Global Disease Specific Medical Nutrition Market

Market Size in USD Billion

USD

26.17 Billion

USD

48.97 Billion

2025

2033

USD

26.17 Billion

USD

48.97 Billion

2025

2033

| 2026 - 2033 | |

| USD 26.17 Billion | |

| USD 48.97 Billion | |

| % | |

|

Disease-Specific Medical Nutrition Market Size

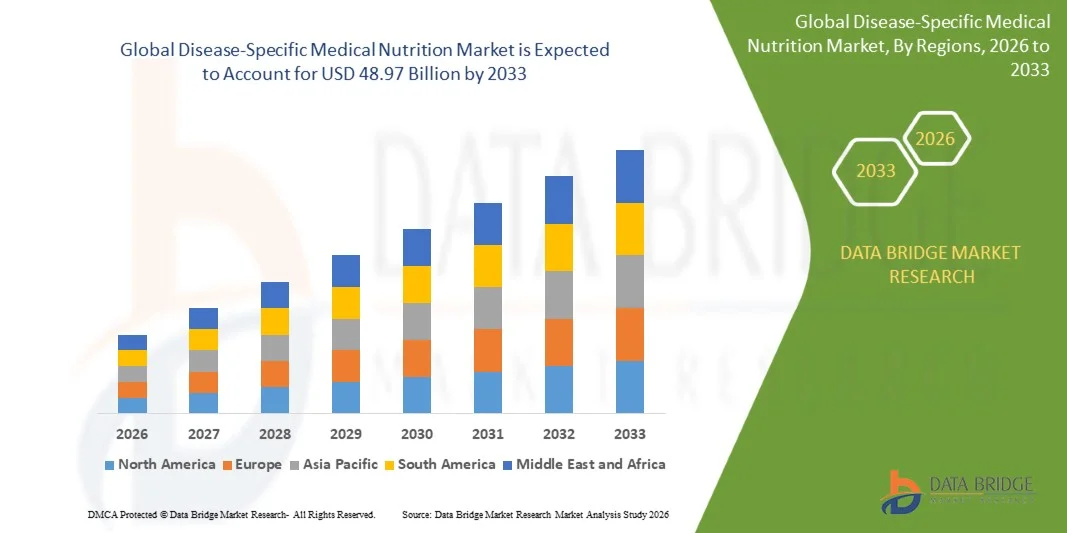

- The global disease-specific medical nutrition market size was valued at USD 26.17 billion in 2025 and is expected to reach USD 48.97 billion by 2033, at a CAGR of 8.15% during the forecast period

- The market growth is largely fueled by the rising prevalence of chronic diseases such as diabetes, cancer, renal disorders, and gastrointestinal conditions, which is increasing the need for targeted nutritional interventions in clinical care settings

- Furthermore, the growing aging population and higher incidence of disease-related malnutrition are strengthening the demand for specialized nutritional formulations, while advancements in medical nutrition science and improved hospital adoption are accelerating the use of disease-specific dietary solutions, thereby significantly supporting market expansion

Disease-Specific Medical Nutrition Market Analysis

- Disease-specific medical nutrition refers to clinically formulated dietary products designed to meet the unique nutritional requirements of patients suffering from specific health conditions such as diabetes, oncology-related complications, renal impairment, and metabolic disorders

- The increasing reliance on evidence-based nutritional therapy in hospitals, home care, and long-term care facilities is driving adoption, as these products help improve patient recovery outcomes, manage disease progression, and address nutrient deficiencies associated with chronic illnesses

- North America dominated the disease-specific medical nutrition market with a share of 47.2% in 2025, due to a high prevalence of chronic diseases such as cancer, diabetes, and renal disorders, along with strong adoption of advanced clinical nutrition therapies in hospital and homecare settings

- Asia-Pacific is expected to be the fastest growing region in the disease-specific medical nutrition market during the forecast period due to rising healthcare expenditure, increasing disease burden, and improving access to clinical nutrition therapies in countries such as China, India, and Japan

- Enteral nutrition segment dominated the market with a market share of 45.5% in 2025, due to its strong clinical preference for patients with functional gastrointestinal tracts requiring long-term nutritional support. Hospitals and critical care settings widely adopt enteral feeding owing to its cost efficiency, lower infection risk, and ability to maintain gut integrity

Report Scope and Disease-Specific Medical Nutrition Market Segmentation

|

Attributes |

Disease-Specific Medical Nutrition Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Disease-Specific Medical Nutrition Market Trends

“Rising Adoption of Personalized Disease-Specific Medical Nutrition Solutions”

- A significant trend in the disease-specific medical nutrition market is the increasing shift toward personalized clinical nutrition formulations designed to meet patient-specific metabolic and disease-related requirements, particularly in conditions such as oncology, diabetes, renal disorders, and gastrointestinal diseases. This trend is being driven by advancements in nutritional science and growing integration of clinical data into dietary planning within healthcare systems

- For instance, Abbott Laboratories offers specialized medical nutrition products such as Ensure and Glucerna that are widely used in hospitals and homecare settings for patients requiring targeted nutritional management in diabetes and recovery care. Such solutions support improved patient outcomes by addressing condition-specific dietary needs under medical supervision

- The integration of precision medicine with clinical nutrition is expanding as healthcare providers increasingly tailor nutritional interventions based on biomarkers, disease progression, and treatment response. This is strengthening the role of disease-specific nutrition in improving therapeutic effectiveness and patient recovery rates

- Hospitals and clinical institutions are increasingly incorporating nutrition therapy into standard treatment protocols for chronic and acute conditions, enhancing the use of specialized formulas in critical care and long-term disease management. This is improving recovery efficiency and reducing complication risks associated with malnutrition

- The rising focus on preventive healthcare is also contributing to demand for condition-specific nutrition solutions aimed at managing disease progression and reducing hospitalization rates. This shift is encouraging earlier nutritional intervention across high-risk patient populations

- The market is witnessing growing collaboration between healthcare providers and nutrition companies to develop scientifically validated formulations for complex disease conditions. This is reinforcing the transition toward more targeted, evidence-based medical nutrition approaches globally

Disease-Specific Medical Nutrition Market Dynamics

Driver

“Growing Prevalence of Chronic Diseases Requiring Clinical Nutrition Support”

- The increasing global burden of chronic diseases such as cancer, diabetes, chronic kidney disease, and gastrointestinal disorders is significantly driving the demand for disease-specific medical nutrition solutions that support patient recovery and long-term disease management. These conditions often require controlled nutritional intake to manage symptoms, improve immunity, and enhance treatment outcomes

- For instance, Nestlé Health Science provides specialized medical nutrition products such as Peptamen and Modulen IBD that are widely used in managing malabsorption disorders and inflammatory bowel disease in clinical settings. These formulations help patients maintain adequate nutrition during disease progression and medical treatment

- The rising incidence of lifestyle-related disorders is increasing the need for structured nutritional interventions that complement pharmacological therapies and improve patient quality of life. Healthcare systems are increasingly adopting medical nutrition as an integral part of chronic disease management protocols

- The aging global population is contributing to higher demand for disease-specific nutrition, as elderly individuals are more susceptible to metabolic disorders and require targeted dietary support. This is strengthening the role of clinical nutrition in geriatric care management

- The continuous rise in chronic disease prevalence is reinforcing long-term dependence on medical nutrition products as part of standard treatment pathways. This sustained demand is positioning disease-specific nutrition as a critical component of modern healthcare delivery

Restraint/Challenge

“High Product Cost and Limited Reimbursement Coverage”

- The disease-specific medical nutrition market faces challenges due to the high cost of specialized formulations, which are developed using advanced clinical research, premium ingredients, and strict regulatory compliance standards. These cost factors make such products less accessible to price-sensitive patient populations, particularly in developing regions

- For instance, Fresenius Kabi produces clinically specialized nutrition solutions used in hospital and critical care settings, where high formulation and production costs contribute to elevated end-user pricing. This limits broader adoption in healthcare systems with constrained budget allocations for nutritional therapies

- Limited reimbursement policies in several healthcare systems restrict patient access to disease-specific medical nutrition products, as coverage is often not fully extended for long-term nutritional therapy. This creates financial barriers for patients requiring sustained nutritional support

- The lack of standardized reimbursement frameworks across different regions results in inconsistent adoption rates and uneven market penetration. Patients in non-reimbursed settings often rely on out-of-pocket expenditure, reducing overall product affordability

- The combined impact of high pricing and restricted reimbursement continues to challenge market expansion, requiring manufacturers and policymakers to work toward cost optimization and improved healthcare coverage mechanisms

Disease-Specific Medical Nutrition Market Scope

The market is segmented on the basis of type, product type, route of administration, application, and distribution channel.

• By Type

On the basis of type, the disease-specific medical nutrition market is segmented into enteral nutrition, parenteral nutrition, oral nutritional supplements, pediatric clinical nutrition, and geriatric clinical nutrition. The enteral nutrition segment dominated the largest market revenue share of 45.5% in 2025 due to its strong clinical preference for patients with functional gastrointestinal tracts requiring long-term nutritional support. Hospitals and critical care settings widely adopt enteral feeding owing to its cost efficiency, lower infection risk, and ability to maintain gut integrity. Increasing prevalence of chronic diseases, trauma cases, and post-surgical recovery needs further strengthens its demand. The segment benefits from established clinical protocols and availability of advanced feeding formulations tailored to disease-specific requirements.

The pediatric clinical nutrition segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by rising awareness of early-life nutrition and increasing incidence of pediatric metabolic and gastrointestinal disorders. Growing focus on managing malnutrition and growth deficiencies in infants and children supports the adoption of specialized nutritional formulations. Healthcare providers are increasingly recommending targeted nutrition therapies to improve recovery outcomes in pediatric patients. Expanding healthcare access in emerging economies and improved diagnostic rates also contribute to segment expansion.

• By Product Type

On the basis of product type, the market is segmented into amino acid formulations, carbohydrate-based nutrition, lipid emulsions, vitamin and mineral blends, trace elements, and oral nutritional supplements. The oral nutritional supplements segment held the largest market revenue share in 2025 due to its widespread use in managing malnutrition across hospital and homecare settings. These products are easy to administer, cost-effective, and suitable for a broad patient base including elderly and chronically ill individuals. Rising incidence of disease-related nutritional deficiencies further supports consistent demand. Strong availability across healthcare and retail channels enhances accessibility and adoption.

The amino acid formulations segment is projected to witness the fastest growth rate from 2026 to 2033, driven by increasing use in critical care and specialized disease management such as liver disorders, kidney diseases, and cancer-related cachexia. These formulations play a key role in supporting metabolic requirements in patients who cannot tolerate standard nutrition. Advancements in precision nutrition and personalized therapeutic approaches are strengthening segment growth. Rising ICU admissions and expanding hospital infrastructure further accelerate adoption.

• By Route of Administration

On the basis of route of administration, the market is segmented into oral, enteral tube feeding, and parenteral intravenous nutrition. The oral route segment dominated the largest market revenue share in 2025 due to its ease of use, patient compliance, and suitability for mild to moderate nutritional deficiencies. It is widely preferred in outpatient and homecare settings where patients require long-term nutritional support without invasive procedures. Growing awareness of preventive healthcare and early nutritional intervention further drives adoption. Availability of disease-specific oral formulations enhances its clinical relevance across multiple conditions.

The parenteral nutrition segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing cases of severe gastrointestinal dysfunction and critical illness requiring intravenous feeding. Hospitals and intensive care units are expanding their use of parenteral nutrition for patients unable to absorb nutrients through the digestive tract. Technological advancements in formulation stability and infusion systems are improving safety and efficiency. Rising surgical procedures and cancer treatments further contribute to segment expansion.

• By Application

On the basis of application, the market is segmented into cancer care, gastrointestinal disorders, neurological diseases, diabetes management, obesity, renal failure, pulmonary diseases, and pediatric malnutrition. The cancer care segment held the largest market revenue share in 2025 due to the high prevalence of cancer-related malnutrition and increased use of nutritional therapy during chemotherapy and radiotherapy. Patients undergoing cancer treatment often require specialized nutrition to maintain strength and improve treatment outcomes. Growing oncology infrastructure and supportive care guidelines further reinforce demand. Rising global cancer incidence continues to strengthen segment dominance.

The obesity segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by increasing prevalence of obesity-related metabolic disorders and growing demand for structured nutritional interventions. Healthcare systems are focusing on medical nutrition therapies to support weight management and reduce comorbidities. Rising awareness of lifestyle-related diseases and preventive healthcare approaches further supports growth. Development of tailored nutritional formulations for metabolic control is accelerating adoption across clinical settings.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into hospitals, compounding pharmacies, retail pharmacies, and e-commerce platforms. The hospitals segment dominated the largest market revenue share in 2025 due to the high volume of critical care treatments and inpatient nutritional therapy requirements. Hospitals serve as the primary point of administration for enteral and parenteral nutrition in severely ill patients. Strong clinical infrastructure and availability of specialized nutrition support teams further enhance segment dominance. Increasing hospitalization rates for chronic and acute diseases continue to support demand.

The e-commerce platforms segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising digital healthcare adoption and increasing preference for convenient home delivery of nutritional products. Patients managing chronic conditions are increasingly purchasing oral nutritional supplements through online channels. Expanding internet penetration and growing telehealth integration further accelerate segment expansion. Competitive pricing and wide product availability enhance consumer accessibility and adoption.

Disease-Specific Medical Nutrition Market Regional Analysis

- North America dominated the disease-specific medical nutrition market with the largest revenue share of 47.2% in 2025, driven by a high prevalence of chronic diseases such as cancer, diabetes, and renal disorders, along with strong adoption of advanced clinical nutrition therapies in hospital and homecare settings

- The region benefits from well-established healthcare infrastructure, high awareness of disease-related malnutrition, and strong presence of leading medical nutrition companies. Increasing demand for personalized nutrition support and early therapeutic intervention further strengthens market growth

- High healthcare expenditure and favorable reimbursement systems also support widespread utilization of disease-specific nutrition solutions across the region

U.S. Disease-Specific Medical Nutrition Market Insight

The U.S. held the largest revenue share within North America in 2025, driven by a high burden of chronic and lifestyle-related diseases and strong integration of medical nutrition into clinical treatment protocols. Hospitals and long-term care facilities widely adopt enteral and parenteral nutrition for critical care and post-operative recovery patients. Growing emphasis on oncology nutrition support and diabetes management further accelerates demand. Advanced healthcare systems, strong R&D activities, and presence of major nutrition companies contribute significantly to market expansion.

Europe Disease-Specific Medical Nutrition Market Insight

The Europe disease-specific medical nutrition market is projected to expand at a steady CAGR during the forecast period, supported by increasing aging population and rising incidence of chronic diseases requiring specialized nutritional support. Strong regulatory frameworks and established clinical nutrition guidelines promote structured adoption in hospitals and care facilities. Growing focus on elderly nutrition and post-acute care recovery further supports market growth. Expansion of home healthcare services and rising awareness of disease-specific dietary management also contribute to regional demand.

U.K. Disease-Specific Medical Nutrition Market Insight

The U.K. market is anticipated to grow at a notable CAGR during the forecast period, driven by increasing prevalence of malnutrition in hospitalized and elderly populations. Healthcare providers are increasingly integrating medical nutrition therapy into treatment pathways for cancer, gastrointestinal disorders, and neurological conditions. Rising demand for home-based nutritional support and growing use of oral nutritional supplements further support market growth. Strong NHS-driven healthcare frameworks and improved clinical awareness contribute to wider adoption of disease-specific nutrition solutions.

Germany Disease-Specific Medical Nutrition Market Insight

The Germany market is expected to expand at a considerable CAGR during the forecast period, supported by strong healthcare infrastructure and high focus on preventive and therapeutic nutrition. Increasing incidence of chronic diseases and rising geriatric population are key factors driving demand for specialized nutrition products. Hospitals widely adopt enteral and parenteral nutrition in critical care management. Strong emphasis on clinical efficiency, product quality, and nutritional precision further supports market expansion across healthcare settings.

Asia-Pacific Disease-Specific Medical Nutrition Market Insight

The Asia-Pacific disease-specific medical nutrition market is poised to grow at the fastest CAGR from 2026 to 2033, driven by rising healthcare expenditure, increasing disease burden, and improving access to clinical nutrition therapies in countries such as China, India, and Japan. Rapid urbanization and growing awareness of disease-related malnutrition are accelerating adoption across hospitals and homecare settings. Expanding healthcare infrastructure and government initiatives to improve nutrition support systems further boost growth. Increasing availability of affordable nutritional products also enhances market penetration across the region.

Japan Disease-Specific Medical Nutrition Market Insight

The Japan market is witnessing steady growth due to its rapidly aging population and high prevalence of chronic conditions requiring specialized nutritional care. Strong focus on elderly healthcare and long-term care facilities supports consistent demand for oral and enteral nutrition products. Integration of advanced clinical nutrition practices into hospital treatment protocols further strengthens adoption. High emphasis on quality healthcare and precision-based nutritional therapy drives market expansion in both institutional and homecare settings.

China Disease-Specific Medical Nutrition Market Insight

The China disease-specific medical nutrition market accounted for the largest revenue share in Asia-Pacific in 2025, driven by a large patient pool, increasing prevalence of chronic diseases, and expanding healthcare infrastructure. Rising awareness of clinical nutrition therapy and growing hospital admissions for critical illnesses support strong demand for enteral and parenteral nutrition. Government initiatives to improve healthcare accessibility and nutrition management further contribute to growth. Strong domestic manufacturing capabilities and availability of cost-effective products also enhance market expansion.

Disease-Specific Medical Nutrition Market Share

The disease-specific medical nutrition industry is primarily led by well-established companies, including:

- Nestlé S.A. (Switzerland)

- Danone S.A. (France)

- Abbott Laboratories (U.S.)

- Fresenius Kabi AG (Germany)

- Baxter International Inc. (U.S.)

- B. Braun Melsungen AG (Germany)

- Mead Johnson Nutrition (U.S.)

- Arla Foods Ingredients Group P/S (Denmark)

- Meiji Holdings Co., Ltd. (Japan)

- Haleon plc (U.K.)

- Nutricia (Netherlands)

- Reckitt Benckiser Group plc (U.K.)

- Société des Produits Nestlé S.A. (Switzerland)

- LONZA Group AG (Switzerland)

- Grifols S.A. (Spain)

Latest Developments in Global Disease-Specific Medical Nutrition Market

- In March 2026, Nestlé introduced an innovative complete nutritional solution designed for children with special medical nutrition needs, strengthening its pediatric clinical nutrition portfolio and improving access to disease-specific dietary management in pediatric care. The launch enhances treatment support for children with metabolic and chronic conditions by offering tailored nutrient-dense formulations, thereby increasing clinical adoption in hospitals and homecare settings. This development reinforces Nestlé’s leadership in pediatric medical nutrition and supports growing demand for specialized child-focused therapeutic nutrition solutions globally

- In December 2025, Abbott Laboratories launched an advanced disease-specific medical nutrition formulation aimed at improving metabolic support for critically ill and chronically diseased patients. The product expansion enhances Abbott’s clinical nutrition offerings across hospital care settings by addressing high-demand conditions such as oncology recovery and renal impairment. This development strengthens the company’s position in precision-based medical nutrition and supports increased adoption of scientifically formulated therapeutic nutrition solutions in intensive care environments

- In April 2025, Arla Foods Ingredients expanded its presence in the medical nutrition market by introducing new milk-based clinical ingredient solutions targeting disease-specific applications. The innovation improves formulation flexibility for manufacturers developing high-protein and easily digestible medical nutrition products. This development enhances product efficiency in managing malnutrition and recovery care, supporting growing demand for clean-label and high-quality nutritional ingredients in clinical nutrition formulations

- In June 2024, Fresenius Kabi introduced an enhanced parenteral nutrition solution aimed at improving intravenous nutritional support for critically ill patients with severe gastrointestinal dysfunction. The development strengthens its hospital-based nutrition portfolio by improving nutrient stability and infusion safety. This advancement supports rising demand for intensive care nutrition therapies and reinforces Fresenius Kabi’s strong position in parenteral nutrition across global healthcare systems

- In October 2023, Nutricia (Danone) pioneered its first medical nutrition drink formulated for pediatric patients using real fruit and vegetable ingredients, improving palatability and acceptance among children requiring long-term nutritional support. The innovation enhances adherence to therapeutic nutrition regimens and supports better clinical outcomes in pediatric malnutrition and disease management. This development strengthens Nutricia’s leadership in pediatric medical nutrition by combining clinical efficacy with improved taste and natural ingredient positioning

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Disease Specific Medical Nutrition Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Disease Specific Medical Nutrition Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Disease Specific Medical Nutrition Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.