

On the basis of organization size, the market is segmented into small and medium-sized enterprises (SMEs) and large enterprises. The large enterprises segment dominated the market with a revenue share of 61.4% in 2024, driven by their higher IT budgets, complex infrastructure, and greater exposure to cyber threats. Large corporations invest heavily in comprehensive, layered security solutions, including AI-powered threat detection and integrated risk management platforms.

The SMEs segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by growing awareness of cyber risks and the availability of affordable cloud-based security solutions. SMEs are rapidly adopting endpoint and application security solutions to protect sensitive business and customer data, especially in the e-commerce and financial services sectors. Government initiatives to strengthen cybersecurity among SMEs further encourage adoption, making this segment a critical growth driver in the forecast period.

• By Application

On the basis of application, the market is segmented into network security, application security, database security, and endpoint security. The network security segment held the largest revenue share of 38.7% in 2024, driven by the need to safeguard enterprise networks against ransomware, phishing, and DDoS attacks. Its dominance is further reinforced by widespread adoption of next-generation firewalls, VPNs, and intrusion detection systems. The endpoint security segment is anticipated to witness the fastest CAGR from 2025 to 2032, as remote work expansion and BYOD (Bring Your Own Device) policies expose vulnerabilities across laptops, mobile devices, and IoT endpoints. Endpoint security adoption is growing rapidly due to the integration of AI-driven monitoring, EDR (Endpoint Detection & Response), and cloud-managed solutions. Application and database security segments are also gaining momentum as businesses prioritize secure coding practices and database encryption, particularly in BFSI and healthcare sectors.

• By Industry

On the basis of industry, the market is segmented into BFSI (Banking, Financial Services, and Insurance), IT and telecom, healthcare, retail, government and defense, media and entertainment, and others. The BFSI segment dominated the market with a revenue share of 29.8% in 2024, owing to the sector’s heavy dependence on digital transactions, sensitive data protection, and compliance with strict regulatory frameworks. Financial institutions lead investments in advanced authentication, fraud detection, and encryption technologies.

The healthcare segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by the digitization of medical records, telemedicine expansion, and the growing need to protect patient data against cyberattacks. IT and telecom continue to drive steady demand with increasing cloud adoption and 5G rollouts, while government and defense focus on securing national critical infrastructure. Retail and media sectors are also emerging adopters due to rising e-commerce penetration and digital content distribution.

DDoS Protection and Mitigation Security Market Regional Analysis

- North America dominated the DDoS protection and mitigation security market with the largest revenue share of 39.6% in 2024, driven by the rising frequency of large-scale cyberattacks and the strong presence of leading cybersecurity vendors

- Enterprises in the region increasingly prioritize advanced defense mechanisms to safeguard mission-critical applications, financial transactions, and customer data

- Government regulations, high internet penetration, and significant investment in cloud security further accelerate adoption, making DDoS protection a critical component of North America’s cybersecurity strategy

U.S. DDoS Protection and Mitigation Security Market Insight

The U.S. market captured the largest revenue share of 80.2% in 2024 within North America, fueled by frequent targeted cyberattacks on BFSI, e-commerce, and government sectors. Organizations are rapidly deploying AI-driven and cloud-based DDoS mitigation services to combat evolving multi-vector threats. Growing reliance on cloud infrastructure, combined with the adoption of IoT and 5G networks, is heightening the risk of attacks, driving continuous investment in advanced solutions. Strong regulatory mandates and partnerships between technology providers and federal agencies further strengthen market growth.

Europe DDoS Protection and Mitigation Security Market Insight

The Europe market is projected to expand at a notable CAGR throughout the forecast period, driven by stricter cybersecurity regulations such as GDPR and NIS2 directives. Enterprises across industries, including telecom, BFSI, and healthcare, are strengthening defenses to prevent costly downtime and data breaches. Growing cloud adoption and digital transformation initiatives are fostering increased investment in mitigation solutions. Demand for scalable, automated defenses is particularly strong, with adoption expanding across both SMEs and large enterprises in the region.

U.K. DDoS Protection and Mitigation Security Market Insight

The U.K. market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by the country’s advanced digital economy and rising cybercrime incidents. Businesses are increasingly adopting managed security services and cloud-based protection to safeguard against volumetric and application-layer attacks. The push for digital resilience in financial services, retail, and critical infrastructure is boosting market demand. In addition, government-backed initiatives promoting cybersecurity readiness are further encouraging adoption across enterprises of all sizes.

Germany DDoS Protection and Mitigation Security Market Insight

The Germany market is expected to expand at a considerable CAGR during the forecast period, supported by the nation’s strong emphasis on data security, privacy, and compliance. Rapid digitalization across manufacturing, automotive, and enterprise sectors makes Germany a prime target for sophisticated DDoS attacks. German organizations are investing in hybrid security architectures combining on-premise appliances with cloud-based scrubbing centers. The country’s focus on Industry 4.0, coupled with rising threats against critical infrastructure, positions DDoS protection as a strategic priority.

Asia-Pacific DDoS Protection and Mitigation Security Market Insight

The Asia-Pacific market is forecasted to grow at the fastest CAGR of 9.98% from 2025 to 2032, driven by surging internet traffic, the rapid expansion of e-commerce, and escalating cyberattack volumes in China, Japan, and India. Digital transformation initiatives and government policies to enhance cybersecurity frameworks further support adoption. APAC’s role as a global hub for online gaming, fintech, and cloud services makes the region highly vulnerable to large-scale attacks, propelling strong demand for scalable, cost-effective solutions.

Japan DDoS Protection and Mitigation Security Market Insight

The Japan market is gaining momentum due to its advanced digital ecosystem and high reliance on connected infrastructure. The rapid adoption of 5G, IoT, and smart city projects is exposing networks to heightened DDoS risks. Enterprises are increasingly turning to cloud-based and AI-driven solutions for proactive threat detection and rapid mitigation. Japan’s regulatory focus on safeguarding critical sectors, including finance and energy, further drives adoption. In addition, the need for secure, low-latency solutions aligns with Japan’s technology-driven market landscape.

China DDoS Protection and Mitigation Security Market Insight

The China market accounted for the largest revenue share in Asia-Pacific in 2024, fueled by the country’s expanding digital economy, massive internet user base, and growing frequency of high-profile cyberattacks. China’s e-commerce, online gaming, and financial sectors are particularly vulnerable, creating strong demand for advanced protection systems. The government’s emphasis on cybersecurity sovereignty and the presence of numerous domestic vendors are also propelling adoption. Moreover, the rise of cloud infrastructure providers and the country’s ongoing smart city initiatives are accelerating the expansion of DDoS mitigation solutions.

DDoS Protection and Mitigation Security Market Share

DDoS Protection and Mitigation Security Market Leaders Operating in the Market Are:

- Akamai Technologies (U.S.)

- Cloudflare, Inc. (U.S.)

- NETSCOUT Systems, Inc. (U.S.)

- Radware (Israel)

- Imperva (U.S.)

- Neustar, Inc. (U.S.)

- Fortinet, Inc. (U.S.)

- Corero Network Security, Inc. (U.S.)

- F5 Networks, Inc. (U.S.)

- Link11 GmbH (Germany)

Latest Developments in Global DDoS Protection and Mitigation Security Market

- In June 2023, Akamai Technologies introduced Enterprise Threat Protector, a service designed to strengthen DDoS protection for enterprises moving toward cloud-based environments. The solution leverages advanced threat intelligence and analytics to help organizations detect and counter emerging DDoS risks more effectively. This launch highlights Akamai’s focus on empowering enterprises with proactive and cloud-ready security solutions

- In May 2023, Nexusguard opened a DDoS scrubbing center in Sao Paulo, Brazil, aimed at safeguarding local operators and enterprises from cyberattacks. Integrated with Nexusguard’s Bastions solution, the center offers real-time detection and mitigation of threats. This initiative emphasizes Nexusguard’s commitment to enhancing cybersecurity resilience across Latin America

- In April 2023, Cloudflare, Inc. rolled out its DDoS Protection and Mitigation Suite, embedding advanced machine learning capabilities to identify and neutralize complex attacks in real time. The suite offers comprehensive protection against both volumetric and application-layer threats. This move reinforces Cloudflare’s role as a global leader in intelligent, adaptive DDoS defense

- In March 2023, Radware launched a cloud application security center in Israel as part of its broader strategy to scale cloud-based offerings. The center represents a major step in expanding Radware’s cloud security portfolio while meeting growing customer demand for agile and advanced protections. This initiative underscores Radware’s dedication to innovation and global market growth in cybersecurity

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Ddos Protection And Mitigation Security Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Ddos Protection And Mitigation Security Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Ddos Protection And Mitigation Security Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.