Global Dendritic Cell Therapy Vaccine Market

Market Size in USD Billion

USD

10.24 Billion

USD

15.41 Billion

2025

2033

USD

10.24 Billion

USD

15.41 Billion

2025

2033

| 2026 - 2033 | |

| USD 10.24 Billion | |

| USD 15.41 Billion | |

| % | |

|

What is the Dendritic Cell Therapy Vaccine Market Size and Overview?

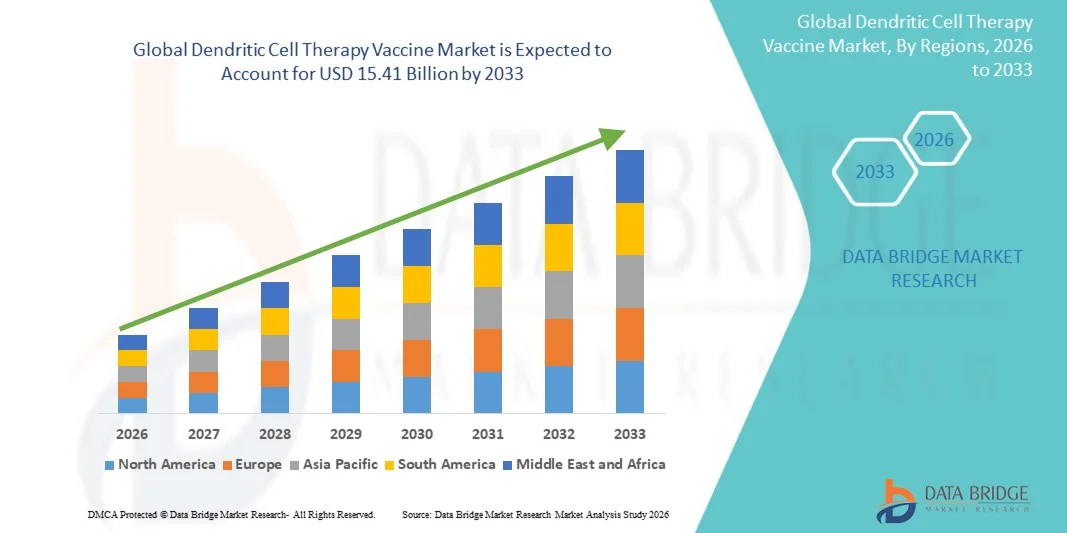

As per Data Bridge Market Research Analysis the Dendritic Cell Therapy Vaccine Market was valued at USD 10.24 billion in 2025 and is projected to reach USD 15.41 billion by 2033, growing at a CAGR of 5.25% from 2026 to 2033. The Dendritic Cell Therapy Vaccine Market is witnessing steady growth driven by increasing prevalence of cancer and rising focus on personalized immunotherapy approaches. Growing clinical evidence supporting dendritic cell-based vaccines in stimulating targeted anti-tumor immune responses is strengthening their adoption in oncology treatment pipelines. In addition, advancements in cell processing technologies, ex vivo dendritic cell culture techniques, and improved antigen-loading methods are enhancing vaccine efficacy and scalability across clinical applications.

The increasing burden of chronic diseases, particularly cancer, combined with the limitations of conventional chemotherapy and radiation therapies, is encouraging healthcare providers and research institutions to adopt next-generation immunotherapeutic approaches. Dendritic cell therapy vaccines are gaining traction in clinical trials and specialized cancer centers due to their ability to activate patient-specific immune responses with reduced systemic toxicity. Expanding regulatory support for cell-based therapies and rising investments in oncology research are further accelerating market growth globally.

Market Size & Forecast

- Global Market Value (2025): USD 10.24 billion

- Expected Market Value (2033): USD 15.41 billion

- Forecast CAGR (2026–2033): 5.25%

Key Market Trends & Insights

- North America dominated the Dendritic Cell Therapy Vaccine Market with the largest revenue share of 39.12% in 2025, supported by strong adoption of advanced cancer immunotherapy, well-established cell therapy manufacturing infrastructure, and high healthcare expenditure. The region benefits from a strong presence of leading biotechnology companies, advanced clinical research networks, and favorable regulatory pathways for cell-based therapies, particularly in the U.S.

- The Sipuleucel-T segment dominated the market with the largest revenue share of 58.42% in 2025, primarily due to its established clinical approval and strong commercialization in prostate cancer immunotherapy

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by rising cancer burden, expanding biotechnology investments, improving access to advanced immunotherapy treatments, and increasing clinical trial activities in China, India, Japan, and South Korea.

- The “Others” product segment is expected to register the fastest growth at a CAGR of 7.6% from 2026 to 2033, driven by ongoing pipeline development of next-generation dendritic cell vaccines, personalized neoantigen-based therapies, and combination immunotherapy approaches.

- The Adults end-use segment dominated the market with a 71.34% revenue share in 2025, owing to the higher prevalence of cancer in adult populations, wider treatment eligibility, and strong adoption of dendritic cell vaccines in oncology hospitals and specialty cancer centers.

- The Pediatrics segment is expected to witness the fastest growth at a CAGR of 7.9% from 2026 to 2033, supported by increasing research into pediatric immunotherapy applications, rising incidence of rare cancers in children, and growing clinical trials evaluating safety and efficacy in younger populations.

Report Scope and Dendritic Cell Therapy Vaccine Market Segmentation

|

Attributes |

Dendritic Cell Therapy Vaccine Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

What is the Key Trend in the Dendritic Cell Therapy Vaccine Market?

Trend: Growth in Personalized Cancer Immunotherapy and Cell-Based Vaccines

The Dendritic Cell Therapy Vaccine Market is witnessing strong growth driven by the rapid expansion of personalized cancer immunotherapy and increasing adoption of cell-based treatment approaches in oncology. Dendritic cell vaccines, such as sipuleucel-T (approved for prostate cancer in the U.S. by Dendreon Pharmaceuticals), have demonstrated improved overall survival in clinical studies, strengthening clinical confidence in immune-based therapies. According to oncology research estimates, cancer immunotherapy now accounts for over 40% of late-stage oncology clinical trials globally, with dendritic cell-based therapies gaining increasing attention for solid tumors such as melanoma, glioblastoma, and prostate cancer. Rising demand for targeted therapies with fewer systemic side effects compared to chemotherapy is further accelerating adoption in advanced cancer treatment centers.

Dendritic Cell Therapy Vaccine Market Dynamics

Key Market Driver: Rising Cancer Burden and Expansion of Immunotherapy Adoption

The Dendritic Cell Therapy Vaccine Market is primarily driven by the increasing global burden of cancer and the growing shift toward advanced immunotherapy-based treatment options. According to the World Health Organization (WHO), cancer is responsible for nearly 10 million deaths annually, with prostate cancer, lung cancer, and colorectal cancer among the most prevalent types. Pharmaceutical companies such as Bristol Myers Squibb, Merck & Co., and Roche are actively expanding immuno-oncology pipelines, accelerating demand for dendritic cell-based vaccines. Increasing approvals and clinical research funding for cell-based therapies are also supporting broader adoption in North America and Europe, where advanced oncology infrastructure enables faster integration of novel treatments.

Key Restraint/Challenge: High Cost of Therapy and Complex Manufacturing Processes

A major challenge in the Dendritic Cell Therapy Vaccine Market is the high cost of treatment and complex manufacturing process associated with personalized cell-based therapies. These vaccines require patient-specific cell extraction, ex vivo manipulation, antigen loading, and reinfusion, making large-scale production difficult and expensive. Treatment costs can exceed USD 80,000–100,000 per patient in certain markets, limiting accessibility, especially in low- and middle-income countries. In addition, stringent regulatory requirements for cell therapy production, cold chain logistics, and quality control further increase operational complexity, slowing down widespread commercialization beyond specialized oncology centers.

Key Market Opportunity: Expansion of Next-Generation Cell Therapy Platforms and Clinical Pipeline Growth

A significant opportunity in the market lies in the advancement of next-generation dendritic cell platforms combined with genetic engineering, mRNA technology, and AI-driven immunotherapy design. Companies such as BioNTech, Moderna, and Gilead Sciences are investing heavily in immune cell engineering and personalized cancer vaccines. More than 200+ cell-based immunotherapy candidates are currently in clinical development globally, with increasing focus on combination therapies that integrate checkpoint inhibitors and dendritic cell vaccines. Additionally, rising clinical trial activity in Asia-Pacific—especially in China, Japan, and South Korea—is expanding global access to innovative immunotherapy solutions and accelerating long-term market growth.

Dendritic Cell Therapy Vaccine Market Scope

The Dendritic Cell Therapy Vaccine market is segmented on the basis of product and end user.

- By Product

On the basis of product, the Dendritic Cell Therapy Vaccine Market is segmented into CreaVax, Sipuleucel-T, and Others. The Sipuleucel-T segment dominated the market with the largest revenue share of 58.42% in 2025, primarily due to its established clinical approval and strong commercialization in prostate cancer immunotherapy. The therapy is widely used for metastatic castration-resistant prostate cancer, supported by increasing global cancer burden, with more than 1.4 million new prostate cancer cases reported annually. Its adoption is further strengthened by strong reimbursement coverage in the United States and select European countries, along with growing physician confidence in dendritic cell-based immunotherapy outcomes. Leading oncology hospitals prefer Sipuleucel-T due to its proven survival benefits and inclusion in treatment guidelines for advanced prostate cancer. Rising investments in personalized cancer vaccines and expanding oncology infrastructure are further supporting its dominance. However, CreaVax also maintains steady adoption in select Asia-Pacific countries such as Japan and South Korea, though regulatory limitations restrict broader global penetration. Continuous advancements in dendritic cell therapy research and increasing clinical trials are expanding long-term product opportunities. Overall, strong clinical validation and commercial maturity make Sipuleucel-T the dominant product segment in the market.

The CreaVax segment is expected to register the fastest CAGR of 11.8% from 2026 to 2033, driven by rising clinical research activity and growing government support for regenerative medicine in Asia-Pacific regions. Countries such as Japan and South Korea are actively investing in personalized immunotherapy platforms, accelerating adoption of dendritic cell-based treatments. Increasing clinical trials targeting glioblastoma, melanoma, and other solid tumors are strengthening the therapeutic potential of CreaVax. The segment is also benefiting from growing interest in autologous cell therapy approaches that enhance patient-specific immune responses. Expanding biotech collaborations and rising funding for oncology innovation are further boosting development pipelines. Compared to conventional treatments, CreaVax offers improved customization potential, increasing its appeal in experimental oncology. Advancements in cell processing technologies are also improving manufacturing efficiency and scalability. Academic research institutes and hospitals are increasingly participating in dendritic cell vaccine trials, contributing to market expansion. Supportive regulatory pathways for orphan and rare cancer indications are further encouraging adoption. Growing global focus on precision medicine is accelerating long-term growth prospects. Overall, CreaVax is emerging as the fastest-growing product segment in the global market.

- By End-Use

On the basis of end-use, the Dendritic Cell Therapy Vaccine Market is segmented into Pediatrics and Adults. The Adults segment dominated the market with a revenue share of 91.36% in 2025, owing to the significantly higher incidence of cancer in adult and elderly populations. Adults above the age of 50 represent the primary patient pool for dendritic cell-based immunotherapies, particularly for prostate cancer, lung cancer, and melanoma. The segment benefits from strong clinical validation and widespread adoption in oncology centers across North America and Europe. Improved healthcare infrastructure, better insurance coverage, and increased access to advanced immunotherapy treatments further strengthen market dominance. Rising global cancer prevalence, coupled with aging populations, continues to expand the adult treatment base. Hospitals and specialty cancer centers are increasingly integrating dendritic cell vaccines into personalized oncology treatment protocols. Additionally, clinical trials and approved therapies are largely focused on adult populations, reinforcing their dominance in the market. Growing awareness of immunotherapy benefits among oncologists is further driving adoption. Government healthcare programs and reimbursement systems in developed economies also support treatment accessibility. Overall, the adult segment remains the core revenue-generating category in the market.

The Pediatrics segment is expected to register the fastest CAGR of 10.6% from 2026 to 2033, driven by increasing research focus on pediatric oncology and rare cancer treatment development. Rising incidence of childhood cancers such as leukemia, brain tumors, and lymphoma is creating demand for advanced immunotherapy approaches. Governments and research organizations are increasing funding for pediatric rare disease programs, supporting innovation in dendritic cell-based vaccines. Clinical trials targeting pediatric oncology are gradually expanding, improving treatment safety and efficacy data. Advances in cell engineering and dosage optimization are enabling safer applications for children. Hospitals and academic institutions are increasingly collaborating to develop pediatric-specific immunotherapy solutions. Growing awareness among healthcare providers about early intervention is improving diagnosis and treatment adoption. Regulatory incentives for orphan drug development are further accelerating research in this segment. Pharmaceutical companies are investing in pediatric oncology pipelines to address unmet medical needs. Personalized medicine approaches are gaining traction in pediatric cancer care. Overall, Pediatrics represents the fastest-growing end-use segment globally.

Dendritic Cell Therapy Vaccine Market Regional Analysis

North America dominated the Dendritic Cell Therapy Vaccine market and accounted for the largest revenue share of 39.12% in 2025, driven by strong adoption of advanced cancer immunotherapy and well-established cell therapy manufacturing infrastructure. The region benefits from high healthcare expenditure, advanced oncology treatment facilities, and strong penetration of personalized medicine approaches across major hospitals and cancer centers. The presence of leading biotechnology and pharmaceutical companies in the United States further strengthens market leadership, supporting rapid development and commercialization of dendritic cell-based therapies. In addition, robust clinical research networks and well-structured regulatory frameworks from agencies such as the FDA facilitate faster approval of innovative cell and gene therapies. Increasing focus on precision oncology and individualized cancer treatment is further accelerating adoption across healthcare systems. Strong investments in R&D for immunotherapy and biologics manufacturing are also expanding production capabilities. Growing prevalence of cancer, particularly prostate and lung cancer, continues to drive consistent demand for dendritic cell vaccines. Academic research institutions and biotech startups are actively contributing to innovation in next-generation immunotherapies. Integration of advanced bioprocessing technologies is improving scalability and treatment efficiency. Expanding clinical trial activity across multiple oncology indications further strengthens regional dominance. Overall, strong infrastructure and early technology adoption make North America the leading regional market.

U.S. Dendritic Cell Therapy Vaccine Market Insight

The U.S. Dendritic Cell Therapy Vaccine market is witnessing strong growth due to rising investment in cancer immunotherapy research, increasing prevalence of chronic and oncological diseases, and strong presence of leading biotechnology companies. The country has a highly advanced healthcare ecosystem with extensive adoption of personalized medicine and cell-based therapies across oncology centers. FDA support for expedited approval pathways such as Breakthrough Therapy Designation is accelerating commercialization of dendritic cell vaccines. Major pharmaceutical companies and biotech firms are heavily investing in immunotherapy pipelines targeting prostate cancer, melanoma, and other solid tumors. The U.S. also benefits from a well-developed clinical trial infrastructure, with thousands of oncology trials actively ongoing. Increasing collaboration between academic research institutes and biotech companies is driving innovation in dendritic cell technology. Rising healthcare expenditure and strong insurance coverage are improving patient access to advanced treatments. Growing demand for precision oncology and targeted therapies is further supporting adoption. Expansion of GMP-certified manufacturing facilities for cell therapy production is strengthening supply capabilities. Continuous advancements in immuno-oncology research are enhancing treatment outcomes. Overall, the U.S. remains the core growth engine of the North American market.

Europe Dendritic Cell Therapy Vaccine Market Insight

The Europe Dendritic Cell Therapy Vaccine market remains a significant contributor to global revenue, supported by strong healthcare systems, increasing adoption of advanced oncology treatments, and well-structured regulatory frameworks for cell and gene therapies. Countries such as Germany, France, and the U.K. are leading in clinical research and immunotherapy adoption. The European Medicines Agency (EMA) provides clear regulatory pathways for advanced therapy medicinal products (ATMPs), supporting faster approval of dendritic cell-based treatments. Rising cancer prevalence across Europe is driving sustained demand for innovative oncology therapies. The region also benefits from strong academic-industry collaborations, which are accelerating research in personalized immunotherapy. Increasing investments in biotechnology infrastructure are expanding production and clinical capabilities. Hospitals and cancer research centers are increasingly integrating dendritic cell vaccines into treatment protocols for advanced cancers. Growing participation in multinational clinical trials is enhancing innovation output. Supportive government funding for oncology research is further strengthening market growth. Adoption of precision medicine approaches is increasing across European healthcare systems. Overall, Europe continues to maintain a strong and stable position in the global market.

U.K. Dendritic Cell Therapy Vaccine Market Insight

The U.K. Dendritic Cell Therapy Vaccine market is experiencing steady growth due to rising focus on advanced cancer treatment research and increasing adoption of immunotherapy-based approaches in oncology care. The country has a strong clinical research ecosystem supported by the National Health Service (NHS) and leading academic institutions. Growing investments in biotechnology and life sciences are strengthening cell therapy development capabilities. The U.K. is actively participating in global oncology clinical trials, particularly in immunotherapy and personalized cancer vaccines. Increasing incidence of cancer and growing demand for targeted therapies are supporting market expansion. Regulatory support from the Medicines and Healthcare products Regulatory Agency (MHRA) is facilitating faster access to innovative therapies. Collaboration between universities, biotech startups, and pharmaceutical companies is accelerating innovation. Expansion of GMP-compliant manufacturing facilities is improving production capacity for cell-based therapies. Rising awareness of precision oncology among clinicians is driving adoption. Government funding for cancer research programs is further boosting development activity. Overall, the U.K. is emerging as an important innovation hub in Europe.

Germany Dendritic Cell Therapy Vaccine Market Insight

The Germany Dendritic Cell Therapy Vaccine market is expanding steadily due to its strong biotechnology sector, advanced healthcare infrastructure, and high level of investment in oncology research. Germany is one of the leading European countries in cell therapy manufacturing and clinical innovation. The presence of world-class research institutes and pharmaceutical companies is driving advancements in dendritic cell-based immunotherapy. Increasing cancer burden, particularly prostate and lung cancer, is supporting demand for advanced treatment options. Hospitals and specialized cancer centers are increasingly adopting personalized immunotherapy approaches. Strong government funding for biotechnology and life sciences research is enhancing innovation capacity. Germany also benefits from robust clinical trial activity in oncology and immunotherapy. Integration of advanced bioprocessing and cell manufacturing technologies is improving production efficiency. Academic-industry collaboration is a key driver of innovation in the country. Regulatory support for ATMPs under EMA guidelines is facilitating market growth. Overall, Germany remains a key contributor to the European dendritic cell therapy vaccine market.

Asia-Pacific Dendritic Cell Therapy Vaccine Market Insight

The Asia-Pacific Dendritic Cell Therapy Vaccine market is expected to witness the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by rising cancer burden, expanding biotechnology investments, and improving access to advanced immunotherapy treatments. Countries such as China, India, Japan, and South Korea are increasingly focusing on strengthening their oncology and biopharmaceutical sectors. Rapid improvements in healthcare infrastructure and growing awareness of personalized medicine are supporting market expansion. Increasing participation in clinical trials for dendritic cell-based therapies is boosting innovation in the region. Governments are investing heavily in biotechnology parks, research institutions, and cell therapy manufacturing facilities. Rising disposable income and healthcare expenditure are improving patient access to advanced cancer treatments. Expansion of domestic biotech companies is accelerating development of immunotherapy pipelines. Adoption of precision oncology is increasing across major hospitals and cancer centers. International collaborations with U.S. and European biotech firms are enhancing technology transfer. Regulatory reforms are also improving approval timelines for advanced therapies. Overall, Asia-Pacific represents the fastest-growing regional market globally.

Japan Dendritic Cell Therapy Vaccine Market Insight

The Japan Dendritic Cell Therapy Vaccine market is witnessing steady growth due to strong government support for regenerative medicine and advanced cancer immunotherapy. Japan is one of the earliest adopters of dendritic cell-based vaccines, particularly CreaVax, in clinical applications. The country has a highly advanced healthcare system and strong regulatory framework supporting regenerative medicine through the PMDA. Increasing incidence of cancer and aging population are driving demand for innovative oncology treatments. Hospitals and research institutes are actively involved in clinical development of personalized immunotherapies. Strong investment in biotechnology and cell therapy manufacturing is enhancing production capabilities. Integration of advanced cell processing technologies is improving treatment efficiency. Japan also benefits from active collaboration between academia and industry in immunotherapy research. Rising focus on precision medicine is further supporting adoption of dendritic cell vaccines. Continuous clinical trials in solid tumor indications are expanding therapeutic applications. Overall, Japan remains a key innovation hub in Asia-Pacific.

China Dendritic Cell Therapy Vaccine Market Insight

The China Dendritic Cell Therapy Vaccine market is growing rapidly due to rising cancer incidence, expanding biotechnology sector, and strong government support for advanced medical innovation. China is heavily investing in oncology research, immunotherapy development, and cell therapy manufacturing infrastructure. Increasing urbanization and improving healthcare access are expanding patient reach for advanced treatments. The country is witnessing strong growth in clinical trials focused on dendritic cell-based vaccines and other immunotherapies. Domestic biotech companies are rapidly expanding their oncology pipelines with strong government backing. Rising awareness of precision oncology among healthcare providers is boosting adoption. China’s regulatory reforms for cell and gene therapies are accelerating approval timelines. Investment in biotechnology parks and GMP-certified facilities is strengthening production capacity. Collaboration with global pharmaceutical companies is supporting technology transfer and innovation. Growing burden of cancer, particularly lung and gastric cancers, is further driving demand. Overall, China is emerging as one of the fastest-growing markets globally.

Dendritic Cell Therapy Vaccine Market Share

The Dendritic Cell Therapy Vaccine industry is primarily led by well-established companies, including:

- Dendreon Pharmaceuticals LLC (U.S.)

- Northwest Biotherapeutics Inc. (U.S.)

- BrainStorm Cell Therapeutics Inc. (Israel)

- Lonza Group AG (Switzerland)

- Bellicum Pharmaceuticals Inc. (U.S.)

- Astellas Pharma Inc. (Japan)

- GlaxoSmithKline plc (U.K.)

- Novartis AG (Switzerland)

- Ferring Pharmaceuticals (Switzerland)

- Bristol Myers Squibb (U.S.)

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Roche Holding AG (Switzerland)

- Johnson & Johnson (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Sanofi S.A. (France)

- AstraZeneca plc (U.K.)

- Amgen Inc. (U.S.)

- Gilead Sciences Inc. (U.S.)

- Celgene Corporation (U.S.)

- Kite Pharma (U.S.)

- Bluebird Bio Inc. (U.S.)

- Adaptimmune Therapeutics plc (U.K.)

- Immunicum AB (Sweden)

- Elicio Therapeutics Inc. (U.S.)

- Sellas Life Sciences Group Inc. (U.S.)

- Medigene AG (Germany)

- Glycostem Therapeutics (Netherlands)

- TreeFrog Therapeutics (France)

- SOTIO Biotech (Czech Republic)

- CellGenix GmbH (Germany)

- Be The Match BioTherapies (U.S.)

- Atara Biotherapeutics Inc. (U.S.)

- Celyad Oncology SA (Belgium)

- Tessa Therapeutics (Singapore)

- Immatics N.V. (Germany)

- BioNTech SE (Germany)

- Moderna Inc. (U.S.)

- CureVac N.V. (Germany)

Latest Developments in Dendritic Cell Therapy Vaccine Market

- In April 2021, multiple peer-reviewed clinical updates and immuno-oncology reviews highlighted the continued clinical validation of Sipuleucel-T (Provenge), the first FDA-approved dendritic cell–based therapeutic cancer vaccine, reinforcing its role in treating metastatic castration-resistant prostate cancer. These publications emphasized improved overall survival outcomes and reaffirmed dendritic cell therapy as a clinically viable immunotherapy platform in oncology, while also discussing ongoing efforts to improve next-generation dendritic cell vaccine efficacy through improved antigen loading and combination therapies

- In June 2021, researchers published findings on next-generation dendritic cell vaccine strategies focusing on overcoming limitations of monocyte-derived DC approaches, particularly in prostate and solid tumor cancers. The study emphasized emerging technologies such as nanoparticle-based antigen delivery and viral vector-assisted dendritic cell activation to improve immune response strength and durability, signaling a major R&D shift toward more advanced DC vaccine engineering platforms

- In September 2022, updated clinical oncology literature confirmed that Sipuleucel-T (Provenge) remained the only FDA-approved dendritic cell–based cancer vaccine, widely used for prostate cancer immunotherapy. The studies reinforced its mechanism of action involving autologous antigen-presenting dendritic cells activated against prostatic acid phosphatase (PAP), while also highlighting its continued clinical relevance despite the emergence of newer immunotherapy modalities

- In February 2023, immunotherapy pipeline reports documented increased global clinical trial activity for dendritic cell–based cancer vaccines targeting glioblastoma, melanoma, and renal cell carcinoma. Companies and research institutions expanded Phase II and Phase III trials, particularly for CreaVax (South Korea) and DCVax-L (U.S.), reflecting growing investment in personalized autologous dendritic cell vaccine platforms for solid tumor treatment and long-term immune activation strategies

- In August 2024, regulatory and market analyses highlighted that Sipuleucel-T continued to dominate the dendritic cell vaccine market, maintaining the largest share due to its FDA approval status and established reimbursement pathways in the United States. However, studies also noted logistical challenges such as complex manufacturing and 3–5 week production cycles, which limited broader adoption in decentralized healthcare systems

- In March 2025, advanced immuno-oncology research publications reported significant progress in dendritic cell–derived exosome therapies and next-generation cell-free vaccine approaches. These developments aimed to overcome limitations of traditional dendritic cell vaccines by improving scalability, reducing manufacturing complexity, and enhancing tumor-specific immune activation, marking a key innovation trend in the DC vaccine landscape

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.