Global Digital Farming Platforms Market

Market Size in USD Billion

USD

8.00 Billion

USD

24.80 Billion

2025

2033

USD

8.00 Billion

USD

24.80 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 8.00 Billion |

Market Size (Forecast Year) |

USD 24.80 Billion |

CAGR |

% |

Major Markets Players |

|

Digital Farming Platforms Market Overview

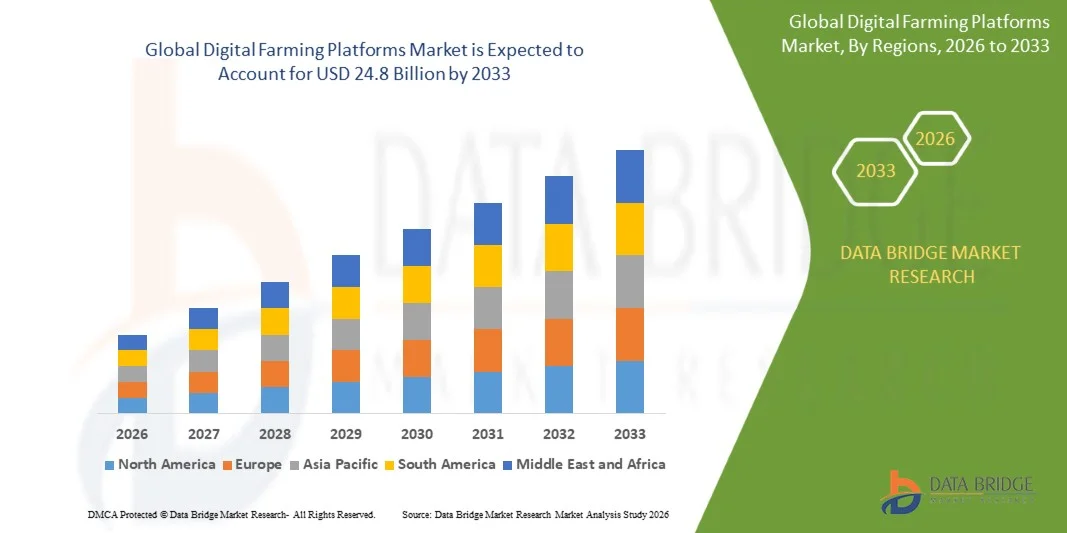

As per Data Bridge Market Research Analysis the global driving simulators market was valued at USD 8 billion in 2025 and is projected to reach USD 24.8 billion by 2033, growing at a CAGR of 15.2% from 2026 to 2033. The market is experiencing robust growth driven by the increasing adoption of precision agriculture technologies, rising demand for data-driven farm management, and continuous advancements in artificial intelligence (AI), Internet of Things (IoT), cloud computing, satellite imagery, drones, and big data analytics. Growing concerns over food security, climate change, water scarcity, labor shortages, and the need to improve agricultural productivity are encouraging farmers and agribusinesses to adopt digital farming platforms that enable real-time crop monitoring, precision irrigation, soil and nutrient management, yield forecasting, and predictive decision-making. Furthermore, supportive government initiatives promoting smart agriculture, expanding digital infrastructure in rural areas, and increasing investments in sustainable farming practices are accelerating the adoption of digital farming platforms across both developed and emerging economies.

Key Market Trends & Insights

- North America dominated the Digital Farming Platforms Market with the largest revenue share in 2025, supported by widespread adoption of precision agriculture technologies, advanced farm mechanization, strong digital infrastructure, and the presence of leading agri-tech solution providers.

- Asia-Pacific is expected to be the fastest-growing regional market during the forecast period of 2026–2033, driven by increasing government support for smart agriculture, rapid digitalization of farming practices, rising adoption of connected farming technologies, and growing investments in agricultural modernization across China, India, Japan, and Australia.

- The Cloud-Based Deployment segment accounted for the largest market share in 2025, owing to its scalability, remote accessibility, real-time data synchronization, and seamless integration with connected farm equipment, sensors, drones, and satellite-based monitoring systems.

- Artificial Intelligence (AI), Machine Learning (ML), and Big Data Analytics represent the fastest-growing technology segment, driven by increasing demand for predictive analytics, crop health monitoring, yield forecasting, disease detection, and automated decision-support systems.

- Crop Monitoring & Precision Farm Management emerged as the leading application segment in 2025, supported by the growing need for real-time field monitoring, optimized input utilization, and improved crop productivity through data-driven farm management.

- Commercial Farms and Agribusiness Enterprises accounted for the largest end-user share, owing to higher investment capacity, increasing adoption of digital technologies, and the need to improve operational efficiency, sustainability, and profitability.

- Integration of IoT-enabled sensors, drones, GPS/GNSS, GIS, and remote sensing technologies is becoming a key market trend, enabling farmers to monitor field conditions in real time, optimize irrigation and fertilizer application, and improve overall farm productivity through precision agriculture practices.

Market Size & Forecast

- Global Market Value (2025): USD 8 Billion

- Expected Market Value (2033): USD 24.8 Billion

- Forecast CAGR (2026–2033): 15.20%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Digital Farming Platforms Market

|

Attributes |

Driving Simulators Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Deere & Company (U.S.) · Kubota Corporation (Japan) · CNH Industrial N.V. (U.K.) · Hexagon AB (Sweden) · Topcon Corporation (Japan) · CLAAS KGaA mbH (Germany) · Trimble (U.S.) · AGCO Corporation (U.S.) · AgEagle Aerial Systems (U.S.) · Bayer AG (Germany) · IBM Corporation (U.S.) |

|

Market Opportunities |

· Expansion of AI-Powered Decision Support Systems · Growing Demand for Cloud-Based Farm Management Platforms · Integration with Carbon Farming and Sustainability Programs |

|

Value Added Data Infosets |

In addition to insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by Data Bridge Market Research also provide in-depth expert analysis of digital agriculture trends, precision farming technology adoption, farm connectivity infrastructure, and regulatory developments supporting smart agriculture. The reports further include geographically mapped company-wise platform deployments and technological capabilities, ecosystem analysis of technology providers, agritech partners and distribution networks, detailed pricing trend analysis for digital farming solutions, and comprehensive assessments of the agricultural value chain, including demand-supply dynamics, farm input optimization, crop monitoring technologies, data integration frameworks, and digital agriculture adoption across key farming regions. |

Digital Farming Platforms Market Trends

Trend: Integration of Artificial Intelligence (AI) and Predictive Analytics

Artificial intelligence (AI) is transforming digital farming platforms by enabling predictive and prescriptive decision-making across agricultural operations. Advanced AI algorithms analyze data collected from sensors, drones, satellites, weather stations, and farm equipment to generate real-time insights on crop health, pest and disease outbreaks, irrigation scheduling, nutrient management, and yield forecasting. The integration of machine learning models is helping farmers optimize input usage, improve productivity, reduce operational costs, and minimize environmental impact. As agriculture becomes increasingly data-driven, AI-powered digital farming platforms are evolving into comprehensive farm management solutions that support precision agriculture and sustainable farming practices. The growing investment in AI-enabled agriculture technologies by leading agri-tech companies and governments is expected to further accelerate innovation and market growth throughout the forecast period.

Digital Farming Platforms Market Dynamics

Key Market Driver: Rising Adoption of Precision Agriculture and Data-Driven Farm Management

The growing need to improve agricultural productivity while optimizing the use of resources is a major driver of the digital farming platforms market. Farmers are increasingly adopting precision agriculture technologies to make data-driven decisions regarding irrigation, fertilization, crop protection, and harvesting. Digital farming platforms integrate AI, IoT, satellite imagery, drones, GPS/GNSS, and cloud analytics to provide real-time insights that improve crop yields, reduce input costs, and promote sustainable farming practices. Governments across several countries are also supporting the adoption of smart farming technologies through funding programs and digital agriculture initiatives, further accelerating market growth.

Key Restraint/Challenge: High Implementation Cost and Digital Infrastructure Limitations

Despite increasing adoption, the high upfront cost associated with precision agriculture equipment, IoT sensors, drones, GPS systems, and subscription-based digital farming platforms remains a significant barrier, particularly for small and medium-sized farms. Additionally, limited internet connectivity, inadequate digital infrastructure, and low digital literacy in several developing regions restrict the effective implementation of cloud-based farming platforms. Interoperability issues between equipment from different manufacturers further complicate digital integration and slow market penetration.

In September 2024, Bayer AG reported that 62% of farmers identified investment requirements as a major barrier to adopting digital farming technologies, while 56% cited digital skill gaps and 47% pointed to technology availability as key challenges.

Key Market Opportunity: Expansion of AI-Enabled Digital Farming Platforms and Connected Farm Ecosystems

Growing demand for AI-powered analytics, cloud-based farm management, and connected agricultural ecosystems is creating significant opportunities for digital farming platform providers. The integration of predictive analytics, autonomous equipment, satellite imagery, and digital twins is enabling farmers to improve operational efficiency, optimize resource utilization, and support climate-smart agriculture. Increasing investments in platform interoperability and mixed-fleet connectivity are expected to further accelerate market growth.

Digital Farming Platforms Market Scope

The digital Farming Platforms is segmented on the basis of Infrastructure, Technology, Product and application.

- By Infrastructure Type

On the basis of infrastructure, the Digital Farming Platforms Market is segmented into Sensing & Monitoring, Communication Technology, Cloud & Data Processing, Telematics/Positioning, and End-Use Components. The Cloud & Data Processing segment dominated the market in 2025 owing to the increasing adoption of cloud-based farm management platforms that enable real-time data storage, analytics, and remote access across multiple agricultural operations. The growing integration of data collected from IoT sensors, drones, satellite imagery, and connected agricultural equipment has further strengthened demand for cloud-based platforms capable of supporting precision agriculture and data-driven decision-making.

The Sensing & Monitoring segment is expected to witness the fastest growth during the forecast period of 2026 to 2033, driven by the increasing deployment of smart sensors, cameras, and remote monitoring technologies for continuous crop health assessment, soil moisture monitoring, pest detection, and environmental condition analysis. Growing investments in precision farming and smart agriculture are accelerating the adoption of advanced sensing technologies across commercial farming operations.

- By Technology Type

On the basis of technology, the Digital Farming Platforms Market is segmented into Artificial Intelligence (AI), Machine Learning (ML) & Natural Language Processing (NLP), Internet of Things (IoT), Blockchain, and Big Data & Analytics. The Internet of Things (IoT) segment accounted for the largest market share in 2025 due to the widespread deployment of connected sensors, GPS-enabled machinery, weather stations, drones, and automated irrigation systems that facilitate real-time farm monitoring and operational efficiency. IoT serves as the foundation for digital farming platforms by enabling seamless collection and transmission of field data.

The Artificial Intelligence (AI), Machine Learning (ML) & Natural Language Processing (NLP) segment is projected to register the fastest growth during the forecast period, supported by increasing adoption of predictive analytics for yield forecasting, disease detection, crop monitoring, precision spraying, and autonomous farm operations. Continuous advancements in AI-powered decision support systems are enabling farmers to improve productivity while optimizing resource utilization.

- By Product Type

On the basis of product, the Digital Farming Platforms Market is segmented into Agricultural Equipment and Drones, Robots & Unmanned Aerial Vehicles (UAVs). The Agricultural Equipment segment dominated the market in 2025 owing to the increasing adoption of connected tractors, harvesters, precision seeders, sprayers, and GPS-guided machinery integrated with digital farming platforms. Modern agricultural equipment equipped with telematics and precision guidance technologies is enabling farmers to improve operational efficiency, reduce input waste, and maximize crop productivity.

The Drones, Robots & Unmanned Aerial Vehicles (UAVs) segment is anticipated to experience the fastest growth during the forecast period, driven by growing demand for aerial crop monitoring, field mapping, precision spraying, livestock monitoring, and automated farm inspection. Advances in drone imaging, artificial intelligence, and remote sensing technologies are expanding the application of UAVs in precision agriculture.

- By Application

On the basis of application, the Digital Farming Platforms Market is segmented into Yield Monitoring & Mapping, Smart Crop Monitoring, Soil & Fertilizer Management, Smart Irrigation Monitoring Systems, Weather Forecasting, and Others (Farm Labor Management and Inventory Management). The Smart Crop Monitoring segment dominated the market in 2025 due to increasing adoption of digital technologies that provide real-time crop health analysis, pest and disease detection, nutrient deficiency assessment, and growth monitoring through satellite imagery, drones, and IoT-enabled sensors. Rising demand for precision agriculture and sustainable farming practices continues to support the widespread implementation of crop monitoring platforms.

The Smart Irrigation Monitoring Systems segment is expected to witness the fastest growth during the forecast period of 2026 to 2033, driven by increasing concerns over water scarcity, growing adoption of precision irrigation technologies, and government initiatives promoting efficient water resource management. The integration of IoT sensors, weather forecasting tools, and AI-based irrigation scheduling is enabling farmers to optimize water consumption while improving crop yield and reducing operational costs.

Digital Farming Platforms Market Regional Analysis

North America held a 37.9% share of the digital agriculture market in 2025, supported by the presence of large-scale farms, a high level of farm mechanization, and consistent funding from programs such as the United States Department of Agriculture’s Climate-Smart Commodity Program. Increasing regulatory pressure on herbicide usage by the Environmental Protection Agency is further driving the adoption of precision spraying solutions. In addition, the Food and Drug Administration’s livestock traceability requirements are encouraging the use of advanced record-keeping and monitoring software. Similar technological progress is also being observed in Canada’s prairie grain farming systems, while Mexico is gradually advancing in the same direction through modernization initiatives.

Asia Pacific Digital Farming Platforms Market Insight

Asia Pacific accounted for a significant share of the global market, valued at USD 6.26 billion in 2025, representing 21.80% of the total, and is projected to rise to USD 7.3 billion in 2026. The region is also expected to record the fastest growth during the forecast period, driven by the early-stage adoption of digital farming technologies and increasing policy-level support aimed at improving agricultural productivity, particularly in countries such as India and Japan.

Country-level growth trends further highlight this expansion: Japan is projected to reach USD 2.12 billion by 2026, China is expected to reach USD 2.52 billion, and India is forecast to attain USD 1.47 billion in the same period. In India, government-led initiatives are promoting the use of advanced technologies such as blockchain, cloud computing, drones, remote sensing, Geographic Information Systems (GIS), and robotics under a digital agriculture mission spanning 2021–2025.

Europe Pacific Digital Farming Platforms Market Insight

Europe accounted for 24.30% of the global market in 2025, generating revenue of USD 7.16 billion, and is projected to reach USD 8.14 billion in 2026. The region is expected to witness steady growth over the forecast period, supported by strong adoption of digital farming practices across key countries such as Germany, the U.K., the Netherlands, and Spain.

Growth in the region is further reinforced by European Union initiatives aimed at promoting advanced agricultural technologies. Programs such as the LIFE GAIA Sense project provide funding support for the deployment of smart farming solutions, including the installation of sensors to monitor soil moisture, pest activity, and crop health, thereby improving farm-level decision-making and productivity.

At the country level, the U.K. market is projected to reach USD 1.49 billion by 2026, while Germany is expected to reach USD 1.41 billion in the same period. Additionally, rising concerns related to climate change and its impact on agricultural output are accelerating the adoption of technology-driven farming solutions across the region.

Digital Farming Platforms Market Share

The driving simulators industry is primarily led by well-established companies, including:

- Deere & Company (U.S.)

- Kubota Corporation (Japan)

- CNH Industrial N.V. (U.K.)

- Hexagon AB (Sweden)

- Topcon Corporation (Japan)

- CLAAS KGaA mbH (Germany)

- Trimble (U.S.)

- AGCO Corporation (U.S.)

- AgEagle Aerial Systems (U.S.)

- Bayer AG (Germany)

- IBM Corporation (U.S.)

Latest Developments in Digital Farming Platforms Market

- In November 2025, Syngenta expanded its digital agriculture ecosystem by integrating AI-driven agronomic models and satellite-based crop monitoring capabilities into its Cropwise platform. The upgrade strengthens real-time decision-making for farmers by combining remote sensing data with predictive analytics to improve yield optimization and input efficiency.

- In June 2026, A new AI collaboration between ANNAM.AI (IIT Ropar) and Syngenta was launched to deploy climate-smart agricultural solutions in India. The initiative focuses on using artificial intelligence for crop health monitoring, pest detection, and heat-stress management, supporting data-driven farming practices in emerging markets.

- December 2025, The OpenAgri Project and the AgStack Foundation entered into a strategic partnership to integrate OpenAgri’s open-source software solutions into AgStack’s digital infrastructure. The collaboration focuses on reducing system fragmentation and vendor lock-in while enhancing interoperability and scalability across digital agriculture ecosystems.

- November 2025, Land O’Lakes and Microsoft formed a strategic alliance to accelerate AI-driven transformation in agriculture. The partnership combines Land O’Lakes’ rich agricultural datasets with Microsoft’s cloud computing and AI capabilities to improve farm productivity, operational efficiency, and sustainability.

- November 2025, Syngenta Group launched the Cropwise Open Platform, opening its core digital agriculture infrastructure to third-party developers. This initiative aims to bridge the technology gap in farming by expanding access to advanced digital tools, particularly for small and medium-scale farmers.

- November 2024, Microsoft Corporation expanded its artificial intelligence portfolio by introducing industry-specific AI models tailored for agriculture and related sectors. These solutions are designed to enhance precision farming through improved crop monitoring, predictive analytics, and resource optimization.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.