Global Defense Cyber Security Market

Market Size in USD Billion

USD

33.53 Billion

USD

77.82 Billion

2025

2033

USD

33.53 Billion

USD

77.82 Billion

2025

2033

| 2026 - 2033 | |

| USD 33.53 Billion | |

| USD 77.82 Billion | |

| % | |

|

Defense Cyber Security Market Overview

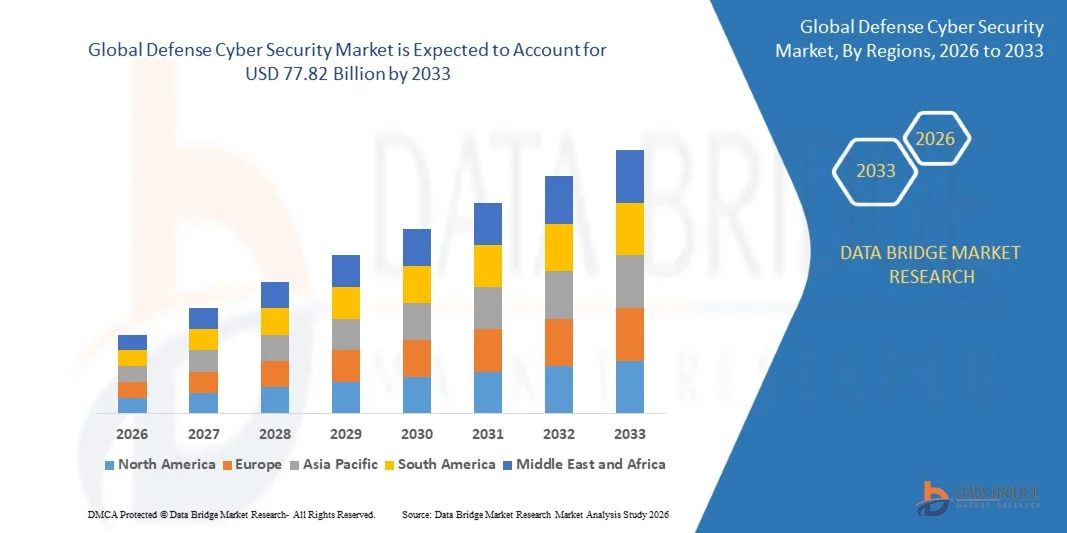

The Defense Cyber Security Market was valued at USD 33.53 billion in 2025 and is projected to reach USD 77.82 billion by 2033, growing at a CAGR of 11.10% from 2026 to 2033. The market is experiencing strong growth driven by rising cyber threats targeting defense infrastructure, increasing investments in military digitalization, and growing adoption of advanced cybersecurity technologies across defense organizations. Expanding use of cloud computing, artificial intelligence, IoT-enabled defense systems, and network-centric warfare is accelerating demand for robust cyber defense solutions worldwide.

The increasing frequency of sophisticated cyberattacks, state-sponsored threats, ransomware incidents, and cyber espionage campaigns is compelling defense agencies and military organizations to strengthen their cybersecurity capabilities. Advanced technologies such as AI-powered threat detection, zero-trust security architectures, endpoint protection, and security information and event management (SIEM) solutions are replacing traditional security approaches by providing real-time threat intelligence, proactive risk mitigation, and resilient protection for critical defense networks, communication systems, and classified military data.

Market Size & Forecast

- Global Market Value (2025): USD 33.53 Billion

- Expected Market Value (2033): USD 77.82 Billion

- Forecast CAGR (2026–2033): 11.10%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America dominated the Defense Cyber Security Market with the largest revenue share of 39.14% in 2025, supported by substantial defense budgets, extensive cybersecurity modernization programs, increasing adoption of zero-trust architecture, and the presence of leading defense cybersecurity vendors across the United States and Canada.

- The on-premises segment dominated the market with a 52.91% share in 2025 due to the defense sector's requirement for complete control over classified military information, mission-critical infrastructure, and national security systems.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 13.9% from 2026 to 2033, fueled by increasing defense modernization initiatives, rising cyber warfare preparedness, growing military digitalization, and expanding cybersecurity investments across China, India, Japan, South Korea, and Australia.

- Cloud security is the fastest-growing security type, projected to register a CAGR of 15.4% during the forecast period, reflecting the increasing adoption of secure defense cloud infrastructure, cloud-native applications, encrypted data storage, and military cloud migration initiatives.

Report Scope and Defense Cyber Security Market Segmentation

|

Attributes |

Defense Cyber Security Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Expansion of Zero Trust Architecture Across Defense Networks · Growing Cybersecurity Investments for Space and Defense Digital Infrastructure · Integration of AI-Driven Threat Detection and Autonomous Cyber Defense |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Defense Cyber Security Market Trends

Trend: Rising Adoption of Zero Trust Architecture and AI-Driven Cyber Defense

The Defense Cyber Security Market is witnessing significant growth as military organizations increasingly strengthen cyber resilience against sophisticated nation-state attacks, ransomware, advanced persistent threats (APTs), and cyber warfare campaigns. The rapid digitalization of defense infrastructure, integration of cloud computing, artificial intelligence, IoT-enabled battlefield systems, and connected command-and-control (C2) platforms have expanded the cyberattack surface across defense ecosystems. Governments worldwide are investing heavily in Zero Trust Architecture (ZTA), AI-powered threat detection, cyber threat intelligence, endpoint protection, and secure military cloud environments to safeguard critical defense assets. According to the Stockholm International Peace Research Institute (SIPRI), global military expenditure surpassed USD 2.7 trillion in 2024, with a growing share allocated toward cyber defense capabilities and digital modernization. Defense agencies are also deploying Security Operations Centers (SOCs), Security Information and Event Management (SIEM), Extended Detection and Response (XDR), and automated incident response platforms to strengthen national cyber resilience and protect mission-critical military networks.

Defense Cyber Security Market Dynamics

Key Market Driver: Increasing Defense Digitalization and Growing Cyber Warfare Threats

The primary driver of the Defense Cyber Security Market is the rapid digital transformation of military operations and the increasing frequency of sophisticated cyberattacks targeting defense infrastructure. Armed forces worldwide are deploying cloud-enabled command systems, satellite communication networks, unmanned aerial vehicles (UAVs), autonomous defense platforms, and AI-powered battlefield management systems that require robust cybersecurity protection. Governments are substantially increasing investments in cyber defense strategies to secure classified military information, weapons systems, intelligence networks, and critical national infrastructure. According to NATO and multiple national defense strategies, cyber has become an operational domain alongside land, sea, air, and space, prompting continuous investment in military cyber capabilities. Increasing geopolitical tensions, ransomware attacks, supply chain compromises, and nation-state cyber espionage campaigns are further accelerating the adoption of network security, endpoint protection, identity & access management, and cloud security solutions across global defense organizations.

Key Restraint/Challenge: Increasing Sophistication of Advanced Persistent Threats (APTs) and Legacy Defense Infrastructure

A major challenge for the Defense Cyber Security Market is the growing sophistication of cyberattacks targeting military networks and the complexity of securing legacy defense infrastructure. Many defense organizations continue to operate aging communication systems, legacy operational technologies, and mission-critical platforms that were not originally designed to withstand modern cyber threats. Integrating advanced cybersecurity technologies with existing defense systems often requires extensive modernization, interoperability testing, and regulatory compliance. Highly sophisticated Advanced Persistent Threats (APTs), supply chain attacks, zero-day vulnerabilities, and AI-assisted cyberattacks continue to challenge defense agencies worldwide. In addition, the shortage of skilled cybersecurity professionals with defense clearance and expertise in military cyber operations increases implementation complexity and operational costs. These factors can delay cybersecurity modernization programs, particularly in developing economies with limited defense budgets.

Key Market Opportunity: AI-Enabled Threat Intelligence and Next-Generation Military Cyber Defense Platforms

The integration of artificial intelligence, machine learning, and predictive analytics into defense cybersecurity platforms presents a significant growth opportunity. AI-powered cyber defense systems can continuously monitor military networks, identify anomalous behavior, detect zero-day attacks, and automate incident response in real time, significantly reducing response times and improving mission readiness. Governments are increasingly investing in cyber threat intelligence platforms, quantum-resistant cryptography, secure defense cloud infrastructure, autonomous Security Operations Centers (SOCs), and Zero Trust Architecture to strengthen national cyber resilience. The growing deployment of military cloud computing, space-based communication systems, connected defense platforms, and AI-enabled battlefield networks is expected to generate substantial demand for advanced defense cybersecurity solutions. Furthermore, increasing collaboration between defense agencies, cybersecurity companies, and technology providers to develop next-generation cyber defense capabilities is creating significant growth opportunities across North America, Europe, Asia-Pacific, and the Middle East throughout the forecast period.

Defense Cyber Security Market Scope

The defense cyber security market is segmented on the basis of security type, deployment mode, and end user.

- By Security Type

On the basis of security type, the Defense Cyber Security Market is segmented into network security, endpoint security, cloud security, application security, data security, identity & access management (IAM), and others. The Network Security segment dominated the market with a 29.84% share in 2025 due to its critical role in protecting military communication networks, classified defense infrastructure, command-and-control systems, and mission-critical operational environments from sophisticated cyber threats. Rising cyber warfare activities, increasing state-sponsored attacks, and growing adoption of secure tactical communication networks have significantly strengthened demand for advanced network security solutions. Defense organizations are investing heavily in next-generation firewalls, intrusion detection and prevention systems (IDS/IPS), secure gateways, and network traffic analytics to safeguard highly sensitive information. Continuous modernization of military communication infrastructure and increasing deployment of software-defined networking technologies further support segment growth. Governments across North America, Europe, and Asia-Pacific continue to prioritize network resilience under national cybersecurity strategies. Growing investments in zero-trust network architectures and AI-powered threat detection platforms are further enhancing protection capabilities. The integration of real-time monitoring, security orchestration, and automated response solutions has strengthened operational readiness against evolving cyber threats. In addition, increasing defense budgets and modernization programs continue to reinforce the dominance of the Network Security segment across global defense organizations.

The Cloud Security segment is expected to witness the fastest CAGR of 14.1% from 2026 to 2033, driven by the increasing migration of defense workloads toward secure government and defense cloud environments. Military organizations are adopting hybrid and sovereign cloud infrastructures to improve operational agility while maintaining stringent security standards. Growing deployment of cloud-based intelligence platforms, battlefield management systems, and secure collaboration environments is accelerating demand for cloud security solutions. AI-driven cloud security monitoring, workload protection, encryption technologies, and cloud access security brokers are becoming increasingly important. Rising investments in defense digital transformation initiatives and multi-cloud architectures are further supporting adoption. Governments are implementing strict compliance frameworks to secure classified cloud environments against cyber espionage and ransomware attacks. The growing adoption of zero-trust cloud security models and continuous authentication is enhancing resilience against sophisticated threats. Cloud-native security platforms also provide scalable protection for globally distributed defense operations. Furthermore, increasing investments in secure cloud infrastructure modernization are expected to accelerate long-term market growth.

- By Deployment Mode

On the basis of deployment mode, the Defense Cyber Security Market is segmented into on-premises, cloud-based, and hybrid. The On-Premises segment dominated the market with a 52.91% share in 2025 due to the defense sector's requirement for complete control over classified military information, mission-critical infrastructure, and national security systems. Most armed forces and defense intelligence agencies continue to rely on highly secure on-premises deployments to comply with national security regulations and minimize exposure to external cyber risks. Dedicated cybersecurity infrastructure enables greater customization, strict access control, and real-time operational monitoring. Defense organizations prefer isolated environments for weapons systems, communication networks, and intelligence databases to reduce attack surfaces. Continuous investment in secure military data centers and classified network environments supports strong adoption. On-premises deployments also provide low-latency performance and operational continuity during disconnected or battlefield operations. Increasing investments in cyber defense modernization and secure infrastructure upgrades further strengthen this segment. Defense contractors and intelligence agencies continue expanding highly protected private environments for sensitive workloads. These factors collectively reinforce the dominant position of the On-Premises deployment segment.

The Hybrid deployment segment is anticipated to register the fastest CAGR of 14.5% from 2026 to 2033, driven by growing demand for flexible cybersecurity architectures that combine secure on-premises infrastructure with trusted cloud environments. Defense organizations are increasingly deploying hybrid models to support secure collaboration, intelligence sharing, and mission planning across multiple locations. Hybrid deployments allow classified information to remain on protected infrastructure while leveraging cloud platforms for analytics, logistics, and operational support. AI-powered monitoring, unified security management, and automated compliance tools are improving visibility across hybrid environments. Increasing adoption of multi-domain military operations and digitally connected defense ecosystems is accelerating implementation. Hybrid security frameworks also improve disaster recovery capabilities and operational resilience. Governments are investing in secure hybrid cloud programs to support modernization initiatives without compromising national security requirements. Continuous advancements in encrypted communications and secure identity management further enhance deployment flexibility. These advantages are expected to drive strong hybrid deployment growth throughout the forecast period.

- By End User

On the basis of end user, the Defense Cyber Security Market is segmented into military & defense forces, defense intelligence agencies, defense contractors & OEMs, homeland security agencies, naval forces, air forces, and others. The Military & Defense Forces segment dominated the market with a 34.62% share in 2025 due to extensive investments in protecting operational technology, command-and-control systems, battlefield communication networks, and classified defense infrastructure from increasingly sophisticated cyberattacks. Modern military operations rely heavily on secure digital communications, satellite networks, and integrated cyber defense capabilities. Governments worldwide continue expanding cyber commands and investing in advanced cybersecurity platforms to safeguard national defense assets. AI-driven threat detection, endpoint protection, network monitoring, and cyber resilience programs are becoming core defense priorities. Continuous modernization of military infrastructure and increasing cyber warfare preparedness further support market leadership. Growing geopolitical tensions and rising frequency of state-sponsored cyberattacks have significantly increased cybersecurity spending across armed forces. Integration of zero-trust security architectures and secure digital identity solutions is improving mission resilience. Military organizations also continue investing in offensive and defensive cyber capabilities to strengthen national security. These factors collectively reinforce the dominant position of the Military & Defense Forces segment.

The Defense Contractors & OEMs segment is projected to witness the fastest CAGR of 13.8% from 2026 to 2033, driven by increasing cybersecurity requirements across defense manufacturing, weapons development, aerospace engineering, and digital defense supply chains. Contractors are adopting advanced cybersecurity solutions to secure intellectual property, production systems, connected manufacturing facilities, and sensitive defense research. Growing regulatory compliance requirements and cybersecurity maturity standards for defense suppliers are accelerating investment. AI-powered threat intelligence, secure DevSecOps platforms, software supply chain security, and continuous vulnerability assessment are becoming critical components of defense production environments. Increasing adoption of cloud engineering, digital twins, and connected manufacturing systems further supports cybersecurity deployment. Governments are strengthening cybersecurity mandates for defense procurement programs and contractor certification. Continuous collaboration between defense ministries and private-sector cybersecurity providers is enhancing protection across defense ecosystems. Investments in secure product development lifecycles and advanced identity management are expected to accelerate adoption further. These trends position Defense Contractors & OEMs as the fastest-growing end-user segment during the forecast period.

.Defense Cyber Security Market Regional Analysis

North America dominated the Defense Cyber Security Market and accounted for the largest revenue share of 39.14% in 2025, supported by substantial defense budgets, extensive cybersecurity modernization programs, increasing adoption of zero-trust architecture, and the presence of leading defense cybersecurity vendors across the United States and Canada. The region continues to invest heavily in securing military networks, cloud-based defense infrastructure, critical national assets, and classified communications against increasingly sophisticated cyber threats. Growing deployment of AI-driven threat detection, secure defense cloud platforms, and advanced cyber resilience solutions further strengthens North America's leadership in the global market.

U.S. Defense Cyber Security Market Insight

The U.S. defense cyber security market is witnessing robust growth owing to rising investments in military cyber defense capabilities, zero-trust security implementation, and modernization of defense IT infrastructure. Increasing cyber threats targeting government agencies, defense contractors, and critical military assets are driving demand for advanced network security, endpoint protection, identity and access management, and cyber intelligence platforms. Furthermore, continued investments by the Department of Defense in AI-enabled cybersecurity, secure cloud environments, and cyber warfare preparedness are supporting sustained market expansion.

Europe Defense Cyber Security Market Insight

Europe remains a significant contributor to the Defense Cyber Security Market, driven by increasing defense digitalization, stronger cybersecurity regulations, and growing investments in military cyber resilience. Governments across the region are strengthening cyber defense capabilities to protect critical defense infrastructure, communication networks, and defense supply chains from evolving cyberattacks. Increasing collaboration among NATO members and rising adoption of zero-trust security frameworks continue to support regional market growth.

U.K. Defense Cyber Security Market Insight

The U.K. defense cyber security market is experiencing steady growth, supported by increasing investments in national cyber defense strategies, military digital transformation, and protection of critical defense infrastructure. The growing adoption of AI-powered threat intelligence, secure cloud computing, and advanced cyber monitoring solutions is enhancing operational resilience across defense organizations. Continuous government initiatives to strengthen cyber warfare readiness are further accelerating market growth.

Germany Defense Cyber Security Market Insight

Germany's defense cyber security market is expanding steadily due to increasing investments in military modernization, secure digital communications, and protection of defense-critical infrastructure. Rising adoption of cloud security, identity management solutions, and advanced threat detection technologies across defense agencies is strengthening national cyber resilience. In addition, government initiatives focused on strengthening cybersecurity capabilities and protecting defense supply chains continue to drive market expansion.

Asia-Pacific Defense Cyber Security Market Insight

The Asia-Pacific defense cyber security market is expected to witness the fastest growth, registering a CAGR of 13.9% from 2026 to 2033, fueled by increasing defense modernization initiatives, rising cyber warfare preparedness, growing military digitalization, and expanding cybersecurity investments across China, India, Japan, South Korea, and Australia. Increasing geopolitical tensions, rapid adoption of advanced defense technologies, and rising investments in secure military communication networks are expected to significantly accelerate regional market growth throughout the forecast period.

Japan Defense Cyber Security Market Insight

Japan's defense cyber security market is witnessing consistent growth due to rising investments in military cybersecurity, national defense modernization, and protection of critical government and defense infrastructure. The country is increasingly deploying advanced threat intelligence, secure cloud platforms, and AI-driven cyber defense technologies to strengthen national security. Continuous enhancement of cyber resilience and defense network security is supporting long-term market expansion.

China Defense Cyber Security Market Insight

China's defense cyber security market is growing rapidly, driven by increasing military digital transformation, expanding defense technology capabilities, and rising investments in cyber warfare preparedness. Government initiatives to strengthen cybersecurity infrastructure, protect military communication systems, and secure critical defense assets are accelerating market demand. Furthermore, continuous advancements in AI-enabled cyber defense, secure data protection technologies, and military network modernization are positioning China as one of the fastest-growing defense cyber security markets globally.

Defense Cyber Security Market Share

The Defense Cyber Security industry is primarily led by well-established companies, including:

- Palo Alto Networks, Inc. (U.S.)

- Lockheed Martin Corporation (U.S.)

- RTX Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- BAE Systems plc (U.K.)

- General Dynamics Corporation (U.S.)

- Leidos Holdings, Inc. (U.S.)

- Booz Allen Hamilton Holding Corporation (U.S.)

- Cisco Systems, Inc. (U.S.)

- Fortinet, Inc. (U.S.)

- CrowdStrike Holdings, Inc. (U.S.)

- Check Point Software Technologies Ltd. (Israel)

- Thales Group (France)

- Leonardo S.p.A. (Italy)

- Airbus Defence and Space (Netherlands)

- IBM Corporation (U.S.)

- Microsoft Corporation (U.S.)

- Oracle Corporation (U.S.)

- Accenture plc (Ireland)

- Capgemini SE (France)

- Atos SE (France)

- Raytheon Intelligence & Space (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- CACI International Inc. (U.S.)

- SAIC (Science Applications International Corporation) (U.S.)

- Splunk Inc. (U.S.)

- SentinelOne, Inc. (U.S.)

- Trellix (U.S.)

- Darktrace plc (U.K.)

- Mandiant (Google Cloud) (U.S.)

- Rapid7, Inc. (U.S.)

- Sophos Ltd. (U.K.)

- Trend Micro Incorporated (Japan)

- Fujitsu Limited (Japan)

Latest Developments in Defense Cyber Security Market

- In June 2021, the North Atlantic Treaty Organization approved its Comprehensive Cyber Defence Policy during the Brussels Summit, strengthening the Alliance's cyber deterrence posture and recognizing cyber defense as a core component of collective security. The policy enhanced resilience, expanded cyber capabilities, and reinforced coordinated responses to increasingly sophisticated cyber threats targeting military and critical defense infrastructure

- In October 2021, Microsoft announced the launch of Microsoft Defender for Cloud, integrating cloud security posture management (CSPM) with cloud workload protection to help defense organizations, government agencies, and critical infrastructure operators strengthen cybersecurity across hybrid and multi-cloud environments. The platform introduced unified threat protection, vulnerability assessment, and regulatory compliance capabilities for mission-critical workloads

- In July 2023, the North Atlantic Treaty Organization launched the Virtual Cyber Incident Support Capability (VCISC) during the Vilnius Summit to provide rapid cyber assistance to Allied nations responding to significant malicious cyber activities. The initiative improves collective cyber resilience by enabling expert support, faster incident response, and enhanced collaboration across member states

- In July 2024, the North Atlantic Treaty Organization announced the establishment of the NATO Integrated Cyber Defence Centre (NICC) at the Washington Summit. The new center is designed to strengthen protection of NATO and Allied military networks, improve cyber situational awareness, integrate civilian and military cyber expertise, and enhance collective defense against increasingly advanced cyber threats

- In October 2024, the North Atlantic Treaty Organization launched the Alliance Data Sharing Ecosystem (ADSE) initiative to enable secure, large-scale defense data sharing across Allied governments, industry, and academia. The platform supports AI-enabled military operations, improves situational awareness, and strengthens cyber resilience through secure and interoperable data exchange across defense organizations

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.