Global Digital Television Tv Market

Market Size in USD Billion

USD

14.88 Billion

USD

38.17 Billion

2024

2032

USD

14.88 Billion

USD

38.17 Billion

2024

2032

| 2025 - 2032 | |

| USD 14.88 Billion | |

| USD 38.17 Billion | |

| % | |

|

Digital Television (TV) Market Size

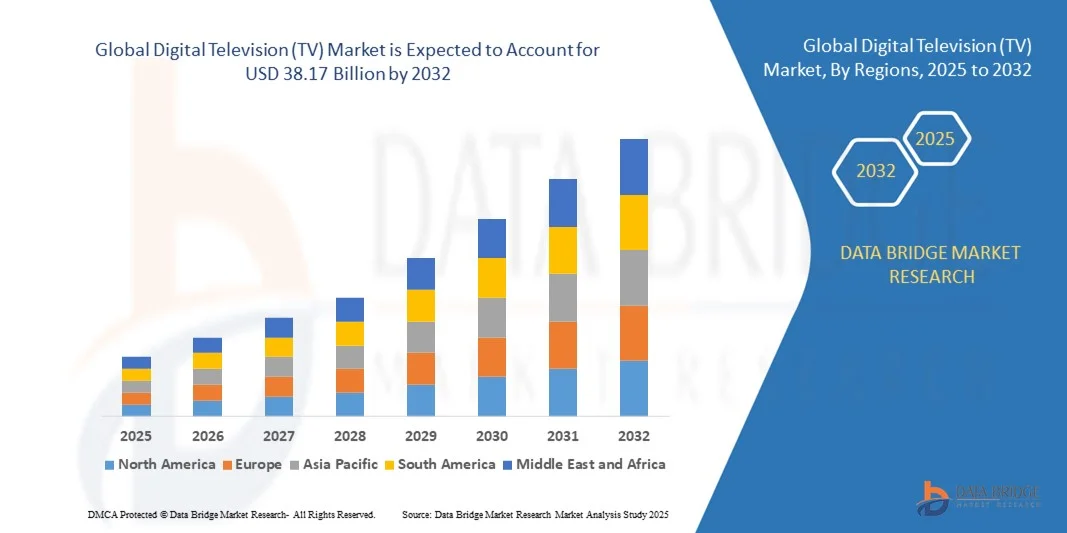

- The global digital television (TV) market size was valued at USD 14.88 billion in 2024 and is expected to reach USD 38.17 billion by 2032, at a CAGR of 12.50% during the forecast period

- The market growth is largely fueled by the growing adoption of smart TVs and advanced display technologies, along with increasing digital content consumption, leading to higher penetration of high-definition and ultra-high-definition television sets in both residential and commercial settings

- Furthermore, rising consumer demand for immersive viewing experiences, larger screen sizes, and feature-rich smart TVs with internet connectivity and streaming capabilities is driving the shift from traditional televisions to digital and connected TV solutions. These factors are accelerating market expansion, thereby significantly boosting the industry’s growth

Digital Television (TV) Market Analysis

- Digital televisions are electronic devices that deliver content through digital signals, supporting high-definition (HD), 4K, and smart functionalities such as internet connectivity, app integration, and voice control. These TVs offer enhanced picture quality, interactive features, and seamless streaming options, catering to evolving consumer preferences in entertainment and information consumption

- The escalating demand for digital TVs is primarily driven by increasing adoption of streaming platforms, rising consumer preference for high-resolution and large-screen TVs, growing disposable incomes, and advancements in display technologies such as OLED, QLED, and HDR. In addition, the integration of smart features and user-friendly interfaces further fuels market growth across residential and commercial sectors

- Asia-Pacific dominated the digital television (TV) market with a share of 39.6% in 2024, due to rising consumer electronics adoption, increasing urbanization, and a strong presence of TV manufacturing hubs.

- North America is expected to be the fastest growing region in the digital television (TV) market during the forecast period due to high consumer demand for smart TVs, large-screen displays, and advanced resolution formats

- HDTV segment dominated the market with a market share of 52.9% in 2024, due to the growing consumer preference for high-definition content and enhanced viewing experiences. HDTVs are widely adopted due to their superior picture quality, compatibility with modern broadcast standards, and support for various multimedia formats. Consumers often prioritize HDTVs for home entertainment setups as they offer a balance of performance, affordability, and advanced features such as smart TV integration and HDR support. The increasing availability of HDTVs across retail and online channels further fuels market demand, making it the go-to choice for residential users

Report Scope and Digital Television (TV) Market Segmentation

|

Attributes |

Digital Television (TV) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Digital Television (TV) Market Trends

Growth of Smart and Connected TVs

- The digital television market is experiencing robust growth due to the increasing preference for smart and connected TVs that integrate internet access and content streaming features. Consumers are embracing advanced platforms that combine traditional broadcasting with on-demand content and interactive applications, transforming home entertainment experiences

- For instance, Samsung and LG have expanded their smart TV portfolios with models offering seamless connectivity, AI-powered voice assistants, and integration with major streaming platforms. Sony has also partnered with Google to deliver Android TV interfaces that enhance content discovery and provide unified access to both streaming apps and live broadcast channels

- The adoption of smart TVs is driven by their ability to offer multiple functionalities beyond traditional viewing, such as gaming support, voice search, and compatibility with connected smart home devices. This multifunctional nature positions smart TVs as entertainment hubs that blend convenience with cutting-edge technology

- Advances in connectivity, such as Wi-Fi 6 and built-in casting solutions, are enabling faster and smoother streaming experiences. These features allow users to enjoy 4K and 8K content without interruptions, promoting an elevated standard for consumer viewing expectations worldwide

- Manufacturers are increasingly focusing on creating user-centric smart TV ecosystems that offer personalized recommendations, multi-device synchronization, and enhanced user interfaces. This integration of hardware and digital platforms is central to capturing consumer loyalty in an intensely competitive marketplace

- The growing demand for connected TVs underscores the future direction of the industry, with smart platforms now serving as the baseline for consumer interest. The trend is reshaping consumption patterns, ensuring smart and connected televisions remain at the forefront of global digital entertainment innovation

Digital Television (TV) Market Dynamics

Driver

Rising Demand for High-Resolution, Large-Screen TVs

- The global rise in demand for immersive viewing and cinematic experiences at home is driving growth in high-resolution, large-screen television sales. Consumers are prioritizing enhanced visuals and wide display formats as prices for advanced screen technologies gradually become more accessible

- For instance, TCL has launched competitively priced 75-inch and 85-inch televisions featuring 4K and mini-LED display technology, making large-format TVs more attainable for mid-range consumers. Similarly, LG’s OLED Evo series has expanded in the premium category, focusing on ultra-high-definition clarity and large screens with vivid contrast

- The adoption of 4K and 8K display technologies is rapidly increasing as households seek superior picture quality, particularly for gaming and high-definition streaming. Larger display sizes create a more immersive environment for sports, movies, and multimedia applications, raising consumer demand in residential settings

- Rapid improvements in panel manufacturing and economies of scale have reduced production costs, enabling wider accessibility to larger televisions. Enhanced features such as HDR, Dolby Vision, and AI-based picture optimization continue to raise the perceived value of large-screen TVs among consumers

- Large-screen, high-resolution televisions are increasingly seen as long-term investments in home entertainment systems. This consistent demand affirms their growing role in establishing digital televisions as central fixtures in modern households and premium entertainment setups across global markets

Restraint/Challenge

High Cost of Premium TVs

- The relatively high cost of advanced premium televisions remains a significant barrier for many consumers, particularly in price-sensitive markets. While demand for 4K and 8K large-screen displays is growing rapidly, affordability issues continue to limit widespread adoption among middle-income households

- For instance, Sony’s Bravia XR 8K and Samsung’s Neo QLED series are priced at the higher end, restricting their reach to affluent buyers and specialized user segments. These high price points create disparities, leaving significant portions of the global population dependent on mid-range digital televisions

- Premium televisions often include additional expenses related to installation, mounting systems, and extended warranties, adding to the total cost of ownership. Furthermore, the availability of affordable alternatives such as budget-friendly smart TVs delays consumer willingness to upgrade to premium formats

- Fluctuating economic conditions and inflationary pressures further impact consumer purchasing decisions in several regions. Many households prioritize cost-effective options that provide good performance rather than investing heavily in premium models with advanced features they may not fully utilize

- In conclusion, the high cost of premium digital televisions is slowing their adoption in broader markets despite strong consumer interest. Manufacturers are expected to focus on cost innovation and flexible financing solutions to bridge this gap and enable sustainable demand for advanced TV technologies

Digital Television (TV) Market Scope

The market is segmented on the basis of type, resolution, and size.

- By Type

On the basis of type, the digital television market is segmented into SDTV, EDTV, HDTV, and Others. The HDTV segment dominated the largest market revenue share of 52.9% in 2024, driven by the growing consumer preference for high-definition content and enhanced viewing experiences. HDTVs are widely adopted due to their superior picture quality, compatibility with modern broadcast standards, and support for various multimedia formats. Consumers often prioritize HDTVs for home entertainment setups as they offer a balance of performance, affordability, and advanced features such as smart TV integration and HDR support. The increasing availability of HDTVs across retail and online channels further fuels market demand, making it the go-to choice for residential users.

The EDTV segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by demand in emerging markets where cost-effectiveness and acceptable image quality are key factors. EDTVs offer improved resolution over SDTV at a lower price point compared with HDTVs, making them an attractive option for budget-conscious consumers. Their smaller size and lighter weight also make EDTVs suitable for secondary rooms or compact living spaces. Manufacturers are increasingly innovating in EDTV design, adding connectivity and multimedia features, which further accelerates adoption in both residential and small business segments.

- By Resolution

On the basis of resolution, the digital television market is segmented into 480p (640 x 480), 720p (1280 x 720), 1080p (1920 x 1080), and Others (4K). The 1080p segment held the largest market revenue share in 2024, driven by the growing availability of high-definition content and consumer demand for sharper visuals. 1080p TVs offer an optimal balance between picture quality and affordability, supporting a wide range of applications including gaming, streaming, and live broadcasting. The widespread adoption of HD-ready broadcasting services and online content platforms further reinforces the preference for 1080p resolution, making it a standard choice for households seeking high-quality entertainment.

The 4K segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by increasing content availability in ultra-high definition and the rising adoption of smart TVs with 4K capability. 4K TVs deliver four times the resolution of 1080p, offering immersive viewing experiences for sports, movies, and gaming. Falling prices of 4K panels and enhanced display technologies such as HDR and OLED further drive consumer adoption. In addition, streaming platforms and gaming consoles increasingly support 4K content, boosting the market potential for this high-resolution segment.

- By Size

On the basis of size, the digital television market is segmented into 11''–32'', 32''–42'', 42''–50'', and 50'' & above. The 42''–50'' segment dominated the largest market revenue share in 2024, driven by its suitability for most living rooms and home entertainment setups. This size range provides a comfortable viewing experience without occupying excessive space, making it a preferred choice for families. TVs in this segment often integrate advanced features such as smart functionality, HDR, and multiple connectivity options, enhancing their appeal for both casual and avid viewers. Retail promotions and availability across online and offline channels further reinforce its market dominance.

The 50'' & Above segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by rising consumer preference for cinematic home viewing experiences. Larger screen sizes offer more immersive experiences, particularly for sports, movies, and gaming, aligning with the trend of home theater setups. Advances in panel technology, improved affordability, and the popularity of wall-mounted designs contribute to increased adoption. Furthermore, smart TV features, 4K resolution, and enhanced audio integration make this segment increasingly attractive in both developed and emerging markets.

Digital Television (TV) Market Regional Analysis

- Asia-Pacific dominated the digital television (TV) market with the largest revenue share of 39.6% in 2024, driven by rising consumer electronics adoption, increasing urbanization, and a strong presence of TV manufacturing hubs

- The region’s cost-effective production, growing disposable income, and expanding e-commerce penetration are accelerating market expansion

- The availability of skilled labor, government incentives for electronics manufacturing, and increasing demand for high-definition and large-screen TVs are contributing to strong regional growth

China Digital Television Market Insight

China held the largest share in the Asia-Pacific digital television market in 2024, owing to its position as a global electronics manufacturing hub. The country’s extensive production infrastructure, favorable policies for consumer electronics, and strong export capabilities are major growth drivers. Rising domestic consumption, increasing smart TV adoption, and continuous technological innovation in display panels further strengthen China’s market dominance.

India Digital Television Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by a rapidly expanding middle class, rising urbanization, and growing demand for affordable HDTV and 4K TVs. Government initiatives such as “Make in India” and incentives for electronics manufacturing are supporting local production. Increasing penetration of online retail platforms and rising awareness of digital entertainment are contributing to robust market expansion.

Europe Digital Television Market Insight

The Europe digital television market is expanding steadily, supported by high consumer spending, preference for premium TVs, and strong demand for smart and connected devices. The region emphasizes energy-efficient and high-resolution televisions, particularly in developed markets. Rising adoption of 4K and large-screen TVs, combined with the availability of advanced display technologies, is driving market growth.

Germany Digital Television Market Insight

Germany’s digital television market is driven by high consumer purchasing power, a mature electronics retail ecosystem, and strong demand for high-definition and smart TVs. The country’s focus on quality, energy efficiency, and innovative display technologies supports premium segment adoption. Consumer preference for connected entertainment systems and large-screen TVs further enhances market growth.

U.K. Digital Television Market Insight

The U.K. market is supported by widespread adoption of smart and high-resolution TVs, rising demand for home entertainment, and robust retail infrastructure. Strong interest in 4K and 50''+ TVs, coupled with ongoing technological upgrades in broadcasting and streaming services, is boosting market growth. The region also benefits from high digital literacy and consumer willingness to invest in premium viewing experiences.

North America Digital Television Market Insight

North America is projected to grow at the fastest CAGR from 2025 to 2032, driven by high consumer demand for smart TVs, large-screen displays, and advanced resolution formats. Increasing adoption of streaming services, connected home ecosystems, and gaming-focused entertainment setups are major growth factors. Continuous technological innovation, premium product launches, and strong brand presence are further accelerating market expansion.

U.S. Digital Television Market Insight

The U.S. accounted for the largest share in the North America market in 2024, underpinned by its mature consumer electronics industry, high disposable income, and strong preference for large-screen and smart TVs. The country’s focus on innovation, early adoption of 4K and UHD technologies, and advanced retail and e-commerce networks reinforce its leading position. Rising demand for home entertainment systems and connected devices further supports market growth.

Digital Television (TV) Market Share

The digital television (TV) industry is primarily led by well-established companies, including:

- Samsung (South Korea)

- Metz (Germany)

- Koninklijke Philips N.V. (Netherlands)

- Hisense Corporation Ltd. (China)

- AT&T Intellectual Property (U.S.)

- Sony Corporation (Japan)

- Changhong (China)

- LG Electronics (South Korea)

- DISH Network (U.S.)

- Verizon (U.S.)

- Funai (Japan)

- TCL (China)

- Vestel (Turkey)

- Roku, Inc. (U.S.)

- Vizio Incorporation (U.S.)

- Skyworth India Electronics Pvt Ltd. (India)

- KONKA Group (China)

Latest Developments in Global Digital Television (TV) Market

- In March 2023, DIRECTV and Newsmax Media reached an agreement to bring the Newsmax channel back to DIRECTV. This move strengthens DIRECTV’s content portfolio, enhancing its competitiveness in the U.S. pay-TV market. By reinstating Newsmax, DIRECTV caters to a broader audience segment seeking diverse news and opinion channels, potentially driving subscriber retention and attracting new viewers, especially in a market facing increasing competition from streaming platforms

- In September 2022, Toshiba announced the launch of its N300 Pro and X300 Pro hard disk drives (HDDs) aimed at businesses and creative professionals. With capacities of up to 18TB and workloads supporting up to 300TB/year, along with a five-year limited warranty, these HDDs enhance storage solutions for high-performance computing, data centers, and content creation markets. The introduction of these high-capacity, durable HDDs is likely to boost Toshiba’s presence in professional storage markets where reliability, speed, and scalability are critical

- In July 2022, Intel and MediaTek partnered to produce chips using IFS’ advanced process technologies. This collaboration aims to strengthen the semiconductor supply chain by adding a high-capacity foundry partner in Europe and North America. The deal has significant implications for the global chip market, helping both companies meet growing demand for advanced processors, improve supply flexibility, and reduce risks associated with supply chain disruptions in a highly competitive semiconductor landscape

- In July 2022, Laird Connectivity unveiled its Summit SOM 8M Plus system-on-module (SOM) portfolio. By integrating NXP Semiconductors’ multi-core processing with dual-band 2x2 Wi-Fi 5 and Bluetooth 5.3, the SOM delivers highly integrated hardware and software solutions for IoT, industrial, and smart device applications. This launch strengthens Laird Connectivity’s position in the wireless module market, offering customers faster deployment, reduced development time, and robust connectivity for next-generation wireless solutions

- In March 2022, MediaTek announced its TV System-on-Chip (SoC) supporting Dolby Vision IQ with the new Precision Detail feature. Targeted at 8K and 4K smart TVs in the Pentatonic series, this innovation enhances high-end display performance by optimizing image clarity and color accuracy. The development bolsters MediaTek’s competitiveness in the premium smart TV chipset market, enabling OEMs to deliver superior viewing experiences and meet rising consumer demand for advanced picture quality

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.