Global Diagnostic Catheter Market

Market Size in USD Billion

CAGR :

%

USD

4.70 Billion

USD

8.22 Billion

2025

2033

USD

4.70 Billion

USD

8.22 Billion

2025

2033

| 2026 –2033 | |

| USD 4.70 Billion | |

| USD 8.22 Billion | |

| % | |

|

Diagnostic Catheter Market Size

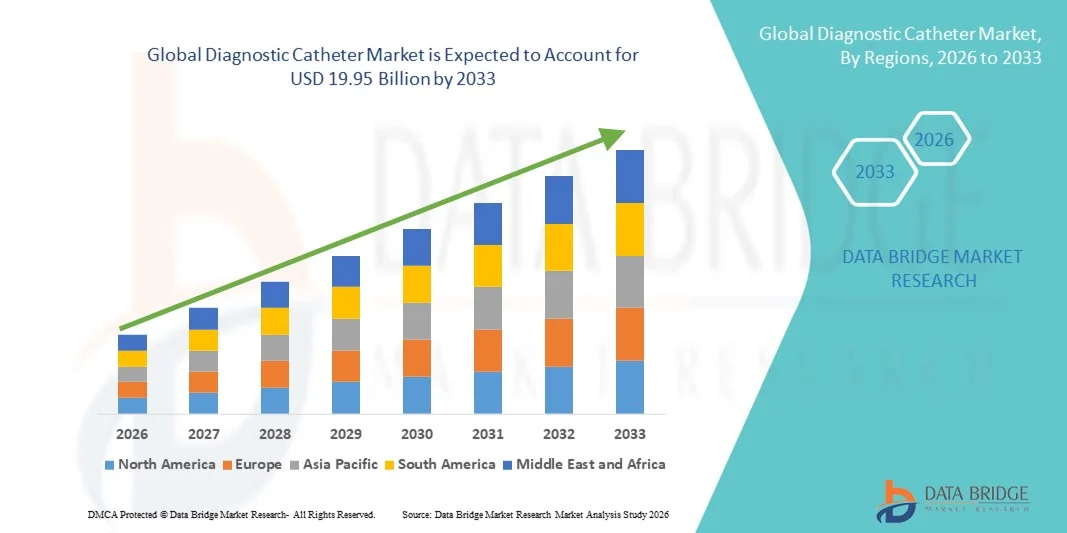

- The global diagnostic catheter market size was valued at USD 4.70 billion in 2025 and is expected to reach USD 8.22 billion by 2033, at a CAGR of 7.25% during the forecast period

- The market growth is largely fueled by the increasing prevalence of cardiovascular and peripheral vascular diseases, along with advancements in minimally invasive diagnostic procedures, driving the demand for precise and efficient catheter-based solutions

- Furthermore, rising adoption of technologically advanced and patient-friendly diagnostic devices in hospitals and ambulatory care settings is strengthening the role of diagnostic catheters as essential tools for early disease detection. These converging factors are accelerating the uptake of diagnostic catheter solutions, thereby significantly boosting the industry's growth

Diagnostic Catheter Market Analysis

- Diagnostic catheters, used for accessing blood vessels and body cavities for imaging, measurement, and monitoring, are increasingly vital components of modern minimally invasive procedures in hospitals and diagnostic centers due to their precision, safety, and compatibility with advanced imaging technologies

- The escalating demand for diagnostic catheters is primarily fueled by the rising prevalence of cardiovascular, neurological, and urological disorders, increasing preference for minimally invasive diagnostics, and growing adoption of technologically advanced, patient-friendly devices

- North America dominated the diagnostic catheter market with the largest revenue share of 38.5% in 2025, characterized by well-established healthcare infrastructure, high incidence of chronic diseases, and strong presence of leading medical device manufacturers, with the U.S. witnessing substantial adoption in cardiac and neurovascular procedures driven by innovations in catheter design and imaging guidance

- Asia-Pacific is expected to be the fastest growing region in the diagnostic catheter market during the forecast period due to rising healthcare expenditure, improving medical infrastructure, and increasing awareness of early disease diagnosis

- Angiography catheters segment dominated the diagnostic catheter market with a market share of 42.9% in 2025, driven by their critical role in visualizing vascular structures and widespread use in cardiology and interventional radiology procedures

Report Scope and Diagnostic Catheter Market Segmentation

|

Attributes |

Diagnostic Catheter Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Diagnostic Catheter Market Trends

Advancements in Imaging-Integrated Catheters

- A significant and accelerating trend in the global diagnostic catheter market is the increasing integration of advanced imaging modalities, such as intravascular ultrasound (IVUS) and optical coherence tomography (OCT), into catheter designs, enhancing procedural precision and real-time visualization

- For instance, OCT catheters enable clinicians to obtain high-resolution images of vessel walls during angiography, allowing for better assessment of lesion morphology and stent placement. Similarly, electrophysiology catheters with integrated mapping systems provide accurate cardiac electrical activity mapping for arrhythmia management

- Imaging integration in diagnostic catheters enables features such as improved accuracy in detecting vascular abnormalities, facilitating early diagnosis, and providing guidance for minimally invasive interventions. For instance, ultrasound catheters can measure blood flow dynamics and pressure gradients in real time, improving clinical decision-making

- The seamless integration of imaging technologies with diagnostic catheters allows physicians to combine multiple diagnostic functions in a single procedure, reducing patient discomfort and procedure time. Through this approach, hospitals can optimize workflow efficiency and enhance patient outcomes

- This trend towards more intelligent, multifunctional, and imaging-enabled catheters is fundamentally reshaping clinician expectations for minimally invasive diagnostics. Consequently, companies such as Abbott and Medtronic are developing catheter systems with combined imaging and pressure monitoring capabilities

- The demand for diagnostic catheters with integrated imaging solutions is growing rapidly across cardiology, neurology, and vascular applications, as hospitals and diagnostic centers increasingly prioritize procedural accuracy and patient safety

Diagnostic Catheter Market Dynamics

Driver

Increasing Prevalence of Cardiovascular and Neurological Disorders

- The rising prevalence of cardiovascular, neurovascular, and peripheral vascular diseases worldwide is a significant driver for the heightened demand for diagnostic catheters

- For instance, in March 2025, Boston Scientific launched a next-generation coronary diagnostic catheter aimed at improving early detection of arterial blockages in high-risk patients. Such advancements by key companies are expected to drive market growth in the forecast period

- As the burden of chronic vascular diseases increases, diagnostic catheters provide minimally invasive solutions for accurate assessment, early diagnosis, and treatment planning, offering a compelling advantage over traditional diagnostic methods

- Furthermore, increasing awareness among physicians and patients about the benefits of minimally invasive diagnostic procedures is encouraging adoption across hospitals and imaging centers, particularly for high-risk patient groups

- The expansion of advanced cardiac and neurovascular catheterization labs, coupled with the availability of training programs for clinicians, is propelling the adoption of diagnostic catheters in both developed and emerging markets

- Rising demand for multifunctional catheters capable of performing both diagnostic and therapeutic interventions is driving market growth, as these devices reduce procedural time and improve patient outcomes

- Government initiatives and funding to improve early diagnosis of chronic and acute diseases are supporting the adoption of diagnostic catheters in public and private healthcare facilities across emerging economies

Restraint/Challenge

Procedure Complexity and Regulatory Compliance Hurdles

- Concerns surrounding procedural complexity, device handling, and regulatory approvals pose a significant challenge to broader adoption of diagnostic catheters. As catheters involve precise manipulation and imaging guidance, clinician skill requirements can limit widespread use

- For instance, high-profile reports of procedural complications with advanced electrophysiology or neurovascular catheters have made some hospitals cautious in adopting new technologies without extensive training and support

- Addressing these challenges through user-friendly designs, robust training programs, and compliance with stringent FDA and CE regulatory standards is crucial for building clinician confidence. Companies such as Terumo and Abbott emphasize their simplified handling mechanisms and comprehensive training support to mitigate adoption barriers

- In addition, the relatively high cost of specialized diagnostic catheters compared to conventional devices can limit procurement in price-sensitive regions or smaller healthcare facilities, slowing market penetration

- Overcoming these challenges through design innovations, clinician education, and streamlined regulatory approvals will be vital for sustained market growth and broader adoption in global healthcare settings

- Limited reimbursement policies and inconsistent insurance coverage for advanced diagnostic catheter procedures can hinder adoption in some regions, affecting market expansion

- Potential risks related to device-associated complications, such as vascular injury or infection, require hospitals to implement strict safety protocols, which may slow the pace of adoption despite technological advancements

Diagnostic Catheter Market Scope

The market is segmented on the basis of product, type, application, and end users.

- By Product

On the basis of product, the diagnostic catheter market is segmented into angiography catheters, electrophysiology catheters, ultrasound catheters, OCT catheters, pressure and hemodynamic monitoring catheters, temperature monitoring catheters, cardiovascular catheters, neurovascular catheters, urological catheters, specialty catheters, and intravenous catheters. The angiography catheters segment dominated the market with the largest market revenue share of 42.9% in 2025, driven by their critical role in visualizing vascular structures and guiding interventional procedures. Hospitals and imaging centers widely adopt angiography catheters for early detection of coronary artery disease, peripheral arterial disease, and other vascular abnormalities. Their compatibility with advanced imaging systems and minimally invasive procedures makes them a preferred choice among cardiologists and interventional radiologists. Continuous innovations, such as low-profile designs and improved radiopacity, have further strengthened their position in the market. In addition, the ability to perform both diagnostic and therapeutic functions using angiography catheters enhances procedural efficiency and patient outcomes.

The electrophysiology catheters segment is anticipated to witness the fastest growth rate of 15.8% from 2026 to 2033, fueled by the rising prevalence of cardiac arrhythmias and increasing adoption of catheter-based ablation procedures. These catheters allow precise mapping and treatment of irregular heart rhythms, offering minimally invasive alternatives to open-heart surgery. Technological advancements, such as integration with 3D mapping and AI-guided navigation, are improving procedural accuracy and safety. Growing awareness among patients and physicians about the benefits of early diagnosis and treatment of arrhythmias is further boosting demand. In addition, rising investments in cardiac care infrastructure, particularly in emerging markets, are supporting the rapid adoption of electrophysiology catheters.

- By Type

On the basis of type, the market is segmented into non-imaging diagnostic catheters and diagnostic imaging catheters. The diagnostic imaging catheter segment dominated the market with the largest market revenue share in 2025, driven by their ability to provide real-time visualization of anatomical structures and vascular conditions. Imaging catheters, including IVUS, OCT, and ultrasound catheters, allow physicians to accurately assess lesion morphology, vessel patency, and procedural outcomes during interventions. Their integration with advanced imaging systems enhances diagnostic precision and reduces procedural risks. Hospitals and diagnostic centers prioritize imaging catheters for complex procedures requiring high-resolution imaging. The adoption of minimally invasive techniques further reinforces the dominance of this segment.

The non-imaging diagnostic catheter segment is expected to witness the fastest CAGR from 2026 to 2033, driven by rising demand for simple, cost-effective solutions for hemodynamic monitoring, pressure measurement, and fluid delivery. These catheters are widely used in routine diagnostic and monitoring procedures across cardiology, urology, and critical care applications. Ease of use, affordability, and compatibility with existing hospital infrastructure contribute to their rapid adoption, particularly in emerging markets. Growing awareness of patient safety and procedural efficiency is also accelerating the uptake of non-imaging catheters.

- By Application

On the basis of application, the market is segmented into gastroenterology, cardiology, urology, neurology, and others. The cardiology segment dominated the market with the largest revenue share in 2025, attributed to the high prevalence of cardiovascular diseases and the critical role of diagnostic catheters in interventional cardiology procedures. Catheters are essential for angiography, electrophysiology studies, and pressure monitoring, enabling accurate diagnosis and treatment planning. The increasing adoption of minimally invasive cardiac procedures and advanced catheter technologies is further boosting demand. Hospitals and specialized cardiac centers are major end users, emphasizing precision, safety, and patient comfort.

The neurology segment is anticipated to witness the fastest growth during the forecast period, driven by rising incidence of neurovascular disorders, such as stroke and aneurysms, and increasing adoption of catheter-based interventions. Neurovascular catheters allow minimally invasive access to cerebral vessels for diagnosis, monitoring, and treatment. Technological innovations, including microcatheter designs and imaging integration, improve procedural success rates. Growing awareness of early detection and intervention for neurological conditions is further accelerating adoption. Expansion of neurointerventional centers in emerging markets also supports rapid growth.

- By End Users

On the basis of end users, the market is segmented into hospitals and imaging & diagnostic centers. The hospitals segment dominated the market with the largest market revenue share in 2025, due to the availability of advanced infrastructure, highly skilled clinicians, and a higher volume of complex diagnostic procedures. Hospitals offer a wide range of interventional and diagnostic services requiring precision catheters, including cardiology, neurology, and vascular procedures. The ability to provide integrated care under one roof encourages the adoption of high-end diagnostic catheters.

The imaging & diagnostic centers segment is expected to witness the fastest growth during the forecast period, driven by the increasing number of standalone diagnostic facilities and outpatient centers offering specialized catheter-based procedures. These centers focus on efficiency, cost-effectiveness, and patient convenience, making them ideal adopters of advanced and minimally invasive catheter technologies. Rising investments in imaging infrastructure and diagnostic services in emerging markets are fueling the rapid growth of this segment.

Diagnostic Catheter Market Regional Analysis

- North America dominated the diagnostic catheter market with the largest revenue share of 38.5% in 2025, characterized by well-established healthcare infrastructure, high incidence of chronic diseases, and strong presence of leading medical device manufacturers

- Hospitals and diagnostic centers in the region prioritize precision, patient safety, and procedural efficiency, increasing demand for advanced angiography, electrophysiology, and imaging-integrated catheters

- This widespread adoption is further supported by strong presence of key medical device manufacturers, high healthcare expenditure, and increasing investments in catheterization labs, establishing diagnostic catheters as essential tools for early diagnosis and intervention in cardiovascular, neurological, and vascular conditions

U.S. Diagnostic Catheter Market Insight

The U.S. diagnostic catheter market captured the largest revenue share of 42% in 2025 within North America, fueled by the high prevalence of cardiovascular and neurovascular diseases and the increasing adoption of minimally invasive diagnostic procedures. Hospitals and specialized cardiac and neurovascular centers prioritize precision, patient safety, and procedural efficiency, driving demand for advanced angiography, electrophysiology, and imaging-integrated catheters. The growing trend of outpatient interventions, catheter-based ablation, and interventional cardiology procedures further propels market growth. Moreover, strong presence of key medical device manufacturers and continuous technological innovations, such as AI-assisted imaging and pressure monitoring, are significantly contributing to the expansion of the U.S. diagnostic catheter market.

Europe Diagnostic Catheter Market Insight

The Europe diagnostic catheter market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the rising prevalence of chronic cardiovascular and neurovascular disorders and increasing demand for minimally invasive procedures. Growth in urbanization, coupled with higher healthcare expenditure and adoption of advanced diagnostic technologies, is fostering the use of diagnostic catheters. European hospitals and diagnostic centers are also adopting imaging-enabled catheters to improve procedural accuracy and patient safety. The market is witnessing significant growth across cardiology, neurology, and vascular applications, with catheters increasingly incorporated into both new interventional facilities and existing healthcare infrastructure.

U.K. Diagnostic Catheter Market Insight

The U.K. diagnostic catheter market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the rising incidence of cardiovascular diseases, increasing investments in advanced catheterization labs, and growing demand for minimally invasive diagnostics. In addition, heightened awareness among physicians and patients regarding early detection and procedural efficiency is encouraging adoption of electrophysiology, angiography, and neurovascular catheters. The U.K.’s robust healthcare infrastructure and growing integration of imaging and monitoring technologies in hospitals and diagnostic centers are expected to continue stimulating market growth.

Germany Diagnostic Catheter Market Insight

The Germany diagnostic catheter market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of cardiovascular and neurovascular health and the adoption of technologically advanced, imaging-enabled catheter systems. Germany’s well-developed healthcare infrastructure, combined with its emphasis on innovation, research, and quality medical care, promotes the adoption of diagnostic catheters in hospitals and specialized intervention centers. The integration of catheters with imaging systems for minimally invasive procedures is also becoming increasingly prevalent, with a strong preference for accurate and patient-safe solutions aligning with local clinical standards.

Asia-Pacific Diagnostic Catheter Market Insight

The Asia-Pacific diagnostic catheter market is poised to grow at the fastest CAGR of 17% during the forecast period of 2026 to 2033, driven by increasing prevalence of cardiovascular and neurovascular disorders, rapid urbanization, and rising healthcare expenditure in countries such as China, Japan, and India. The region’s growing focus on minimally invasive diagnostics and expansion of interventional cardiology and neurology centers are driving adoption of advanced diagnostic catheters. Furthermore, as APAC emerges as a hub for medical device manufacturing and catheter innovations, affordability and accessibility of high-quality catheters are expanding to a wider healthcare provider base.

Japan Diagnostic Catheter Market Insight

The Japan diagnostic catheter market is gaining momentum due to the country’s advanced healthcare infrastructure, high awareness of minimally invasive procedures, and demand for precise diagnostic technologies. Hospitals and cardiac centers in Japan are increasingly adopting imaging-integrated and electrophysiology catheters to improve procedural outcomes and patient safety. Integration with real-time imaging and monitoring systems is fueling growth, while the aging population is driving demand for safer and more efficient catheter-based diagnostics in both residential and hospital-based care.

India Diagnostic Catheter Market Insight

The India diagnostic catheter market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s expanding healthcare infrastructure, increasing prevalence of cardiovascular and neurovascular diseases, and rising adoption of minimally invasive diagnostic procedures. India’s growing number of hospitals, diagnostic centers, and outpatient intervention facilities supports the adoption of advanced catheters. The push toward smart hospitals, rising healthcare expenditure, and availability of cost-effective catheter solutions are key factors propelling the market in India, alongside increasing awareness among physicians and patients about early disease diagnosis and intervention.

Diagnostic Catheter Market Share

The Diagnostic Catheter industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Cook (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Olympus Corporation (Japan)

- Smiths Medical (U.K.)

- NIPRO CORPORATION (Japan)

- B. Braun SE (Germany)

- Edwards Lifesciences Corporation (U.S.)

- Cardinal Health, Inc. (U.S.)

- Merit Medical Systems, Inc. (U.S.)

- AngioDynamics, Inc. (U.S.)

- BIOTRONIK SE & Co. KG (Germany)

- Teleflex Incorporated (U.S.)

- MicroPort Scientific Corporation (China)

- Lepu Medical Technology Co., Ltd. (China)

- Baylis Medical Company Inc. (Canada)

- Conavi Medical (U.S.)

- Endovascular Solutions, Inc. (U.S.)

- Medtronic (U.S.)

- Boston Scientific Corporation (U.S.)

What are the Recent Developments in Global Diagnostic Catheter Market?

- In December 2025, Bendit Technologies announced that the U.S. Food and Drug Administration (FDA) granted 510(k) clearance for its Bendit17™ Microcatheter, described as the smallest steerable microcatheter available. This device enables controlled navigation through complex vascular anatomies both with and without a guidewire, enhancing precision and accessibility in neurovascular and endovascular procedures, and is expected to begin commercial clinical use in the U.S.

- In October 2025, Terumo Interventional Systems announced U.S. FDA 510(k) clearance for its OpusWave imaging system, featuring the DualView imaging catheter that combines optical frequency domain imaging (OFDI) and intravascular ultrasound (IVUS). This system enables comprehensive evaluation of coronary artery disease with simultaneous imaging views, improving diagnostic insights during catheter‑based procedures

- In May 2025, Royal Philips introduced its VeriSight Pro 3D Intracardiac Echocardiography (ICE) catheter in Europe, offering real‑time 2D/3D imaging inside the heart through a miniaturized ultrasound probe at the catheter tip. This innovation helps physicians perform structural heart interventions with greater clarity and without the need for general anesthesia, expanding patient access for complex procedures

- In February 2025, Johnson & Johnson MedTech launched the CEREGLIDE™ 92 Catheter System in the U.S., a next‑generation neurovascular catheter with a large .092” inner diameter and the co‑packaged INNERGLIDE™ 9 delivery aid. It is designed to facilitate distal access and support during acute ischemic stroke procedures, improving navigation of interventional devices during thrombectomy interventions

- In September 2023, MicroVention, Inc., a neurovascular device maker, received FDA 510(k) clearance for its SOFIA™ EX 5F 115 cm Intracranial Support Catheter. This catheter offers enhanced support and trackability for intracranial access, including reinforced design features for improved pushability and kink resistance during complex neurovascular interventions

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.