Global Diaphragm Valves Market

Market Size in USD Billion

USD

6.50 Billion

USD

11.77 Billion

2025

2033

USD

6.50 Billion

USD

11.77 Billion

2025

2033

| 2026 - 2033 | |

| USD 6.50 Billion | |

| USD 11.77 Billion | |

| % | |

|

Diaphragm Valves Market Size

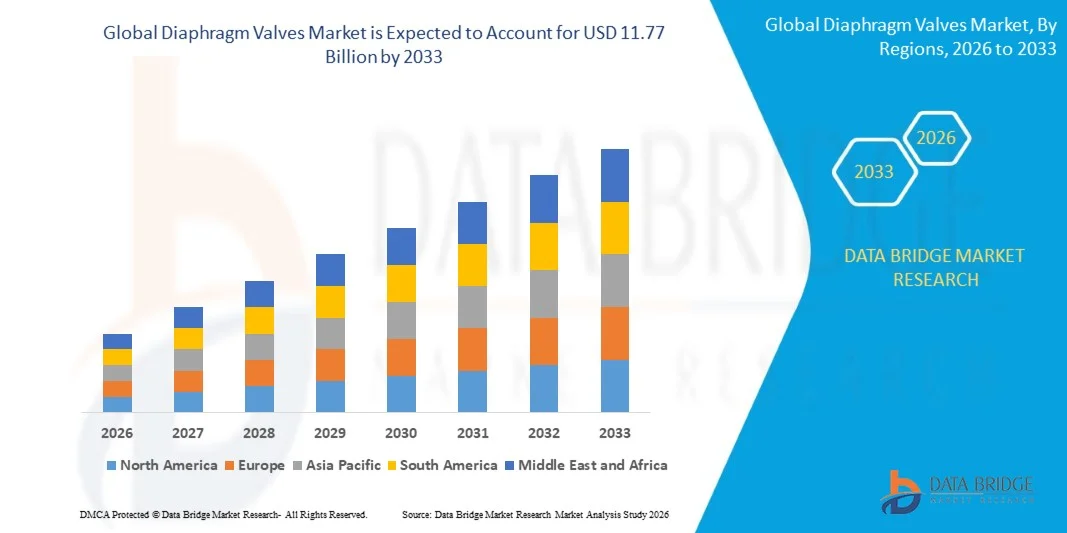

- The global diaphragm valves market size was valued at USD 6.50 billion in 2025 and is expected to reach USD 11.77 billion by 2033, at a CAGR of 7.70% during the forecast period

- The market growth is largely fuelled by the increasing demand from industries such as pharmaceuticals, water and wastewater treatment, food and beverage, and chemicals, where contamination-free and leak-proof flow control is critical for maintaining product quality and safety standards

- Rising investments in water infrastructure projects and stringent environmental regulations are driving the adoption of diaphragm valves for efficient fluid handling and corrosion-resistant operations. In addition, the growing focus on hygienic processing in biopharmaceutical and food industries is further accelerating market expansion

Diaphragm Valves Market Analysis

- The diaphragm valves market is witnessing steady growth due to rising industrial automation and increasing need for precise and reliable flow control solutions across multiple end-use industries

- Expanding applications in sterile processing environments, coupled with advancements in valve materials and design, are enhancing performance, durability, and operational efficiency across critical industrial processes

- North America dominated the diaphragm valves market with the largest revenue share in 2025, driven by strong demand from pharmaceutical, water treatment, and chemical industries, along with increasing adoption of advanced flow control solutions

- Asia-Pacific region is expected to witness the highest growth rate in the global diaphragm valves market, driven by expanding manufacturing activities, increasing infrastructure development, and rising adoption of efficient fluid handling systems across emerging economies

- The Weir segment held the largest market revenue share in 2025 driven by its superior sealing capability, reduced diaphragm wear, and suitability for handling corrosive and viscous fluids. Weir-type valves are widely used in pharmaceutical, water treatment, and chemical applications due to their reliability and longer service life. These valves provide better control over throttling applications and are suitable for handling slurries and semi-solid materials. Their design reduces stress on diaphragms, increasing operational lifespan. Increasing demand for hygienic and maintenance-friendly solutions further strengthens their adoption across industries

Report Scope and Diaphragm Valves Market Segmentation

|

Attributes |

Diaphragm Valves Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• GEMÜ Group (Germany) |

|

Market Opportunities |

• Expansion Of Water And Wastewater Treatment Infrastructure |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Diaphragm Valves Market Trends

“Rising Demand For Hygienic And Corrosion-Resistant Flow Control Solutions”

• The increasing focus on hygienic processing and contamination-free operations is significantly shaping the diaphragm valves market, as industries increasingly require reliable flow control solutions for sensitive applications. Diaphragm valves are gaining traction due to their leak-proof design, corrosion resistance, and suitability for handling aggressive and high-purity fluids. This trend strengthens their adoption across pharmaceuticals, food and beverage, and water treatment industries, encouraging manufacturers to develop advanced valve materials and designs

• Growing awareness regarding environmental safety and regulatory compliance has accelerated the demand for diaphragm valves in water and wastewater treatment applications. Governments and industries are investing in efficient fluid management systems to ensure safe water handling and minimize environmental impact, driving the adoption of corrosion-resistant and durable valve solutions

• Increasing demand for automation and smart process control is influencing purchasing decisions, with manufacturers focusing on integrating diaphragm valves with automated systems and IoT-enabled monitoring technologies. These advancements improve operational efficiency, reduce maintenance requirements, and enhance system reliability across industrial processes

• For instance, in 2024, Georg Fischer in Switzerland and GEMÜ Group in Germany expanded their diaphragm valve product lines for pharmaceutical and water treatment applications, emphasizing high purity, durability, and compliance with stringent industry standards. These developments were introduced to meet rising demand for hygienic and efficient fluid control solutions across global markets

• While demand for diaphragm valves is increasing, sustained market growth depends on continuous innovation in materials, cost-effective manufacturing, and maintaining durability under extreme operating conditions. Manufacturers are also focusing on improving product lifespan, scalability, and integration with automated systems to support broader industrial adoption

Diaphragm Valves Market Dynamics

Driver

“Increasing Demand For Hygienic And Reliable Flow Control Systems”

• Rising demand for contamination-free and leak-proof fluid handling solutions is a major driver for the diaphragm valves market. Industries such as pharmaceuticals, biotechnology, and food processing are increasingly adopting diaphragm valves to ensure product safety, maintain purity standards, and comply with stringent regulatory requirements

• Expanding applications in water and wastewater treatment, chemical processing, and power generation are influencing market growth. Diaphragm valves offer excellent resistance to corrosion and aggressive chemicals, making them suitable for harsh operating environments and critical industrial processes

• Industrial manufacturers are actively promoting advanced diaphragm valve technologies through product innovation, automation integration, and improved material performance. These efforts are supported by the growing need for efficient and reliable process control systems, encouraging partnerships between equipment providers and end users to enhance system performance

• For instance, in 2023, Crane Co. in the U.S. and Alfa Laval in Sweden reported increased adoption of diaphragm valves in pharmaceutical and chemical processing applications, driven by the need for hygienic and high-performance flow control solutions. Both companies emphasized improved efficiency, durability, and regulatory compliance in their product offerings

• Although demand is rising, wider adoption depends on cost optimization, material availability, and technological advancements in valve design. Investment in automation, advanced materials, and supply chain efficiency will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

“High Cost And Maintenance Requirements”

• The relatively high cost of diaphragm valves compared to conventional valve types remains a key challenge, limiting adoption among cost-sensitive industries. Advanced materials, specialized manufacturing processes, and strict quality standards contribute to higher pricing, impacting large-scale deployment

• Maintenance requirements and diaphragm wear over time also present challenges, particularly in high-pressure and high-temperature applications. Frequent replacement of diaphragms can increase operational costs and downtime, affecting overall efficiency

• Supply chain and material sourcing challenges also impact market growth, as diaphragm valves often require high-quality elastomers and corrosion-resistant materials. Fluctuations in raw material availability and costs can influence pricing and production timelines

• For instance, in 2024, manufacturers in Southeast Asia and Latin America reported slower adoption of diaphragm valves in industrial applications due to higher costs and maintenance concerns compared to alternative valve technologies. Limited technical expertise and infrastructure also contributed to reduced market penetration in certain regions

• Overcoming these challenges will require cost-effective production methods, improved material durability, and enhanced maintenance solutions. Collaboration between manufacturers, suppliers, and end users will be essential to improve product efficiency, reduce lifecycle costs, and support long-term market growth

Diaphragm Valves Market Scope

The diaphragm valves market is segmented into eleven notable segments based on type, valve type, controller, end connection, material, size, body material, switch type, usage, distribution channel, and end user.

• By Type

On the basis of type, the diaphragm valves market is segmented into Weir and Straight. The Weir segment held the largest market revenue share in 2025 driven by its superior sealing capability, reduced diaphragm wear, and suitability for handling corrosive and viscous fluids. Weir-type valves are widely used in pharmaceutical, water treatment, and chemical applications due to their reliability and longer service life. These valves provide better control over throttling applications and are suitable for handling slurries and semi-solid materials. Their design reduces stress on diaphragms, increasing operational lifespan. Increasing demand for hygienic and maintenance-friendly solutions further strengthens their adoption across industries.

The Straight segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its ability to provide full bore flow and minimal pressure drop. Straight diaphragm valves are increasingly preferred in applications requiring high flow rates and low resistance, particularly in slurry and bulk fluid handling operations. These valves are suitable for industries requiring uninterrupted flow and efficient fluid transfer. Their simple design supports easy cleaning and maintenance. Growing demand in mining and large-scale water handling applications is further supporting segment growth.

• By Valve Type

On the basis of valve type, the diaphragm valves market is segmented into Two-Way Valve, Forged-T Valve, Multi-Port Valve, Block-T Valve, Tandem Valve, Forged Tank Outlet Valve, Block Tank Outlet Valve, and Others. The Two-Way Valve segment held the largest market revenue share in 2025 driven by its widespread use in basic flow control applications across industries. These valves are simple, cost-effective, and widely deployed in fluid handling systems. They are highly reliable and suitable for a wide range of pressure and temperature conditions. Their easy installation and maintenance further support their widespread adoption. Increasing industrial automation is also driving demand for these valves.

The Multi-Port Valve segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its ability to manage complex flow paths and reduce the need for multiple valves in a system. These valves are increasingly used in biopharmaceutical and chemical processing industries for efficient fluid distribution. They help optimize space and reduce installation costs in complex piping systems. Their ability to support multiple flow directions enhances process efficiency. Growing demand for advanced fluid management systems is accelerating their adoption.

• By Controller

On the basis of controller, the diaphragm valves market is segmented into Manual, Pneumatic, Electric, Hydraulic, and Others. The Pneumatic segment held the largest market revenue share in 2025 driven by its reliability, fast response time, and suitability for automated industrial processes. Pneumatic valves are widely used in process industries where quick and precise control is required. These systems offer high durability and low maintenance in harsh industrial environments. Their compatibility with automated control systems enhances process efficiency. Increasing adoption in chemical and water treatment industries is supporting segment dominance.

The Electric segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of automation and smart control systems. Electric actuated valves offer better precision, remote operation, and integration with digital monitoring systems. They support energy-efficient operations and reduce dependency on compressed air systems. Growing adoption of IoT-enabled industrial solutions is further driving demand. Their ability to provide accurate control in complex systems enhances operational performance.

• By End Connection

On the basis of end connection, the diaphragm valves market is segmented into Flanged, Butt Weld, Tri Clamp, and Others. The Flanged segment held the largest market revenue share in 2025 driven by its ease of installation, strong sealing performance, and widespread use in industrial pipelines. Flanged connections are commonly used in water treatment and chemical industries. They provide reliable connections for high-pressure applications. Their durability and reusability make them suitable for long-term operations. Increasing infrastructure projects are further supporting their demand.

The Tri Clamp segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for hygienic and easy-to-clean connections in food, beverage, and pharmaceutical applications. These connections support quick assembly and disassembly, making them ideal for sanitary environments. They reduce contamination risks and ensure compliance with hygiene standards. Their ease of maintenance improves operational efficiency. Growing demand for sterile processing environments is accelerating adoption.

• By Material

On the basis of material, the diaphragm valves market is segmented into Metal, Rubber, Polytetrafluoroethylene (PTFE), Fluorine Plastic, and Others. The Metal segment held the largest market revenue share in 2025 driven by its high strength, durability, and ability to withstand extreme temperatures and pressures. Metal diaphragm valves are widely used in heavy industrial applications. They offer superior mechanical strength and long service life. Their resistance to harsh operating conditions supports reliability. Increasing demand from power and chemical industries is strengthening segment growth.

The Polytetrafluoroethylene (PTFE) segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its excellent chemical resistance and suitability for handling aggressive fluids. PTFE-based valves are increasingly used in chemical and pharmaceutical industries. They provide non-reactive surfaces suitable for sensitive applications. Their low friction properties improve flow efficiency. Rising demand for corrosion-resistant solutions is driving segment expansion.

• By Size

On the basis of size, the diaphragm valves market is segmented into Below 8”, 8”, 12”, 14”, 16”, 18”, 20” and Others. The Below 8” segment held the largest market revenue share in 2025 driven by its extensive use in small to medium-scale industrial and commercial applications. These valves are commonly used in pipelines requiring precise flow control. They are easy to install and cost-effective for standard operations. Their compact design supports usage in confined spaces. Increasing demand from residential and light industrial sectors is supporting growth.

The 12” segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand in large-scale industrial operations and water infrastructure projects. Larger valve sizes are essential for high-capacity fluid handling systems. They support efficient flow management in large pipelines. Their use in municipal water systems is expanding rapidly. Growing infrastructure development is boosting segment demand.

• By Body Material

On the basis of body material, the diaphragm valves market is segmented into Solid Plastic, Hygiene Valve, Fluorine Plastic and Others. The Solid Plastic segment held the largest market revenue share in 2025 driven by its corrosion resistance, lightweight properties, and cost-effectiveness. These valves are widely used in chemical and water treatment applications. They provide durability in corrosive environments. Their low maintenance requirements support long-term usage. Increasing use in industrial fluid handling is driving demand.

The Hygiene Valve segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for sanitary processing in pharmaceutical and food industries. These valves are designed to meet strict hygiene and safety standards. They ensure contamination-free operations in critical applications. Their compatibility with clean-in-place systems enhances usability. Growing regulatory compliance requirements are supporting adoption.

• By Switch Type

On the basis of switch type, the diaphragm valves market is segmented into Limit Switch, Basic Switches, Indicator Switch and Others. The Limit Switch segment held the largest market revenue share in 2025 driven by its ability to provide accurate position feedback and improve operational safety in automated systems. These switches are widely used in industrial automation setups. They enhance system control and reliability. Their integration with monitoring systems supports process efficiency. Increasing demand for automation is strengthening their usage.

The Indicator Switch segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing need for real-time monitoring and visual status indication in process industries. These switches enhance system visibility and operational efficiency. They provide immediate feedback on valve status. Their role in improving safety and maintenance planning is growing. Adoption in advanced industrial systems is increasing.

• By Usage

On the basis of usage, the diaphragm valves market is segmented into Multi Use and Single Use. The Multi Use segment held the largest market revenue share in 2025 driven by its cost-effectiveness and durability in long-term industrial applications. These valves are widely used across multiple industries for repeated operations. They support continuous processing environments. Their long lifespan reduces replacement frequency. Increasing industrial demand is reinforcing segment dominance.

The Single Use segment is expected to witness the fastest growth rate from 2026 to 2033, driven by growing demand in biopharmaceutical and sterile processing applications. Single-use valves reduce contamination risk and eliminate cleaning requirements. They are ideal for disposable processing systems. Their use improves operational efficiency in sensitive environments. Rising adoption in biotech industries is driving growth.

• By Distribution Channel

On the basis of distribution channel, the diaphragm valves market is segmented into Offline Channel and Online Channel. The Offline Channel segment held the largest market revenue share in 2025 driven by strong presence of distributors, direct sales networks, and industrial supply chains. Offline channels offer technical support and customized solutions for industrial buyers. They enable direct interaction with suppliers. Their reliability in bulk procurement supports dominance. Industrial partnerships further strengthen this segment.

The Online Channel segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing digitalization and ease of product procurement. Online platforms provide quick access to product information, pricing, and supplier comparison. They reduce procurement time and operational costs. Their convenience is attracting small and medium enterprises. Growth of e-commerce platforms is supporting expansion.

• By End User

On the basis of end user, the diaphragm valves market is segmented into Water and Wastewater Treatment, Pharmaceuticals, Chemical, Food and Beverages, Biopharma, Mining and Minerals, Power, Pulp and Paper and Others. The Water and Wastewater Treatment segment held the largest market revenue share in 2025 driven by rising investments in water infrastructure and increasing need for efficient fluid control systems. These valves are widely used for handling corrosive and contaminated fluids. They ensure safe and efficient water management. Their durability supports long-term usage in harsh environments. Growing environmental regulations are driving demand.

The Pharmaceuticals segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for hygienic and contamination-free processing solutions. Diaphragm valves play a critical role in maintaining purity and compliance with stringent regulatory standards in pharmaceutical manufacturing. They support sterile processing and high-quality production. Their integration with automated systems enhances efficiency. Rising global demand for pharmaceutical products is accelerating adoption.

Diaphragm Valves Market Regional Analysis

• North America dominated the diaphragm valves market with the largest revenue share in 2025, driven by strong demand from pharmaceutical, water treatment, and chemical industries, along with increasing adoption of advanced flow control solutions

• Industries in the region highly value the reliability, corrosion resistance, and hygienic properties offered by diaphragm valves, particularly in applications requiring contamination-free fluid handling and strict regulatory compliance

• This widespread adoption is further supported by advanced industrial infrastructure, high investment in automation, and the presence of leading manufacturers, establishing diaphragm valves as a preferred solution across critical processing industries

U.S. Diaphragm Valves Market Insight

The U.S. diaphragm valves market captured the largest revenue share in 2025 within North America, fueled by strong demand from pharmaceutical manufacturing, water infrastructure, and chemical processing industries. Industries are increasingly prioritizing high-performance and contamination-free flow control systems to meet regulatory and safety standards. The growing adoption of automation and smart manufacturing technologies, combined with increasing investments in industrial modernization, further propels the market. Moreover, the presence of key industry players and continuous product innovation is significantly contributing to market expansion.

Europe Diaphragm Valves Market Insight

The Europe diaphragm valves market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent environmental regulations and the rising demand for efficient fluid management systems. Increasing investments in water treatment infrastructure and sustainable industrial practices are fostering market growth. European industries are also focusing on energy efficiency and high-performance valve solutions, leading to increased adoption across multiple sectors. The region is experiencing strong demand in pharmaceutical, chemical, and food processing industries, with diaphragm valves being integrated into both new and upgraded facilities.

U.K. Diaphragm Valves Market Insight

The U.K. diaphragm valves market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing investments in water and wastewater treatment and the growing need for hygienic processing systems. In addition, stringent regulatory requirements and focus on sustainable industrial practices are encouraging the adoption of advanced valve technologies. The country’s strong industrial base and ongoing infrastructure upgrades are expected to continue to stimulate market growth.

Germany Diaphragm Valves Market Insight

The Germany diaphragm valves market is expected to witness the fastest growth rate from 2026 to 2033, fueled by strong industrial manufacturing capabilities and increasing demand for advanced flow control solutions. Germany’s well-developed infrastructure, combined with its focus on engineering excellence and automation, promotes the adoption of diaphragm valves across industrial sectors. The integration of valves with automated systems is also becoming increasingly prevalent, with a strong preference for efficient and high-quality solutions aligning with industry standards.

Asia-Pacific Diaphragm Valves Market Insight

The Asia-Pacific diaphragm valves market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid industrialization, increasing infrastructure development, and rising demand for efficient fluid handling systems in countries such as China, Japan, and India. The region's growing focus on water management, supported by government initiatives, is driving adoption. Furthermore, as APAC emerges as a major manufacturing hub, the affordability and availability of diaphragm valves are expanding to a wider industrial base.

Japan Diaphragm Valves Market Insight

The Japan diaphragm valves market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s advanced industrial base, focus on automation, and demand for high-quality flow control systems. The Japanese market places significant emphasis on precision and reliability, driving adoption across pharmaceutical and electronics industries. The integration of diaphragm valves with automated production systems is fueling growth. Moreover, Japan's focus on innovation and efficiency is supporting increased demand in both industrial and infrastructure applications.

China Diaphragm Valves Market Insight

The China diaphragm valves market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid industrialization, expanding manufacturing sector, and strong investments in infrastructure development. China stands as one of the largest markets for industrial equipment, and diaphragm valves are increasingly used in water treatment, chemical, and power industries. The push towards industrial automation and the presence of strong domestic manufacturers are key factors propelling the market in China.

Diaphragm Valves Market Share

The Diaphragm Valves industry is primarily led by well-established companies, including:

• GEMÜ Group (Germany)

• KDV Flow (U.S.)

• PureValve (U.S.)

• KOSEN VALVE (Japan)

• Gopfert AG (Germany)

• Christian Bürkert GmbH & Co. KG (Germany)

• Century Instrument Company (U.S.)

• ASTECH VALVE CO., LTD. (South Korea)

• Plast-O-Matic Valves, Inc. (U.S.)

• ITT Inc. (U.S.)

• GEA Group Aktiengesellschaft (Germany)

• G.J. Johnson & Sons Ltd. (U.K.)

• GCE Group AB (Sweden)

• International Polymer Solutions (U.S.)

• FLOWONE (India)

• Valves Only (U.A.E.)

• Valvorobica Industriale S.p.A. (Italy)

• Xiamen Kemus Valve Co., Ltd. (China)

• FIP - Formatura Iniezione Polimeri S.p.A. (Italy)

• Aquasyn LLC (U.S.)

• Watson-Marlow Fluid Technology Group (U.K.)

• IPEX Inc. (Canada)

• ALFA LAVAL (Sweden)

• Crane Co. (U.S.)

• NTGD Diaphragm Valve (China)

• SEMON ENGG INDUSTRIES PVT LTD (India)

• NIPPON DAIYA VALVE (Japan)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Diaphragm Valves Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Diaphragm Valves Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Diaphragm Valves Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.