Global Echinocandins Market

Market Size in USD Billion

USD

640.66 Billion

USD

990.69 Billion

2025

2033

USD

640.66 Billion

USD

990.69 Billion

2025

2033

| 2026 - 2033 | |

| USD 640.66 Billion | |

| USD 990.69 Billion | |

| % | |

|

Echinocandins Market Size

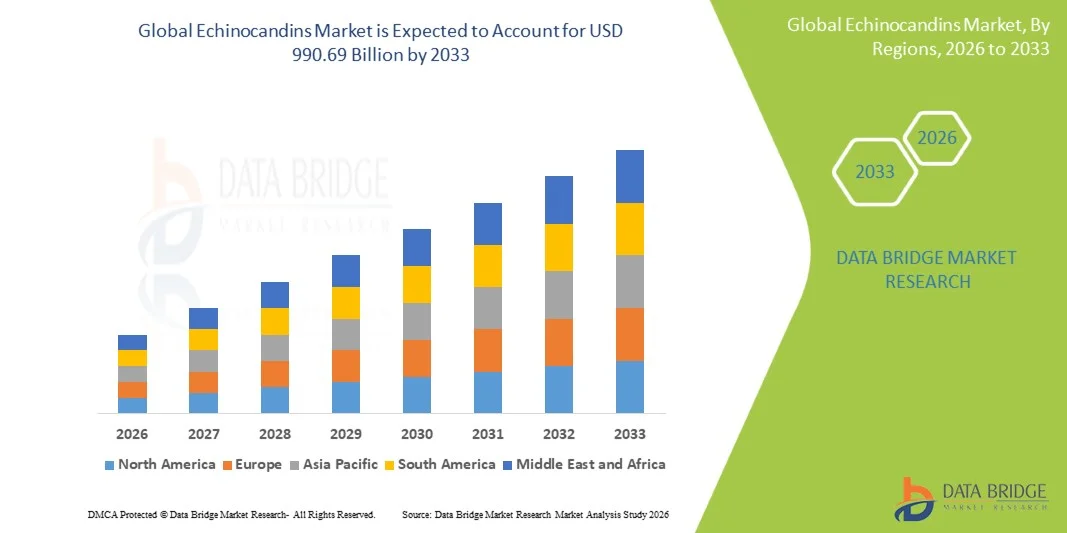

- The global Echinocandins market size was valued at USD 640.66 billion in 2025 and is expected to reach USD 990.69 billion by 2033, at a CAGR of 5.60% during the forecast period

- The market growth is largely fueled by the rising prevalence of invasive fungal infections, increasing immunocompromised patient population, and continuous advancements in antifungal therapies, leading to greater adoption of effective hospital-based treatment solutions across healthcare settings

- Furthermore, growing demand for safe, broad-spectrum, and clinically effective antifungal treatments, increasing incidence of candidemia and aspergillosis, and expanding awareness regarding early infection management are establishing Echinocandins solutions as a preferred option in modern antifungal care. These converging factors are accelerating the uptake of Echinocandins solutions, thereby significantly boosting the industry's growth

Echinocandins Market Analysis

- Echinocandins, a class of antifungal drugs including caspofungin, micafungin, and anidulafungin, are increasingly vital components of modern infectious disease management due to their strong efficacy against invasive Candida and Aspergillus infections and favorable safety profile compared to older antifungal therapies

- The escalating demand for Echinocandins is primarily fueled by the rising incidence of hospital-acquired fungal infections, increasing number of immunocompromised patients (including cancer, transplant, and ICU patients), and growing clinical preference for targeted antifungal therapy with fewer drug resistance concerns

- North America dominated the echinocandins market with the largest revenue share of approximately 42.6% in 2025, characterized by advanced healthcare infrastructure, high awareness of invasive fungal infections, strong hospital infection control practices, and widespread adoption of newer antifungal therapies across major healthcare institutions in the U.S. and Canada

- Asia-Pacific is expected to be the fastest growing region in the echinocandins market during the forecast period due to rising hospital admissions, increasing prevalence of chronic diseases, improving healthcare infrastructure, growing awareness of fungal infections, and expanding access to advanced antifungal treatments across China, India, Japan, and Southeast Asia

- The Injectables segment accounted for the largest market revenue share of 88.2% in 2025, driven by the intravenous administration requirement of echinocandin antifungal drugs for systemic infections

Report Scope and Echinocandins Market Segmentation

|

Attributes |

Echinocandins Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Echinocandins Market Trends

“Rising Demand for Echinocandins in Invasive Fungal Infections”

- A significant and accelerating trend in the global Echinocandins market is the rising incidence of invasive fungal infections (IFIs), particularly in immunocompromised populations such as cancer patients, transplant recipients, and intensive care unit (ICU) patients. This is driving increased clinical reliance on echinocandins as first-line antifungal therapy

- Echinocandins such as caspofungin, micafungin, and anidulafungin are increasingly recommended in treatment guidelines for invasive candidiasis and aspergillosis due to their favorable safety profile and fungicidal activity against Candida species

- For instance, clinical guidelines from major infectious disease societies highlight micafungin as a preferred option for empiric therapy in critically ill patients with suspected candidemia, reflecting its growing acceptance in hospital protocols worldwide

- Growing hospital admissions related to bloodstream infections, along with rising prevalence of chronic diseases and immunosuppressive therapies, are further strengthening demand for advanced antifungal treatment options globally

- In addition, the increasing use of broad-spectrum antibiotics in ICU settings is contributing to secondary fungal infections, further expanding the patient pool requiring echinocandin-based therapies

- This trend is particularly strong in North America and Europe due to advanced healthcare infrastructure, while Asia-Pacific is witnessing rapid growth due to increasing awareness and diagnostic improvements

- Moreover, expanding access to hospital infection surveillance programs and improved laboratory identification of fungal pathogens in emerging economies are enabling earlier diagnosis and timely initiation of echinocandin therapy, thereby supporting market expansion globally

Echinocandins Market Dynamics

Driver

“Rising Incidence of Immunocompromised Patients and Hospital-Acquired Fungal Infections”

- The primary driver of the global Echinocandins market is the increasing number of immunocompromised patients, including those undergoing chemotherapy, organ transplantation, and long-term corticosteroid therapy

- For instance, in 2025, hospitals across the United States reported a continued rise in ICU-associated candidemia cases, reinforcing the need for effective antifungal therapies such as echinocandins

- In addition, the growing burden of hospital-acquired infections (HAIs) and invasive candidiasis is significantly boosting prescription rates of echinocandins as first-line therapy in critical care settings

- Expanding aging population globally, which is more susceptible to infections due to weakened immunity, is also contributing to sustained market growth

- Increasing awareness among clinicians regarding antifungal resistance and the clinical advantages of echinocandins over azoles in certain infections further supports market expansion

Restraint/Challenge

“High Treatment Cost and Emergence of Antifungal Resistance Concern”

- One of the major restraints in the Echinocandins market is the high cost of therapy compared to older antifungal agents such as azoles and polyenes, limiting accessibility in cost-sensitive regions and healthcare systems

- For instance, in several developing countries across Asia and Latin America, limited reimbursement coverage and high per-dose treatment costs restrict widespread adoption of echinocandins in hospital formularies

- In addition, although relatively rare, emerging reports of reduced susceptibility and resistance among certain Candida species (such as Candida glabrata) are raising clinical concerns regarding long-term efficacy

- Limited availability of advanced diagnostic tools in low- and middle-income countries further delays appropriate initiation of echinocandin therapy, impacting patient outcomes

- Addressing these challenges through improved affordability, wider insurance coverage, and strengthened antifungal stewardship programs will be essential for sustained global market growth

Echinocandins Market Scope

The market is segmented on the basis of drug type, application, dosage, route of administration, end-users, and distribution channel.

• By Drug Type

On the basis of drug type, the Echinocandins market is segmented into Caspofungin, Micafungin, and Anidulafungin. The Caspofungin segment dominated the largest market revenue share of 41.6% in 2025, driven by its strong clinical efficacy against invasive fungal infections and widespread first-line use in hospitals. It is extensively used for treating candidemia and esophageal candidiasis, especially in immunocompromised patients. High physician preference and established treatment guidelines further strengthen its dominance. Growing incidence of hospital-acquired fungal infections supports demand. Strong availability in injectable form across hospital settings reinforces market leadership. Increasing global burden of fungal diseases continues to drive usage.

The Micafungin segment is expected to witness the fastest growth rate of 22.3% from 2026 to 2033, driven by its favorable safety profile and broad-spectrum antifungal activity. It is increasingly used in prophylaxis for high-risk patients such as transplant and chemotherapy recipients. Rising awareness regarding early fungal infection management is boosting adoption. Expanding hospital formulary inclusion is further supporting growth. Growing use in pediatric and critical care settings enhances demand. Increasing approvals across emerging markets are accelerating penetration. Continuous clinical research supporting improved outcomes is strengthening segment expansion.

• By Application

On the basis of application, the Echinocandins market is segmented into Esophageal Candidiasis, Candidemia with Invasive Candidiasis, Febrile Neutropenia, Invasive Aspergillosis, and Others. The Candidemia with Invasive Candidiasis segment held the largest market revenue share of 39.8% in 2025, driven by rising hospital-acquired bloodstream infections and high mortality risk associated with invasive fungal infections. Increasing ICU admissions and immunocompromised patient populations are major growth drivers. Echinocandins are widely recommended as first-line therapy for systemic candidiasis. Growing use in tertiary care hospitals supports strong demand. Improved diagnostic capabilities are enabling faster detection and treatment initiation. Expanding healthcare infrastructure is further reinforcing segment dominance.

The Febrile Neutropenia segment is expected to witness the fastest CAGR of 24.5% from 2026 to 2033, driven by increasing cancer prevalence and chemotherapy-induced immunosuppression. Patients undergoing chemotherapy are highly susceptible to fungal infections, increasing prophylactic and therapeutic use of echinocandins. Rising oncology treatment volumes are supporting growth. Improved infection screening protocols in hospitals are boosting early intervention. Expanding cancer care centers are accelerating demand. Growing awareness among oncologists about antifungal prophylaxis is further strengthening adoption. Increasing clinical guidelines recommending echinocandins in high-risk patients support rapid expansion.

• By Dosage

On the basis of dosage, the Echinocandins market is segmented into Injectables and Others. The Injectables segment accounted for the largest market revenue share of 88.2% in 2025, driven by the intravenous administration requirement of echinocandin antifungal drugs for systemic infections. Injectable formulations ensure rapid bioavailability and effective therapeutic response in critically ill patients. Hospital dependency for administration further strengthens demand. Rising ICU admissions and severe fungal infection cases support segment dominance. Strong clinical preference for injectable antifungals reinforces usage. Availability of standardized dosing regimens enhances treatment efficiency. Continuous hospital-based care requirements further drive growth.

The Others segment is expected to witness the fastest CAGR of 21.8% from 2026 to 2033, driven by ongoing research into alternative formulations and extended-release delivery systems. Innovations in antifungal drug delivery are improving patient compliance and treatment outcomes. Growing demand for outpatient-compatible therapies is supporting development. Pharmaceutical companies are investing in novel dosage forms. Increasing focus on reducing hospital stay duration is accelerating adoption. Technological advancements in drug formulation are enhancing efficiency. Expansion of clinical trials continues to support segment growth.

• By Route of Administration

On the basis of route of administration, the Echinocandins market is segmented into Intravenous and Others. The Intravenous segment held the largest market revenue share of 92.4% in 2025, driven by the requirement of direct bloodstream delivery for rapid and effective treatment of invasive fungal infections. IV administration ensures high drug bioavailability and immediate therapeutic action. It is the standard route in hospital and ICU settings. Increasing prevalence of severe fungal infections supports dominance. Strong clinical guidelines recommend intravenous use for echinocandins. Expansion of critical care infrastructure further reinforces segment leadership.

The Others segment is expected to witness the fastest CAGR of 20.9% from 2026 to 2033, driven by research into alternative administration routes such as long-acting formulations and potential oral delivery innovations. Pharmaceutical advancements are focusing on improving patient convenience. Rising demand for home-based antifungal therapy supports development. Clinical trials exploring novel delivery mechanisms are expanding opportunities. Increasing emphasis on reducing hospital dependency is fueling innovation. Growth in outpatient care models is also supporting adoption.

• By End-Users

On the basis of end-users, the Echinocandins market is segmented into Hospitals, Specialty Clinics, Homecare, and Others. The Hospitals segment dominated the largest market revenue share of 68.7% in 2025, driven by high incidence of invasive fungal infections requiring inpatient care and intensive monitoring. Hospitals are primary treatment centers for candidemia and aspergillosis cases. Availability of critical care units and infectious disease specialists strengthens dominance. Increasing ICU admissions and surgical complications support demand. Strong diagnostic infrastructure enables rapid treatment initiation. High adoption of intravenous antifungal therapy further reinforces leadership.

The Specialty Clinics segment is expected to witness the fastest CAGR of 23.1% from 2026 to 2033, driven by rising outpatient management of fungal infections and oncology-related care. Specialty clinics are increasingly managing immunocompromised patients requiring antifungal therapy. Growth in cancer treatment centers is supporting demand. Improved diagnostic access in outpatient settings is accelerating adoption. Rising healthcare decentralization trends are boosting growth. Increasing physician preference for specialized care environments further supports expansion. Expanding private healthcare infrastructure continues to drive segment growth.

• By Distribution Channel

On the basis of distribution channel, the Echinocandins market is segmented into Hospital Pharmacy, Retail Pharmacy, Online Pharmacy, and Others. The Hospital Pharmacy segment accounted for the largest market revenue share of 74.6% in 2025, driven by the direct administration of echinocandin drugs in hospital settings for severe infections. Most prescriptions originate in inpatient departments and ICUs. Strict regulatory handling of antifungal injectables supports hospital-based dispensing. Strong procurement systems in hospitals reinforce dominance. High dependency on controlled drug administration further supports growth. Increasing hospitalization rates for fungal infections strengthen segment leadership.

The Online Pharmacy segment is expected to witness the fastest CAGR of 25.2% from 2026 to 2033, driven by growing digital healthcare adoption and increasing accessibility of pharmaceutical supply chains. Expansion of e-prescription systems is supporting online procurement. Rising awareness of digital health platforms is boosting demand. Improved logistics and cold chain delivery systems enhance feasibility. Growth in remote healthcare services is accelerating adoption. Increasing patient preference for convenience and home delivery supports expansion. Technological advancements in e-pharmacy platforms continue to drive strong growth.

Echinocandins Market Regional Analysis

- North America dominated the echinocandins market with the largest revenue share of 42.6% in 2025, characterized by advanced healthcare infrastructure, high awareness of invasive fungal infections, strong hospital infection control practices, and widespread adoption of newer antifungal therapies across major healthcare institutions in the U.S. and Canada. The region has also witnessed increasing use of echinocandins in treating candidemia, invasive candidiasis, and immunocompromised patient infections in critical care settings

- Healthcare providers in the region highly value the clinical efficacy, safety profile, and targeted antifungal action offered by echinocandins, particularly in hospital-acquired and life-threatening fungal infections. Growing preference for evidence-based antifungal stewardship programs and guideline-driven treatment protocols continues to strengthen market demand

- This widespread adoption is further supported by high healthcare expenditure, strong diagnostic capabilities, increasing ICU admissions, and rising prevalence of immunosuppressive conditions, establishing echinocandins as a favored class of antifungal agents in tertiary care hospitals and specialized treatment centers

U.S. Echinocandins Market Insight

The U.S echinocandins market captured the largest revenue share in 2025 within North America, fueled by high incidence of invasive fungal infections, strong clinical adoption of advanced antifungal therapies, and well-established hospital infection control systems. Physicians are increasingly prioritizing echinocandins such as caspofungin, micafungin, and anidulafungin for first-line and empiric treatment in critically ill patients. The growing preference for hospital-based antifungal stewardship programs, combined with robust demand in oncology wards, transplant centers, and intensive care units, further propels the market. Moreover, increasing integration of rapid diagnostic tools and guideline-based treatment pathways is significantly contributing to market expansion.

Europe Echinocandins Market Insight

The Europe echinocandins market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising hospital-acquired infections, increasing immunocompromised patient populations, and strong regulatory emphasis on infection control. The region’s well-structured healthcare systems and standardized treatment protocols are fostering the adoption of echinocandin therapies. European healthcare providers are also drawn to their safety, efficacy against resistant fungal strains, and suitability for critically ill patients. The market is experiencing significant growth across public hospitals, specialty clinics, and transplant centers, with echinocandins widely incorporated into antifungal treatment guidelines.

U.K. Echinocandins Market Insight

The U.K. echinocandins market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of invasive fungal infections and a strong focus on hospital infection prevention strategies. In addition, rising numbers of immunocompromised patients due to cancer therapies and organ transplants are encouraging broader use of echinocandin antifungals. The UK’s robust NHS infrastructure and evidence-based prescribing practices are expected to continue stimulating market growth.

Germany Echinocandins Market Insight

The Germany echinocandins market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, increasing focus on antimicrobial resistance management, and high demand for advanced antifungal therapies. Germany’s well-developed hospital systems and emphasis on clinical precision promote the adoption of echinocandins in intensive care and infectious disease treatment settings. The integration of antifungal stewardship programs and hospital infection surveillance systems is also becoming increasingly prevalent.

Asia-Pacific Echinocandins Market Insight

The Asia-Pacific echinocandins market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rising hospital admissions, increasing prevalence of chronic diseases, improving healthcare infrastructure, growing awareness of fungal infections, and expanding access to advanced antifungal treatments across China, India, Japan, and Southeast Asia. The region’s growing burden of immunocompromised patients, coupled with expanding critical care facilities, is accelerating demand. Furthermore, increasing government healthcare investments and improved availability of hospital formulary antifungal drugs are making echinocandin therapies more accessible across public and private healthcare systems.

Japan Echinocandins Market Insight

The Japan echinocandins market is gaining momentum due to the country’s advanced healthcare system, aging population, and high incidence of hospital-acquired infections among elderly and immunocompromised patients. Japanese healthcare providers place strong emphasis on infection control and evidence-based antifungal treatment, driving adoption of echinocandins in tertiary hospitals. The integration of advanced diagnostics, antimicrobial stewardship programs, and hospital infection monitoring systems is fueling growth.

China Echinocandins Market Insight

The China echinocandins market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s large patient population, expanding hospital infrastructure, increasing incidence of invasive fungal infections, and rising adoption of advanced antifungal therapies. China’s growing ICU capacity and increasing organ transplant and oncology treatments are further driving demand for echinocandins. Government healthcare reforms, improved hospital access, and strong domestic pharmaceutical production capabilities are key factors propelling market growth.

Echinocandins Market Share

The Echinocandins industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Astellas Pharma Inc. (Japan)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Gilead Sciences, Inc. (U.S.)

- Novartis AG (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

- GlaxoSmithKline plc (U.K.)

- AbbVie Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Cipla Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Sandoz Group AG (Switzerland)

- Fresenius Kabi AG (Germany)

- Hikma Pharmaceuticals PLC (U.K.)

- Viatris Inc. (U.S.)

- Lupin Limited (India)

- Zydus Lifesciences Ltd. (India)

- Baxter International Inc. (U.S.)

Latest Developments in Global Echinocandins Market

- In January 2021, global clinical practice updates reinforced echinocandins (caspofungin, micafungin, and anidulafungin) as first-line intravenous therapies for invasive candidiasis and candidemia, supporting their continued dominance in hospital antifungal treatment protocols. This reaffirmation strengthened demand across critical care and immunocompromised patient settings

- In August 2022, clinical pharmacology reviews highlighted expanding population-based studies on echinocandins, focusing on optimized dosing strategies for micafungin, caspofungin, and anidulafungin in special patient groups such as pediatrics and critically ill patients. This development supported improved precision antifungal therapy

- In March 2023, the U.S. FDA approved rezafungin (Rezzayo), a next-generation echinocandin, for the treatment of candidemia and invasive candidiasis in adults with limited or no alternative options. The approval marked a major innovation milestone in echinocandin-class antifungals due to its long-acting pharmacokinetic profile and once-weekly dosing potential

- In December 2023, rezafungin also received European Medicines Agency (EMA) approval, expanding its availability across Europe for invasive candidiasis treatment. This strengthened the global adoption of next-generation echinocandins in hospital antifungal formularies

- In January 2024, pharmacokinetic and clinical reviews emphasized increasing use of echinocandins in optimized antifungal dosing strategies, particularly in critically ill patients and those with organ dysfunction, highlighting advances in individualized antifungal therapy approaches

- In January 2025, clinical pharmacokinetic studies consolidated evidence on echinocandins (micafungin, caspofungin, anidulafungin, and rezafungin), focusing on dose optimization in special populations and reinforcing their critical role in invasive fungal infection management

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.