Global Eco Friendly Packaging Materials Market

Market Size in USD Billion

USD

191.49 Billion

USD

292.93 Billion

2024

2032

USD

191.49 Billion

USD

292.93 Billion

2024

2032

| 2025 - 2032 | |

| USD 191.49 Billion | |

| USD 292.93 Billion | |

| % | |

|

Eco-Friendly Packaging Materials Market Size

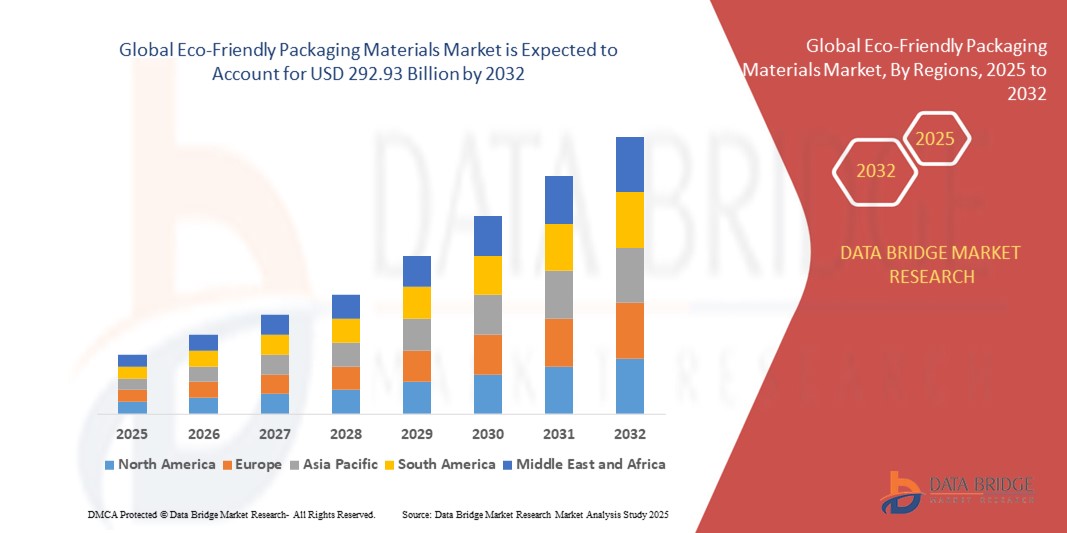

- The global eco-friendly packaging materials market size was valued at USD 191.49 billion in 2024 and is expected to reach USD 292.93 billion by 2032, at a CAGR of 5.00% during the forecast period

- The market growth is largely fuelled by increasing consumer demand for sustainable products, stringent government regulations on plastic usage, and rising adoption of biodegradable and recyclable packaging solutions

- Growing awareness about environmental impact, along with corporate sustainability initiatives, is driving manufacturers to shift toward eco-friendly alternatives such as paper, bioplastics, and compostable materials

Eco-Friendly Packaging Materials Market Analysis

- The market is witnessing significant growth due to increasing consumer awareness regarding environmental sustainability and the harmful effects of conventional plastic packaging.

- Companies across industries are adopting eco-friendly packaging solutions to comply with regulatory requirements, reduce

- Asia-Pacific dominated the eco-friendly packaging materials market with the largest revenue share in 2024, driven by rapid urbanization, increasing environmental awareness, and government initiatives promoting sustainable packaging

- North America region is expected to witness the highest growth rate in the global eco-friendly packaging materials market, driven by technological advancements, high disposable incomes, and the expansion of eco-conscious retail and e-commerce sectors

- The Recyclable segment held the largest market revenue share in 2024, driven by increasing consumer preference for sustainable and circular packaging solutions. Recyclable packaging reduces environmental impact, aligns with government regulations, and supports corporate sustainability initiatives, making it widely adopted across industries

Report Scope and Eco-Friendly Packaging Materials Market Segmentation

|

Attributes |

Eco-Friendly Packaging Materials Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

• Growing Adoption Of Biodegradable And Compostable Packaging |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Eco-Friendly Packaging Materials Market Trends

Rising Adoption of Sustainable and Biodegradable Packaging Solutions

• The growing consumer preference for eco-friendly and biodegradable packaging is transforming the packaging landscape by encouraging manufacturers to adopt sustainable materials. These materials reduce environmental impact, lower carbon footprint, and support corporate sustainability initiatives. Rising consumer advocacy for green products and social media awareness campaigns are further amplifying the adoption of sustainable packaging across industries

• Increasing demand from retail, food & beverage, and e-commerce sectors is accelerating the shift toward compostable, recyclable, and plant-based packaging materials. Businesses are responding with innovative designs and packaging formats that meet consumer expectations for convenience and sustainability. The trend is also driving collaborations between material suppliers and manufacturers to create scalable, eco-conscious packaging solutions

• Technological advancements in bio-based polymers, paper-based packaging, and molded fiber solutions are improving durability, functionality, and aesthetics, making sustainable options competitive with conventional packaging. Continuous R&D in material engineering is helping overcome previous limitations in strength, shelf-life, and barrier properties, broadening application potential

• For instance, in 2023, several global foodservice chains and e-commerce companies introduced biodegradable packaging for takeaway meals and delivery products, boosting consumer adoption and enhancing brand image. The initiatives also fostered customer loyalty and demonstrated corporate commitment to environmental responsibility, reinforcing market credibility

• While demand is rising, continuous innovation in material development, cost-efficiency, and scalable production will be key to sustaining market growth and broader adoption globally. Integration of automated manufacturing techniques and alternative feedstocks is expected to improve profitability and accessibility for small and large enterprises alike

Eco-Friendly Packaging Materials Market Dynamics

Driver

Increasing Environmental Awareness and Regulatory Support

• Growing awareness about plastic pollution and environmental degradation is encouraging both businesses and consumers to adopt eco-friendly packaging alternatives. Governments worldwide are enforcing stricter regulations to curb single-use plastics, which is boosting demand for sustainable packaging. This regulatory push is complemented by voluntary corporate sustainability initiatives, creating a strong multi-stakeholder adoption environment

• The surge in corporate sustainability initiatives and ESG commitments is prompting manufacturers to incorporate recyclable, compostable, and renewable packaging materials across product lines. Companies are leveraging eco-certifications, carbon footprint labeling, and green marketing campaigns to attract environmentally conscious consumers and strengthen brand reputation

• Consumers’ preference for green products and brands with a strong environmental stance is reinforcing market adoption, especially in developed economies with high disposable income and environmental consciousness. Awareness campaigns, influencer marketing, and educational programs are further accelerating consumer-driven demand for sustainable packaging

• For instance, in 2022, several European and North American FMCG companies switched to biodegradable packaging, reducing plastic usage and strengthening brand perception among eco-conscious consumers. These initiatives also prompted suppliers to innovate in renewable materials, contributing to overall market expansion

• While environmental awareness and regulation are driving growth, the industry needs to focus on innovation in materials and processes to maintain competitiveness and meet increasing sustainability standards. Investment in circular economy models and renewable feedstock sourcing is expected to enhance long-term market resilience

Restraint/Challenge

High Production Costs and Material Availability Constraints

• Eco-friendly packaging materials, such as biodegradable plastics, molded fibers, and plant-based polymers, often involve higher production costs compared to conventional plastics, limiting adoption among price-sensitive manufacturers. The cost disparity can slow adoption in emerging economies where profit margins are tight and price competition is high

• Limited availability of raw materials and reliance on agricultural or renewable feedstocks can cause supply inconsistencies and affect scalability, especially in emerging markets with underdeveloped supply chains. Seasonal fluctuations, geopolitical factors, and competition for biomass feedstock can exacerbate supply challenges

• Technological limitations in processing, performance, and durability compared to traditional packaging solutions can restrict use for certain applications, particularly for long shelf-life or heavy-duty products. Continuous R&D is required to improve barrier properties, heat resistance, and moisture protection to meet diverse industry needs

• For instance, in 2023, several SMEs in Asia-Pacific reported challenges in sourcing affordable biodegradable polymers, leading to delays in switching from conventional packaging. The lack of local suppliers also increased reliance on imports, adding logistical and cost pressures

• Addressing cost challenges, improving supply chain infrastructure, and enhancing material performance will be essential for widespread adoption and long-term growth of eco-friendly packaging materials. Strategic partnerships, government incentives, and scaling production through automation are expected to mitigate these barriers

Eco-Friendly Packaging Materials Market Scope

The market is segmented on the basis of type, material type, product type, technique, layer, and application.

- By Type

On the basis of type, the eco-friendly packaging materials market is segmented into Recyclable, Reusable, and Degradable. The Recyclable segment held the largest market revenue share in 2024, driven by increasing consumer preference for sustainable and circular packaging solutions. Recyclable packaging reduces environmental impact, aligns with government regulations, and supports corporate sustainability initiatives, making it widely adopted across industries.

The Reusable segment is expected to witness the fastest growth rate from 2025 to 2032, driven by growing demand for long-lasting, eco-conscious packaging in retail, e-commerce, and foodservice sectors. Reusable packaging reduces single-use waste, offers cost-efficiency over time, and encourages consumer loyalty through innovative designs, particularly in household and commercial applications.

- By Material Type

On the basis of material type, the market is segmented into Paper and Paper Board, Plastic, Metal, Glass, Starch-Based Materials, and Others. Paper and Paper Board held the largest share in 2024, driven by sustainability initiatives and their versatility in packaging various products. These materials are lightweight, cost-effective, and fully recyclable, which supports the circular economy.

Plastic-based eco-friendly packaging is expected to witness the fastest growth rate from 2025 to 2032 due to innovations in biodegradable and compostable polymers. These plastics provide durability, flexibility, and moisture resistance, making them suitable for food, beverages, and pharmaceutical packaging.

- By Product Type

On the basis of product type, the market is segmented into Bags, Pouches and Sachets, Boxes, Containers, Films, Trays, Tubes, Bottles and Jars, Cans, and Others. Bags and pouches held the largest market revenue share in 2024, supported by the e-commerce boom and retail packaging demand. Their lightweight, customizable, and recyclable features make them a popular choice across industries.

Bottles, jars, and containers is expected to witness the fastest growth rate from 2025 to 2032, driven by growing demand for eco-friendly food, beverage, and personal care packaging. Innovations in biodegradable plastics and glass alternatives are further boosting adoption.

- By Technique

On the basis of technique, the market is segmented into Active Packaging, Molded Packaging, Alternate Fiber Packaging, and Others. Molded packaging held the largest market share in 2024 due to its versatility, structural strength, and cost-effectiveness across food, beverage, and consumer goods sectors.

Alternate fiber packaging is expected to witness the fastest growth rate from 2025 to 2032, driven by the demand for paper-based, molded fiber, and biodegradable packaging solutions. These techniques support sustainability goals and reduce reliance on plastics.

- By Layer

On the basis of layer, the market is segmented into Primary Packaging, Secondary Packaging, and Tertiary Packaging. Primary packaging held the largest share in 2024, driven by the widespread need for consumer-facing sustainable solutions in food, beverage, and personal care industries.

Secondary packaging is expected to witness the fastest growth rate from 2025 to 2032 due to the increasing demand for branded, protective, and recyclable packaging in retail and e-commerce channels.

- By Application

On the basis of application, the market is segmented into Food, Beverages, Pharmaceutical, Personal Care, Home Care, and Others. The food segment held the largest market share in 2024, driven by increasing consumer demand for sustainable packaging in ready-to-eat and fresh food products.

Beverages is expected to witness the fastest growth rate from 2025 to 2032 due to stricter regulations on single-use plastics and rising consumer awareness about environmental sustainability.

Eco-Friendly Packaging Materials Market Regional Analysis

• Asia-Pacific dominated the eco-friendly packaging materials market with the largest revenue share in 2024, driven by rapid urbanization, increasing environmental awareness, and government initiatives promoting sustainable packaging

• Consumers and businesses in the region highly value recyclable, reusable, and biodegradable packaging for reducing environmental impact and supporting corporate sustainability goals

• This widespread adoption is further supported by rising disposable incomes, expanding e-commerce and retail sectors, and the emergence of APAC as a manufacturing hub for eco-friendly packaging materials, making solutions more accessible and affordable

China Eco-Friendly Packaging Materials Market Insight

The China eco-friendly packaging materials market captured the largest revenue share in 2024 within Asia-Pacific, fueled by regulatory measures to curb single-use plastics, rising consumer demand for green products, and robust industrial growth. Companies are increasingly introducing paper-based, biodegradable, and compostable packaging solutions to meet sustainability standards and corporate ESG commitments. Furthermore, technological advancements and large-scale production capabilities are enhancing the availability and affordability of sustainable packaging across the country.

Japan Eco-Friendly Packaging Materials Market Insight

The Japan market is expected to witness the fastest growth rate from 2025 to 2032 due to stringent environmental policies, high consumer awareness, and increasing demand for sustainable packaging solutions in food, beverage, and pharmaceutical sectors. Adoption of biodegradable, recyclable, and reusable materials is rising, supported by technological improvements in packaging durability and aesthetics. Japan’s focus on reducing plastic waste and promoting green manufacturing is driving the continued expansion of eco-friendly packaging materials.

North America Eco-Friendly Packaging Materials Market Insight

The North America eco-friendly packaging materials market is expected to witness the fastest growth rate from 2025 to 2032 corporate sustainability initiatives. The U.S. leads the regional market, with widespread adoption of recyclable, reusable, and degradable packaging across retail, food & beverage, and e-commerce sectors. In addition, innovation in molded fiber, paper-based, and bio-based packaging solutions is enhancing functionality and consumer acceptance.

U.S. Eco-Friendly Packaging Materials Market Insight

The U.S. market is expected to witness the fastest growth rate from 2025 to 2032, fueled by government policies targeting single-use plastics, increasing corporate ESG commitments, and strong consumer preference for sustainable packaging. Companies are integrating biodegradable, compostable, and recyclable materials into product packaging, while technological advancements improve durability and visual appeal. The market is further supported by rising demand from foodservice, e-commerce, and retail industries seeking eco-conscious packaging alternatives.

Europe Eco-Friendly Packaging Materials Market Insight

The Europe eco-friendly packaging materials market i is expected to witness the fastest growth rate from 2025 to 2032, driven by stringent EU regulations, growing environmental awareness, and the adoption of sustainable packaging across food, beverage, and personal care sectors. Consumers in the region increasingly prefer brands with environmentally responsible packaging. Innovation in molded fiber, paper-based, and bio-based materials is facilitating wider adoption and meeting both industrial and consumer demands.

U.K. Eco-Friendly Packaging Materials Market Insight

The U.K. market is expected to witness the fastest growth rate from 2025 to 2032, supported by government initiatives promoting sustainability, increasing consumer awareness, and strong retail adoption of recyclable and biodegradable packaging. Businesses are actively incorporating eco-friendly materials such as paperboard, molded fiber, and bio-based plastics to enhance brand image and meet regulatory requirements. In addition, e-commerce growth and ready-to-use sustainable packaging formats are accelerating market penetration.

Germany Eco-Friendly Packaging Materials Market Insight

The Germany market is expected to witness the fastest growth rate from 2025 to 2032, fueled by regulatory support, high environmental consciousness, and adoption of innovative eco-friendly packaging solutions. German companies focus on biodegradable plastics, molded fiber, and paper-based packaging to meet sustainability standards. Integration of eco-friendly packaging across food, beverage, and personal care sectors is further boosting adoption, supported by technological advancements and robust industrial infrastructure.

Eco-Friendly Packaging Materials Market Share

The Eco-Friendly Packaging Materials industry is primarily led by well-established companies, including:

- Mondi (U.K.)

- Segezha group (Russia)

- Klabin SA (Brazil)

- Billerudkorsnas (Sweden)

- Stora Enso (Finland)

- Daio Paper construction (Japan)

- Nordic Paper (Sweden)

- Glatfelter (U.S.)

- Gascogne Papier (Austria)

- Glatfelter Corporation (U.S.)

- Tokushu Tokai Paper Co., Ltd. (Japan)

- Goodwin Robbins Packaging Company Inc. (U.S.)

- Oji Holdings Corporation (Japan)

- CTI Paper USA (U.S.)

- Canfor (Canada)

- Genus Paper and Boards Limited (India)

- Georgia-Pacific (U.S.)

- Canadian Paper packaging Ltd.(Canada)

- Fujian Qingshan Paper Co., Ltd. (China)

- Smurfit Kappa(US)

- WestRock Company (Ireland)

- SCG PACKAGING (Thailand)

- International Paper (U.S.)

Latest Developments in Global Eco-Friendly Packaging Materials Market

- In 2021, ProAmpac, a U.S.-based sustainable packaging company, completed the acquisition of Ultimate Packaging Ltd., a U.K.-based firm specializing in creative packaging solutions. This strategic move expanded ProAmpac’s sustainable product portfolio, enhanced its presence across the U.K., and strengthened its position in the creative food packaging segment. The acquisition allows the company to provide end-to-end support across the supply chain with innovative eco-friendly packaging products, boosting its market competitiveness and driving adoption of sustainable packaging solutions globally

- In 2021, Huhtamaki partnered with RiverRecycle and VTT to develop river waste collection technology, which has been deployed on the Mithi River in India. This initiative aims to address floating river waste, reinforcing Huhtamaki’s sustainability efforts in the Asia-Pacific region, particularly India. The collaboration strengthens the company’s market presence, enhances its eco-friendly image, and supports broader environmental and waste management initiatives in the packaging industry

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Eco Friendly Packaging Materials Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Eco Friendly Packaging Materials Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Eco Friendly Packaging Materials Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.