Global Driverless Tractors Market

Market Size in USD Billion

USD

1.05 Billion

USD

2.06 Billion

2025

2033

USD

1.05 Billion

USD

2.06 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 1.05 Billion |

Market Size (Forecast Year) |

USD 2.06 Billion |

CAGR |

% |

Major Markets Players |

|

Driverless Tractor Market Size

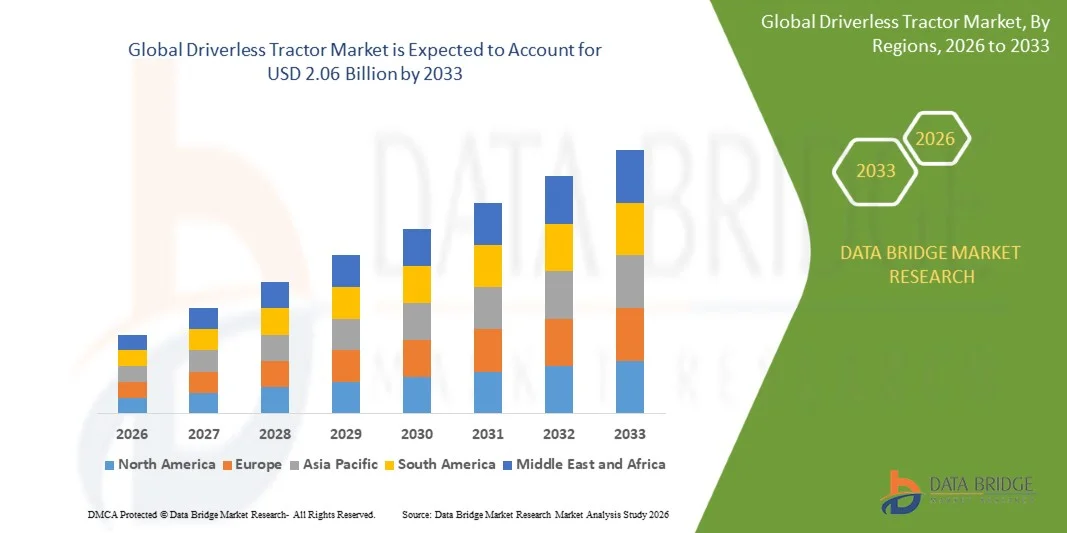

- The global driverless tractor market size was valued at USD 1.05 billion in 2025 and is expected to reach USD 2.06 billion by 2033, at a CAGR of 8.8% during the forecast period

- The market growth is largely fueled by the increasing adoption of precision agriculture and automation technologies in farming operations, leading to improved productivity, reduced labor dependency, and higher operational efficiency across large-scale agricultural activities

- Furthermore, rising labor shortages in the agriculture sector along with the growing need to optimize farming costs and time are accelerating the shift toward autonomous machinery solutions. These converging factors are significantly boosting the adoption of driverless tractors across modern agricultural practices

Driverless Tractor Market Analysis

- Driverless tractors, enabled by advanced technologies such as GPS, sensors, artificial intelligence, and machine vision systems, are becoming essential components of modern agriculture due to their ability to perform autonomous field operations with high accuracy and minimal human intervention

- The escalating demand for driverless tractors is primarily driven by the need for enhanced farm productivity, increasing focus on sustainable farming practices, and the rapid integration of smart farming solutions that improve efficiency and reduce resource wastage

- North America dominated the driverless tractor market with a share of 38.7% in 2025, due to the early adoption of precision agriculture technologies and strong presence of advanced farming infrastructure

- Asia-Pacific is expected to be the fastest growing region in the driverless tractor market during the forecast period due to increasing mechanization of agriculture and rising demand for higher crop productivity across emerging economies

- Sensor segment dominated the market with a market share of 39.1% in 2025, due to its critical role in enabling real-time detection, obstacle avoidance, and operational safety across autonomous farming environments. Sensors such as LiDAR, ultrasonic, and radar systems provide precise field mapping and environmental awareness, which are essential for efficient tractor navigation

Report Scope and Driverless Tractor Market Segmentation

|

Attributes |

Driverless Tractor Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Deere & Company (U.S.) · Tractors and Farm Equipment Limited (India) · Kubota Corporation (Japan) · CLAAS KGaA GmbH (Germany) · AGCO Corporation (U.S.) · CNH Industrial N.V. (U.K.) · Mahindra & Mahindra Ltd. (India) · SDF Group (Italy) · Bucher Industries (Switzerland) · Alamo Group, Inc. (U.S.) |

|

Market Opportunities |

· Expansion of Smart Farming in Emerging Agricultural Economies · Development of Retrofit Solutions for Existing Tractors |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Driverless Tractor Market Trends

“Increasing Integration of AI and Machine Learning in Autonomous Farming Systems”

- A significant trend in the driverless tractor market is the rising integration of AI, machine learning, and autonomous navigation technologies that enable real-time decision-making, field mapping, and precision farming operations. This integration is transforming traditional agricultural machinery into intelligent systems capable of performing complex tasks with minimal human intervention

- For instance, Deere & Company has introduced its autonomous 8R tractor equipped with advanced AI-based vision systems and GPS-guided navigation that allows fully autonomous field operations without onboard drivers. Such developments enhance operational accuracy and improve productivity across large-scale farming environments

- The adoption of sensor fusion and computer vision technologies is increasing rapidly as tractors are now equipped with LiDAR, radar, and camera systems to detect obstacles, crop rows, and terrain variations. This is strengthening the reliability of autonomous systems and enabling safer operations in dynamic agricultural conditions

- The expansion of connected farming ecosystems is further accelerating the use of cloud-based data analytics and IoT-enabled tractors that continuously monitor soil conditions, crop health, and machine performance. This trend is improving decision-making efficiency and enabling predictive agricultural planning

- Manufacturers are increasingly focusing on developing scalable autonomous platforms that can be integrated into existing farm equipment, reducing the need for full fleet replacement. This is supporting faster adoption of driverless tractors across diverse farm sizes and regions

- The growing emphasis on precision agriculture and sustainable farming practices continues to reinforce the importance of automation technologies in agriculture. This is positioning driverless tractors as key enablers of efficient resource utilization, reduced environmental impact, and higher agricultural productivity

Driverless Tractor Market Dynamics

Driver

“Rising Demand for Precision Agriculture and Labor-Saving Solutions”

- The increasing demand for precision agriculture and labor-efficient farming practices is a major driver of the driverless tractor market as farmers seek to improve yield quality while reducing operational costs. Autonomous tractors enable precise planting, fertilizing, and harvesting, minimizing wastage of inputs and improving productivity

- For instance, AGCO Corporation has been actively integrating autonomous technologies into its Fendt tractor lineup to support precision farming and reduce dependence on manual labor in large-scale agricultural operations. Such advancements enhance efficiency and support sustainable farming practices

- The global shortage of agricultural labor is pushing farmers to adopt automated solutions that can perform continuous field operations without human fatigue or interruption. This is significantly increasing the demand for driverless tractors in both developed and emerging agricultural economies

- The need to optimize farm inputs such as water, fertilizers, and pesticides is further driving adoption as autonomous tractors enable targeted application based on real-time field data. This improves cost efficiency and supports environmentally sustainable farming practices

- The continuous expansion of commercial farming and large-scale agricultural operations is reinforcing the need for high-efficiency equipment capable of managing extensive farmland. This is driving sustained growth in the driverless tractor market globally

Restraint/Challenge

“High Initial Investment and Limited Affordability of Autonomous Tractors”

- The driverless tractor market faces significant challenges due to the high initial investment required for purchasing and deploying advanced autonomous farming equipment. The cost of integrating AI systems, sensors, GPS modules, and connectivity infrastructure increases the overall price of these tractors, limiting accessibility for small and medium farmers

- For instance, CNH Industrial has developed advanced autonomous farming solutions under its Case IH brand, but the high cost of these technologically advanced tractors restricts widespread adoption in price-sensitive agricultural markets. This limits penetration in developing regions with smaller farm holdings

- The requirement for supporting digital infrastructure such as high-speed connectivity, data platforms, and maintenance systems further increases total ownership costs. This creates additional financial pressure on farmers adopting autonomous technologies

- Maintenance and software upgrade costs associated with autonomous tractors also contribute to long-term operational expenses, making affordability a key concern for many end-users. This slows down adoption rates despite the potential productivity benefits

- The overall high cost structure combined with uncertain return on investment continues to act as a barrier to mass adoption of driverless tractors. This challenge is slowing down market expansion, particularly in cost-sensitive agricultural economies

Driverless Tractor Market Scope

The market is segmented on the basis of component, power output, technology, crop type, and application.

- By Component

On the basis of component, the driverless tractor market is segmented into sensor, GPS, vision system, and others. The sensor segment dominated the market with the largest revenue share of 39.1% in 2025, driven by its critical role in enabling real-time detection, obstacle avoidance, and operational safety across autonomous farming environments. Sensors such as LiDAR, ultrasonic, and radar systems provide precise field mapping and environmental awareness, which are essential for efficient tractor navigation. Farmers increasingly rely on advanced sensor integration to improve accuracy in field operations and reduce human intervention. The rising focus on precision agriculture and automation further strengthens the demand for high-performance sensor systems in driverless tractors.

The vision system segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by advancements in artificial intelligence and machine learning for image recognition and crop monitoring. Vision systems enable tractors to identify crop rows, detect weeds, and make data-driven decisions in real time, improving productivity and reducing input wastage. Increasing adoption of smart farming practices and computer vision technologies is accelerating the deployment of vision-based autonomous solutions. The growing emphasis on improving yield quality and operational efficiency supports the rapid expansion of this segment.

- By Power Output

On the basis of power output, the driverless tractor market is segmented into >30 H.P., 31 to 80 H.P., and >80 H.P. The 31 to 80 H.P. segment dominated the market with the largest revenue share in 2025, driven by its suitability for a wide range of farming activities across small to medium-sized farms. These tractors offer a balance between power, efficiency, and cost, making them ideal for diverse agricultural operations such as plowing, sowing, and spraying. Farmers prefer this power range due to its versatility and compatibility with various implements. The increasing mechanization of agriculture in developing regions further supports the dominance of this segment.

The >80 H.P. segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising demand for high-capacity machinery in large-scale farming operations. These tractors provide superior performance for heavy-duty applications and large field coverage, improving operational efficiency and reducing time consumption. The expansion of commercial farming and increasing adoption of advanced autonomous equipment are accelerating demand for higher horsepower tractors. The need for improved productivity and scalability in agriculture contributes to the rapid growth of this segment.

- By Technology

On the basis of technology, the driverless tractor market is segmented into fully autonomous tractors, supervised autonomous tractors, and operator assisted autonomous tractors. The supervised autonomous tractors segment dominated the market with the largest revenue share in 2025, driven by its balance between automation and human oversight, ensuring safety and operational control. These systems allow farmers to monitor and intervene when necessary, reducing risks associated with complete automation. The gradual transition toward fully autonomous farming supports the adoption of supervised systems as an intermediate solution. The growing trust in semi-autonomous technologies further reinforces the dominance of this segment.

The fully autonomous tractors segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rapid advancements in artificial intelligence, connectivity, and precision navigation technologies. Fully autonomous systems eliminate the need for human intervention, enabling continuous operations and reducing labor dependency. Increasing labor shortages in agriculture and the push toward smart farming practices are key factors driving adoption. The focus on maximizing efficiency and minimizing operational costs accelerates the expansion of this segment.

- By Crop Type

On the basis of crop type, the driverless tractor market is segmented into cereals & grains, oilseeds and pulses, and fruits and vegetables. The cereals & grains segment dominated the market with the largest revenue share in 2025, driven by the large-scale cultivation of staple crops such as wheat, rice, and corn across major agricultural economies. These crops require extensive field operations, making them suitable for automation through driverless tractors. The need for increased productivity and efficiency in staple crop production supports the adoption of autonomous machinery. The widespread availability of large farming areas further strengthens the dominance of this segment.

The fruits and vegetables segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing demand for high-value crops and precision farming techniques. Autonomous tractors equipped with advanced technologies enable careful handling and precise operations required for sensitive crops. The rising focus on improving yield quality and reducing post-harvest losses contributes to the adoption of driverless solutions in this segment. The shift toward intensive and technology-driven horticulture farming accelerates its growth.

- By Application

On the basis of application, the driverless tractor market is segmented into tillage, harvesting, irrigation, seed sowing, and spraying and fertilizing. The tillage segment dominated the market with the largest revenue share in 2025, driven by its fundamental role in soil preparation and the extensive use of tractors in plowing and land conditioning activities. Autonomous tillage operations enhance efficiency by ensuring consistent depth and coverage, reducing manual effort and time consumption. Farmers prioritize automation in tillage due to its repetitive nature and high labor requirements. The growing adoption of precision farming practices further supports this segment’s dominance.

The spraying and fertilizing segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the increasing need for precise input application and resource optimization. Driverless tractors enable accurate distribution of fertilizers and pesticides, minimizing wastage and environmental impact. The integration of smart technologies and data analytics enhances decision-making in crop management. The rising emphasis on sustainable agriculture and cost efficiency accelerates the growth of this segment.

Driverless Tractor Market Regional Analysis

- North America dominated the driverless tractor market with the largest revenue share of 38.7% in 2025, driven by the early adoption of precision agriculture technologies and strong presence of advanced farming infrastructure

- Farmers in the region increasingly rely on automation to address labor shortages and improve operational efficiency, supported by high investment capacity and widespread awareness of smart farming solutions

- This strong adoption is further supported by government support for agricultural innovation, large-scale farming practices, and the presence of leading technology providers, establishing driverless tractors as a key component of modern agriculture

U.S. Driverless Tractor Market Insight

The U.S. driverless tractor market captured the largest revenue share in 2025 within North America, fueled by the rapid adoption of autonomous farming technologies and increasing focus on improving farm productivity. Farmers are actively investing in advanced machinery to reduce dependency on manual labor and enhance precision in agricultural operations. The presence of major agricultural equipment manufacturers and continuous technological advancements further accelerates market growth. Moreover, the integration of AI, GPS, and IoT in farming equipment is significantly contributing to the expansion of the driverless tractor market.

Europe Driverless Tractor Market Insight

The Europe driverless tractor market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing emphasis on sustainable agriculture and precision farming practices. The region’s strict environmental regulations and focus on reducing carbon emissions are encouraging the adoption of automated farming solutions. European farmers are adopting advanced technologies to optimize resource utilization and improve crop yield. The growing trend of digital farming and smart agriculture is further supporting market expansion across the region.

U.K. Driverless Tractor Market Insight

The U.K. driverless tractor market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing adoption of smart farming technologies and rising need for labor-efficient agricultural solutions. Farmers are increasingly adopting automation to enhance productivity and manage operational costs effectively. The growing awareness regarding precision agriculture and government initiatives supporting agricultural innovation are boosting demand. The presence of advanced digital infrastructure is also contributing to the growth of the market in the country.

Germany Driverless Tractor Market Insight

The Germany driverless tractor market is expected to expand at a considerable CAGR during the forecast period, fueled by strong focus on technological innovation and sustainable farming practices. Germany’s well-established agricultural equipment industry and emphasis on automation are promoting the adoption of driverless tractors. Farmers are increasingly integrating advanced systems to improve efficiency and reduce environmental impact. The rising adoption of precision agriculture technologies further strengthens market growth in the country.

Asia-Pacific Driverless Tractor Market Insight

The Asia-Pacific driverless tractor market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by increasing mechanization of agriculture and rising demand for higher crop productivity across emerging economies. The region is witnessing rapid adoption of smart farming technologies supported by government initiatives promoting digital agriculture and modernization of farming practices, with India emerging as the fastest growing country due to increasing focus on farm automation and labor optimization. Furthermore, expanding agricultural activities, growing population, and rising need for food security are accelerating the demand for autonomous farming solutions, making driverless tractors more accessible across a wider farmer base.

Japan Driverless Tractor Market Insight

The Japan driverless tractor market is gaining momentum due to the country’s advanced technological ecosystem and increasing labor shortages in agriculture. Farmers are adopting autonomous machinery to maintain productivity despite a declining agricultural workforce. The integration of robotics and AI in farming equipment is supporting efficient farm operations. Moreover, Japan’s strong focus on innovation and smart agriculture is driving the adoption of driverless tractors.

China Driverless Tractor Market Insight

The China driverless tractor market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid agricultural modernization and strong government support for smart farming initiatives. The country is investing heavily in advanced agricultural machinery to improve productivity and efficiency. The presence of large-scale farming operations and increasing adoption of automation technologies are key growth drivers. The availability of cost-effective solutions and strong domestic manufacturing capabilities further propel the market in China.

Driverless Tractor Market Share

The driverless tractor industry is primarily led by well-established companies, including:

- Deere & Company (U.S.)

- Tractors and Farm Equipment Limited (India)

- Kubota Corporation (Japan)

- CLAAS KGaA GmbH (Germany)

- AGCO Corporation (U.S.)

- CNH Industrial N.V. (U.K.)

- Mahindra & Mahindra Ltd. (India)

- SDF Group (Italy)

- Bucher Industries (Switzerland)

- Alamo Group, Inc. (U.S.)

Latest Developments in Global Driverless Tractor Market

- In June 2025, John Deere expanded deployment of its autonomous 8R tractor across commercial farms in the U.S., strengthening real-world adoption of driverless farming systems. This expansion reflects a major step toward large-scale commercialization of autonomous tractors, as real farm deployment validates system reliability under varied soil and crop conditions. It reduces farmer hesitation by proving consistent performance in productivity, fuel efficiency, and labor replacement. The development also accelerates market acceptance by showcasing how autonomous tractors can operate continuously with minimal human intervention, improving overall operational scalability and driving stronger demand across large farming enterprises

- In May 2025, China introduced the Honghu T70 fully autonomous electric tractor, marking a major advancement in electric and self-driving agricultural machinery. This launch significantly impacts the market by integrating electrification with full autonomy, addressing both sustainability and labor efficiency challenges in agriculture. It supports reduced carbon emissions while enhancing precision farming capabilities through AI-driven navigation. The introduction of such advanced machinery increases competitive pressure in the market and encourages faster adoption of next-generation autonomous farming equipment, particularly in regions focusing on smart agriculture transformation and environmental sustainability

- In April 2025, John Deere advanced its next-generation autonomous 8R tractor equipped with enhanced AI-based vision and sensing systems. This upgrade strengthens the driverless tractor market by improving machine perception and decision-making accuracy in complex field environments. Enhanced vision systems allow better detection of obstacles, crops, and terrain variations, reducing operational risks and increasing productivity. The integration of advanced AI also supports more efficient task execution such as planting and tillage, thereby improving farm output consistency. This development reinforces trust in autonomous systems and encourages wider adoption among commercial farmers seeking precision and efficiency

- In March 2025, CNH Industrial enhanced its autonomous tractor technology development program focused on scalable automation and retrofit solutions. This initiative positively influences the market by enabling existing tractors to be upgraded with autonomous capabilities, lowering the entry barrier for farmers. It promotes cost-effective adoption of smart farming technologies without requiring full fleet replacement. The scalability aspect supports gradual transition toward automation, making driverless tractors more accessible to mid-sized and small farms. This approach broadens the potential customer base and accelerates overall market penetration of autonomous agricultural solutions

- In February 2025, John Deere continued expansion of its autonomous farming ecosystem through ongoing enhancements in AI-driven navigation and remote operation capabilities. This development improves the efficiency and flexibility of driverless tractors by enabling precise remote monitoring and control of farming operations. It enhances productivity by allowing farmers to manage multiple machines simultaneously while optimizing field operations in real time. The advancement also strengthens connectivity within smart farming ecosystems, improving data-driven decision-making. As a result, it supports higher operational efficiency, reduces dependency on manual labor, and contributes to faster global adoption of autonomous agricultural machinery

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.