Global Direct To Consumer Fmcg Market

Market Size in USD Billion

USD

185.30 Billion

USD

430.11 Billion

2025

2033

USD

185.30 Billion

USD

430.11 Billion

2025

2033

| 2026 - 2033 | |

| USD 185.30 Billion | |

| USD 430.11 Billion | |

| % | |

|

Direct-to-Consumer FMCG Market Overview

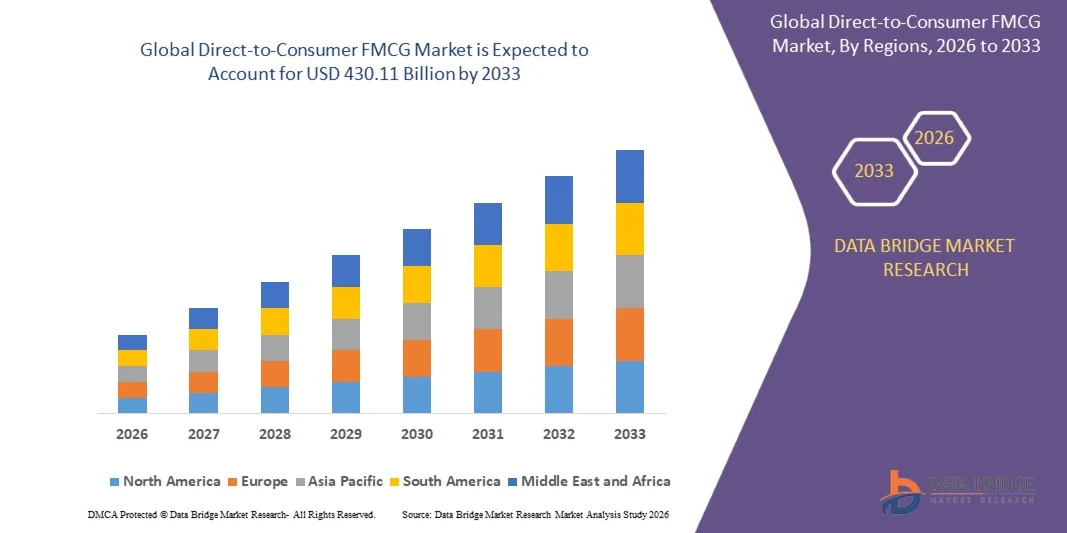

The Direct-to-Consumer FMCG Market was valued at USD 185.3 Billion in 2025 and is projected to reach USD 430.11 Billion by 2033, growing at a CAGR of 11.10% from 2026 to 2033. The market is experiencing consistent growth driven by increasing consumer preference for direct brand engagement, rising penetration of e-commerce platforms, and growing adoption of digital payment solutions. Expanding smartphone usage, rapid development of last-mile delivery networks, and increasing investments in personalized shopping experiences are further supporting market expansion across major economies. Rising popularity of subscription-based purchasing models and social commerce platforms is also contributing to sustained market growth.

The increasing global shift toward digital consumption patterns and convenience-oriented shopping, combined with advancements in data analytics and customer relationship management technologies, is encouraging FMCG companies to strengthen their direct-to-consumer strategies. Brands are increasingly leveraging their own websites, mobile applications, and social commerce channels to offer personalized products, enhance customer loyalty, and improve profit margins by reducing dependence on traditional retail intermediaries. Growing demand for premium, health-focused, and sustainable products is further accelerating the adoption of direct-to-consumer business models across the global FMCG industry.

Key Market Trends & Insights

- Asia-Pacific dominated the Direct-to-Consumer FMCG Market with the largest revenue share of 51% in 2025, supported by rapid digitalization, expanding e-commerce infrastructure, and a large consumer base with increasing online purchasing habits

- The hybrid D2C and retail brands segment led the market with a 39.7% share in 2025, driven by the ability of companies to combine online direct sales with established offline retail networks

- North America is expected to be the fastest-growing region at a CAGR of 10.1% from 2026 to 2033, fueled by increasing demand for personalized shopping experiences and rising adoption of subscription-based consumption models

- Social commerce platforms are the fastest-growing distribution channel type, projected to register a CAGR of 15.4% from 2026 to 2033, supported by rising influence of social media on purchasing decisions

- The food & beverages segment dominated the product type category with a 36.8% revenue share in 2025, led by strong consumer preference for convenient online purchasing and increasing demand for fresh, packaged, and ready-to-eat products

- Family households accounted for 34.9% of the market in 2025, preferred by high consumption frequency of daily essentials and bulk purchasing behavior

- The health & wellness products segment is the fastest-growing product type category, with a CAGR of 14.1% from 2026 to 2033, driven by increasing awareness regarding preventive healthcare and nutrition

Market Size & Forecast

- Global Market Value (2025): USD 185.3 Billion

- Expected Market Value (2033): USD 430.11 Billion

- Forecast CAGR (2026–2033): 11.10%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: North America

Report Scope and Direct-to-Consumer FMCG Market Segmentation

|

Attributes |

Direct-to-Consumer FMCG Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Procter & Gamble Company (U.S.) · Unilever PLC (U.K.) · Nestlé S.A. (Switzerland) · The Kraft Heinz Company (U.S.) · PepsiCo, Inc. (U.S.) · Colgate-Palmolive Company (U.S.) · L'Oréal S.A. (France) · The Estée Lauder Companies Inc. (U.S.) · Reckitt Benckiser Group plc (U.K.) · Johnson & Johnson (U.S.) · Henkel AG & Co. KGaA (Germany) · Marico Limited (India) · Hindustan Unilever Limited (India) · Emami Limited (India) · ITC Limited (India) · Beiersdorf AG (Germany) · Shiseido Company, Limited (Japan) |

|

Market Opportunities |

· Expansion of Subscription-Based FMCG Delivery Models · Growing Demand for Personalized Health and Wellness Products · Increasing Penetration of D2C FMCG Brands in Emerging Markets through Quick Commerce Platforms |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Direct-to-Consumer FMCG Market Trends

Trend: Rising Adoption of Social Commerce and Live Shopping Platforms

Direct-to-consumer FMCG brands are increasingly leveraging social media platforms and live commerce channels to strengthen customer engagement and drive online sales. Interactive shopping experiences, influencer marketing, and short-form video content are becoming important tools for increasing product visibility and improving conversion rates. Growing smartphone penetration and rising consumer preference for seamless digital purchasing experiences are further accelerating the trend across major markets. Social commerce has witnessed rapid growth in Asia-Pacific, particularly in China, where live-stream shopping has become a mainstream retail channel.

Companies such as L'Oréal S.A. are actively expanding their social commerce capabilities through partnerships with digital platforms and influencer-driven campaigns, enabling stronger direct consumer relationships and supporting sales growth across beauty and personal care categories.

Direct-to-Consumer FMCG Market Dynamics

Key Market Driver: Growing Preference for Direct Brand Engagement

Consumers are increasingly seeking personalized experiences, product transparency, and direct interaction with brands, which is significantly driving the growth of the Direct-to-Consumer FMCG market. Companies are utilizing customer data analytics and digital platforms to provide customized offerings, loyalty programs, and targeted promotions. The shift toward online shopping and increasing penetration of digital payment systems are further supporting the expansion of direct sales channels. Rising demand for premium and health-oriented products is encouraging FMCG companies to strengthen their digital ecosystems.

Major companies such as Unilever PLC and Procter & Gamble Company are increasing investments in digital commerce and consumer engagement platforms, while Hindustan Unilever Limited completed the acquisition of Minimalist in 2025 to strengthen its digital-first beauty portfolio and expand direct customer access.

Key Restraint/Challenge: High Customer Acquisition Costs and Intensifying Competition Among D2C Brands

A major challenge in the Direct-to-Consumer FMCG market is the increasing cost of acquiring and retaining customers amid rising competition from both established FMCG companies and emerging digital-native brands. Companies are facing higher expenditures on digital advertising, influencer collaborations, and customer engagement initiatives to maintain market share. Changes in online advertising algorithms and increasing dependence on paid promotions are affecting profitability. In addition, the growing number of brands competing across similar categories is intensifying price competition and reducing customer loyalty.

The acquisition activities undertaken by companies such as Emami Limited and ITC Limited during 2025 highlight the competitive nature of the market, where companies are relying on inorganic expansion and portfolio diversification to strengthen their position in the increasingly crowded D2C FMCG landscape.

Key Market Opportunity: Growing Demand for Personalized Health and Wellness Products

The increasing consumer focus on preventive healthcare and healthier lifestyles is creating significant opportunities for the Direct-to-Consumer FMCG market. Consumers are increasingly purchasing personalized nutrition products, dietary supplements, and wellness-focused offerings directly from brands to ensure authenticity and tailored solutions. Advances in artificial intelligence and data analytics are enabling companies to deliver customized recommendations and improve customer experiences. Growing awareness regarding clean-label, plant-based, and functional products is further supporting market expansion.

Companies such as Marico Limited strengthened their presence in this segment through the acquisition of Plix, while Emami Limited acquired a majority stake in IncNut Digital, the parent company of Vedix and SkinKraft, in 2026, reflecting increasing industry emphasis on personalized health, wellness, and beauty solutions.

Direct-to-Consumer FMCG Market Scope

The direct-to-consumer FMCG market is segmented on the basis of product type, distribution channel, business model, and consumer type.

- By Product Type

On the basis of product type, the Direct-to-Consumer FMCG Market is segmented into food & beverages, personal care & beauty products, household care products, health & wellness products, baby care products, pet care products, and others. The Food & Beverages segment dominated the market with the largest share of 36.8% in 2025, driven by strong consumer preference for convenient online purchasing and increasing demand for fresh, packaged, and ready-to-eat products. Brands are increasingly leveraging direct digital channels to offer personalized recommendations and subscription services. Rising penetration of quick commerce and same-day delivery platforms is supporting repeat purchases. Expansion of premium and organic food offerings through D2C channels is further strengthening segment leadership. Growing consumer reliance on digital grocery ecosystems continues to reinforce its dominant position.

The Health & Wellness Products segment is projected to register the fastest growth at a CAGR of 14.1% from 2026 to 2033, driven by increasing awareness regarding preventive healthcare and nutrition. Consumers are increasingly purchasing vitamins, supplements, immunity boosters, and functional foods directly from brands to ensure authenticity and product transparency. Growing emphasis on fitness and healthy lifestyles is expanding the consumer base for wellness products. Companies are introducing customized formulations and personalized health solutions through online platforms. Rising demand for clean-label and plant-based offerings is further accelerating segment expansion across major economies.

- By Distribution Channel

On the basis of distribution channel, the Direct-to-Consumer FMCG Market is segmented into brand-owned websites, mobile applications, online marketplaces, subscription-based platforms, social commerce platforms, and others. The Online Marketplaces segment dominated the market with a share of 41.3% in 2025, supported by extensive product availability and strong consumer trust in established e-commerce ecosystems. These platforms provide brands with broad customer reach and efficient logistics capabilities. Attractive discounts, customer reviews, and multiple payment options are encouraging higher transaction volumes. Continuous improvements in delivery infrastructure are enhancing customer satisfaction and retention. Increasing smartphone penetration and digital payment adoption are further strengthening segment dominance.

The Social Commerce Platforms segment is projected to register the fastest growth at a CAGR of 15.4% from 2026 to 2033, driven by rising influence of social media on purchasing decisions. Consumers are increasingly discovering and buying FMCG products through integrated shopping experiences across digital platforms. Influencer marketing and live commerce events are significantly improving product visibility and engagement. AI-based recommendation tools are enhancing personalized shopping experiences. Growing popularity of short-form video content and community-driven promotions is accelerating adoption of social commerce channels worldwide.

- By Business Model

On the basis of business model, the Direct-to-Consumer FMCG Market is segmented into pure D2C brands, hybrid D2C and retail brands, subscription-based D2C, private label D2C, community-led D2C brands, and others. The Hybrid D2C and Retail Brands segment dominated the market with the largest share of 39.7% in 2025, driven by the ability of companies to combine online direct sales with established offline retail networks. This approach enables wider market reach and strengthens customer engagement across multiple touchpoints. Brands benefit from greater flexibility in inventory management and fulfillment operations. Established retail presence also enhances consumer confidence and brand visibility. Increasing adoption of omnichannel strategies is further supporting segment leadership.

The Subscription-Based D2C segment is projected to register the fastest growth at a CAGR of 13.8% from 2026 to 2033, driven by growing consumer preference for convenience and recurring product deliveries. Subscription models are enabling companies to improve customer retention and generate predictable revenue streams. Personalized product bundles and flexible delivery schedules are increasing consumer loyalty. Rising demand for curated experiences in categories such as beauty, wellness, and food products is supporting market expansion. Advancements in data analytics and customer relationship management tools are further accelerating adoption.

- By Consumer Type

On the basis of consumer type, the Direct-to-Consumer FMCG Market is segmented into individual consumers, family households, premium consumers, health-conscious consumers, value-oriented consumers, and others. The Family Households segment dominated the market with a share of 34.9% in 2025, driven by high consumption frequency of daily essentials and bulk purchasing behavior. Families increasingly prefer direct purchasing channels to access better pricing and wider product assortments. Demand for packaged foods, personal care items, and household products remains consistently high within this consumer category. Growing urbanization and rising disposable income are contributing to stronger purchasing power. Increasing adoption of digital shopping platforms is further reinforcing segment dominance.

The Health-Conscious Consumers segment is projected to register the fastest growth at a CAGR of 14.6% from 2026 to 2033, driven by increasing awareness regarding nutrition, wellness, and product ingredients. Consumers are actively seeking natural, organic, and clean-label products through direct brand interactions. Demand for transparency and personalized product offerings is encouraging brands to expand their health-focused portfolios. Rising prevalence of lifestyle-related disorders is supporting higher spending on preventive wellness products. Expansion of digital health communities and fitness-oriented lifestyles is significantly accelerating segment growth.

Direct-to-Consumer FMCG Market Regional Analysis

Asia-Pacific dominated the direct-to-consumer FMCG market and accounted for the largest revenue share of 51% in 2025, supported by rapid digitalization, expanding e-commerce infrastructure, and a large consumer base with increasing online purchasing habits. The region benefits from widespread smartphone penetration, growing disposable income, and strong presence of domestic and international FMCG brands adopting direct sales strategies. Rising demand for convenience, personalized products, and faster delivery services is accelerating market expansion. Increasing investments in digital payment ecosystems and logistics networks are further supporting regional growth. In addition, strong adoption of social commerce and mobile-based shopping platforms is reinforcing the region's leadership position.

China Direct-to-Consumer FMCG Market Insight

China held the largest share in the Asia-Pacific Direct-to-Consumer FMCG market in 2025, supported by its highly developed e-commerce ecosystem and extensive consumer engagement through digital channels. The country has a strong logistics and fulfillment infrastructure that enables rapid product delivery and efficient inventory management. High penetration of mobile commerce and live-stream shopping platforms is significantly supporting market expansion. Strong demand for packaged foods, beauty products, and health supplements through direct channels is further driving growth. In addition, the presence of major domestic brands and increasing investments in AI-driven customer engagement are reinforcing China's market leadership.

India Direct-to-Consumer FMCG Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, driven by increasing internet penetration, rising smartphone usage, and expanding digital payment adoption. Growing consumer preference for convenience and direct brand interactions is significantly supporting market expansion. Rising demand for health products, personal care items, and packaged foods through online channels is creating strong growth opportunities. The country is also benefiting from rapid expansion of quick commerce platforms and increasing presence of emerging D2C brands. In addition, growing awareness regarding premium and personalized products is accelerating long-term market development.

Europe Direct-to-Consumer FMCG Market Insight

The Europe Direct-to-Consumer FMCG market is expanding steadily, supported by increasing preference for online shopping and rising demand for premium and sustainable products. Consumers across the region are increasingly adopting direct purchasing channels to access customized offerings and exclusive product ranges. Strong digital infrastructure and advanced delivery networks are contributing to market growth. Rising awareness regarding clean-label products and eco-friendly packaging is further supporting adoption. In addition, increasing investments by FMCG companies in omnichannel strategies are strengthening regional market development.

Germany Direct-to-Consumer FMCG Market Insight

Germany accounted for the largest share in the Europe Direct-to-Consumer FMCG market in 2025, driven by strong consumer spending, advanced e-commerce capabilities, and high demand for premium consumer goods. The country has a well-established retail and logistics ecosystem that supports seamless direct deliveries. Rising demand for organic foods, beauty products, and household essentials through digital platforms is strengthening market growth. Increasing preference for subscription-based purchasing models is further contributing to segment expansion. In addition, strong adoption of sustainable packaging solutions is reinforcing Germany's leading market position.

U.K. Direct-to-Consumer FMCG Market Insight

The U.K. market is supported by increasing consumer preference for convenience-oriented shopping and growing popularity of subscription-based product deliveries. Rising demand for health and wellness products, premium beauty items, and packaged foods is driving market expansion. Consumers are increasingly engaging with brands through social media platforms and mobile applications. Strong penetration of digital payments and same-day delivery services is further enhancing customer experiences. In addition, increasing investments in personalized marketing and customer loyalty programs are supporting sustained market growth.

North America Direct-to-Consumer FMCG Market Insight

North America is projected to grow at the fastest CAGR of 10.1% from 2026 to 2033, driven by increasing demand for personalized shopping experiences and rising adoption of subscription-based consumption models. Growing preference for direct brand engagement and premium products is significantly supporting regional market expansion. Strong investments in digital technologies, artificial intelligence, and customer analytics are enhancing consumer experiences across the region. Rising popularity of health-focused and sustainable FMCG products is further accelerating adoption. In addition, continuous innovation in fulfillment services and omnichannel retail strategies is boosting long-term market growth.

U.S. Direct-to-Consumer FMCG Market Insight

The U.S. accounted for the largest share in the North America Direct-to-Consumer FMCG market in 2025, supported by strong consumer spending and widespread adoption of digital commerce platforms. The country benefits from advanced logistics infrastructure and a high concentration of established FMCG brands operating through direct channels. Strong demand for personalized beauty products, nutritional supplements, and premium food offerings is further supporting market growth. Increasing use of data-driven marketing and AI-enabled recommendation systems is enhancing customer retention. In addition, rising popularity of subscription services and social commerce platforms is reinforcing the U.S. leadership position in the regional market.

Direct-to-Consumer FMCG Market Share

The direct-to-consumer FMCG industry is primarily led by well-established companies, including:

- Procter & Gamble Company (U.S.)

- Unilever PLC (U.K.)

- Nestlé S.A. (Switzerland)

- The Kraft Heinz Company (U.S.)

- PepsiCo, Inc. (U.S.)

- Colgate-Palmolive Company (U.S.)

- L'Oréal S.A. (France)

- The Estée Lauder Companies Inc. (U.S.)

- Reckitt Benckiser Group plc (U.K.)

- Johnson & Johnson (U.S.)

- Henkel AG & Co. KGaA (Germany)

- Marico Limited (India)

- Hindustan Unilever Limited (India)

- Emami Limited (India)

- ITC Limited (India)

- Beiersdorf AG (Germany)

- Shiseido Company, Limited (Japan)

Latest Developments in Direct-to-Consumer FMCG Market

- In May 2026, Emami announced the acquisition of a 60% stake in IncNut Digital, the parent company of D2C brands Vedix and SkinKraft, for ₹321 crore. The transaction strengthened Emami’s presence in the rapidly expanding personalized beauty and wellness segment and enhanced its portfolio with science-based skincare and haircare offerings. The development reflects the increasing importance of digital-first brands in the FMCG sector and is expected to accelerate innovation and customer engagement across direct-to-consumer channels

- In September 2025, Emami completed the acquisition of The Man Company, a premium men's grooming D2C brand. The acquisition expanded Emami’s footprint in the fast-growing male personal care segment and strengthened its omnichannel capabilities. The development highlighted the growing consolidation trend within the D2C FMCG industry as established companies seek stronger digital brand portfolios and direct access to consumers

- In September 2025, ITC completed the acquisition of Yoga Bar, a leading healthy snacks and nutrition-focused D2C brand. The move enabled ITC to strengthen its position in premium and health-oriented food categories while expanding its direct-to-consumer presence. The acquisition also demonstrated the increasing emphasis on functional foods and wellness products, which are emerging as major growth areas within the global D2C FMCG market

- In April 2025, Hindustan Unilever Limited acquired a 90.5% stake in Minimalist for approximately ₹2,706 crore. The acquisition significantly enhanced the company’s digital beauty and skincare portfolio and strengthened its presence among younger consumers seeking ingredient-focused products. The development underscored the rising importance of premium personal care brands and accelerated competition in the direct-to-consumer FMCG ecosystem

- In February 2025, Marico acquired a majority stake in Plix, a plant-based nutrition and wellness brand. The acquisition expanded Marico’s portfolio in health and functional nutrition categories and reinforced its long-term strategy of investing in digital-first consumer brands. The development reflected increasing industry focus on preventive healthcare, clean-label products, and personalized wellness solutions, which are driving growth across the D2C FMCG market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.