Global Digital Substation Market

Market Size in USD Billion

USD

8.76 Billion

USD

14.50 Billion

2025

2033

USD

8.76 Billion

USD

14.50 Billion

2025

2033

| 2026 - 2033 | |

| USD 8.76 Billion | |

| USD 14.50 Billion | |

| % | |

|

Digital Substation Market Size

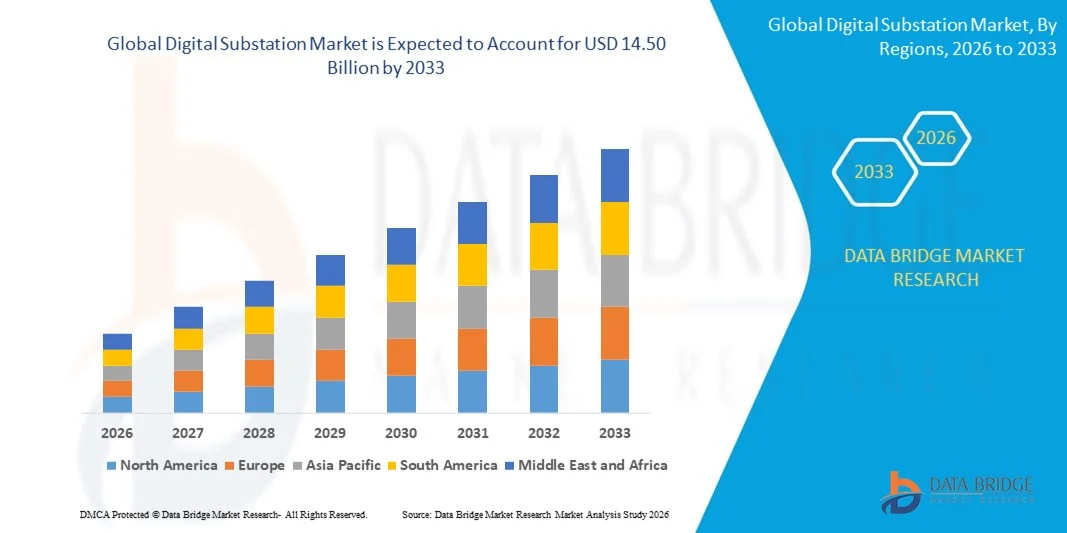

- The global digital substation market size was valued at USD 8.76 billion in 2025 and is expected to reach USD 14.50 billion by 2033, at a CAGR of 6.50% during the forecast period

- The market growth is largely fuelled by the increasing demand for reliable and efficient power transmission and distribution systems, rising adoption of smart grid technologies, and the need for real-time monitoring and automation in substations

- Growing government initiatives for modernizing electrical infrastructure and investments in renewable energy integration are also supporting market expansion

Digital Substation Market Analysis

- The digital substation market is witnessing significant transformation with advancements in communication protocols, IoT-enabled monitoring, and intelligent electronic devices (IEDs)

- Increasing focus on operational efficiency, predictive maintenance, and minimizing downtime is driving utilities to adopt digital substation solutions

- Asia-Pacific dominated the digital substation market with the largest revenue share of 36.00% in 2025 driven by rapid urbanization, increasing electricity demand, and government investments in smart grid and renewable energy infrastructure

- North America region is expected to witness the highest growth rate in the global digital substation market, driven by modernization of legacy transmission and distribution infrastructure, government support for grid automation, and increasing deployment of digital substations across utilities and industrial networks

- The hardware segment held the largest market revenue share in 2025, driven by the essential role of intelligent electronic devices, relays, and transformers in enabling automation and real-time monitoring in substations. Hardware solutions form the backbone of digital substations, providing reliable performance and compatibility with modern communication protocols

Report Scope and Digital Substation Market Segmentation

|

Attributes |

Digital Substation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• ABB (Switzerland) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Digital Substation Market Trends

Rising Adoption Of Smart Grid And Automation Technologies

- The increasing focus on efficient, reliable, and automated power transmission is significantly shaping the digital substation market, as utilities and energy companies prefer solutions that improve monitoring, control, and operational performance. Digital substations are gaining traction due to their ability to reduce downtime, enhance grid reliability, and enable real-time data analysis without compromising safety or performance. This trend strengthens their adoption across transmission and distribution networks, encouraging manufacturers to innovate with advanced substation automation solutions

- Growing emphasis on energy efficiency, grid modernization, and integration of renewable energy sources has accelerated the demand for digital substations in utilities, industrial facilities, and commercial power networks. Operators are actively seeking systems that provide predictive maintenance, enhanced fault detection, and improved asset utilization, prompting suppliers to focus on scalable and interoperable solutions

- Government initiatives and regulatory frameworks supporting smart grids, energy security, and low-carbon infrastructure are influencing purchasing decisions. Utilities are emphasizing compliance with IEC 61850 standards, communication network reliability, and cybersecurity features. These factors are helping companies differentiate products and reinforce market positioning, while also driving adoption of modular, scalable digital substation solutions

- For instance, in 2024, Siemens in Germany and ABB in Switzerland expanded their digital substation portfolios by introducing advanced IEC 61850-compliant systems and intelligent electronic devices (IEDs) with predictive maintenance capabilities. These deployments were implemented across high-voltage transmission and distribution networks, offering improved operational efficiency, reduced energy losses, and increased grid resilience

- While demand for digital substations is growing, sustained market expansion depends on continuous R&D, cost optimization, and integration with existing grid infrastructure. Manufacturers are also focusing on enhancing interoperability, cybersecurity, and modular design to meet evolving power sector requirements and ensure reliable, scalable solutions for global adoption

Digital Substation Market Dynamics

Driver

Rising Demand For Efficient And Automated Power Transmission

- Increasing investment in smart grid projects and modernization of aging electrical infrastructure is a major driver for the digital substation market. Utilities are replacing conventional substations with digital alternatives to enhance monitoring, reduce transmission losses, and ensure system reliability. This trend also encourages research into advanced IEDs and real-time data analytics solutions, supporting market growth

- Expanding adoption of renewable energy sources and distributed generation systems is influencing market growth. Digital substations help integrate solar, wind, and other renewable sources efficiently, improving grid stability and operational flexibility. The growing focus on predictive maintenance, fault detection, and remote control further reinforces this trend

- Utilities and industrial operators are actively promoting digital substation solutions through pilot projects, technology partnerships, and government-supported smart grid initiatives. These efforts are supported by the increasing need for real-time monitoring, enhanced safety, and optimized power distribution, encouraging broader adoption of digital technologies

- For instance, in 2023, Schneider Electric in France and General Electric in the U.S. reported increased implementation of digital substation solutions across transmission and distribution networks. These deployments improved operational efficiency, reduced downtime, and enhanced grid reliability, driving technology adoption and market differentiation

- Although rising smart grid and automation trends support growth, wider adoption depends on cost-efficiency, standardization, and cybersecurity readiness. Investment in advanced communication protocols, system integration, and modular architectures will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

High Initial Investment And Cybersecurity Concerns

- The high upfront cost of digital substations compared to conventional substations remains a key challenge, limiting adoption among cost-sensitive utilities. Expenses related to intelligent devices, communication infrastructure, and system integration contribute to elevated pricing. In addition, maintaining compliance with standards and regulatory requirements can further impact deployment

- Cybersecurity risks and the need for robust protection of critical infrastructure are significant concerns. Vulnerabilities in communication networks, data management systems, and remote monitoring can pose threats, requiring utilities to invest heavily in secure and reliable systems

- Limited awareness and technical expertise, particularly in emerging markets, restrict adoption of advanced digital substation solutions. Utilities may hesitate to implement new technologies due to operational complexity, training requirements, and perceived risks

- For instance, in 2024, utilities in Southeast Asia and Latin America reported slower adoption of digital substations due to high capital expenditure and limited understanding of functional benefits. Challenges in integrating legacy systems and ensuring cybersecurity compliance further affected implementation timelines

- Overcoming these challenges will require cost-effective deployment strategies, workforce training, and strengthened cybersecurity measures. Collaboration with technology providers, government agencies, and industry standards organizations can help unlock long-term growth potential in the global digital substation market, while developing scalable and secure solutions will be essential for broader adoption

Digital Substation Market Scope

The market is segmented on the basis of module, type, installation type, connectivity, voltage level, industry, and architecture.

- By Module

On the basis of module, the digital substation market is segmented into hardware, fiber-optic communication networks, and SCADA systems. The hardware segment held the largest market revenue share in 2025, driven by the essential role of intelligent electronic devices, relays, and transformers in enabling automation and real-time monitoring in substations. Hardware solutions form the backbone of digital substations, providing reliable performance and compatibility with modern communication protocols.

The fiber-optic communication networks segment is expected to witness the fastest growth from 2026 to 2033, driven by the increasing demand for high-speed, secure, and interference-free data transmission. Fiber-optic solutions facilitate efficient integration with SCADA systems and real-time control, making them crucial for advanced digital substations.

- By Type

On the basis of type, the market is segmented into transmission substations and distribution substations. Transmission substations accounted for the largest share in 2025, owing to the high deployment of digital solutions in power transmission networks for efficient energy management and grid stability.

Distribution substations are expected to register the highest growth rate during 2026–2033, due to rising urbanization and smart grid initiatives that require enhanced monitoring, automation, and fault management at the distribution level. The growing adoption of distributed energy resources (DERs) and rooftop solar installations is increasing the need for real-time load balancing and grid intelligence

- By Installation Type

On the basis of installation type, the market is categorized into new installations and retrofit installations. New installations held the largest revenue share in 2025, driven by government investments in smart grids and modern substations for efficient power distribution.

Retrofit installations are expected to grow rapidly from 2026 to 2033, fueled by the need to modernize aging infrastructure and improve operational efficiency through digital upgrades. Many existing substations still operate with legacy equipment that cannot support advanced automation or remote monitoring.

- By Connectivity

On the basis of connectivity, the market is segmented into < 33 kV, 33 kV to 110 kV, 110 kV to 220 kV, 220 kV to 550 kV, and > 550 kV. The 220 kV to 550 kV segment held the largest share in 2025, owing to its widespread use in regional transmission networks and the increasing integration of digital monitoring and control systems.

The > 550 kV segment is expected to witness the fastest growth during 2026–2033, driven by the expansion of ultra-high-voltage transmission projects and the demand for advanced digital solutions to enhance grid reliability. These ultra-high-voltage lines are essential for long-distance power transmission from renewable energy sources, such as hydro and wind farms, to urban centers.

- By Voltage Level

On the basis of voltage level, the market is categorized into low, medium, and high. High-voltage digital substations accounted for the largest market revenue in 2025, due to their critical role in transmitting electricity over long distances and the need for robust automation and protection systems.

Medium-voltage digital substations are expected to grow at the fastest rate from 2026 to 2033, driven by the proliferation of smart grids, renewable energy integration, and urban infrastructure development. These substations provide a critical interface between high-voltage transmission networks and low-voltage distribution systems.

- By Industry

On the basis of industry, the market is segmented into utility, heavy industries, transportation, and others. The utility segment held the largest share in 2025, owing to substantial investments in smart grid modernization and digital substation deployment to improve energy efficiency and reliability.

The transportation segment is expected to witness the fastest growth during 2026–2033, fueled by electrification of railways, metro systems, and industrial transport networks that require advanced digital monitoring and automation. Digital substations in transportation ensure reliable power supply, rapid fault detection, and seamless operation of critical transport infrastructure.

- By Architecture

On the basis of architecture, the market is segmented into process, bay, and station. The station architecture segment accounted for the largest revenue share in 2025, driven by its ability to provide comprehensive automation, monitoring, and control of entire substation operations

The bay architecture segment is expected to register the fastest growth from 2026 to 2033, due to increasing adoption of modular designs, scalable automation, and localized control solutions in modern digital substations. Bay architecture allows utilities to add or modify individual bays without affecting overall substation operations, offering flexibility and reduced downtime.

Digital Substation Market Regional Analysis

- Asia-Pacific dominated the digital substation market with the largest revenue share of 36.00% in 2025 driven by rapid urbanization, increasing electricity demand, and government investments in smart grid and renewable energy infrastructure

- Countries such as China, Japan, and India are actively upgrading transmission and distribution networks with digital solutions, enabling efficient load management, automated protection, and real-time monitoring

- Rising industrialization and smart city projects are further supporting the adoption of digital substation

Japan Digital Substation Market Insight

The Japan digital substation market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s advanced technological infrastructure, focus on renewable energy integration, and need for reliable urban power distribution. Utilities are adopting fiber-optic networks, SCADA systems, and intelligent monitoring devices to ensure operational efficiency. Increasing demand for smart grids and automation solutions in urban and industrial sectors is driving market expansion

China Digital Substation Market Insight

The China digital substation market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to extensive investments in ultra-high-voltage transmission projects, rapid urbanization, and government-led smart grid initiatives. The country is a leading adopter of digital substations, driven by rising electricity demand, renewable energy integration, and modernization of existing transmission and distribution networks. Domestic manufacturers and competitive pricing of digital solutions are also accelerating market growth across residential, industrial, and utility sectors.

North America Digital Substation Market Insight

North America digital substation market is expected to witness the fastest growth rate from 2026 to 2033, driven by extensive smart grid modernization initiatives, rising investments in renewable energy integration, and the demand for reliable and automated power distribution networks. Utilities and industrial players in the region are increasingly adopting digital substations to enhance operational efficiency, improve real-time monitoring, and reduce downtime. The presence of technologically advanced infrastructure, coupled with favorable government policies and high capital expenditure on grid automation, supports widespread adoption across transmission and distribution networks

U.S. Digital Substation Market Insight

The U.S. digital substation market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the modernization of aging transmission and distribution infrastructure and growing investments in renewable energy projects. Utilities are increasingly deploying intelligent electronic devices, SCADA systems, and fiber-optic communication networks for enhanced monitoring, protection, and automation. The shift toward digital substations is further supported by the country’s emphasis on smart grids, energy efficiency, and reliable power supply for residential, commercial, and industrial sectors.

Europe Digital Substation Market Insight

The Europe digital substation market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by government initiatives promoting smart grids and stringent regulations for energy efficiency and grid reliability. The integration of renewable energy sources, rising urbanization, and advanced grid management solutions is accelerating digital substation deployment. European utilities are focusing on upgrading existing substations with modular, scalable, and secure automation solutions to meet increasing demand across residential, industrial, and transportation sectors.

U.K. Digital Substation Market Insight

The U.K. digital substation market is expected to witness the fastest growth rate from 2026 to 2033, driven by the adoption of smart grid technologies, electrification of transport networks, and modernization of legacy infrastructure. The government’s push for renewable energy integration and reduced transmission losses is encouraging utilities to implement automated monitoring and control systems. Deployment of process, bay, and station architectures is increasing across urban and suburban areas, supporting efficient energy management and grid stability.

Germany Digital Substation Market Insight

The Germany digital substation market is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising energy transition initiatives, demand for renewable integration, and advanced automation solutions. Utilities are increasingly focused on predictive maintenance, digital monitoring, and secure communication networks. The country’s emphasis on sustainability, reliability, and cutting-edge technology adoption is driving investments in digital substations, particularly in industrial, utility, and commercial applications.

Digital Substation Market Share

The Digital Substation industry is primarily led by well-established companies, including:

• ABB (Switzerland)

• General Electric (U.S.)

• Siemens (Germany)

• Eaton (Ireland/U.S.)

• Schneider Electric (France)

• Honeywell International Inc. (U.S.)

• Cisco (U.S.)

• Emerson Electric Co. (U.S.)

• NR Electric Co., Ltd. (China)

• L&T Construction (India)

• Schweitzer Engineering Laboratories, Inc. (U.S.)

• WELOTEC (Germany)

• TCS Digital (India)

• Tesco Automation Inc. (U.S.)

• Locamation (Netherlands)

• SIFANG (China)

• Netcontrol Group (U.K.)

• Prosoft-Systems Ltd. (U.K.)

• Fuji Electric Co., Ltd. (Japan)

• Tekvel (Russia)

• Efacec (Portugal)

Latest Developments in Global Digital Substation Market

- In December 2025, Hitachi Energy joined SP Energy Networks’ FITNESS project in Scotland to advance digital substation technology. The initiative aims to modernize transmission networks by replacing traditional copper wiring with fiber-optic communication, enhancing safety, flexibility, and reliability, while reducing costs and environmental impact. This collaboration is expected to accelerate the adoption of digital substations across Europe and improve grid efficiency

- In March 2025, Siemens unveiled its latest grid modernization innovations at DISTRIBUTECH 2025 through Siemens Xcelerator. The platform offers interoperable, scalable, and AI-driven solutions, enabling utilities to simplify energy system transformation, manage growing complexity, and enhance operational efficiency, thereby strengthening the global digital substation market

- In March 2025, Schneider Electric launched the One Digital Grid Platform, providing a technical foundation for independent software solutions. The platform helps utilities accelerate grid modernization, integrate cleaner and more affordable energy solutions, and enhance operational reliability, promoting wider adoption of digital substations

- In August 2024, Hitachi Energy introduced SF6-free circuit breakers for substations, offering high-performance switching and protection while minimizing greenhouse gas emissions. This sustainable solution enhances operational safety, reliability, and environmental compliance, supporting the market shift toward eco-friendly digital substation technologies

- In February 2024, GE Vernova launched the GridBeats Integrated Digital Substation, a hardware-inclusive automation platform with software-defined merging units and protection relays. The solution reduces copper cabling by up to 80%, enables real-time data conversion, and strengthens grid resilience, driving efficiency in high-voltage environments

- In January 2024, Hitachi Energy released the upgraded SAM600 3.0 process interface unit, integrating multiple functions into a single device. This innovation reduces wiring complexity by up to 90%, enhances operational flexibility, reliability, and sustainability, and supports compliance with IEC 61850 standards and cybersecurity requirements

- In July 2023, the U.S. commissioned its first fully digital substation in California. The facility leverages advanced digital technologies to improve monitoring, control, and operational efficiency, resulting in better service reliability, reduced operational costs, and a boost to the digital substation market in North America

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Digital Substation Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Digital Substation Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Digital Substation Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.