Global Drive By Wire Market

Market Size in USD Billion

USD

31.23 Billion

USD

75.68 Billion

2025

2033

USD

31.23 Billion

USD

75.68 Billion

2025

2033

| 2026 - 2033 | |

| USD 31.23 Billion | |

| USD 75.68 Billion | |

| % | |

|

Drive-by-Wire Market Overview

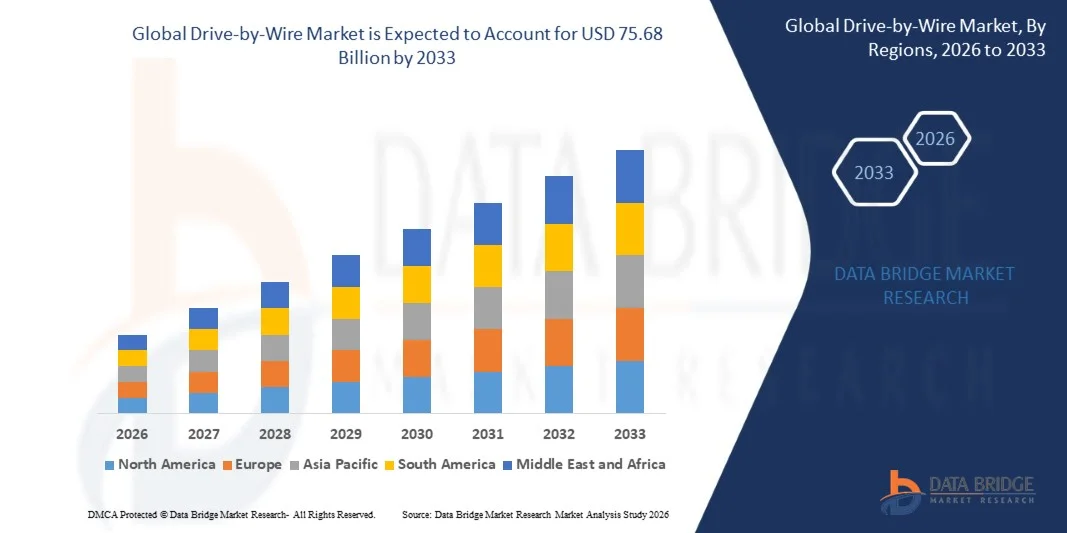

As per Data Bridge Market Research Analysis, the Drive-by-Wire Market was valued at USD 31.23 billion in 2025 and is projected to reach USD 75.68 billion by 2033, growing at a CAGR of 11.70% from 2026 to 2033. Drive-by-wire technology refers to the electronic replacement of traditional mechanical linkages with sophisticated electronic control systems that manage a vehicle's steering, braking, acceleration, and other critical functions. By replacing hydraulic and mechanical components that are prone to wear, drive-by-wire systems enhance vehicle safety, reliability, and performance.

The market is experiencing steady expansion fueled by innovations in automotive electronics, a heightened focus on fuel efficiency, and the rising prevalence of autonomous vehicles. The transition from traditional mechanical linkages to electronic control systems is especially evident in electric vehicles (EVs) and autonomous driving applications, where drive-by-wire technologies facilitate precise control over steering, braking, and acceleration. As vehicles move toward software-defined architectures, regular over-the-air (OTA) updates, and flexible interior and platform designs, drive-by-wire is becoming increasingly important, driving its adoption across passenger and commercial vehicles.

Key Market Trends & Insights

- Asia Pacific emerged as the leading regional market in 2025, driven by high vehicle production volumes, rapid electric vehicle (EV) adoption, and strong expansion of automotive electronics manufacturing across China, Japan, South Korea, and India.

- North America is projected to register the fastest growth in the Drive-by-Wire Market during the forecast period, driven by rapid electrification of vehicles, expansion of autonomous driving trials, and increasing investments in advanced automotive R&D across the U.S. and Canada.

- The Throttle-By-Wire segment dominated the market with a significant share in 2025, as it has achieved widespread adoption across internal combustion engine (ICE), hybrid, and electric vehicles.

- Brake-By-Wire is expected to be the fastest-growing segment during the forecast period, as OEMs shift toward fully electronic and software-defined vehicle architectures that demand faster, more precise, and fail-operational braking control.

- The market is shifting from throttle-by-wire and shift-by-wire systems toward steer-by-wire and integrated chassis-by-wire platforms with advanced redundancy, higher computing capability, and software-defined control.

- Software-defined vehicle architectures are driving drive-by-wire adoption by enabling centralized control, OTA updates, and precise electronic actuation.

- Opportunities are emerging from AI, V2X, and OTA-enabled vehicle control systems.

- Growing production of electric and autonomous vehicles across developing economies, along with rising investments in automotive R&D and smart mobility solutions, will generate significant opportunities for market growth.

Market Size & Forecast

- Global Market Value (2025): USD 31.23 Billion

- Expected Market Value (2033): USD 75.68 Billion

- Forecast CAGR (2026–2033): 11.70%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: North America

Report Scope and Drive-by-Wire Market Segmentation

|

Attributes |

Drive-by-Wire Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Robert Bosch GmbH (Germany) · ZF Friedrichshafen AG (Germany) · Continental AG (Germany) · Nexteer Automotive (U.S.) · Curtiss-Wright Corporation (U.S.) · JTEKT Corporation (Japan) · Denso Corporation (Japan) · Hitachi Astemo, Ltd. (Japan) · NSK Ltd. (Japan) · Thyssenkrupp AG (Germany) · Schaeffler AG (Germany) · Mando Corporation (South Korea) · Hyundai Mobis (South Korea) · Aptiv PLC (Ireland) · Brembo S.p.A. (Italy) · Valeo S.A. (France) · Magna International Inc. (Canada) · Nidec Corporation (Japan) · Mitsubishi Electric Corporation (Japan) · BWI Group (China/Hong Kong) · Showa Corporation (Japan) · CTS Corporation (U.S.) · Infineon Technologies AG (Germany) · Orscheln Products (U.S.) · Panasonic Automotive Systems (Japan) |

|

Market Opportunities |

· Integration of AI, V2X, and OTA-enabled vehicle control systems · Rising demand for steer-by-wire and integrated chassis-by-wire platforms · Expansion of electric and hybrid vehicle production requiring advanced electronic actuation · Development of fail-operational power and communication redundancy architectures · Sensor fusion and zonal E/E systems enabling scalable drive-by-wire functions |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Drive-by-Wire Market Trends

Trend: Software-Defined Vehicle Architectures

Software-defined vehicle architectures are driving drive-by-wire adoption by enabling centralized control, OTA updates, and precise electronic actuation. As vehicles become more software-defined, throttle response, drive modes, and energy management are calibrated through software rather than hardware modifications. This trend is accelerating the transition from mechanical linkages to electronic control systems, as OEMs seek to reduce vehicle weight, improve fuel efficiency, and enable advanced features for autonomous driving. The integration of drive-by-wire systems with software-defined architectures allows for regular OTA updates, flexible interior and platform designs, and centralized electronic architectures. Technological changes such as high-voltage electrical platforms, zonal controllers, fail-operational electronics, and real-time in-vehicle networks are accelerating this transition.

Drive-by-Wire Market Dynamics

Key Market Driver: Growing Adoption of Autonomous Driving Technologies

The growing adoption of autonomous driving technologies is a key factor propelling the demand for drive-by-wire systems. As vehicles increasingly depend on electronic control mechanisms for essential functions, drive-by-wire technology becomes fundamental to achieving higher levels of automation. Autonomous vehicles require precise, software-controlled actuation of steering, braking, throttle, and gear selection, which drive-by-wire systems provide. The integration of drive-by-wire with AI, V2X, and OTA-enabled vehicle control systems is creating new opportunities for market growth. Increasing production of electric and autonomous vehicles across developing economies, along with rising investments in automotive R&D and smart mobility solutions, will generate significant opportunities for market expansion.

Key Restraint/Challenge: High Development Costs and Cybersecurity Concerns

High initial development costs, cybersecurity concerns, system reliability challenges, and complexities related to electronic architecture integration act as market restraint factors for the growth of the drive-by-wire market. Validating safe system behavior across extreme and combined real-world scenarios, synthetically recreating intuitive steering and pedal feedback in the absence of mechanical linkages, and engineering vehicles with fail-operational power and communication redundancy are critical challenges that make drive-by-wire a fundamental shift in vehicle system engineering and the validation process. The threat of cyberattacks and compliance costs also pose significant restraints. These factors create high entry barriers and reinforce Tier-1 concentration in the market.

Key Market Opportunity: Integration of AI and Autonomous Vehicle Validation Platforms

Opportunities are emerging from AI, V2X, and OTA-enabled vehicle control systems. The integration of drive-by-wire with AI-powered vehicle control systems enables predictive and adaptive vehicle responses, enhancing safety and driving experience. V2X communication allows vehicles to share data with infrastructure and other vehicles, enabling coordinated and efficient traffic flow. OTA updates enable continuous improvement and feature enhancement without physical recalls. Growth will also be supported by sensor fusion, fail-operational architectures, zonal E/E systems, and OTA-enabled control software that allow drive-by-wire functions to scale across electric, autonomous, and next-generation vehicle platforms.

Drive-by-Wire Market Scope

The drive-by-wire market is segmented based on type, vehicle type, component, and electric and hybrid vehicle.

- By Type

On the basis of type, the Drive-by-Wire Market is segmented into throttle-by-wire, brake-by-wire, shift-by-wire, steer-by-wire, and park-by-wire. The Throttle-By-Wire segment dominated the market in 2025, as it is the earliest developed, most standardized, and most widely deployed by-wire function across ICE, electric, and hybrid vehicles. Throttle-by-wire allows for precise torque control, smoother acceleration, regenerative braking coordination in hybrids and EVs, and seamless integration with ADAS features such as adaptive cruise control, traction control, and automated emergency braking. The widespread adoption of throttle-by-wire is driven by its ability to meet stringent emission standards while enhancing fuel efficiency and vehicle performance. The Brake-By-Wire segment is expected to be the fastest-growing, driven by OEMs shifting toward fully electronic and software-defined vehicle architectures. Brake-by-wire systems replace conventional hydraulic actuation with electronically controlled braking systems, improving response time, enabling regenerative braking optimization, and supporting higher levels of vehicle automation. The removal of hydraulic components reduces system weight, simplifies packaging, and improves response time, which is critical for ADAS and automated emergency braking. Steer-by-wire eliminates mechanical linkages between the steering wheel and wheels, enabling variable steering ratios and flexible vehicle packaging, and is gaining traction among premium OEMs..

-

By Vehicle Type

On the basis of vehicle type, the Drive-by-Wire Market is segmented into passenger cars and commercial vehicles. Passenger cars represent the largest segment, driven by platform flexibility, repeatable and tunable vehicle driving performance, and architectural advantages in safety redundancy. The growing demand for advanced driver assistance systems and autonomous driving features in passenger vehicles is accelerating the adoption of drive-by-wire technologies. Passenger car OEMs are increasingly integrating throttle-by-wire, brake-by-wire, and steer-by-wire systems to enhance vehicle safety, comfort, and efficiency. Commercial vehicles are also adopting drive-by-wire systems for steering, braking, throttle, and shifting to support electrification, automation, and centralized electronic architectures. The electrification of commercial vehicle fleets, including delivery vans, trucks, and buses, is driving demand for electronic actuation systems that improve operational efficiency and reduce maintenance costs. The adoption of drive-by-wire systems in commercial vehicles depends on validating safe system behavior across extreme scenarios, recreating intuitive feedback, and engineering fail-operational redundancy. Fleet operators are increasingly recognizing the benefits of drive-by-wire technologies in reducing downtime, improving driver comfort, and enabling advanced fleet management capabilities.

-

By Component

On the basis of component, the Drive-by-Wire Market is segmented into electronic control unit (ECU), actuator, feedback motor, sensors, and others. The ECU is the brain of the drive-by-wire system, processing sensor inputs and sending commands to actuators to ensure precise and reliable vehicle control. The ECU integrates complex algorithms for torque management, braking force distribution, and steering assistance, making it a critical component for system performance. Actuators convert electronic signals into mechanical action, enabling precise control over throttle, braking, steering, and shifting functions. Sensors, including throttle pedal sensors, throttle position sensors, pinion angle sensors, hand wheel angle sensors, gear shift position sensors, park sensors, and brake pedal sensors, are critical for system operation and safety. Advancements in sensor technology, including higher accuracy, faster response times, and improved reliability, are driving the adoption of drive-by-wire systems. The development of redundancy architectures, including dual ECUs, backup power supplies, and fail-operational communication networks, is essential for meeting safety requirements in autonomous and semi-autonomous vehicles. Continuous improvements in sensor technology, control algorithms, and power electronics are enabling more sophisticated and reliable drive-by-wire systems across all vehicle types.

-

By Electric and Hybrid Vehicle

On the basis of electric and hybrid vehicle, the Drive-by-Wire Market is segmented into BEV, PHEV, and FCEV. Battery electric vehicles (BEVs) are the largest segment, as drive-by-wire systems are essential for performance and reliability in EVs, enabling precise control over regenerative braking, torque management, and vehicle dynamics. The rapid growth of the BEV market, driven by government incentives, environmental regulations, and consumer demand, is a key factor propelling the adoption of drive-by-wire systems. Plug-in hybrid electric vehicles (PHEVs) also require advanced electronic actuation for optimal performance, combining internal combustion engines with electric motors and regenerative braking systems. Fuel cell electric vehicles (FCEVs) represent a growing segment, with hydrogen-powered vehicles requiring sophisticated electronic control systems for power management and vehicle dynamics.. OEMs are integrating drive-by-wire systems into their electric vehicle platforms to enhance efficiency, reduce weight, and enable advanced driver assistance features. The compatibility of drive-by-wire systems with software-defined vehicle architectures makes them ideal for electric vehicles, which rely heavily on electronic control for battery management, motor control, and energy optimization. As battery technology improves and charging infrastructure expands, the demand for drive-by-wire systems in electric vehicles is expected to grow significantly.

Drive-by-Wire Market Regional Analysis

Asia-Pacific Drive-by-Wire Market Insight

Asia Pacific emerged as the leading regional market in 2025, driven by high vehicle production volumes, rapid electric vehicle (EV) adoption, and strong expansion of automotive electronics manufacturing across China, Japan, South Korea, and India. The region's dominance is attributed to the presence of major automotive manufacturers, increasing investments in EV infrastructure, and growing consumer demand for advanced automotive technologies. China leads the region with its aggressive EV adoption policies and massive automotive production volumes. Japan and South Korea are significant contributors, with their strong automotive electronics manufacturing bases and advanced R&D capabilities. India is emerging as a key growth market, fueled by increasing vehicle production and rising demand for passenger cars.

North America Drive-by-Wire Market Insight

North America is projected to register the fastest growth in the Drive-by-Wire Market during the forecast period, driven by rapid electrification of vehicles, expansion of autonomous driving trials, and increasing investments in advanced automotive R&D across the U.S. and Canada. The United States is at the forefront of drive-by-wire development, with strong adoption of ADAS and automated driving technologies. Key players such as Nexteer Automotive and Curtiss-Wright Corporation are headquartered in the U.S., strengthening the region's market position. The region's strong venture capital funding for automotive technology startups and favorable regulatory environment for autonomous vehicle testing are further accelerating market growth.

Europe Drive-by-Wire Market Insight

Europe represented a significant regional market for drive-by-wire systems, supported by strong regulatory frameworks, stringent safety and emission standards, and high EV adoption rates. The European Union's ambitious targets for EV adoption and the deployment of advanced driver assistance systems are driving market growth. Key players such as Robert Bosch GmbH, ZF Friedrichshafen AG, Continental AG, and Schaeffler AG are headquartered in Europe, strengthening the region's market position. The integration of drive-by-wire with software-defined vehicle architectures, OTA updates, and advanced redundancy systems is shaping the European drive-by-wire landscape. The region's focus on UNECE R79, R155/R156, and ISO 26262 ASIL-D compliance ensures high safety and cybersecurity standards.

Latin America Drive-by-Wire Market Insight

Latin America represented an emerging market for drive-by-wire systems, with growing demand driven by increasing vehicle production, government incentives for EV adoption, and urbanization. Countries such as Brazil and Mexico are witnessing significant investments in automotive manufacturing and EV manufacturing ecosystems. The region's expanding automotive industry and growing awareness of advanced vehicle technologies are driving consumer interest in drive-by-wire systems. However, market growth is currently constrained by limited consumer awareness, higher vehicle costs compared to traditional vehicles, and fragmented regulatory frameworks. The development of regional supply chains and partnerships with global automotive technology providers is expected to accelerate market growth.

Middle East & Africa Drive-by-Wire Market Insight

The Middle East and Africa region represented a nascent market for drive-by-wire systems, with demand primarily concentrated in the GCC countries and South Africa. Governments across the region are increasing investments in electric mobility and advanced automotive technologies to reduce carbon emissions and diversify transportation systems. The UAE is investing in electric mobility, advanced vehicle technologies, and intelligent transportation systems, while Saudi Arabia is expanding EV infrastructure through Vision 2030 initiatives. South Africa is gradually adopting advanced automotive technologies to support the growing demand for passenger vehicles and commercial fleets. Increasing investments from global automotive technology providers are improving technology availability across major urban centers. However, relatively low EV penetration, limited technology awareness, and high costs continue to restrain market growth.

Drive-by-Wire Market Share

The Drive-by-Wire industry is primarily led by well-established companies, including:

- Robert Bosch GmbH (Germany)

- ZF Friedrichshafen AG (Germany)

- Continental AG (Germany)

- Nexteer Automotive (U.S.)

- Curtiss-Wright Corporation (U.S.)

- JTEKT Corporation (Japan)

- Denso Corporation (Japan)

- Hitachi Astemo, Ltd. (Japan)

- NSK Ltd. (Japan)

- Thyssenkrupp AG (Germany)

- Schaeffler AG (Germany)

- Mando Corporation (South Korea)

- Hyundai Mobis (South Korea)

- Aptiv PLC (Ireland)

- Brembo S.p.A. (Italy)

- Valeo S.A. (France)

- Magna International Inc. (Canada)

- Nidec Corporation (Japan)

- Mitsubishi Electric Corporation (Japan)

- BWI Group (China/Hong Kong)

- Showa Corporation (Japan)

- CTS Corporation (U.S.)

- Infineon Technologies AG (Germany)

- Orscheln Products (U.S.)

- Panasonic Automotive Systems (Japan)

Latest Developments in Drive-by-Wire Market

- In January 2026, Nexteer Automotive sponsored a Coalition Meeting of the Automotive Chassis-by-Wire Standards Research Group in China to advance the country's national Steer-by-Wire (SbW) standard. The meeting reflects growing industry collaboration to establish technical frameworks for by-wire systems in the world's largest automotive market.

- In October 2025, Continental AG announced that its Future Brake System roadmap is on track, featuring an integrated brake-by-wire solution that reduces system weight by nearly 30% and enables fully electromechanical dry brake concepts for electrified and automated vehicles. The company's Automotive group was rebranded as Aumovio at Auto Shanghai 2025, with China identified as a priority growth market for software-defined and autonomous vehicle solutions.

- In September 2025, Robert Bosch GmbH showcased its brake-by-wire and steer-by-wire technologies at IAA Mobility 2025 in Munich, projecting cumulative sales of over EUR 7 billion from these businesses by 2032. The company also announced plans to invest several hundred million euros in vehicle motion management software by 2028.

- In September 2025, ZF Friedrichshafen AG demonstrated its production-ready by-wire systems at IAA Mobility 2025, positioning itself among the leading suppliers of steer-by-wire and brake-by-wire solutions with series orders from Chinese, European, and North American manufacturers. ZF's "Chassis 2.0" concept integrates by-wire solutions with rear-axle steering, active damping, and electronic roll stabilization.

- In July 2025, ZF Friedrichshafen AG announced the start of production of its Electric Park Brake in India for a new EV platform, designed to improve efficiency and NVH through a low-drag architecture while adding safety features such as emergency braking, dynamic actuation, pad-wear sensing, and scalability across vehicle segments.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.