Global Diabetic Macular Edema Treatment Market

Market Size in USD Billion

USD

54.87 Billion

USD

73.09 Billion

2025

2033

USD

54.87 Billion

USD

73.09 Billion

2025

2033

| 2026 - 2033 | |

| USD 54.87 Billion | |

| USD 73.09 Billion | |

| % | |

|

Diabetic Macular Edema Treatment Market Size

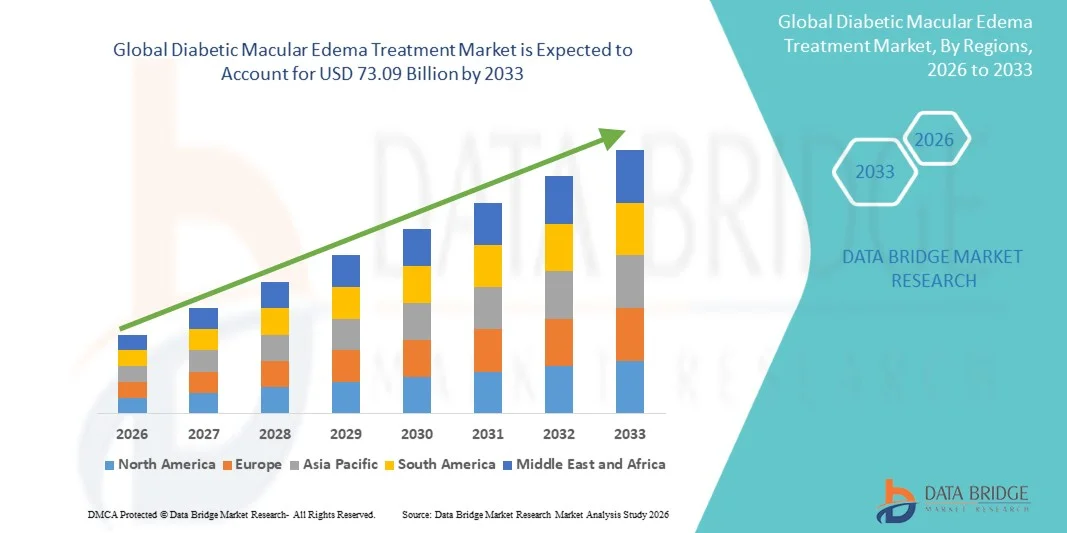

- The global Diabetic Macular Edema Treatment market size was valued at USD 54.87 billion in 2025and is expected to reach USD 73.09 billion by 2033, at a CAGR of 3.65% during the forecast period

- The market growth is largely fueled by the increasing prevalence of diabetes and advancements in ophthalmic treatment technologies, leading to improved diagnosis and management of retinal disorders such as diabetic macular edema

- Furthermore, rising patient awareness, growing demand for effective vision-preserving therapies, and the availability of advanced treatment options such as anti-VEGF therapies and corticosteroid implants are establishing diabetic macular edema treatments as essential components of modern eye care. These converging factors are accelerating the uptake of Diabetic Macular Edema Treatment solutions, thereby significantly boosting the industry's growth

Diabetic Macular Edema Treatment Market Analysis

- Diabetic macular edema (DME) treatment solutions, including anti-VEGF therapies, corticosteroid implants, and laser treatments, are increasingly vital components of modern ophthalmic care across hospitals, specialty eye clinics, and ambulatory surgical centers due to their ability to preserve vision and prevent disease progression

- The escalating demand for DME treatments is primarily fueled by the rising global prevalence of diabetes, increasing awareness about early diagnosis of retinal disorders, and a growing preference for minimally invasive and highly effective treatment options

- North America dominated the Diabetic Macular Edema Treatment market with the largest revenue share of 38.6% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative biologics, and a strong presence of key pharmaceutical players, with the U.S. experiencing substantial growth driven by continuous R&D and increasing patient access to treatment

- Asia-Pacific is expected to be the fastest growing region in the Diabetic Macular Edema Treatment market during the forecast period due to the rapidly increasing diabetic population, improving healthcare access, and rising healthcare expenditure across emerging economies such as China and India

- The intravitreous injections segment dominated the market with a revenue share of approximately 68.9% in 2025, driven by its widespread use as the primary method for delivering anti-VEGF drugs

Report Scope and Diabetic Macular Edema Treatment Market Segmentation

|

Attributes |

Diabetic Macular Edema Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· F. Hoffmann-La Roche Ltd. (Switzerland) · Novartis AG (Switzerland) · Regeneron Pharmaceuticals, Inc. (U.S.) · Bayer AG (Germany) · AbbVie Inc. (U.S.) · Alimera Sciences, Inc. (U.S.) · Santen Pharmaceutical Co., Ltd. (Japan) · Ocular Therapeutix, Inc. (U.S.) · Allergan (an AbbVie company) (U.S.) · Kodiak Sciences Inc. (U.S.) · Oxurion NV (Belgium) · Graybug Vision, Inc. (U.S.) · Adverum Biotechnologies, Inc. (U.S.) · Rocket Pharmaceuticals, Inc. (U.S.) · Lineage Cell Therapeutics, Inc. (U.S.) · Apellis Pharmaceuticals, Inc. (U.S.) · Chugai Pharmaceutical Co., Ltd. (Japan) · Chengdu Kanghong Pharmaceutical Group Co., Ltd. (China) · Samsung Bioepis Co., Ltd. (South Korea) · Biogen Inc. (U.S.) |

|

Market Opportunities |

· Rising Diabetic Population and Untapped Emerging Markets · Advancements in Long-Acting Therapies and Drug Delivery Systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Diabetic Macular Edema Treatment Market Trends

“Advancements in Anti-VEGF Therapies and Long-Acting Treatment Modalities”

- A significant and accelerating trend in the global Diabetic Macular Edema Treatment market is the increasing adoption of advanced anti-VEGF therapies, sustained-release drug delivery systems, and personalized ophthalmic care approaches aimed at improving visual outcomes and reducing treatment burden. This shift is significantly enhancing long-term disease management

- For instance, anti-VEGF agents such as aflibercept, ranibizumab, and newer long-acting formulations are widely used to reduce retinal swelling and improve vision in patients with Diabetic Macular Edema, while ongoing innovations focus on extending dosing intervals to minimize frequent injections

- Advances in retinal imaging technologies, including optical coherence tomography (OCT), are enabling precise diagnosis and continuous monitoring of disease progression. For instance, clinicians can assess retinal thickness and fluid accumulation in real time, allowing for more accurate and individualized treatment planning. Furthermore, sustained-release implants and corticosteroid-based therapies are providing alternative options for patients with inadequate response to first-line treatments

- The integration of combination therapies, including laser photocoagulation alongside pharmacologic treatment, is facilitating a more comprehensive approach to disease control. Through coordinated ophthalmology care, patients receive optimized therapy based on severity and response patterns

- This trend toward more durable, patient-centric, and outcome-driven treatment strategies is fundamentally reshaping expectations in retinal disease management. Consequently, companies such as Regeneron, Roche, and Novartis are investing in innovative ophthalmic therapies and delivery platforms

- The demand for Diabetic Macular Edema treatments that offer improved visual acuity, reduced injection frequency, and enhanced patient compliance is growing rapidly across ophthalmology clinics and specialty eye care centers

Diabetic Macular Edema Treatment Market Dynamics

Driver

“Rising Prevalence of Diabetes and Increasing Awareness of Vision Complications”

- The increasing global prevalence of diabetes, along with growing awareness of diabetes-related vision complications, is a significant driver for the Diabetic Macular Edema Treatment marke

- For instance, rising screening programs for diabetic retinopathy in hospitals and eye care clinics are leading to earlier detection of macular edema, thereby increasing demand for timely treatment interventions

- As patients become more aware of the risks of untreated retinal conditions, there is a higher tendency to seek regular eye examinations and specialist consultations

- Furthermore, improvements in healthcare infrastructure and access to ophthalmology services are enabling better diagnosis and treatment availability across both developed and emerging regions

- The growing adoption of advanced therapeutics and imaging technologies is further accelerating market growth by improving treatment outcomes and patient adherence

Restraint/Challenge

“High Treatment Costs and Need for Repeated Interventions”

- One of the major challenges in the Diabetic Macular Edema Treatment market is the high cost associated with advanced therapies, particularly anti-VEGF injections and sustained-release implants, which may limit accessibility for some patients

- For instance, patients often require multiple intravitreal injections over extended periods, leading to increased financial burden and reduced adherence to long-term treatment regimens

- The need for frequent clinical visits and continuous monitoring can also create logistical challenges for elderly patients or those in remote areas

- Variability in treatment response and potential side effects associated with repeated injections may further impact patient compliance and outcomes

- Addressing these challenges through cost-effective treatment options, extended-duration therapies, and improved patient support programs will be essential for sustained market growth

Diabetic Macular Edema Treatment Market Scope

The market is segmented on the basis of indication type, treatment type, drug delivery, and end user.

- By Indication Type

On the basis of indication type, the Diabetic Macular Edema Treatment market is segmented into diffuse diabetic macular edema and focal diabetic macular edema. The diffuse diabetic macular edema segment dominated the largest market revenue share of approximately 57.4% in 2025, driven by its higher prevalence among diabetic patients and its association with widespread retinal thickening. This form is more complex to manage, often requiring long-term and repeated treatment interventions, thereby increasing market demand. The rising global burden of diabetes significantly contributes to the growth of this segment. Increased awareness regarding early diagnosis and treatment further supports its dominance. Advancements in imaging technologies such as OCT enable better identification and monitoring of diffuse cases. The segment also benefits from the availability of multiple therapeutic options including anti-VEGF therapies and corticosteroids. Healthcare providers prioritize treating diffuse cases due to their higher risk of vision loss. Growing geriatric population also adds to patient pool. Strong clinical pipeline targeting advanced stages further boosts growth.

The focal diabetic macular edema segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, driven by improved diagnostic capabilities and early-stage detection. Focal edema is more localized and often treated effectively with targeted therapies such as laser photocoagulation. Increasing screening programs for diabetic retinopathy contribute to early identification of focal cases. This segment benefits from shorter treatment durations and cost-effective therapies. Technological advancements in laser systems enhance treatment outcomes. Rising patient awareness regarding eye health also fuels growth. Increasing access to ophthalmology services in emerging regions supports expansion. Pharmaceutical companies are focusing on developing targeted therapies for focal cases. Favorable reimbursement policies in developed markets further drive adoption. Continuous improvements in minimally invasive procedures enhance patient compliance.

- By Treatment Type

On the basis of treatment type, the market is segmented into vascular endothelial growth factor (VEGF), corticosteroids, laser photocoagulation therapy, and other off-label drugs. The VEGF segment held the largest market revenue share of around 48.6% in 2025, driven by its high efficacy in reducing retinal swelling and improving vision outcomes. Anti-VEGF therapies are considered the gold standard for treating diabetic macular edema. Increasing adoption of drugs such as ranibizumab and aflibercept supports segment growth. Frequent product approvals and strong clinical evidence further enhance dominance. Growing awareness among ophthalmologists regarding advanced biologics boosts usage. Rising healthcare expenditure enables access to these premium therapies. The segment also benefits from ongoing research and development activities. Expansion of specialty eye care centers increases treatment adoption. Favorable clinical guidelines recommending VEGF therapies further strengthen the segment. Improved patient outcomes drive repeat treatments, increasing revenue share.

The corticosteroids segment is projected to witness the fastest CAGR of 9.7% from 2026 to 2033, driven by their effectiveness in patients unresponsive to anti-VEGF therapies. Corticosteroids help reduce inflammation and vascular leakage in the retina. Increasing use of sustained-release steroid implants boosts segment growth. These therapies require fewer injections compared to anti-VEGF treatments, improving patient compliance. Growing demand for long-acting treatments further supports expansion. Technological advancements in drug formulations enhance safety profiles. Rising prevalence of chronic diabetic complications drives adoption. Increasing physician preference for combination therapies also contributes to growth. Expansion of treatment options in emerging markets enhances accessibility. Continuous innovation in steroid delivery systems accelerates market penetration.

- By Drug Delivery

On the basis of drug delivery, the market is segmented into intravitreal injections and intravitreal implants. The intravitreous injections segment dominated the market with a revenue share of approximately 68.9% in 2025, driven by its widespread use as the primary method for delivering anti-VEGF drugs. This method allows direct delivery of medication into the eye, ensuring high efficacy and rapid action. Increasing number of patients undergoing repeated injections supports segment growth. Availability of established treatment protocols further strengthens dominance. Healthcare providers prefer injections due to their proven clinical outcomes. Rising number of ophthalmology clinics offering injection-based therapies boosts demand. Technological advancements in injection devices improve safety and precision. Strong reimbursement frameworks in developed regions further support adoption. Growing patient awareness regarding vision preservation contributes to demand. Continuous use in long-term treatment plans ensures sustained revenue.

The intravitreal implants segment is expected to witness the fastest CAGR of 10.4% from 2026 to 2033, driven by the increasing demand for sustained drug release systems. Implants reduce the frequency of administration, improving patient convenience and adherence. Growing preference for long-acting therapies supports segment growth. Technological advancements in biodegradable implants enhance safety and effectiveness. Increasing adoption among patients requiring chronic treatment further drives demand. Expansion of product pipelines with innovative implant solutions boosts growth. Rising healthcare investments in advanced ophthalmic care also contribute. Improved clinical outcomes with fewer hospital visits enhance patient satisfaction. Growing awareness among physicians regarding implant benefits accelerates adoption. Continuous innovation in drug delivery technologies supports long-term expansion.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, and home care. The hospitals segment accounted for the largest market revenue share of approximately 55.1% in 2025, driven by the availability of advanced diagnostic and treatment facilities. Hospitals serve as primary centers for managing complex diabetic eye conditions. Presence of skilled ophthalmologists and specialized equipment enhances treatment outcomes. Increasing number of hospital-based eye care units supports growth. Government investments in healthcare infrastructure further strengthen the segment. Hospitals also handle a high volume of patients requiring advanced therapies. Integration of diagnostic and therapeutic services improves efficiency. Rising number of surgical and injection procedures boosts demand. Strong referral networks contribute to patient inflow. Continuous expansion of hospital services ensures sustained dominance.

The clinics segment is anticipated to witness the fastest CAGR of 9.2% from 2026 to 2033, driven by the growing number of specialized ophthalmology clinics. Clinics offer cost-effective and accessible treatment options compared to hospitals. Increasing patient preference for outpatient care supports growth. Expansion of private eye care centers enhances accessibility. Technological advancements enable clinics to provide advanced treatments. Rising awareness regarding early diagnosis boosts patient visits. Clinics also benefit from shorter waiting times and personalized care. Growing urban population increases demand for nearby healthcare facilities. Partnerships with pharmaceutical companies improve treatment availability. Continuous growth in ambulatory care services accelerates segment expansion.

Diabetic Macular Edema Treatment Market Regional Analysis

- North America dominated the diabetic macular edema treatment market with the largest revenue share of 38.6% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative biologics, and a strong presence of key pharmaceutical players

- The region is witnessing increased utilization of anti-VEGF therapies, corticosteroid implants, and laser treatments for effective disease management

- Moreover, the growing diabetic population and improved access to ophthalmic care are further supporting market growth, with the U.S. experiencing substantial expansion driven by continuous R&D and increasing patient access to advanced treatment options

U.S. Diabetic Macular Edema Treatment Market Insight

The U.S. diabetic macular edema treatment market captured the largest revenue share in 2025 within North America, fueled by the high prevalence of diabetes and strong adoption of advanced treatment modalities. Patients and healthcare providers are increasingly relying on biologics such as anti-VEGF injections and sustained-release drug implants for improved visual outcomes. In addition, favorable reimbursement policies, robust clinical research activities, and the presence of leading pharmaceutical companies are accelerating market growth. The integration of innovative drug delivery systems and ongoing clinical trials further strengthens the country’s leadership in this market.

Europe Diabetic Macular Edema Treatment Market Insight

The Europe diabetic macular edema treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by well-established healthcare systems and increasing awareness regarding early diagnosis and treatment of diabetic eye diseases. The growing aging population, along with the rising incidence of diabetes, is contributing to the demand for effective treatment options. In addition, government initiatives supporting vision care and access to advanced therapies are fostering market growth across the region.

U.K. Diabetic Macular Edema Treatment Market Insight

The U.K. diabetic macular edema treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of diabetic complications and strong adoption of anti-VEGF therapies. The presence of an organized healthcare system and rising screening programs for diabetic retinopathy are encouraging early diagnosis and timely intervention. Furthermore, continuous advancements in ophthalmology treatments and patient access to innovative therapies are expected to support market growth.

Germany Diabetic Macular Edema Treatment Market Insight

The Germany diabetic macular edema treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing healthcare expenditure and strong demand for advanced ophthalmic treatments. Germany’s well-developed healthcare infrastructure and emphasis on technological innovation are promoting the adoption of novel therapies, including biologics and combination treatments. In addition, a growing focus on early disease management and patient awareness is contributing to sustained market expansion.

Asia-Pacific Diabetic Macular Edema Treatment Market Insight

The Asia-Pacific diabetic macular edema treatment market market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by the rapidly increasing diabetic population, improving healthcare access, and rising healthcare expenditure across emerging economies such as China and India. The region is witnessing growing awareness regarding diabetic eye diseases and expanding availability of advanced treatment options. Government initiatives aimed at strengthening healthcare infrastructure and increasing screening programs are further boosting market growth.

Japan Diabetic Macular Edema Treatment Market Insight

The Japan Diabetic diabetic macular edema treatment market is gaining momentum due to the country’s advanced healthcare system and increasing prevalence of diabetes among the aging population. The market is characterized by high adoption of innovative treatment options, including anti-VEGF therapies and sustained drug delivery systems. In addition, strong regulatory support and continuous advancements in ophthalmic research are contributing to market expansion.

China Diabetic Macular Edema Treatment Market Insight

The China Diabetic diabetic macular edema treatment market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s large diabetic population and rapidly improving healthcare infrastructure. Increasing awareness regarding early diagnosis and treatment, along with expanding access to advanced therapies, is driving market growth. Furthermore, government initiatives to enhance healthcare services and the presence of domestic and international pharmaceutical companies are key factors propelling the market in China.

Diabetic Macular Edema Treatment Market Share

The Diabetic Macular Edema Treatment industry is primarily led by well-established companies, including:

- Hoffmann-La Roche Ltd. (Switzerland)

- Novartis AG (Switzerland)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Bayer AG (Germany)

- AbbVie Inc. (U.S.)

- Alimera Sciences, Inc. (U.S.)

- Santen Pharmaceutical Co., Ltd. (Japan)

- Ocular Therapeutix, Inc. (U.S.)

- Allergan (an AbbVie company) (U.S.)

- Kodiak Sciences Inc. (U.S.)

- Oxurion NV (Belgium)

- Graybug Vision, Inc. (U.S.)

- Adverum Biotechnologies, Inc. (U.S.)

- Rocket Pharmaceuticals, Inc. (U.S.)

- Lineage Cell Therapeutics, Inc. (U.S.)

- Apellis Pharmaceuticals, Inc. (U.S.)

- Chugai Pharmaceutical Co., Ltd. (Japan)

- Chengdu Kanghong Pharmaceutical Group Co., Ltd. (China)

- Samsung Bioepis Co., Ltd. (South Korea)

- Biogen Inc. (U.S.)

Latest Developments in Global Diabetic Macular Edema Treatment Market

- In August 2023, Regeneron announced that the U.S. FDA approved EYLEA HD (aflibercept 8 mg) for the treatment of diabetic macular edema, introducing a higher-dose formulation designed to extend dosing intervals and reduce the frequency of intravitreal injections while maintaining visual outcomes

- In February 2025, Genentech (a member of Roche Group) announced that the U.S. FDA approved Susvimo (ranibizumab injection) for the treatment of diabetic macular edema, making it the first and only continuous delivery implant system that maintains vision with fewer treatments compared to standard monthly eye injections

- In May 2025, Genentech highlighted expanded clinical utility of Susvimo through its Port Delivery Platform, demonstrating the ability to maintain vision in diabetic retinopathy and DME patients with as few as one refill every nine months, significantly reducing treatment burden for patients and healthcare systems

- In May 2025, the FDA approval of the Port Delivery System (PDS) with ranibizumab for both diabetic retinopathy and diabetic macular edema marked a major advancement in long-acting ophthalmic drug delivery, supported by clinical data showing comparable outcomes to monthly anti-VEGF injections with reduced injection frequency

- In November 2025, Regeneron announced that the U.S. FDA approved EYLEA HD (aflibercept 8 mg) for macular edema following retinal vein occlusion, while also supporting flexible dosing across approved indications including diabetic macular edema, reinforcing the shift toward extended-interval anti-VEGF therapies

- In December 2025, ophthalmology updates highlighted increasing market competition with the introduction of biosimilar anti-VEGF therapies referencing aflibercept, aimed at improving affordability and expanding patient access to DME treatments globally

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.