Global Dna Fragmentation Technique Market

Market Size in USD Billion

USD

9.23 Billion

USD

22.69 Billion

2025

2033

USD

9.23 Billion

USD

22.69 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 9.23 Billion |

Market Size (Forecast Year) |

USD 22.69 Billion |

CAGR |

% |

Major Markets Players |

|

DNA Fragmentation Technique Market Overview

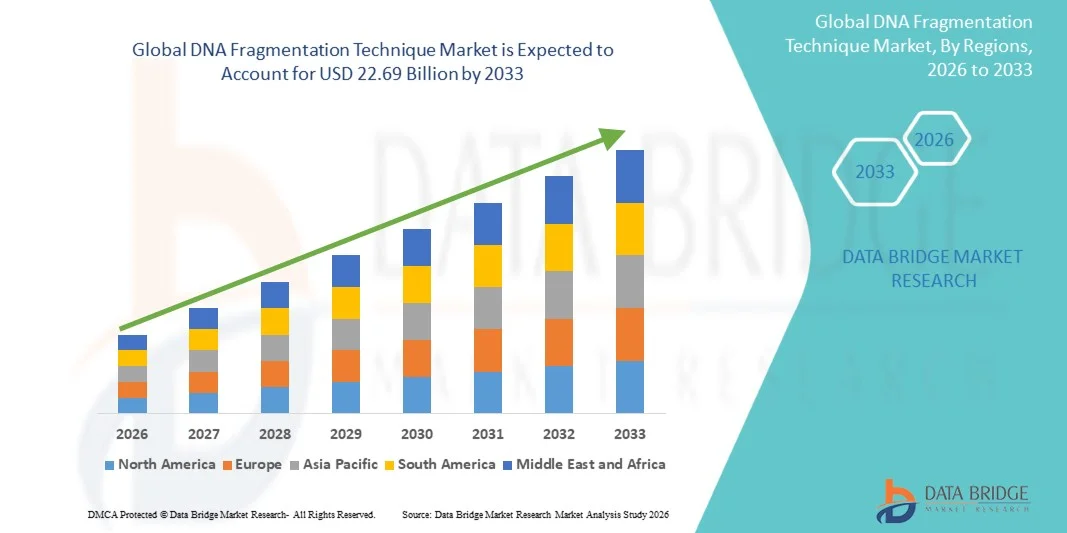

The DNA Fragmentation Technique Market was valued at USD 9.23 billion in 2025 and is projected to reach USD 22.69 billion by 2033, growing at a CAGR of 11.90% from 2026 to 2033. The market is witnessing steady growth driven by the increasing adoption of next-generation sequencing (NGS), rising demand for high-quality genomic sample preparation, and expanding applications across clinical diagnostics, oncology research, and precision medicine.

The growing prevalence of genetic disorders and cancer, along with rapid advancements in genomics and molecular biology, is significantly boosting the need for accurate and efficient DNA fragmentation methods. Mechanical, enzymatic, and microfluidics-based fragmentation technologies are increasingly being integrated into automated workflows in pharmaceutical companies, research laboratories, and diagnostic centers to improve sequencing accuracy, reduce processing time, and support large-scale genomic studies.

Key Market Trends & Insights

- North America dominated the DNA Fragmentation Technique Market with the largest revenue share of 36.42% in 2025, supported by strong genomic research infrastructure, high NGS adoption, and the presence of leading biotechnology and sequencing companies.

- The Assisted Reproductive Technology segment led the market with a 46.12% share in 2025, driven by the rising infertility rates and increasing use of advanced sperm DNA integrity testing in IVF and ICSI procedures.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by expanding genomics research programs, rising healthcare investments, and increasing adoption of precision medicine in China, India, and Japan.

- Medication is the fastest-growing treatment type, projected to register a CAGR of 8.4%, reflecting the surge in increasing use of antioxidant therapies and pharmacological interventions aimed at reducing sperm DNA damage.

- The SCSA (Sperm Chromatin Structure Assay) segment dominated the test type category with a 38.56% revenue share in 2025, led by high accuracy, strong clinical validation, and widespread use in fertility clinics for assessing sperm DNA integrity.

- Next-Generation Sequencing (NGS) accounted for 48.91% of the market, preferred by rapid expansion of genomic sequencing projects and increasing demand for high-quality DNA fragmentation in library preparation.

- The Clinical Diagnostics segment is the fastest-growing application category, with a CAGR of 9.1%, driven by the increasing adoption of molecular diagnostics in fertility, oncology, and genetic disease screening.

Market Size & Forecast

- Global Market Value (2025): USD 9.23 Billion

- Expected Market Value (2033): USD 22.69 Billion

- Forecast CAGR (2026–2033): 11.90%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and DNA Fragmentation Technique Market Segmentation

|

Attributes |

DNA Fragmentation Technique Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Illumina, Inc. (U.S.) · Thermo Fisher Scientific Inc. (U.S.) · Agilent Technologies, Inc. (U.S.) · QIAGEN (Netherlands) · Roche Holding AG (Switzerland) · Bio-Rad Laboratories, Inc. (U.S.) · Takara Bio Inc. (Japan) · New England Biolabs, Inc. (U.S.) · PerkinElmer (U.S.) · Danaher Corporation (U.S.) · Beckman Coulter, Inc. (U.S.) · Oxford Nanopore Technologies plc (U.K.) · 10x Genomics, Inc. (U.S.) · BD (U.S.) · Promega Corporation (U.S.) · Fluidigm Corporation (U.S.) · Eppendorf SE (Germany) · Hamilton Company (U.S.) · Merck KGaA (Germany) · Tecan Group Ltd. (Switzerland) |

|

Market Opportunities |

· Expansion of liquid biopsy and circulating tumor DNA (ctDNA) testing · Growing adoption of fully automated, high-throughput library preparation platforms in NGS workflows · Increasing investment in population-scale genomics and biobanking projects |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

DNA Fragmentation Technique Market Trends

Trend: Rising Integration of Automated Library Preparation in Genomics Workflows

Research and clinical laboratories are increasingly adopting automated DNA fragmentation systems integrated with NGS library preparation platforms to improve reproducibility, reduce human error, and enhance throughput in large-scale genomic studies. The shift toward standardized, high-efficiency workflows is accelerating adoption of microfluidics-based and enzymatic fragmentation technologies across oncology, rare disease research, and precision medicine programs, while digital tracking and AI-assisted QC tools are improving fragment size accuracy and process control. For instance, automated sample-to-sequencing platforms used in high-throughput cancer genome projects are streamlining fragmentation and downstream sequencing preparation.

DNA Fragmentation Technique Market Dynamics

Key Market Driver: Expanding Adoption of Next-Generation Sequencing in Clinical and Research Applications

The rapid growth of NGS-based applications in oncology, genetic disease screening, and infectious disease research is driving strong demand for accurate DNA fragmentation techniques that ensure optimal library preparation and sequencing efficiency. Increasing investments in precision medicine initiatives and population-scale genomic mapping projects are further strengthening market growth, with pharmaceutical companies and research institutes integrating advanced fragmentation methods to improve data quality and sequencing depth. For instance, national genome sequencing programs supporting large cancer and rare disease databases are significantly increasing the use of enzymatic and automated fragmentation systems.

Key Restraint/Challenge: High Dependence on Skilled Operation and Standardization Issues

Despite technological advancements, variability in fragmentation outcomes due to protocol sensitivity, operator expertise, and sample quality remains a key challenge limiting consistent adoption across smaller laboratories and emerging markets. The need for specialized training, strict protocol optimization, and compatibility with diverse sequencing platforms increases operational complexity and restricts scalability in cost-sensitive settings. For instance, variability in DNA shearing efficiency across different laboratory setups continues to impact reproducibility in multi-site genomic studies.

Key Market Opportunity: Expansion of Liquid Biopsy and Cell-Free DNA Applications

The growing use of liquid biopsy and cell-free DNA (cfDNA) analysis in early cancer detection and non-invasive prenatal testing is creating significant opportunities for highly precise DNA fragmentation technologies capable of handling low-input and degraded samples. Increasing clinical adoption of cfDNA-based diagnostics is driving demand for ultra-sensitive, contamination-free fragmentation systems that ensure accurate downstream sequencing results, while advancements in microfluidics and automated platforms are improving scalability and clinical integration. For instance, cfDNA-based oncology screening programs are expanding the need for high-efficiency fragmentation in diagnostic laboratories worldwide.

DNA Fragmentation Technique Market Scope

The DNA fragmentation technique market is segmented on the basis of treatment type, test type, application, distribution channel, and end user.

- By Treatment Type

On the basis of treatment type, the DNA Fragmentation Technique Market is segmented into assisted reproductive technology (ART), varicocele surgery, and medication. The Assisted Reproductive Technology (ART) segment dominated the market with the largest share of 46.12% in 2025, driven by rising infertility rates and increasing use of advanced sperm DNA integrity testing in IVF and ICSI procedures. ART clinics extensively rely on DNA fragmentation analysis to improve embryo selection and pregnancy success rates, making it a critical diagnostic step in fertility treatment workflows. Growing awareness of male infertility and its genetic factors is further strengthening adoption across fertility centers. Continuous advancements in reproductive genetics and laboratory automation are improving testing accuracy and efficiency. Increasing global demand for personalized fertility treatments is also supporting segment expansion. The segment benefits from strong clinical integration of DNA fragmentation testing in assisted conception procedures.

The Medication segment is expected to register the fastest growth at a CAGR of 8.4% from 2026 to 2033, driven by increasing use of antioxidant therapies and pharmacological interventions aimed at reducing sperm DNA damage. Rising clinical focus on non-invasive infertility management is supporting demand for targeted drug-based treatments. Growing research into oxidative stress and its role in DNA fragmentation is further accelerating innovation in therapeutic approaches. Pharmaceutical companies are investing in novel compounds to improve sperm DNA integrity. Increasing preference for early-stage medical intervention before ART procedures is boosting adoption. For instance, antioxidant-based treatment regimens are increasingly prescribed in idiopathic infertility cases to improve reproductive outcomes.

- By Test Type

On the basis of test type, the market is segmented into SCSA (Sperm Chromatin Structure Assay), TUNEL assay, Halo test, Comet assay, and unexplained infertility testing. The SCSA segment dominated the market with a 38.56% share in 2025, due to its high accuracy, strong clinical validation, and widespread use in fertility clinics for assessing sperm DNA integrity. SCSA provides rapid, reproducible results, making it a preferred diagnostic tool in assisted reproduction settings. Its standardized protocol allows large-scale clinical adoption across developed healthcare systems. Increasing infertility screening programs are further driving demand. Strong correlation between SCSA results and IVF outcomes enhances its clinical relevance. The test is widely integrated into male infertility diagnostic pathways globally.

The TUNEL assay segment is projected to witness the fastest growth at a CAGR of 8.7% from 2026 to 2033, driven by its high sensitivity in detecting DNA strand breaks at a cellular level. Growing research applications in reproductive biology and oncology are increasing its adoption. The assay is widely used in both clinical diagnostics and academic research for apoptosis and DNA damage evaluation. Advancements in fluorescence-based detection systems are improving test efficiency and accuracy. Increasing use in unexplained infertility cases is further supporting demand. For instance, TUNEL-based testing is increasingly applied in IVF labs to evaluate sperm DNA damage prior to embryo selection.

- By Application

On the basis of application, the market is segmented into next-generation sequencing (NGS), epigenetics research, clinical diagnostics, forensic science, and animal genetics. The Next-Generation Sequencing (NGS) segment dominated the market with a 48.91% share in 2025, driven by rapid expansion of genomic sequencing projects and increasing demand for high-quality DNA fragmentation in library preparation. Accurate fragmentation is essential for sequencing efficiency, read depth, and data reliability in large-scale genomic studies. Rising investments in precision medicine and cancer genomics are further strengthening demand. Pharmaceutical companies and research institutions extensively use fragmentation techniques to ensure sequencing accuracy. Continuous advancements in automated fragmentation platforms are enhancing throughput and reproducibility. The segment benefits from strong integration with genomic research pipelines worldwide.

The Clinical Diagnostics segment is expected to register the fastest growth at a CAGR of 9.1% from 2026 to 2033, driven by increasing adoption of molecular diagnostics in fertility, oncology, and genetic disease screening. Rising demand for early and non-invasive disease detection is expanding the use of DNA fragmentation-based assays. Growth in personalized medicine is further accelerating clinical applications. Healthcare providers are integrating advanced DNA testing into routine diagnostic workflows. Increasing awareness of genetic risk factors is boosting demand for precise molecular analysis. For instance, fragmentation-based cfDNA testing is increasingly used in cancer diagnostics and prenatal screening programs.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, pharmacies & drug stores, and online pharmacies. The Hospital Pharmacies segment dominated the market with a 52.44% share in 2025, as most DNA fragmentation tests and related reagents are administered within clinical and hospital-based fertility and diagnostic laboratories. Hospitals act as primary centers for infertility diagnosis and genetic testing, ensuring high sample throughput and standardized testing protocols. Strong integration of laboratory services within hospital systems supports consistent demand. Increasing hospital-based IVF treatments are further driving adoption. Advanced diagnostic infrastructure in tertiary care centers enhances market dominance. The segment benefits from centralized testing and physician-led diagnostics.

The Online Pharmacies segment is expected to witness the fastest growth at a CAGR of 8.2% from 2026 to 2033, driven by increasing availability of diagnostic kits and consumables through digital healthcare platforms. Rising adoption of home-based sample collection kits and direct-to-consumer genetic testing is supporting growth. Convenience, wider accessibility, and competitive pricing are encouraging online distribution. Expanding e-health infrastructure is further strengthening market penetration. Growing awareness of fertility testing is boosting online demand. For instance, at-home DNA-based fertility screening kits are increasingly being ordered through digital pharmacy platforms.

- By End User

On the basis of end user, the market is segmented into hospitals & clinics, fertility centers, research institutes, and other end users. The Fertility Centers segment dominated the market with a 44.37% share in 2025, driven by high utilization of DNA fragmentation testing in assisted reproductive procedures. These centers rely heavily on sperm DNA integrity analysis to improve IVF success rates and optimize embryo selection. Increasing infertility cases globally are further strengthening demand. Fertility centers integrate advanced molecular diagnostics into routine patient evaluation. Rising adoption of personalized reproductive medicine is boosting testing frequency. Strong focus on improving clinical pregnancy outcomes supports segment leadership. The segment benefits from specialized reproductive healthcare infrastructure.

The Research Institutes segment is expected to witness the fastest growth at a CAGR of 8.9% from 2026 to 2033, driven by expanding genomic research, cancer studies, and molecular biology investigations. Increasing government and private funding for life sciences research is supporting adoption of DNA fragmentation techniques. Institutes are extensively using these methods for studying DNA damage, repair mechanisms, and disease pathways. Growth in academic collaborations and international research programs is further accelerating demand. Advanced laboratory infrastructure is improving experimental accuracy and scalability. For instance, research institutes involved in cancer genomics are increasingly using fragmentation-based sequencing workflows for biomarker discovery.

DNA Fragmentation Technique Market Regional Analysis

North America dominated the DNA Fragmentation Technique Market with the largest revenue share of 36.42% in 2025, supported by strong genomic research infrastructure, high NGS adoption, and the presence of leading biotechnology and sequencing companies. The region also benefits from significant investments in precision medicine, oncology research, and fertility diagnostics, which drive continuous demand for high-quality DNA fragmentation solutions. Widespread integration of automated library preparation systems and enzymatic fragmentation technologies across research institutes and clinical laboratories further strengthens market leadership. Increasing government and private funding for genomic sequencing programs continues to support innovation and large-scale adoption of advanced molecular biology tools in the region.

U.S. DNA Fragmentation Technique Market Insight

The U.S. DNA fragmentation technique market is witnessing strong growth due to extensive investments in genomics research, precision medicine programs, and advanced cancer diagnostics. The country’s well-established biotechnology ecosystem, along with high adoption of next-generation sequencing platforms, is driving significant demand for high-quality DNA fragmentation methods. Increasing use of enzymatic and automated fragmentation technologies in clinical laboratories and research institutes is further enhancing workflow efficiency and reproducibility. In addition, rising focus on fertility diagnostics, rare disease research, and large-scale genomic mapping projects continues to accelerate market expansion across the U.S.

Europe DNA Fragmentation Technique Market Insight

The Europe DNA fragmentation technique market remains a major contributor to global revenue, driven by strong academic research networks, advanced healthcare infrastructure, and increasing adoption of molecular diagnostics across clinical and research settings. The widespread use of NGS-based applications in oncology, reproductive health, and genetic disease screening is supporting market expansion across the region. Increasing investments in precision medicine initiatives, coupled with strong regulatory support for genomic research, continue to enhance adoption of advanced fragmentation technologies. High penetration of automated laboratory systems and standardized testing protocols further strengthens market growth throughout Europe.

U.K. DNA Fragmentation Technique Market Insight

The U.K. DNA fragmentation technique market is experiencing steady growth, supported by strong biotechnology research activity, expanding fertility diagnostics demand, and increasing adoption of NGS-based workflows. Rising investments in genomic medicine programs and biobank initiatives are contributing to higher utilization of DNA fragmentation methods in research and clinical applications. Integration of advanced enzymatic and automated fragmentation platforms is improving workflow efficiency and data accuracy. Furthermore, strong collaborations between academic institutes and life science companies are accelerating innovation in molecular diagnostics across the country.

Germany DNA Fragmentation Technique Market Insight

The Germany DNA fragmentation technique market is expanding steadily due to the country’s strong pharmaceutical sector, advanced molecular biology research capabilities, and growing focus on precision medicine. Increasing use of DNA fragmentation in oncology research, genetic testing, and fertility diagnostics is driving market adoption. Continuous technological advancements in automated sample preparation and sequencing platforms are enhancing laboratory efficiency. Strong government support for life sciences innovation and increasing collaboration between research institutes and biotech companies are further supporting market growth in Germany.

Asia-Pacific DNA Fragmentation Technique Market Insight

The Asia-Pacific DNA fragmentation technique market is expected to witness rapid growth, driven by expanding genomics research infrastructure, rising healthcare investments, and increasing adoption of precision medicine across countries such as China, India, and Japan. Growing prevalence of genetic disorders and cancer is boosting demand for advanced diagnostic and sequencing technologies. Increasing establishment of genomic research centers and rising outsourcing of clinical research activities are further supporting regional expansion. In addition, growing awareness of fertility diagnostics and molecular testing is accelerating adoption across both clinical and research sectors.

Japan DNA Fragmentation Technique Market Insight

The Japan DNA fragmentation technique market is witnessing consistent growth due to strong investments in life sciences research, advanced healthcare systems, and increasing focus on genomic medicine. Rising adoption of NGS technologies in oncology, reproductive health, and rare disease research is driving demand for precise DNA fragmentation methods. Integration of automated laboratory systems and high-accuracy enzymatic fragmentation technologies is improving workflow efficiency. Furthermore, Japan’s emphasis on personalized medicine and aging population-related healthcare needs is supporting sustained market growth.

China DNA Fragmentation Technique Market Insight

The China DNA fragmentation technique market is growing rapidly, driven by expanding biotechnology investments, large-scale genomic sequencing initiatives, and increasing government focus on precision medicine. Rising adoption of NGS technologies in clinical diagnostics, cancer research, and reproductive health is significantly boosting demand for DNA fragmentation solutions. Continuous advancements in laboratory automation and cost-effective sequencing platforms are accelerating market penetration. In addition, growing investments in domestic biotech companies and research institutions are positioning China as one of the fastest-growing markets globally.

DNA Fragmentation Technique Market Share

The DNA fragmentation technique industry is primarily led by well-established companies, including:

- Illumina, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- QIAGEN (Netherlands)

- Roche Holding AG (Switzerland)

- Bio-Rad Laboratories, Inc. (U.S.)

- Takara Bio Inc. (Japan)

- New England Biolabs, Inc. (U.S.)

- PerkinElmer (U.S.)

- Danaher Corporation (U.S.)

- Beckman Coulter, Inc. (U.S.)

- Oxford Nanopore Technologies plc (U.K.)

- 10x Genomics, Inc. (U.S.)

- BD (U.S.)

- Promega Corporation (U.S.)

- Fluidigm Corporation (U.S.)

- Eppendorf SE (Germany)

- Hamilton Company (U.S.)

- Merck KGaA (Germany)

- Tecan Group Ltd. (Switzerland)

Latest Developments in DNA Fragmentation Technique Market

- In February 2024, Agilent Technologies advanced its SureSelect portfolio by enhancing DNA library preparation and target enrichment workflows, improving fragmentation consistency and sequencing accuracy for applications in oncology research, inherited disease analysis, and large-scale genomic studies across research institutions worldwide

- In June 2023, QIAGEN expanded its QIAseq portfolio to strengthen enzymatic DNA fragmentation and library preparation solutions for next-generation sequencing, supporting improved efficiency in genomic research, oncology profiling, and precision medicine applications through streamlined and standardized sample preparation workflows

- In March 2022, Thermo Fisher Scientific advanced its Ion Torrent sequencing ecosystem by enhancing automated library preparation workflows integrated with enzymatic DNA fragmentation steps, improving turnaround time and accuracy in clinical and translational research sequencing applications across oncology and genetic disease studies

- In January 2022, Illumina expanded adoption support for its Illumina DNA Prep (tagmentation-based library preparation kit), enhancing automation compatibility and workflow efficiency for next-generation sequencing applications, thereby strengthening high-throughput DNA fragmentation and sequencing library preparation capabilities across research and clinical genomics laboratories

- In July 2021, 10x Genomics launched Chromium Single Cell Multiome ATAC + Gene Expression solution enabling simultaneous chromatin accessibility and gene expression profiling using integrated transposase-based DNA fragmentation technology, significantly advancing single-cell multi-omics research and high-resolution genomic analysis workflows across academic and clinical research laboratories

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.