Global Digital Pathology Hardware Systems Market

Market Size in USD Billion

USD

1.74 Billion

USD

5.94 Billion

2025

2033

USD

1.74 Billion

USD

5.94 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 1.74 Billion |

Market Size (Forecast Year) |

USD 5.94 Billion |

CAGR |

% |

Major Markets Players |

|

Digital Pathology Hardware Systems Market Size

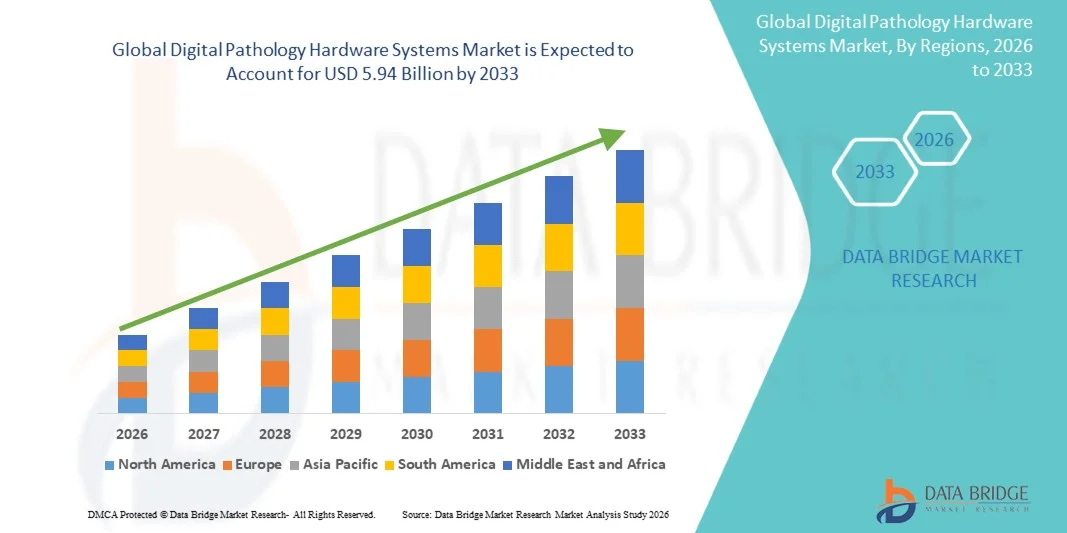

- The global digital pathology hardware systems market size was valued at USD 1.74 billion in 2025 and is expected to reach USD 5.94 billion by 2033, at a CAGR of 16.60% during the forecast period

- The market growth is largely fueled by the increasing adoption of digital pathology solutions across hospitals, diagnostic laboratories, and research institutions, driven by the need for faster, more accurate, and remote-enabled pathology workflows, along with advancements in whole slide imaging systems and high-resolution scanning hardware

- Furthermore, rising demand for automation in laboratory diagnostics, growing integration of artificial intelligence and cloud-enabled infrastructure, and the shift toward digitization of healthcare systems are establishing digital pathology hardware as a critical component of modern diagnostic ecosystems, thereby accelerating the overall market expansion

Digital Pathology Hardware Systems Market Analysis

- Digital pathology hardware systems, including whole slide imaging scanners, high-resolution imaging cameras, workstations, and storage/networking devices, are increasingly vital components of modern diagnostic and research workflows in hospitals, diagnostic labs, and academic institutions due to their ability to enable high-throughput slide digitization, remote consultation, and seamless integration with advanced analytical and AI-enabled tools

- The escalating demand for digital pathology hardware is primarily fueled by the growing adoption of digital pathology solutions across clinical and research settings, rising cancer incidence, increasing need for accurate and efficient diagnostics, and the integration of artificial intelligence and cloud-based infrastructure into pathology workflows

- North America dominated the digital pathology hardware systems market with the largest revenue share of 42.7% in 2025, driven by early adoption of advanced healthcare technologies, strong digital infrastructure, high healthcare expenditure, and the presence of key market players, with the U.S. witnessing substantial deployments of whole slide imaging systems and digital scanners across hospitals and reference laboratories

- Asia-Pacific is expected to be the fastest growing region in the digital pathology hardware systems market during the forecast period due to expanding healthcare infrastructure, rising healthcare investments, increasing patient population, and growing awareness of digital diagnostics technologies

- The Whole Slide Imaging (WSI) Systems segment dominated the digital pathology hardware systems market with a market share of 47.2% in 2025, propelled by its capability to capture high-resolution digital images of entire tissue slides, enabling efficient storage, sharing, and detailed analysis in both clinical diagnostics and research applications

Report Scope and Digital Pathology Hardware Systems Market Segmentation

|

Attributes |

Digital Pathology Hardware Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Digital Pathology Hardware Systems Market Trends

“Advancements in AI-Integrated Imaging and Cloud Connectivity”

- A significant and accelerating trend in the global digital pathology hardware systems market is the growing integration of artificial intelligence (AI) with whole slide imaging systems and scanners, alongside increasing adoption of cloud-connected platforms that enhance image storage, sharing, and collaborative diagnostics across multiple locations

- For instance, leading digital pathology systems are being deployed with AI-enabled image analysis capabilities that assist pathologists in detecting abnormalities, classifying tissue samples, and prioritizing cases for review, improving workflow efficiency and diagnostic accuracy

- AI integration in digital pathology hardware enables features such as automated slide classification, quantitative image analysis, and intelligent decision support, while cloud connectivity allows remote access to high-resolution slide images and centralized data management across institutions

- The seamless integration of digital scanners, workstations, and cloud-based infrastructure enables a unified ecosystem where pathology images can be captured, processed, analyzed, and shared efficiently, supporting telepathology and multi-site collaboration

- This trend towards intelligent, connected, and high-throughput imaging systems is fundamentally reshaping pathology workflows, as companies such as Leica Biosystems and Philips continue to develop AI-enabled whole slide imaging platforms with enhanced interoperability and remote diagnostic capabilities

- The demand for advanced digital pathology hardware with AI and cloud integration is growing rapidly across hospitals, diagnostic laboratories, and research centers, as stakeholders increasingly prioritize automation, scalability, and improved diagnostic turnaround times

- In addition, there is a growing emphasis on interoperability and standardization of imaging formats and systems, enabling seamless integration of digital pathology hardware with laboratory information systems (LIS) and hospital information systems (HIS) to improve operational efficiency

Digital Pathology Hardware Systems Market Dynamics

Driver

“Rising Demand for Advanced Diagnostic Accuracy and Digital Transformation in Healthcare”

- The increasing demand for improved diagnostic accuracy, coupled with the ongoing digital transformation of healthcare systems, is a significant driver for the heightened adoption of digital pathology hardware systems across clinical and research environments

- For instance, in recent years, healthcare providers have been investing in whole slide imaging systems and high-resolution scanners to streamline pathology workflows, reduce manual errors, and enable faster diagnosis of complex diseases such as cancer

- As healthcare institutions seek to enhance efficiency and manage growing patient volumes, digital pathology hardware offers capabilities such as remote slide viewing, centralized data access, and automated image capture, providing a strong alternative to traditional microscopy-based workflows

- Furthermore, the rising prevalence of chronic diseases and cancer, along with the increasing need for second opinions and collaborative diagnostics, is driving the adoption of connected pathology systems that facilitate real-time sharing and consultation among specialists

- The growing adoption of laboratory automation, telepathology, and integration with hospital information systems further contributes to market growth, as digital pathology hardware becomes an essential component of modern diagnostic infrastructure

- Another key driver is the increasing investment in healthcare infrastructure and digital health initiatives by governments and private organizations, which is accelerating the deployment of advanced diagnostic imaging systems in both developed and emerging markets

- In addition, the growing use of digital pathology in pharmaceutical and biotechnology research for drug discovery and clinical trials is further boosting demand for high-performance imaging hardware solutions.

Restraint/Challenge

“High Implementation Costs and Data Management & Integration Complexities”

- Concerns surrounding the high initial investment required for digital pathology hardware systems, including whole slide scanners, high-performance workstations, and storage infrastructure, pose a significant challenge to broader market adoption, particularly among smaller laboratories and healthcare facilities

- For instance, the deployment of fully integrated digital pathology solutions often requires substantial capital expenditure for hardware acquisition, IT infrastructure upgrades, and system maintenance, which can limit adoption in cost-sensitive settings

- Addressing these cost barriers through scalable solutions, flexible deployment models, and improved cost-efficiency of hardware components is crucial for expanding market penetration. In addition, challenges related to large data volumes generated by high-resolution imaging, interoperability with existing laboratory systems, and the need for secure and compliant data storage add further complexity to implementation

- While advancements in cloud storage and standardized data formats are helping to mitigate some of these issues, concerns around system integration, cybersecurity, and regulatory compliance remain critical considerations for end users

- Overcoming these challenges through cost optimization, enhanced interoperability standards, robust data management solutions, and increased awareness of long-term efficiency benefits will be vital for sustained growth of the digital pathology hardware systems market

- Another restraint is the shortage of skilled professionals trained to operate and interpret digital pathology systems, which can slow down adoption in regions where digital pathology expertise is still developing

- In addition, regulatory approval processes for digital pathology systems vary across regions, which can delay commercialization and limit the speed of market expansion in certain geographies

Digital Pathology Hardware Systems Market Scope

The market is segmented on the basis of product type, technology, application, and end user.

- By Product Type

On the basis of product type, the digital pathology hardware systems market is segmented into whole slide imaging (WSI) systems, digital scanners, microscopes with digital output, cameras & imaging sensors, workstations & displays, and storage & networking hardware. The whole slide imaging (WSI) systems segment dominated the market with the largest market revenue share of 47.2% in 2025, driven by its ability to capture high-resolution digital images of entire tissue slides, enabling comprehensive analysis, efficient storage, and seamless sharing across platforms. WSI systems are widely adopted in hospitals and diagnostic laboratories due to their critical role in digitizing pathology workflows and supporting telepathology and AI-based analysis. Their compatibility with advanced imaging software and integration with laboratory systems further strengthens their dominance in clinical diagnostics and research applications. The demand is also supported by increasing cancer screening programs and the need for centralized pathology services. Continuous technological advancements in scanning speed, image quality, and automation are further reinforcing the leadership of this segment.

The whole slide imaging (WSI) systems segment is also expected to witness the fastest growth rate during the forecast period, driven by increasing adoption of digital pathology in emerging markets, rising demand for remote diagnostics, and growing integration of AI-enabled analysis tools with WSI platforms. The scalability and efficiency of these systems make them suitable for high-throughput laboratories and multi-site healthcare networks. Expanding use in pharmaceutical research and clinical trials for precise tissue analysis is further accelerating growth. In addition, regulatory approvals and growing acceptance of digital slides for primary diagnosis in several regions are encouraging wider deployment of WSI systems. Increasing investments in healthcare digitization and infrastructure are also contributing to rapid expansion of this segment.

- By Technology

On the basis of technology, the market is segmented into optical digital pathology systems, AI-enabled systems, cloud-connected systems, and on-premise systems. The optical digital pathology systems segment dominated the market with the largest revenue share of 45% in 2025, driven by their established reliability, high-resolution imaging capabilities, and widespread use in existing laboratory workflows. These systems form the foundation of digital pathology hardware by enabling accurate capture and visualization of tissue samples without requiring advanced computational dependencies. Their compatibility with a wide range of laboratory environments and relatively lower complexity compared to advanced AI-integrated systems supports their continued dominance. Many healthcare facilities continue to rely on optical systems as a transition step from traditional microscopy to fully digital workflows. The availability of mature and standardized hardware solutions further reinforces this segment’s leadership.

The AI-enabled systems segment is expected to witness the fastest growth rate during the forecast period, driven by increasing adoption of artificial intelligence for automated image analysis, disease detection, and workflow optimization. AI-enabled hardware systems enhance diagnostic accuracy, reduce manual workload, and support decision-making through advanced analytics. Growing integration of machine learning algorithms with imaging hardware is enabling features such as tumor detection, tissue classification, and predictive diagnostics. Rising investments by key market players in AI-driven pathology solutions and partnerships between technology firms and healthcare providers are accelerating innovation in this segment. The increasing need for efficiency, scalability, and precision in diagnostics is further fueling rapid adoption of AI-enabled digital pathology systems.

- By Application

On the basis of application, the market is segmented into oncology, infectious disease diagnosis, drug discovery & development, academic research & education, and other clinical pathology. The oncology segment dominated the market with the largest revenue share of 50% in 2025, driven by the high global burden of cancer and the critical role of pathology in cancer diagnosis, staging, and treatment planning. Digital pathology hardware systems are extensively used in oncology for analyzing biopsy samples, identifying tumor characteristics, and supporting precision medicine approaches. The increasing demand for early and accurate cancer detection is significantly contributing to the adoption of advanced imaging systems. In addition, integration of AI tools for tumor detection and grading is further enhancing the efficiency of oncology diagnostics. Rising investments in cancer research and screening programs across hospitals and diagnostic centers continue to support the dominance of this segment.

The drug discovery & development segment is expected to witness the fastest growth rate during the forecast period, driven by increasing use of digital pathology in pharmaceutical and biotechnology research. Digital imaging systems enable high-throughput analysis of tissue samples in preclinical and clinical studies, improving efficiency in drug testing and biomarker identification. The ability to digitize and share pathology data across global research teams is accelerating collaboration and decision-making in drug development pipelines. Growing adoption of digital pathology in clinical trials for histopathological analysis is also contributing to segment growth. Furthermore, increasing R&D investments by pharmaceutical companies and the need for precise, reproducible data in drug evaluation are fueling rapid expansion of this application segment.

- By End User

On the basis of end user, the market is segmented into hospitals & healthcare systems, diagnostic laboratories, pharmaceutical & biotechnology companies, research & academic institutes, and others. The hospitals & healthcare systems segment dominated the market with the largest revenue share of 42% in 2025, driven by the increasing adoption of digital diagnostics to improve workflow efficiency, reduce turnaround time, and enhance collaboration among pathologists. Hospitals are major users of whole slide imaging systems and workstations for primary diagnosis, second opinions, and telepathology applications. The integration of digital pathology hardware with hospital information systems (HIS) and laboratory information systems (LIS) further supports its widespread adoption. Rising patient volumes, increasing prevalence of chronic diseases, and the need for accurate and timely diagnosis are key factors driving demand in this segment. Continuous upgrades in hospital infrastructure and investments in digital health technologies further reinforce its dominance.

The pharmaceutical & biotechnology companies segment is expected to witness the fastest growth rate during the forecast period, driven by increasing use of digital pathology hardware in drug discovery, biomarker research, and clinical trials. These organizations rely on high-resolution imaging systems to analyze tissue samples for evaluating drug efficacy and safety. The ability to digitize pathology workflows enhances data sharing across global research teams and improves efficiency in research processes. Growing R&D expenditure by pharmaceutical companies and increasing adoption of precision medicine approaches are further contributing to segment growth. In addition, collaborations between technology providers and life sciences companies are accelerating the deployment of advanced digital pathology systems in this segment.

Digital Pathology Hardware Systems Market Regional Analysis

- North America dominated the digital pathology hardware systems market with the largest revenue share of 42.7% in 2025, driven by early adoption of advanced healthcare technologies, strong digital infrastructure, high healthcare expenditure, and the presence of key market players

- Healthcare providers in the region highly value the enhanced diagnostic accuracy, workflow efficiency, and seamless integration offered by digital pathology hardware systems with hospital information systems (HIS), laboratory information systems (LIS), and AI-enabled analytical platforms

- This widespread adoption is further supported by high healthcare expenditure, a technologically advanced medical ecosystem, and the growing preference for telepathology, remote consultations, and centralized data management, establishing digital pathology hardware as a key enabler of modern diagnostic and research workflows

U.S. Digital Pathology Hardware Systems Market Insight

The U.S. digital pathology hardware systems market captured the largest revenue share in North America in 2025, driven by rapid adoption of advanced diagnostic technologies and the expansion of digital healthcare infrastructure. Healthcare providers are increasingly prioritizing high-resolution whole slide imaging systems and integrated workstations to enhance diagnostic accuracy and workflow efficiency. The growing emphasis on telepathology, AI-enabled diagnostics, and remote consultations is further accelerating adoption across hospitals and reference laboratories. Moreover, strong investments in healthcare digitization, coupled with the presence of leading market players and favorable regulatory support for digital pathology solutions, are significantly contributing to market growth in the country.

Europe Digital Pathology Hardware Systems Market Insight

The Europe digital pathology hardware systems market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing healthcare digitization initiatives and the rising demand for efficient diagnostic solutions. The region’s stringent regulatory frameworks and emphasis on high-quality healthcare standards are encouraging the adoption of advanced imaging systems and standardized digital workflows. Growing investments in hospital modernization, along with increasing use of telepathology for cross-border consultations, are further supporting market expansion. In addition, the integration of digital pathology hardware with laboratory and hospital information systems is gaining traction across both public and private healthcare sectors.

U.K. Digital Pathology Hardware Systems Market Insight

The U.K. digital pathology hardware systems market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the National Health Service’s (NHS) focus on digital transformation and improved diagnostic efficiency. The increasing need to reduce turnaround times for pathology results and enhance collaboration among specialists is fueling the adoption of whole slide imaging systems and digital scanners. In addition, the growing prevalence of chronic diseases, particularly cancer, is encouraging the deployment of advanced diagnostic tools. The country’s strong research ecosystem and investments in AI-enabled healthcare technologies are also contributing to the expansion of digital pathology infrastructure.

Germany Digital Pathology Hardware Systems Market Insight

The Germany digital pathology hardware systems market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s emphasis on technological innovation, high-quality healthcare services, and precision diagnostics. Germany’s well-established healthcare infrastructure supports the integration of advanced imaging systems in hospitals, diagnostic laboratories, and research institutes. Increasing awareness of digital diagnostics, along with a strong focus on data security and interoperability, is driving adoption of digital pathology solutions. Furthermore, the growing application of digital pathology in pharmaceutical research and clinical trials is enhancing demand for high-performance hardware systems.

Asia-Pacific Digital Pathology Hardware Systems Market Insight

The Asia-Pacific digital pathology hardware systems market is poised to grow at the fastest CAGR during the forecast period, driven by rapid urbanization, expanding healthcare infrastructure, and increasing investments in digital health technologies across countries such as China, Japan, and India. The region’s growing patient population and rising incidence of chronic diseases are accelerating demand for efficient and scalable diagnostic solutions. Governments across APAC are promoting healthcare digitization initiatives, further supporting adoption. In addition, the region’s role as a manufacturing hub for medical imaging equipment is improving affordability and accessibility of digital pathology hardware to a broader customer base.

Japan Digital Pathology Hardware Systems Market Insight

The Japan digital pathology hardware systems market is gaining momentum due to the country’s advanced technological ecosystem, strong healthcare system, and increasing demand for precision diagnostics. The adoption of digital pathology is supported by the integration of AI-enabled imaging systems and telepathology solutions across hospitals and research institutions. Japan’s aging population is also driving demand for efficient and accurate diagnostic tools to manage age-related diseases, including cancer. Furthermore, the country’s focus on innovation and automation in healthcare is encouraging the deployment of high-resolution scanners and connected pathology platforms.

India Digital Pathology Hardware Systems Market Insight

The India digital pathology hardware systems market accounted for a significant revenue share in Asia Pacific in 2025, attributed to rapid urbanization, expanding healthcare infrastructure, and increasing adoption of digital technologies in diagnostics. The growing burden of chronic diseases, particularly cancer, is driving demand for advanced pathology solutions across hospitals and diagnostic laboratories. Government initiatives aimed at improving healthcare access and promoting digital health are further supporting market growth. In addition, the availability of cost-effective digital pathology hardware and increasing investments by domestic and international players are making these solutions more accessible across both urban and semi-urban regions.

Digital Pathology Hardware Systems Market Share

The Digital Pathology Hardware Systems industry is primarily led by well-established companies, including:

- Leica Biosystems Nussloch GmbH (Germany)

- Hamamatsu Photonics K.K. (Japan)

- Koninklijke Philips N.V. (Netherlands)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Olympus Corporation (Japan)

- NIKON Corporation (Japan)

- Mikroscan Technologies Inc. (U.S.)

- Huron Digital Pathology Inc. (Canada)

- Inspirata Inc. (U.S.)

- OptraSCAN Inc. (U.S.)

- Sectra AB (Sweden)

- XIFIN Inc. (U.S.)

- Akoya Biosciences, Inc. (U.S.)

- Aiforia Technologies Oy (Finland)

- DeepBio Inc. (U.S.)

- Paige AI, Inc. (U.S.)

- PathAI, Inc. (U.S.)

- Visiopharm A/S (Denmark)

- Motic Digital Pathology (China)

What are the Recent Developments in Global Digital Pathology Hardware Systems Market?

- In March 2026, Philips expanded its digital pathology portfolio with the cloud-enabled Philips IntelliSite Pathology Solution on HealthSuite, a hardware-enabled system designed to help healthcare organizations scale digital pathology adoption and workflows without complex on-premise infrastructure. This expansion underscores the trend toward integrated, scalable digital pathology platforms that combine imaging hardware with cloud services to support high-throughput diagnostics

- In December 2025, Leica Biosystems expanded its clinical digital pathology portfolio with the launch of multiple new whole slide scanners including the Aperio GT 180 DX and Aperio CS5 DX showcasing next-generation hardware offerings for pathology departments

- In November 2025, Hologic, Inc. revealed expanded CE marking in the EU for its Genius™ Digital Diagnostics System, enabling the hardware to image and review both cell and tissue specimens broadening clinical use cases in digital pathology workflows

- In April 2025, academic research introduced Iris, a next-generation digital pathology rendering engine aimed at accelerating high-quality slide image rendering a foundational hardware-software advancement that can improve whole slide scanner performance

- In January 2025, Roche announced that its VENTANA DP 600 high-volume slide scanner, part of the Roche Digital Pathology Dx system, received FDA 510(k) clearance for aiding clinical diagnosis with high-resolution whole-slide imaging a significant milestone for digital pathology hardware adoption in clinical workflows

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.