Global Drug Delivery In Cancer Market

Market Size in USD Billion

USD

120.05 Billion

USD

230.56 Billion

2025

2033

USD

120.05 Billion

USD

230.56 Billion

2025

2033

| 2026 - 2033 | |

| USD 120.05 Billion | |

| USD 230.56 Billion | |

| % | |

|

Drug Delivery in Cancer Market Size

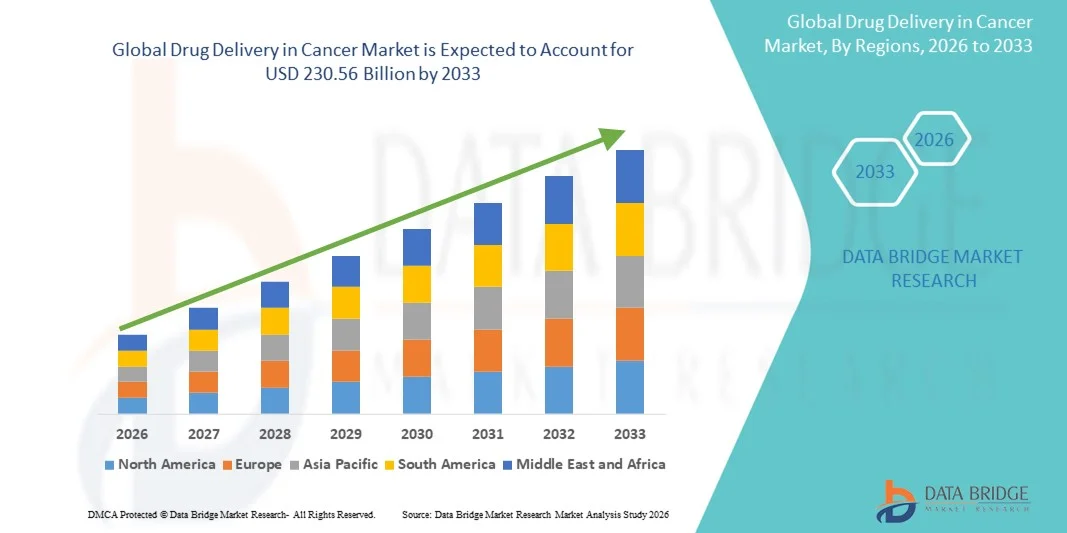

- The global drug delivery in cancer market size was valued at USD 120.05 billion in 2025 and is expected to reach USD 230.56 billion by 2033, at a CAGR of 8.50% during the forecast period

- The market growth is largely fueled by technological progress in targeted drug delivery systems, including protein-drug conjugates, PEGylated proteins, liposomes, and polymer nanoparticles, leading to improved treatment precision and efficacy in cancer car

- Furthermore, increasing demand for safe, efficient, and patient-friendly delivery mechanisms is driving the adoption of advanced drug delivery platforms in clinics and hospitals, accelerating the uptake of cancer therapies and significantly boosting industry growth

Drug Delivery in Cancer Market Analysis

- The Drug Delivery in Cancer market is experiencing strong growth due to rising global cancer prevalence, increasing demand for targeted and personalized therapies, and continuous advancements in drug delivery technologies such as nanoparticles, liposomes, and antibody–drug conjugates, which improve treatment efficacy while minimizing side effects

- The expanding focus on precision medicine, growing investments in oncology research and development, and the increasing number of clinical trials for innovative delivery platforms are significantly accelerating the adoption of advanced cancer drug delivery solutions across healthcare systems worldwide

- North America dominated the drug delivery in cancer market with the largest revenue share of 38.7% in 2025, supported by a well-established healthcare infrastructure, high adoption of advanced oncology treatments, strong presence of leading pharmaceutical and biotechnology companies, and substantial government and private funding for cancer research, with the U.S. contributing the majority share due to early access to novel therapies and clinical innovations

- Asia-Pacific is expected to be the fastest-growing region in the drug delivery in cancer market during the forecast period, registering a strong CAGR of 11.2%, driven by increasing cancer incidence, rising healthcare expenditure, expanding access to modern cancer treatments, improving clinical infrastructure, and growing awareness of early diagnosis and advanced therapeutic options in countries such as China, India, and Japan

- The liposomes segment dominated the largest market revenue share of 38.6% in 2025, driven by its proven ability to improve drug solubility, enhance bioavailability, and reduce the systemic toxicity associated with conventional chemotherapy drugs

Report Scope and Drug Delivery in Cancer Market Segmentation

|

Attributes |

Drug Delivery in Cancer Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Pfizer Inc. (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Drug Delivery in Cancer Market Trends

Advancements in Targeted and Personalized Drug Delivery Systems

- A significant and accelerating trend in the global drug delivery in cancer market is the growing development of targeted and personalized delivery systems, which aim to deliver therapeutic agents directly to cancerous cells while minimizing damage to healthy tissues. This approach is significantly improving treatment efficacy and reducing adverse side effects for patients

- For instance, the increasing adoption of antibody-drug conjugates (ADCs), nanoparticle-based carriers, and liposomal drug formulations is enabling more precise targeting of tumor cells, thereby enhancing the therapeutic index of anticancer drugs

- Advancements in nanotechnology and biomaterial engineering have allowed for the development of drug carriers that can respond to tumor-specific environments such as pH, temperature, and enzyme activity, enabling controlled and site-specific drug release

- These innovations are transforming conventional chemotherapy into more targeted and effective treatment approaches, which is reshaping the overall landscape of cancer treatment

- The growing shift toward precision medicine is further encouraging pharmaceutical companies to invest in the development of customized drug delivery platforms tailored to individual patient profiles and genetic markers

- This trend is fundamentally improving treatment outcomes, patient compliance, and long-term survival rates, making targeted drug delivery systems an essential component of modern oncology therapies

Drug Delivery in Cancer Market Dynamics

Driver

Rising Global Cancer Burden and Increasing Demand for Effective Therapies

- The rapidly increasing prevalence of cancer worldwide, along with the rising mortality rate associated with the disease, is a major driver for the growth of the drug delivery in cancer market

- For instance, in September 2024, several pharmaceutical and biotechnology companies accelerated investments in the development of advanced drug delivery platforms to improve the effectiveness of immunotherapies and chemotherapy drugs

- As the number of cancer patients continues to grow due to factors such as aging populations, lifestyle changes, and environmental exposure, the need for efficient, safe, and responsive drug delivery methods is increasing significantly

- Healthcare providers and patients alike are seeking improved treatment options that enhance drug bioavailability, minimize systemic toxicity, and improve patient quality of life, leading to greater adoption of advanced cancer drug delivery technologies

- Furthermore, growing government initiatives, rising healthcare expenditure, and increasing research funding for oncology treatments are supporting the expansion of cancer drug delivery solutions across both developed and developing region

Restraint/Challenge

High Development Costs and Regulatory Complexities

- The development of advanced drug delivery systems for cancer treatment requires extensive research, complex manufacturing processes, and sophisticated technologies, which significantly increases overall development and production costs

- The high financial investment required for clinical trials, regulatory approvals, and quality assurance can be a major barrier for small and mid-sized pharmaceutical companies entering the market

- For instance, in June 2023, a mid-stage pharmaceutical company faced a delay in the clinical progression of its novel nanoparticle-based chemotherapy delivery system due to additional data requirements requested by regulatory authorities to ensure long-term safety and stability

- Furthermore, the strict and lengthy regulatory approval process for cancer therapies and novel drug delivery platforms can delay product launches and limit rapid market entry

- Ensuring safety, stability, efficacy, and reproducibility of complex delivery systems such as nanoparticles and biomaterial-based carriers presents additional technical challenges

- These factors can restrict access to advanced drug delivery solutions in low-income and price-sensitive regions, where affordability and availability remain significant concerns

- Overcoming these challenges through cost-effective manufacturing techniques, simplified regulatory pathways, and improved clinical validation processes will be essential for sustaining long-term growth in the drug delivery in cancer market

Drug Delivery in Cancer Market Scope

The market is segmented on the basis of type, end user and distribution channel.

- By Type

On the basis of type, the Drug Delivery in Cancer market is segmented into Protein-drug conjugates, PEGylated proteins & polypeptides, Liposomes, Polymer nanoparticles, and Others. The liposomes segment dominated the largest market revenue share of 38.6% in 2025, driven by its proven ability to improve drug solubility, enhance bioavailability, and reduce the systemic toxicity associated with conventional chemotherapy drugs. Liposomal drug carriers allow for targeted delivery to tumor tissues while minimizing damage to surrounding healthy cells, which significantly enhances treatment outcomes. Their extensive use in approved oncology drugs such as liposomal doxorubicin has further strengthened their market position. In addition, liposomes demonstrate excellent biocompatibility and can encapsulate both hydrophilic and hydrophobic drugs, making them highly versatile. The rising incidence of cancer globally and the growing adoption of advanced treatment modalities have also contributed to the widespread use of liposomal delivery systems. Moreover, continuous advancements in liposomal formulation technologies and increased investments from pharmaceutical companies have further solidified the segment’s dominance. Hospitals and oncology centers increasingly prefer liposome-based products due to their improved safety profile and higher patient compliance. The established clinical efficacy of liposomal carriers continues to support strong demand. These factors collectively supported its leading position in the overall market revenue.

The polymer nanoparticle segment is expected to witness the fastest CAGR of 14.2% from 2026 to 2033, owing to its superior ability to deliver drugs with high precision and controlled release profiles. Polymer nanoparticles enable site-specific targeting, prolonged circulation time, and improved drug stability, which significantly enhances therapeutic efficiency in cancer treatment. They are also highly customizable, allowing researchers to engineer particles according to tumor-specific characteristics. The growing focus on personalized medicine and targeted therapies is accelerating the adoption of polymer nanoparticle systems. In addition, increasing R&D activities and collaborations between research institutes and pharmaceutical companies are promoting technological breakthroughs in this segment. Polymer nanoparticles are gaining substantial attention for their application in combination therapies and gene delivery applications. Their potential to overcome multidrug resistance in cancer cells further contributes to their rising demand. Positive clinical trial results and enhanced safety profiles are also fostering acceptance among oncologists. Increased funding for nanotechnology in healthcare continues to boost innovation in this space. These combined factors are expected to drive rapid expansion of this segment during the forecast period.

- By End-Users

On the basis of end-users, the Drug Delivery in Cancer market is segmented into Hospitals, Clinics, and Others. The hospital segment accounted for the largest market revenue share of 46.4% in 2025, primarily due to the high volume of cancer patients receiving treatment in hospital-based oncology departments. Hospitals possess advanced infrastructure, skilled healthcare professionals, and access to modern therapeutic technologies, making them the primary point of care for complex cancer treatments. The availability of chemotherapy, radiation therapy, immunotherapy, and advanced drug delivery systems under one roof further strengthens their dominance. Moreover, the rising prevalence of cancer has significantly increased patient inflows in hospitals worldwide. Hospitals also lead in adopting newly approved and innovative drug delivery systems, as they are better equipped to handle specialized treatments. The presence of government-funded cancer care programs and reimbursement facilities in hospital settings further fuels their growth. Continuous expansion of oncology wards and cancer centers in developed and developing countries alike supports this segment’s strong position. The rising number of inpatient and outpatient visits for cancer treatment has further contributed to increasing hospital revenues. Better monitoring capabilities and immediate access to emergency care also make hospitals a preferred choice for patients. These factors together enabled hospitals to dominate the global market share.

The clinic segment is projected to register the fastest CAGR of 12.9% from 2026 to 2033, driven by the growing shift toward outpatient and ambulatory cancer care services. Clinics provide more accessible and cost-effective treatment options, especially for early-stage diagnosis and follow-up therapies. Increasing establishment of specialized oncology clinics is improving patient access in both urban and semi-urban regions. Clinics are becoming more equipped with advanced drug delivery devices and infusion systems, which is enhancing their role in cancer treatment. The convenience of shorter waiting times and personalized patient care is also driving patient preference. Furthermore, the rising adoption of home-based and near-home treatment models is boosting clinic-based service delivery. Improved awareness regarding early cancer screening is increasing footfall in clinics for initial consultation and therapy. Technological integration in clinics, such as tele-oncology and digital health records, is further enhancing operational efficiency. Supportive government initiatives to strengthen local healthcare networks are also benefitting this segment. Growing investment by private healthcare providers is contributing to the rapid expansion of oncology clinics globally.

- By Distribution Channel

On the basis of distribution channel, the Drug Delivery in Cancer market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The hospital pharmacy segment held the largest market revenue share of 44.8% in 2025, due to the direct integration of pharmacies with oncology departments within hospital settings. Hospital pharmacies are the primary suppliers of chemotherapy drugs and advanced cancer drug delivery systems. They ensure strict control over storage conditions, preparation, and administration, which is crucial for high-potency oncology drugs. These pharmacies are also responsible for dispensing specialized formulations such as liposomes and protein-drug conjugates. The increasing number of hospital admissions for cancer treatments continues to boost demand in this channel. Hospital pharmacies maintain close coordination with physicians, ensuring accurate dosage and real-time treatment adjustments. Their ability to manage bulk procurement also reduces operational delays and ensures uninterrupted availability. Moreover, the rising number of cancer treatment centers globally is leading to the expansion of hospital-based pharmacies. Government and institutional funding further supports this channel. High trust levels among patients and caregivers reinforce its dominance. These combined factors allowed hospital pharmacies to maintain the largest share in this market.

The online pharmacy segment is expected to grow at the fastest CAGR of 15.6% from 2026 to 2033, driven by the increasing adoption of digital healthcare platforms and e-pharmacy services. Patients with chronic conditions, including cancer, are increasingly ordering supportive and prescription medicines through online platforms due to convenience and home delivery services. The expansion of telemedicine and digital prescription systems is further facilitating online procurement. Growing internet penetration and smartphone usage in developing regions are accelerating this trend. Online pharmacies also offer competitive pricing, discounts, and subscription-based delivery models, which attract a large patient base. During and after the COVID-19 pandemic, there has been a significant shift toward contactless delivery of medicines. Enhanced logistics infrastructure has improved the reliability and speed of order fulfillment. Regulatory support and verification mechanisms are increasing consumer trust in online platforms. As more cancer patients seek ease of access to essential medications, online pharmacies are expected to grow rapidly throughout the forecast period.

Drug Delivery in Cancer Market Regional Analysis

- North America dominated the drug delivery in cancer market with the largest revenue share of 38.7% in 2025

- Supported by a well-established healthcare infrastructure, the high adoption of advanced oncology treatments, a strong presence of leading pharmaceutical and biotechnology companies, and substantial government and private funding for cancer research

- The region benefits from early access to novel therapies, continuous clinical innovations, and widespread availability of targeted and personalized drug delivery systems, strengthening its market leadership

U.S. Drug Delivery in Cancer Market Insight

The U.S. drug delivery in cancer market captured the majority revenue share within North America in 2025, driven by its advanced cancer research ecosystem, a high prevalence of cancer cases, and rapid uptake of innovative drug delivery technologies such as antibody–drug conjugates, liposomes, and nanoparticle-based systems. Strong support from the FDA for oncology drug approvals, extensive clinical trial activity, and the presence of major pharmaceutical companies further accelerate market growth. Increasing investments in precision medicine and immuno-oncology are also key contributors to the expanding market in the U.S.

Europe Drug Delivery in Cancer Market Insight

The Europe drug delivery in cancer market is expected to expand at a steady CAGR during the forecast period, supported by rising cancer incidence, strong government funding for healthcare, and growing adoption of advanced treatment modalities. The presence of well-established research institutions and an expanding focus on personalized medicine are driving demand for innovative drug delivery platforms. In addition, favorable reimbursement policies in several countries are encouraging the uptake of advanced cancer therapies.

U.K. Drug Delivery in Cancer Market Insight

The U.K. drug delivery in cancer market is anticipated to grow at a noteworthy CAGR, driven by increasing awareness of early cancer diagnosis, better access to specialized oncology centers, and strong investments in research and development. The National Health Service (NHS) is increasingly integrating advanced drug delivery technologies into cancer treatment protocols, while collaborations between academic institutions and pharmaceutical companies are boosting innovation in the field.

Germany Drug Delivery in Cancer Market Insight

The Germany drug delivery in cancer market is projected to witness considerable growth during the forecast period, owing to its highly developed healthcare infrastructure, robust pharmaceutical industry, and strong focus on biotechnology and precision medicine. The increasing adoption of targeted drug delivery systems, along with rising clinical research initiatives and government support for oncology innovation, continues to strengthen Germany’s position in the European market.

Asia-Pacific Drug Delivery in Cancer Market Insight

The Asia-Pacific drug delivery in cancer market region is expected to be the fastest-growing in the Drug Delivery in Cancer market, registering a strong CAGR of 11.2% during the forecast period. This growth is driven by increasing cancer incidence, rising healthcare expenditure, expanding access to modern cancer treatments, improving clinical infrastructure, and growing awareness of early diagnosis and advanced therapeutic options in countries such as China, India, and Japan. Government initiatives aimed at strengthening cancer care systems and increasing investments in pharmaceutical manufacturing are further accelerating market growth across the region.

Japan Drug Delivery in Cancer Market Insight

The Japan drug delivery in cancer market is gaining significant traction due to its rapidly aging population, increasing cancer burden, and advanced medical technology landscape. The country’s strong emphasis on research and precision medicine has led to a growing adoption of innovative drug delivery methods, including targeted therapies and nanotechnology-based systems. Continuous advancements in clinical infrastructure and rising investment in oncology R&D are further boosting market expansion.

China Drug Delivery in Cancer Market Insight

China drug delivery in cancer market accounted for the largest revenue share in the Asia-Pacific Drug Delivery in Cancer market in 2025, driven by a large patient population, growing middle-class demand for advanced healthcare, and significant government investment in cancer research and treatment facilities. The expansion of domestic pharmaceutical and biotechnology companies, along with increased availability of innovative cancer medicines, is accelerating the adoption of advanced drug delivery systems across the country.

Drug Delivery in Cancer Market Share

The Drug Delivery in Cancer industry is primarily led by well-established companies, including:

• Pfizer Inc. (U.S.)

• Novartis AG (Switzerland)

• Merck & Co., Inc. (U.S.)

• Bristol-Myers Squibb Company (U.S.)

• Johnson & Johnson (U.S.)

• AstraZeneca PLC (U.K.)

• Takeda Pharmaceutical Company Limited (Japan)

• Eli Lilly and Company (U.S.)

• AbbVie Inc. (U.S.)

• Sanofi S.A. (France)

• Bayer AG (Germany)

• Amgen Inc. (U.S.)

• Gilead Sciences, Inc. (U.S.)

• Daiichi Sankyo Company, Limited (Japan)

• Celgene Corporation (U.S.)

• Teva Pharmaceutical Industries Ltd. (Israel)

• 3M Drug Delivery Systems (U.S.)

• Nanobiotix (France)

• Sirtex Medical (Australia)

Latest Developments in Global Drug Delivery in Cancer Market

- In December 2023, Pfizer acquired Seagen, bringing Seagen’s advanced antibody‑drug conjugate (ADC) platform and late-stage oncology pipeline into Pfizer’s fold. This acquisition bolsters Pfizer’s ability to deliver potent cancer payloads directly to tumor cells, accelerating its presence in the rapidly growing ADC‑based cancer therapy space

- In February 2024, AbbVie completed its acquisition of ImmunoGen, gaining access to the ADC mirvetuximab soravtansine (ELAHERE) and leveraging ImmunoGen’s delivery technology. This move strengthens AbbVie’s targeted‑delivery portfolio and underscores the strategic importance of ADCs in modern cancer treatment

- In March 2024, the U.S. FDA granted full approval to mirvetuximab soravtansine (ELAHERE) for certain platinum-resistant ovarian cancer patients, transforming what was previously an accelerated approval into a traditional full approval. The decision was based on robust Phase 3 data, validating the efficacy and safety of this ADC and cementing its role in standard ovarian cancer therapy

- In April 2024, the FDA approved tisotumab vedotin (TIVDAK) for recurrent or metastatic cervical cancer, marking a significant milestone for ADCs in gynecologic oncology. TIVDAK couples a highly potent cytotoxic payload with a targeted antibody, offering a novel delivery‑based therapy for a difficult-to-treat cancer subtype

- In February 2024, the FDA expanded the approved use of liposomal irinotecan (Onivyde) to include a specific pancreatic cancer setting, reflecting the ongoing value of nanoparticle-based delivery systems. Liposomal encapsulation helps maximize drug concentration at the tumor site while reducing systemic toxicity, making it an attractive strategy for hard-to-treat solid tumors

- In May 2024, lisocabtagene maraleucel, a CAR‑T cell therapy, received accelerated FDA approval for follicular lymphoma. This development highlights how engineered living cells are being leveraged as a highly precise drug delivery vehicle, offering durable responses in a subset of cancer patients

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.