Global Digital Insurance Platform Market

Market Size in USD Billion

CAGR :

%

USD

170.55 Billion

USD

476.36 Billion

2025

2033

USD

170.55 Billion

USD

476.36 Billion

2025

2033

| 2026 –2033 | |

| USD 170.55 Billion | |

| USD 476.36 Billion | |

| % | |

|

What is the Global Digital Insurance Platform Market Size and Growth Rate?

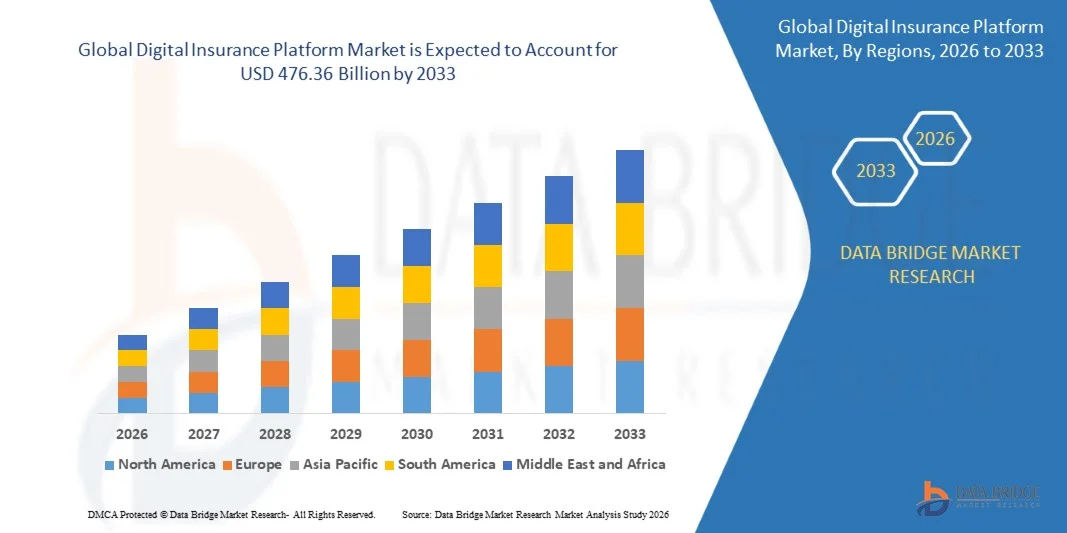

- The global digital insurance platform market size was valued at USD 170.55 billion in 2025 and is expected to reach USD 476.36 billion by 2033, at a CAGR of 13.7% during the forecast period

- The digital insurance platform market is being driven by the rising adoption of IoT products. The upsurge in the adoption rate of underwater acoustic modems in naval defense is a major factor driving the market's growth. The changing insurer’s focus from product-based to consumer-centric strategies is driving up demand for digital insurance platform equipment market

What are the Major Takeaways of Digital Insurance Platform Market?

- Rising awareness amongst insurers towards digital channels, and technological advancement will cushion the growth rate of digital insurance platform market. Furthermore, upsurge in the adoption rate of cloud-based digital solutions by the insurers to obtain the high scalability will accelerate the growth rate of digital insurance platform market for the forecast period mentioned above

- Moreover, increasing awareness amongst insurers to access a broader segment of the market and emerging new markets will boost the beneficial opportunities for the digital insurance platform market growth

- North America dominated the digital insurance platform market with a 38.0% revenue share in 2025, driven by early adoption of cloud-native insurance platforms, strong InsurTech ecosystems, and rapid digital transformation initiatives across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 20.3% from 2026 to 2033, driven by rapid digital transformation, increasing insurance penetration, and rising smartphone and internet adoption across China, India, Japan, South Korea, and Southeast Asia

- The Tools segment dominated the market with a 61.7% share in 2025, as it remains the core element for policy administration, underwriting automation, claims management, fraud analytics, CRM integration, and customer engagement workflows

Report Scope and Digital Insurance Platform Market Segmentation

|

Attributes |

Digital Insurance Platform Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Digital Insurance Platform Market?

“Increasing Shift Toward AI-Driven, Cloud-Native, and Customer-Centric Insurance Platforms”

- The digital insurance platform market is witnessing strong adoption of cloud-based, AI-enabled, and API-driven platforms designed to support policy administration, underwriting, claims processing, and omnichannel customer engagement across life, health, and general insurance segments

- Market players are introducing modular, low-code, and SaaS-based insurance solutions that offer seamless integration with CRM systems, analytics tools, payment gateways, and third-party InsurTech ecosystems

- Growing demand for digital self-service portals, mobile policy management, and automated claims settlement is driving adoption across insurers, brokers, and third-party administrators

- For instance, companies such as IBM, Oracle, SAP, Accenture, and Infosys are enhancing their insurance platforms with AI-powered underwriting, fraud detection, and real-time customer service capabilities

- Increasing need for personalized policy recommendations, faster claim approvals, and regulatory compliance automation is accelerating the shift toward intelligent digital insurance ecosystems

- As insurers continue to modernize legacy systems and improve customer experience, Digital Insurance Platforms will remain vital for operational efficiency, policy lifecycle management, and digital transformation initiatives

What are the Key Drivers of Digital Insurance Platform Market?

- Rising demand for streamlined policy issuance, automated underwriting, and faster claims processing is one of the major drivers supporting market expansion

- For instance, in 2025–2026, leading companies expanded their digital insurance capabilities through AI integration, cloud migration, and API-based platform modernization

- Growing adoption of InsurTech solutions, mobile insurance apps, embedded insurance, and digital customer onboarding is boosting demand across the U.S., Europe, and Asia-Pacific

- Advancements in machine learning, predictive analytics, fraud detection engines, and robotic process automation (RPA) have strengthened platform efficiency and decision-making

- Rising use of AI-based risk scoring, usage-based insurance models, and connected ecosystem platforms is creating strong growth opportunities

- Supported by steady investments in financial services digitization, cybersecurity, and customer experience transformation, the digital insurance platform market is expected to witness strong long-term growth

Which Factor is Challenging the Growth of the Digital Insurance Platform Market?

- High costs associated with legacy system modernization, cloud migration, and enterprise-wide software implementation restrict adoption among small and mid-sized insurers

- For instance, during 2024–2025, rising cybersecurity risks, compliance costs, and complex integration requirements increased deployment expenses for several insurers

- Complexity in managing data privacy, regulatory compliance, and multi-channel customer interactions increases the need for skilled IT and insurance professionals

- Limited digital maturity among traditional insurers and emerging markets slows adoption

- Competition from in-house software systems, InsurTech startups, and legacy core insurance vendors creates pricing pressure and reduces product differentiation

- To address these issues, companies are focusing on cloud-native platforms, AI automation, low-code development, and stronger cybersecurity frameworks to increase global adoption of Digital Insurance Platforms

How is the Digital Insurance Platform Market Segmented?

The market is segmented on the basis of component, end-user, insurance application, deployment type, and organization size.

• By Component

On the basis of component, the Digital Insurance Platform market is segmented into Tools and Services. The Tools segment dominated the market with a 61.7% share in 2025, as it remains the core element for policy administration, underwriting automation, claims management, fraud analytics, CRM integration, and customer engagement workflows. These platforms provide insurers with centralized dashboards, AI-driven decision support, workflow automation, and omnichannel communication capabilities, making them essential for digital transformation initiatives. Increasing adoption of cloud-native software, low-code insurance suites, and API-enabled ecosystems continues to strengthen segment dominance across global insurers.

The Services segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by rising demand for implementation, consulting, managed services, system integration, migration support, and post-deployment optimization. As insurers modernize legacy infrastructure and adopt AI-enabled solutions, demand for professional services is expected to accelerate significantly.

• By End-User

On the basis of end-user, the market is segmented into Insurance Companies, Third-Party Administrators and Brokers, and Aggregators. The Insurance Companies segment dominated the market with a 48.9% share in 2025, supported by increasing investments in claims automation, policy lifecycle management, customer onboarding, and digital underwriting solutions. Large insurers are actively adopting digital insurance platforms to improve operational efficiency, reduce claim settlement time, and enhance customer retention through personalized offerings. The growing focus on customer experience, fraud prevention, and compliance management further supports strong segment leadership.

The Aggregators segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising consumer preference for digital comparison platforms, instant premium quotations, and seamless policy purchase journeys. Increased use of embedded insurance models and mobile-first insurance marketplaces is expected to drive rapid expansion in this segment.

• By Insurance Application

On the basis of insurance application, the market is segmented into Automotive and Transportation, Home and Commercial Buildings, Life and Health, Business and Enterprise, Consumer Electronics and Industrial Machines, and Travel. The Life and Health segment dominated the market with a 34.6% share in 2025, driven by growing demand for digital claims processing, health policy management, telehealth integration, and automated underwriting solutions. Increasing healthcare digitization, rising insurance penetration, and higher demand for personalized health coverage plans continue to strengthen segment growth.

The Travel segment is expected to grow at the fastest CAGR from 2026 to 2033, propelled by increasing global travel activity, digital policy issuance, instant claims settlement, and mobile-based travel insurance solutions. Growing consumer preference for app-based insurance purchases and real-time coverage activation is accelerating adoption.

• By Deployment Type

On the basis of deployment type, the market is segmented into On-Premises and Cloud. The Cloud segment dominated the market with a 57.8% share in 2025, owing to its scalability, lower infrastructure costs, faster deployment, and seamless integration capabilities. Cloud-based insurance platforms enable real-time analytics, remote access, automated updates, and improved disaster recovery, making them highly preferred among insurers undergoing digital transformation. Rising adoption of SaaS-based insurance core systems continues to strengthen this segment.

The Cloud segment is also projected to grow at the fastest CAGR from 2026 to 2033, driven by growing demand for flexible deployment models, cost optimization, and AI-powered insurance workflows.

• By Organization Size

On the basis of organization size, the market is segmented into Large Enterprises and Small and Medium-Sized Enterprises. The Large Enterprises segment dominated the market with a 63.2% share in 2025, driven by strong IT budgets, large customer bases, and higher investments in advanced digital transformation initiatives. Large insurers are rapidly deploying AI, automation, and analytics-driven platforms to streamline operations and improve policyholder experience.

The Small and Medium-Sized Enterprises segment is expected to grow at the fastest CAGR from 2026 to 2033, supported by increasing adoption of cloud-based subscription models, low-code platforms, and cost-efficient digital insurance tools that reduce entry barriers for smaller firms.

Which Region Holds the Largest Share of the Digital Insurance Platform Market?

- North America dominated the digital insurance platform market with a 38.0% revenue share in 2025, driven by early adoption of cloud-native insurance platforms, strong InsurTech ecosystems, and rapid digital transformation initiatives across the U.S. and Canada. The region benefits from a mature insurance industry, widespread use of AI-driven underwriting, claims automation, fraud detection systems, and customer experience platforms. Increasing investments in policy administration modernization, embedded insurance solutions, and digital claims settlement continue to strengthen regional leadership

- Leading companies in North America are introducing advanced digital insurance solutions with AI-powered risk analytics, blockchain-based claims verification, omnichannel customer engagement tools, and cloud-based policy management systems, strengthening the region’s technological advantage. Continuous investment in InsurTech, cybersecurity, and regulatory compliance platforms supports long-term market expansion

- High concentration of insurance carriers, strong digital infrastructure, and sustained investment in customer-centric platforms further reinforce regional market leadership

U.S. Digital Insurance Platform Market Insight

The U.S. is the largest contributor in North America, supported by the presence of major insurers, InsurTech startups, and leading technology providers. Increasing deployment of AI-based underwriting engines, automated claims workflows, predictive risk assessment tools, and customer self-service portals continues to drive market growth. Rising demand for usage-based insurance, embedded insurance, and digital-first customer experiences further intensifies adoption across life, health, property, and automotive insurance sectors. Strong regulatory frameworks and high enterprise IT spending continue to accelerate digital insurance platform penetration.

Canada Digital Insurance Platform Market Insight

Canada contributes significantly to regional growth, driven by expanding adoption of cloud insurance platforms, digital broker ecosystems, and automated policy servicing solutions. Rising investments in financial technology, data security frameworks, and AI-driven claims processing support steady market expansion. Insurance providers are increasingly leveraging digital platforms to improve customer engagement, reduce claim turnaround times, and strengthen fraud prevention capabilities.

Asia-Pacific Digital Insurance Platform Market

Asia-Pacific is projected to register the fastest CAGR of 20.3% from 2026 to 2033, driven by rapid digital transformation, increasing insurance penetration, and rising smartphone and internet adoption across China, India, Japan, South Korea, and Southeast Asia. Growing middle-class populations, strong demand for affordable digital insurance products, and rapid expansion of mobile-first insurance ecosystems continue to accelerate market growth. Increasing use of AI-enabled customer onboarding, digital payments, and embedded insurance models is further driving demand across the region.

China Digital Insurance Platform Market Insight

China is the largest contributor to Asia-Pacific due to strong digital infrastructure, rapid InsurTech expansion, and widespread adoption of app-based financial services. Rising demand for mobile insurance products, AI-powered claims systems, and super-app insurance integrations continues to strengthen market growth.

Japan Digital Insurance Platform Market Insight

Japan shows steady growth supported by advanced financial services digitization, strong regulatory compliance systems, and growing adoption of AI-driven insurance platforms. Increasing focus on aging population insurance products and health-tech integration supports long-term expansion.

India Digital Insurance Platform Market Insight

India is emerging as a major growth hub, driven by rapid digital payments adoption, expanding InsurTech startups, and government-backed financial inclusion initiatives. Rising demand for digital health, life, and motor insurance solutions is accelerating market penetration.

South Korea Digital Insurance Platform Market Insight

South Korea contributes significantly due to strong fintech infrastructure, advanced mobile ecosystems, and increasing adoption of AI-driven insurance automation tools. Technological innovation and high digital literacy continue to support sustained market growth.

Which are the Top Companies in Digital Insurance Platform Market?

The digital insurance platform industry is primarily led by well-established companies, including:

- Tata Consultancy Services Limited (India)

- DXC Technology Company (U.S.)

- Infosys Limited (India)

- Pegasystems Inc. (U.S.)

- Appian (U.S.)

- Mindtree Ltd. (India)

- Prima Solutions (France)

- FINEOS (Ireland)

- Cognizant (U.S.)

- Inzura Limited (U.K.)

- Cogitate Technology Solutions, Inc. (U.S.)

- Duck Creek Technologies (U.S.)

- Bolt Solutions (U.S.)

- Majesco (U.S.)

- EIS Group (U.S.)

- iPipeline, Inc. (U.S.)

- Vertafore, Inc. (U.S.)

- eBaoTech Corporation (China)

- IBM (U.S.)

- Microsoft (U.S.)

- Accenture (Ireland)

- Oracle (U.S.)

- SAP SE (Germany)

What are the Recent Developments in Global Digital Insurance Platform Market?

- In August 2025, AXA partnered with MOTOGO to launch typhoon parametric and cross-border travel insurance products, expanding parametric insurance adoption into specialized risk segments and strengthening innovation in travel coverage

- In July 2025, Munich Re completed its USD 2.6 billion acquisition of NEXT Insurance, marking the largest insurtech P&C deal to date and reinforcing its leadership in digital insurance solutions

- In June 2025, Willis Towers Watson launched Zest Insurance targeting Australia’s USD 9 billion SME sector through a digital-first platform, driving adoption of cloud-based insurance solutions for small businesses

- In April 2025, Zopper secured USD 121 million in funding to expand its insurance-infrastructure APIs, accelerating platform integration and supporting scalable digital insurance offerings

- In March 2025, Liberty Specialty Markets and Baobab Insurance introduced e-crime coverage for SMEs up to EUR 5 million to combat deepfake and cyber fraud, enhancing digital protection for small enterprises

- In December 2024, YAS and QBE Hong Kong unveiled “Pay-As-You-Sell” liability insurance for e-commerce merchants leveraging real-time sales data, driving innovation in usage-based insurance models

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.